Halliburton Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Halliburton Bundle

What is included in the product

Evaluates control held by suppliers and buyers, and their influence on pricing and profitability.

Customize pressure levels based on new data or evolving market trends.

What You See Is What You Get

Halliburton Porter's Five Forces Analysis

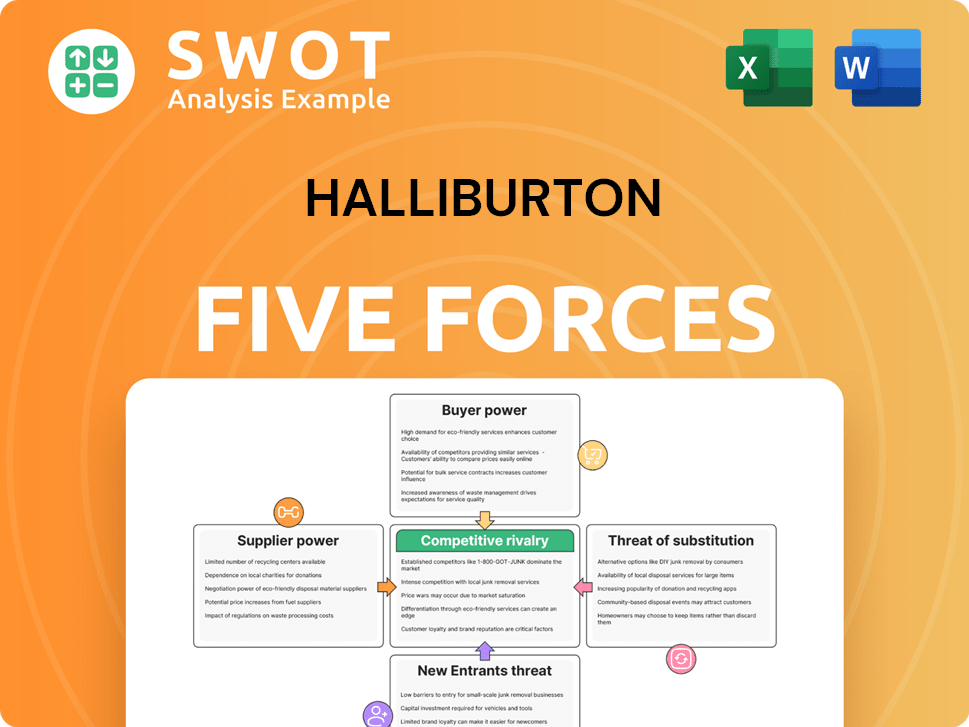

This preview is the complete Halliburton Porter's Five Forces analysis you'll receive. It details competitive rivalry, supplier power, buyer power, threat of substitutes, and threat of new entrants. The document you're viewing is the exact file you'll download instantly after purchase. It's ready for your immediate review and use—no need to wait. This is the full, professionally formatted analysis.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Halliburton faces significant competitive pressures. Buyer power, particularly from large oil companies, is substantial. The threat of new entrants is moderate due to high capital requirements. Bargaining power of suppliers, especially equipment manufacturers, is considerable. Intense rivalry among existing players, like Schlumberger, drives down profit margins. The threat of substitutes is relatively low, though renewable energy poses a long-term challenge.

Ready to move beyond the basics? Get a full strategic breakdown of Halliburton’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited supplier concentration

Halliburton benefits from limited supplier concentration, relying on diverse providers for equipment and services. This broad base strengthens its bargaining position, allowing for competitive pricing and terms. For example, in 2024, Halliburton sourced from over 5,000 suppliers globally. This diversification minimizes supply disruptions, ensuring a stable supply chain.

Standardized components availability

Halliburton benefits from the availability of standardized components. This widespread availability, due to the nature of oilfield services, gives Halliburton leverage. They can switch suppliers easily. For example, in 2024, Halliburton's cost of revenue was about $15 billion, showcasing the impact of supply chain efficiency.

Halliburton's influence on supplier relationships

Halliburton wields substantial power over its suppliers due to its significant market presence. The company's substantial order volumes and the prevalence of long-term contracts bolster its negotiation leverage. In 2024, Halliburton's revenue reached approximately $23 billion, showcasing its substantial buying power. This allows Halliburton to secure advantageous terms, pricing, and service agreements.

