Corebridge Financial Bundle

How has Corebridge Financial evolved since its inception?

Corebridge Financial, a major player in retirement solutions and insurance, has a fascinating past. Its journey began long before its 2022 IPO, tracing back to its roots within American International Group (AIG). Understanding the Corebridge Financial SWOT Analysis is key to grasping its current market position.

From its early days as SunAmerica Holdings Inc. to its current status, the Corebridge Financial story is one of strategic adaptation and growth. This AIG spinoff Corebridge has become a significant insurance company and financial services provider. Examining the Corebridge history reveals valuable insights into its mission and future direction, including its recent financial performance and strategic focus on the U.S. retirement market.

What is the Corebridge Financial Founding Story?

The story of Corebridge Financial, a prominent player in the financial services sector, begins with a rich history connected to American General Corporation. American General was established on March 8, 1926, by Gus Sessions Wortham in Houston, Texas. This early foundation laid the groundwork for what would eventually become Corebridge Financial.

The entity that would become Corebridge Financial was initially incorporated on December 3, 1998, in Delaware, under the name SunAmerica Holdings Inc. Over the years, it went through several name changes, including SunAmerica Inc., AIG SunAmerica Inc., and SAFG Retirement Services, Inc., before adopting the name Corebridge Financial, Inc. on March 28, 2022.

The modern inception of Corebridge Financial stems from AIG's strategic decision in 2020 to spin off its life and retirement insurance business. This move allowed AIG to concentrate on its core property and casualty insurance operations. Kevin Hogan, formerly the CEO of AIG's life insurance division, continues to lead Corebridge as its CEO. For more information about the company, you can check out the Revenue Streams & Business Model of Corebridge Financial.

Key Milestones in Corebridge Financial's Founding

Corebridge Financial's journey includes significant milestones that shaped its current status as an independent entity.

- In July 2021, Blackstone Group acquired a 9.9% stake in the new unit for $2.2 billion in cash.

- Blackstone and AIG also formed a long-term asset management agreement for a significant portion of AIG's life and retirement portfolio.

- The company officially launched on September 15, 2022, with an initial public offering (IPO) on the New York Stock Exchange under the ticker symbol 'CRBG.'

- The IPO raised $1.68 billion, marking the largest U.S. IPO of 2022 at that time.

- The IPO priced 80 million common shares at $21 per share.

