BancFirst Bundle

Can BancFirst Maintain Its Momentum in a Changing Financial World?

BancFirst, a cornerstone of Oklahoma's financial landscape, has consistently demonstrated robust growth since its inception. From its humble beginnings in 1985 to becoming the largest state-chartered bank in Oklahoma, BancFirst's journey is a testament to strategic vision and community focus. Now, with assets reaching $14.0 billion as of March 31, 2025, the question remains: what are BancFirst's BancFirst SWOT Analysis and future prospects?

This analysis delves into BancFirst's BancFirst growth strategy, examining its expansion plans, technological advancements, and financial outlook. We'll explore its BancFirst market position within the competitive banking sector and assess its BancFirst financial performance. Understanding the company's commitment to its 'super community bank' model is key to evaluating its BancFirst strategic planning and long-term growth potential.

How Is BancFirst Expanding Its Reach?

The BancFirst growth strategy is primarily driven by strategic expansion initiatives, focusing on both acquisitions and organic growth within its established markets. This approach aims to strengthen its market position and enhance its financial performance. The company's strategic planning includes a 'super community bank' model that allows for decentralized management, enabling quick responses to local customer needs.

A key element of BancFirst's expansion involves strategic acquisitions. The most recent announcement is the agreement to acquire American Bank of Oklahoma, a community bank with approximately $385 million in total assets. This acquisition is expected to close in the third quarter of 2025. This acquisition is a part of BancFirst's mergers and acquisitions strategy. Furthermore, the company has a history of successful acquisitions, such as Worthington National Bank in February 2022, for $77.70 million, and The First National Bank and Trust Company of Vinita in 2021.

The company's operational model supports its expansion strategy by empowering local offices to make decisions. BancFirst currently operates in 59 communities across Oklahoma with 106 banking locations. Additionally, Pegasus Bank has three locations in Dallas, Texas, and Worthington Bank operates five locations in the Dallas-Fort Worth Metroplex area. These locations are instrumental in customer acquisition strategies.

BancFirst continues to expand through strategic acquisitions, such as the planned acquisition of American Bank of Oklahoma. These acquisitions are a key part of BancFirst's expansion plans Oklahoma. The company's mergers and acquisitions strategy has been a consistent driver of growth.

BancFirst is focused on expanding its presence in Oklahoma and the Dallas-Fort Worth Metroplex. The company's market position benefits from its strong local presence. BancFirst's community involvement programs also play a role in its market position.

The 'super community bank' model enables BancFirst to respond effectively to local customer needs. This decentralized approach provides substantial autonomy in credit and pricing decisions. This model supports the company's customer acquisition strategies.

BancFirst focuses on enhancing its comprehensive suite of banking services. These services include commercial, real estate, energy, agricultural, and consumer lending. The company's investment in technology supports its digital banking initiatives.

Key Expansion Initiatives

BancFirst's expansion strategy is multi-faceted, encompassing acquisitions, organic growth, and service enhancements. The company's long term growth potential is significant due to its strategic approach. The impact of interest rates is a key factor in BancFirst's financial results review.

- Strategic Acquisitions: Acquiring community banks to expand its geographical footprint.

- Organic Growth: Leveraging its existing network to attract new customers and deepen relationships.

- Service Enhancements: Improving its banking services, including lending and deposit options.

- Technological Investments: Improving the digital banking experience.