Supplier switching costs are low

Halliburton benefits from low supplier switching costs, particularly for standard goods and services. This flexibility reduces supplier power, forcing them to compete for Halliburton's business. Halliburton can easily change suppliers to secure better pricing or terms. This adaptability is crucial in the volatile oil and gas market, allowing Halliburton to react swiftly to market changes. In 2023, Halliburton reported a cost of revenue of $14.9 billion, reflecting its ability to manage supplier costs effectively.

- Halliburton's cost of revenue in 2023 was $14.9 billion, indicating efficient supplier management.

- The ability to switch suppliers reduces dependency and enhances negotiation leverage.

- Standardized products and services further lower switching costs.

- This strategy supports Halliburton's profitability and operational agility.

Potential for backward integration

Halliburton can potentially integrate backward, creating its own manufacturing for vital components. This threat lessens supplier bargaining power, offering Halliburton cost control. Internal production reduces dependence on external suppliers, enhancing its market position.

- In 2024, Halliburton's capital expenditures were approximately $1 billion, reflecting investments in its supply chain and manufacturing capabilities.

- Backward integration can lead to cost savings; for example, sourcing key components internally might reduce costs by 5-10%.

- Halliburton's strategic initiatives include expanding its in-house manufacturing capacity to reduce reliance on external vendors.

Strong Bargaining Power: A Look at the Company's Strategy

Halliburton's diverse supplier base and competitive landscape provide strong bargaining power. The company's substantial revenue ($23B in 2024) and long-term contracts offer leverage. Low switching costs and potential backward integration further weaken suppliers.

| Factor | Impact | Example/Data (2024) |

|---|---|---|

| Supplier Concentration | Low | Sourced from 5,000+ suppliers |

| Switching Costs | Low | Standard components available |

| Market Presence | High | $23B Revenue |

Customers Bargaining Power

Customer concentration exists

Halliburton faces concentrated customers, primarily major E&P companies. These firms, due to their large scale, wield significant negotiating power. This allows them to secure competitive pricing and beneficial contract terms. In 2024, top E&P companies controlled a substantial share of oil and gas production. Their influence directly impacts Halliburton's profitability.

Service commoditization increases buyer power

Service commoditization is rising, boosting buyer power in the oilfield sector. With services becoming more alike, customers prioritize price, squeezing margins. For instance, in 2024, the average price per rig day decreased by 5% due to this pressure. Halliburton needs to innovate to stand out and retain pricing power.

Customers' ability to perform services in-house

Some large Exploration and Production (E&P) companies can do oilfield services themselves, boosting their bargaining power. This in-house capability lets customers threaten to use fewer external service providers. Halliburton must show it's better in expertise, tech, and efficiency to keep their business. In 2024, the oilfield services market was valued at approximately $270 billion.

Access to information empowers customers

Customers' access to information on service pricing and performance benchmarks strengthens their bargaining power. This transparency allows for informed decisions and effective negotiations. Halliburton needs to provide clear value and demonstrate a competitive edge to secure contracts. In 2024, the oilfield services market faced pressure from clients seeking lower costs.

- Service pricing transparency increased due to online platforms.

- Performance benchmarks are readily available, enabling comparisons.

- Customers have more options, increasing negotiation power.

- Halliburton must offer superior value to retain clients.

Impact of long-term contracts

Long-term contracts offer Halliburton predictable revenue, yet they can restrict pricing adjustments in volatile markets. Customers leverage these contracts for favorable terms, especially during market fluctuations. Halliburton must balance contract stability with pricing flexibility. In 2024, Halliburton's revenue was $23 billion, with a significant portion tied to long-term agreements.

- Contract negotiations are critical in the oilfield services sector.

- Halliburton's ability to adapt to price changes is limited by existing contracts.

- Customers' bargaining power is amplified during market downturns.

- Effective contract management is key to sustained profitability.