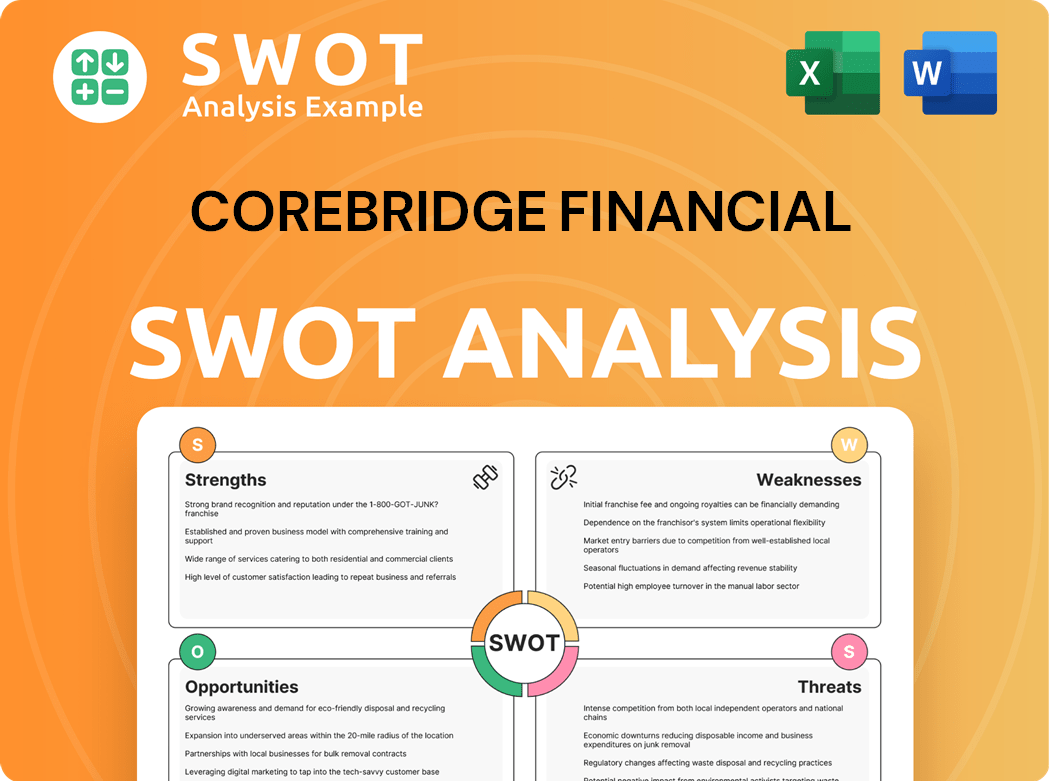

Corebridge Financial SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of Corebridge Financial?

The early growth and expansion of Corebridge Financial, following its spin-off from AIG, have been marked by strategic initiatives. These efforts aimed to strengthen its market position within the U.S. retirement solutions and insurance products sector. Corebridge Financial quickly established itself as a key player, managing or administering over $400 billion in client assets as of December 31, 2024.

In its IPO year, 2022, Corebridge Financial reported revenue of $9.1 billion and a net income of $1.3 billion. The company's adjusted after-tax operating income for 2024 reached $2.9 billion, with operating EPS at $4.83, an 18% increase year-over-year. Premiums and deposits for the full year 2024 were $41.7 billion, reflecting significant top-line growth.

Corebridge has focused on broadening its product offerings and distribution networks. A notable example is the introduction of the MarketLock RILA product in October 2024, which generated $260 million in sales during the first quarter of 2025. The company rebranded its direct-to-consumer life insurance business from AIG Direct to Corebridge Direct in July 2024 to streamline access to life insurance.

Strategic partnerships have played a crucial role in Corebridge's growth. Agreements with Blackstone and BlackRock were established to manage certain annuity assets. Nippon Life Insurance Company acquired an equity interest in Corebridge Financial from AIG for $3.8 billion in 2024, bolstering its capital base and market presence.

Despite a net loss of $664 million in Q1 2025, Corebridge reported a strong adjusted after-tax operating income of $649 million for the same period. The company's holding company liquidity stood at $2.4 billion as of March 31, 2025, and it returned $454 million to shareholders in Q1 2025, including $321 million of share repurchases. For more information on the company's values, please read about the Mission, Vision & Core Values of Corebridge Financial.

Corebridge Financial PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in Corebridge Financial history?

The Corebridge Financial, following its separation from AIG, has achieved significant milestones in the financial services sector. The Corebridge history is marked by strategic moves and market adaptations, solidifying its position as a key player in the insurance and retirement solutions market. The AIG spinoff Corebridge has been a pivotal moment for the company.

| Year | Milestone |

|---|---|

| September 2022 | Successful Initial Public Offering (IPO), raising $1.68 billion, the largest U.S. IPO of the year, and becoming a publicly traded company on the New York Stock Exchange. |

| July 2024 | Rebranded its direct-to-consumer life insurance business to Corebridge Direct, aiming for a simpler approach to life insurance. |

| April 2024 | Completed the sale of its UK life insurance business to Aviva plc, focusing on U.S. life and retirement products. |

Corebridge Financial has consistently introduced innovative products and services to meet evolving market demands. These innovations have helped the insurance company maintain a competitive edge and expand its market reach.

MarketLock RILA Launch

In October 2024, Corebridge Financial launched its MarketLock Registered Index-Linked Annuity (RILA). This product positioned the company as the largest annuity seller offering products in every major category, generating $260 million in sales in Q1 2025.

Corebridge Direct Rebrand

In July 2024, the company rebranded its direct-to-consumer life insurance business to Corebridge Direct. This move aimed to simplify the approach to life insurance, making it more accessible to consumers.