Customer Bargaining Power Challenges

Halliburton faces strong customer bargaining power due to concentrated clients and commoditization. Customers leverage information and in-house capabilities to negotiate better terms. Long-term contracts impact pricing flexibility, affecting revenue.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Customer Concentration | High negotiation power | Top 10 E&P firms controlled 35% of oil production. |

| Service Commoditization | Price sensitivity | Average rig day rate fell by 5%. |

| Contract Influence | Restricts pricing | 2024 Revenue: $23 billion; significant portion from long-term deals. |

Rivalry Among Competitors

Intense competition among major players

The oilfield services sector is fiercely competitive. Halliburton faces strong rivals, including Schlumberger and Baker Hughes, in 2024. This rivalry pressures pricing and profit margins. To stay ahead, Halliburton must constantly innovate. In Q1 2024, Schlumberger's revenue was $11.9 billion, highlighting the competition.

Pricing pressures and commoditization

Commoditization of services fuels intense pricing pressure, heightening competition. Similar services cause customers to focus on price, resulting in bidding wars and lower profits. Halliburton needs differentiation through technology to avoid price competition. In 2024, Halliburton’s revenue was $23.05 billion, influenced by these pressures.

Market share battles

Companies like Halliburton fiercely compete for market share in the oilfield services industry, often engaging in aggressive bidding and strategic acquisitions. The pursuit of a larger market presence and the benefits of economies of scale fuels this competitive landscape. In 2024, Halliburton's revenue reached approximately $23 billion, highlighting the scale of operations. This intense competition requires Halliburton to meticulously balance its growth aspirations with the critical need to maintain profitability.

Technological innovation as a differentiator

Technological innovation is a major differentiator in the oilfield services sector. Companies that develop advanced technologies gain a competitive edge. Halliburton’s innovation, like its Zeus electric fracking platform, is vital for its position. This focus helps Halliburton compete effectively in a dynamic market. It allows them to offer superior services and stay ahead.

- Halliburton invested $799 million in research and development in 2023.

- Zeus electric fracking platform can reduce emissions by up to 30%.

- Halliburton's revenue from Completion and Production was $6.8 billion in 2024.

Cyclical nature of the industry

The cyclical nature of the oil and gas industry significantly impacts competitive rivalry. During downturns, like the one in 2023-2024, reduced demand triggers intense competition. Companies aggressively pursue fewer projects, often leading to price wars and profit margin declines. For instance, in 2023, Halliburton's revenue decreased due to lower North American activity, highlighting the impact of market cycles.

- Price wars and profit margin declines are common during downturns.

- Halliburton's revenue can be affected by market cycles.

- Companies must adapt strategies to navigate fluctuations.

- Financial resilience is crucial to survive downturns.

Oilfield Giants Clash: Profitability Under Siege

Halliburton faces intense competition from Schlumberger and Baker Hughes, pressuring profit margins in 2024. Commoditization and similar services intensify price wars, requiring technological differentiation. Market share battles and cyclical downturns further exacerbate rivalry, impacting revenue.

| Aspect | Details | Impact |

|---|---|---|

| Key Competitors | Schlumberger, Baker Hughes | Price Pressure |

| Differentiation | Technological Innovation | Competitive Edge |

| Market Dynamics | Cyclical Downturns | Revenue Fluctuations |

SSubstitutes Threaten

Internal service capabilities as substitutes

The threat of substitutes for Halliburton includes internal service capabilities by large oil and gas companies. This shift allows them to perform services in-house, lessening dependence on external providers. For example, in 2024, Chevron expanded its in-house drilling capabilities. Halliburton must highlight its value to counter this trend.

Technological advancements and efficiency gains

Technological advancements pose a threat to Halliburton. Innovations like enhanced drilling technologies can reduce the need for traditional services. For instance, more efficient drilling methods could lower demand for Halliburton's intervention services. Halliburton's ability to integrate these technologies is key to mitigating this threat. In 2024, investment in R&D was $600 million.

Alternative energy sources impact demand

The rise of renewable energy presents a significant threat to Halliburton. Solar and wind power's increasing adoption reduces demand for oil and gas, impacting oilfield services. According to the IEA, global renewable capacity grew by 50% in 2023. Halliburton must diversify to counter this shift.

Enhanced oil recovery techniques

Enhanced oil recovery (EOR) techniques pose a threat to Halliburton by potentially reducing the need for new drilling and specific intervention services. EOR methods can extend the lifespan of existing oil wells, which might lower the demand for Halliburton's services in the long run. This shift requires Halliburton to adapt its service offerings to capitalize on opportunities within the EOR market. Despite challenges, EOR also creates new prospects for Halliburton, such as providing specialized equipment and expertise.

- Global EOR market was valued at $55.8 billion in 2023.

- The EOR market is projected to reach $78.3 billion by 2028.

- Halliburton reported a revenue of $23.05 billion in 2023.

Geopolitical and economic factors

Geopolitical instability and economic downturns significantly threaten Halliburton by reducing oil and gas demand, fostering substitution effects. Economic uncertainty can prompt project delays or cancellations, directly impacting Halliburton's service demand. For instance, in 2024, global oil demand growth slowed due to economic concerns. Halliburton needs to adapt and diversify geographically to counter these risks effectively.

- Geopolitical tensions, like those in the Middle East, can disrupt oil supply and demand.

- Economic slowdowns in major economies (China, Europe) can curb energy consumption.

- Increased adoption of renewable energy sources acts as a substitute.

- Halliburton's diversification efforts into less volatile markets are critical.

Substitutes Threaten Oilfield Services

The threat of substitutes for Halliburton is multifaceted. Key substitutes include in-house services by oil companies, advancements in drilling technology, and the growth of renewable energy, all impacting demand. Halliburton's need to innovate and diversify is crucial.

| Substitute | Impact | 2024 Data |

|---|---|---|

| In-house Services | Reduced reliance on external providers | Chevron expanded drilling capabilities. |

| Technological Advancements | Lower demand for traditional services | R&D investment: $600M in 2024. |

| Renewable Energy | Reduced oil and gas demand | Global renewable capacity +50% in 2023. |

Entrants Threaten

High capital expenditure requirements

The oilfield services sector demands substantial capital investment in specialized gear, tech, and infrastructure, acting as a barrier. Acquiring and keeping up with this equipment can be expensive, hindering new entrants. Halliburton's established infrastructure and scale give it an edge. In 2024, Halliburton's capital expenditures totaled approximately $1.1 billion.

Specialized knowledge and expertise

The oilfield services sector demands specific expertise, making entry challenging. New entrants struggle against established players like Halliburton. Building a skilled team and tech is costly and time-consuming. Halliburton's 2024 revenue was roughly $23 billion, highlighting its market strength. This expertise provides a strong barrier.

Stringent regulatory environment

The oil and gas sector faces stringent regulations, increasing entry costs and complexity. New entrants must invest heavily in compliance and acquire specialized expertise. Halliburton benefits from its established regulatory navigation. In 2024, the industry faced increased environmental standards, raising operational costs by up to 15%.

Established customer relationships

Halliburton benefits from established customer relationships, a significant barrier against new competitors. These deep ties with major oil and gas firms offer a competitive edge new entrants struggle to match. Trust and credibility, earned over time, solidify Halliburton's position. The company's reputation and proven track record are key differentiators. In 2024, Halliburton's revenue was $23 billion, highlighting the strength of its customer relationships.

- Halliburton's long-term contracts provide revenue stability.

- Customer loyalty reduces the risk of market share erosion.

- Existing relationships often lead to repeat business.

- New entrants face high costs to build similar networks.

Economies of scale and scope

Halliburton's massive size gives it significant advantages. It benefits from economies of scale and scope, allowing it to offer various services affordably. New companies struggle to match Halliburton's cost structure due to their smaller scale. This makes it tough for them to compete on price.

- Halliburton operates in over 70 countries, showcasing its global presence.

- In 2023, Halliburton's revenue was approximately $23 billion.

- Its diversified service portfolio includes drilling, evaluation, and production.

- New entrants face high capital expenditure requirements to compete.

Oilfield Services: Barriers to Entry

New entrants in the oilfield services sector face tough barriers. High upfront costs for equipment and technology pose a significant challenge. Established firms like Halliburton benefit from economies of scale and established market positions, making it difficult for new competitors to gain traction. The regulatory landscape and Halliburton's established customer relationships also create obstacles.

| Factor | Impact | Data |

|---|---|---|

| Capital Requirements | High initial investment | Halliburton's 2024 CapEx: ~$1.1B |

| Expertise & Tech | Need for specialized skills | Industry R&D spending: ~5-10% of revenue |

| Customer Relationships | Established ties hard to break | Halliburton's 2024 Revenue: ~$23B |

Porter's Five Forces Analysis Data Sources

Our Halliburton analysis utilizes data from SEC filings, industry reports, and financial databases to assess competition.