Bermuda Reinsurance Strategy

Corebridge Financial is expanding its Bermuda reinsurance strategy as part of its capital management toolkit. This involves ceding additional reserves to strengthen its financial position and manage risk effectively.

Despite its successes, Corebridge Financial has faced several challenges, particularly in the financial performance area. These challenges have led to strategic adjustments and a focus on financial stability within the financial services sector.

Net Loss in Q1 2025

In the first quarter of 2025, Corebridge Financial reported a net loss of $664 million. This was a significant downturn compared to the net income of $878 million in the prior year quarter.

Decline in Premiums and Deposits

Premiums and deposits decreased by 12% in Q1 2025 compared to the strong performance in Q1 2024. This decline reflects the impact of market conditions and strategic shifts.

Impact of Realized Losses

The net loss was primarily attributed to higher realized losses, including those from the Fortitude Re funds withheld embedded derivative, and an unfavorable change in the fair value of market risk benefits. These factors impacted the company's financial outcomes.

Strategic Capital Management

Corebridge Financial is actively managing its capital, including returning $454 million to shareholders in Q1 2025. This includes $321 million in share repurchases, demonstrating confidence in the company's financial health.

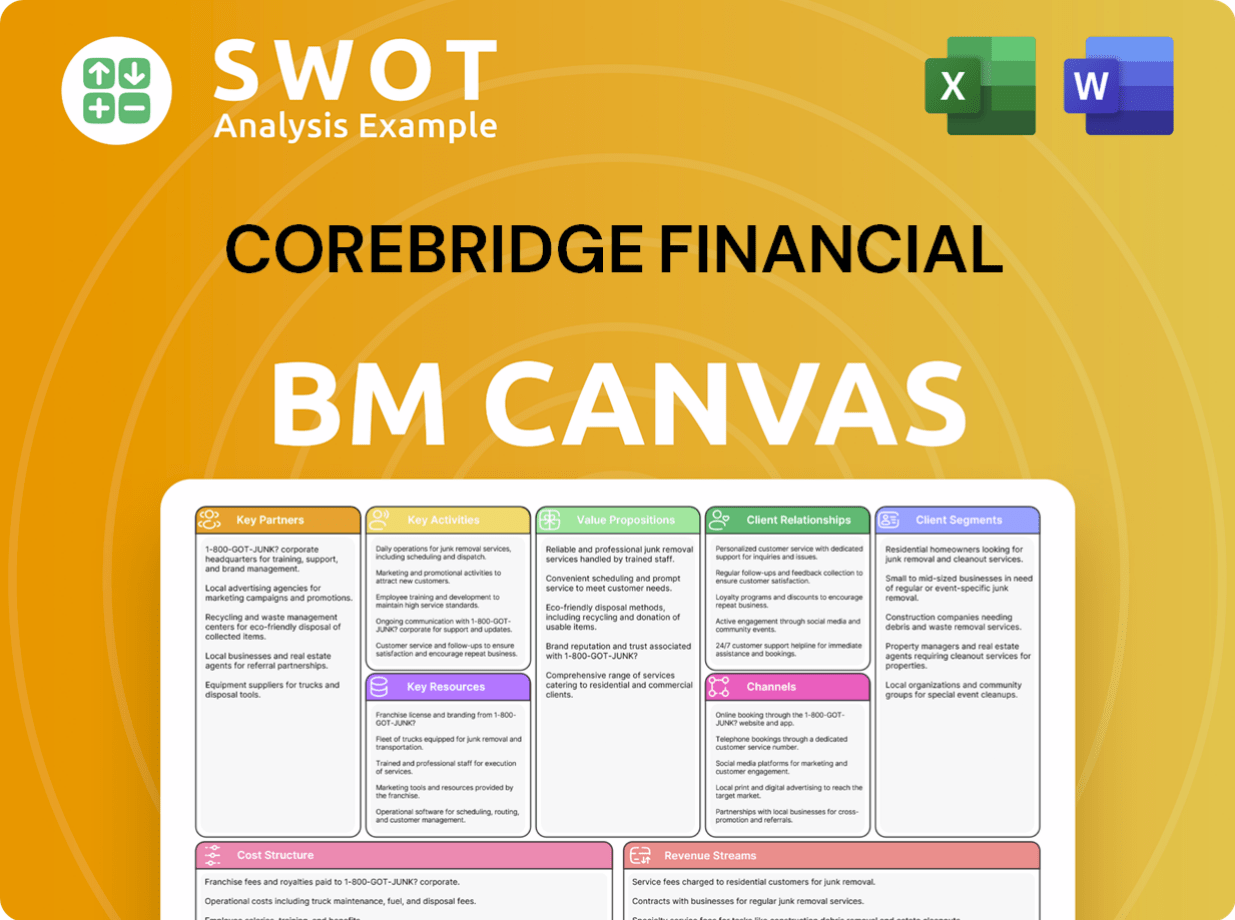

Corebridge Financial Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for Corebridge Financial?

The Corebridge Financial journey is marked by significant milestones, from its inception to its current status as a major player in financial services. This evolution includes name changes, strategic shifts, and key financial moves that have shaped its identity.

| Year | Key Event |

|---|---|

| 1926 | American General Corporation, a predecessor to Corebridge, was founded on March 8 in Houston, Texas. |

| 1998 | Corebridge Financial was incorporated on December 3 as SunAmerica Holdings Inc. in Delaware. |

| 2020 | AIG announced plans to spin off its life and retirement business, which would become Corebridge Financial. |

| 2021 | Blackstone Group acquired a 9.9% stake in the new unit for $2.2 billion in July. |

| 2022 | The company officially changed its name to Corebridge Financial, Inc., on March 28. |

| 2022 | Corebridge Financial launched its Initial Public Offering (IPO) on the NYSE on September 15, raising $1.68 billion. |

| 2023 | Corebridge sold its subsidiary, AIG Life Limited (AIG Life UK), to Aviva for £460 million and Irish health insurer Laya Healthcare to AXA for €650 million. |

| 2024 | In April, Corebridge completed the sale of its UK life insurance business to Aviva plc, focusing on U.S. life and retirement products. |

| 2024 | The direct-to-consumer life insurance business, AIG Direct, was renamed Corebridge Direct in July. |

| 2024 | In September, the Corebridge brand name replaced AIG on the America Tower of the American General Center, its headquarters. |

| 2024 | Corebridge launched its MarketLock RILA (Registered Index-Linked Annuity) product in October. |

| 2024 | Nippon Life Insurance Company acquired an equity interest in Corebridge Financial from AIG for $3.8 billion in December. |

| 2025 | Corebridge reported full-year 2024 net income of $2.2 billion and operating EPS of $4.83, representing an 18% increase year-over-year. |

| 2025 | In Q1, Corebridge reported a net loss of $664 million but adjusted after-tax operating income of $649 million and operating EPS of $1.16. |

Corebridge Financial is strategically positioned to capitalize on the aging U.S. population and the sustained need for retirement solutions. This trend is anticipated to continue through 2029, offering significant growth opportunities.

The company focuses on organic growth, balance sheet optimization, expense efficiencies, and active capital management. Capital-efficient product offerings and reinsurance strategies are key areas of focus for expansion.

Corebridge aims to maintain its positive momentum, leveraging its strategic differentiators and favorable market dynamics. Leadership is committed to generating shareholder and client value, especially in uncertain markets.

Analysts highlight Corebridge's strategic focus on the U.S. retirement market and initiatives to enhance capital efficiency and product offerings as drivers for future growth. Adapting to the evolving retirement landscape is crucial.

Corebridge Financial Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of Corebridge Financial Company?

- What is Growth Strategy and Future Prospects of Corebridge Financial Company?

- How Does Corebridge Financial Company Work?

- What is Sales and Marketing Strategy of Corebridge Financial Company?

- What is Brief History of Corebridge Financial Company?

- Who Owns Corebridge Financial Company?

- What is Customer Demographics and Target Market of Corebridge Financial Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.