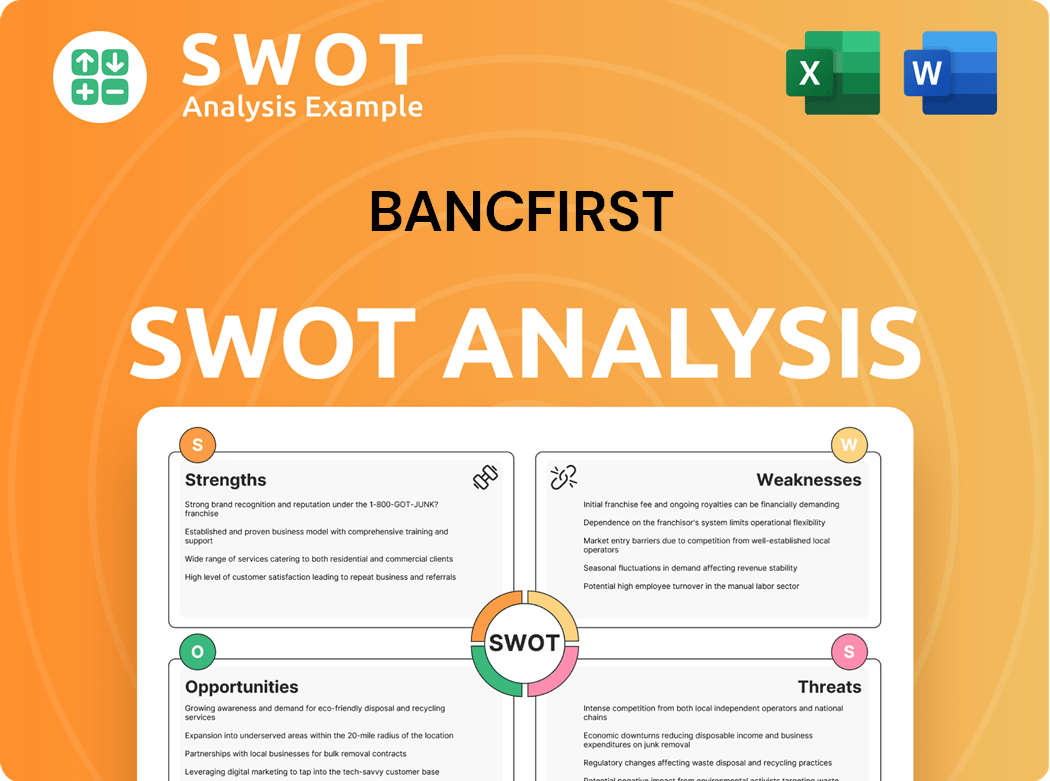

BancFirst SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does BancFirst Invest in Innovation?

The innovation and technology strategy of BancFirst plays a crucial role in its sustained growth and future prospects. The company strategically leverages technology to enhance its service offerings and improve operational efficiency. This approach supports its 'super community bank' model, which balances local responsiveness with centralized functions.

BancFirst's focus on digital transformation is evident through its online banking and bill payment services. This commitment allows the company to meet evolving customer needs and preferences in the digital age. The strategic use of technology is integral to maintaining a competitive edge in the financial services market.

The company's approach involves centralizing processing, support, and investment functions to achieve consistency and operational efficiencies. This centralization includes crucial control functions such as operations support, bookkeeping, accounting, loan review, compliance, and internal auditing. These functions are vital for effective risk management in a technology-driven environment, ensuring stability and reliability.

Digital Banking Services

BancFirst offers online banking and bill payment services, reflecting its commitment to digital transformation. These services are designed to meet the evolving needs of customers who desire convenient and accessible banking options. This focus is crucial for maintaining a competitive position in the market.

Centralized Operations

Centralization of functions like operations support, bookkeeping, and compliance is a key aspect of BancFirst's strategy. This approach ensures consistency and efficiency across the organization. It also helps manage risks effectively in a technology-driven environment.

Specialized Financial Services

BancFirst provides specialized financial services that require unique expertise. These services are supported by the company's centralized operations, ensuring quality and efficiency. This approach allows the company to meet diverse customer needs.

Flexible Home Loan Program

The Flexible Home Loan Program (FHLP) demonstrates an innovative approach to serving diverse customer needs. This program uses more accommodative terms for minority loan applicants. It highlights the company's commitment to community involvement.

Adaptation to Technological Changes

BancFirst acknowledges the need to adapt to technological changes in the financial services industry. This adaptation is viewed as both a challenge and a necessity. The company's focus on efficient back-office functions suggests an internal application of technology to streamline processes.

Internal Application of Technology

The emphasis on efficient back-office functions and integrated services suggests an internal application of technology. This approach streamlines processes and supports its community banking model. It ensures operational efficiency and supports sustained growth.

BancFirst's strategy includes a focus on adapting to technological changes, which is crucial for its long-term growth potential. While specific details on cutting-edge technologies like AI or IoT for external customer-facing platforms aren't extensively publicized, the emphasis on efficient back-office functions and integrated services suggests an internal application of technology to streamline processes and support its community banking model. For more insights into the company's structure and ownership, you can explore Owners & Shareholders of BancFirst. This approach is essential for navigating the evolving financial landscape and maintaining a competitive edge. BancFirst's commitment to innovation and technology is a key factor in its ability to meet customer needs and drive future success.

Key Technological Initiatives

BancFirst focuses on digital banking, centralized operations, and internal technology applications to enhance efficiency and customer service. These initiatives support the company's 'super community bank' model, which emphasizes local responsiveness with centralized functions.

- Digital Banking: Online banking and bill payment services provide convenient access for customers.

- Centralized Operations: Streamlines processes and ensures consistency across the organization.

- Internal Technology: Supports efficient back-office functions and integrated services.

- Flexible Home Loan Program: Uses accommodative terms for minority loan applicants.

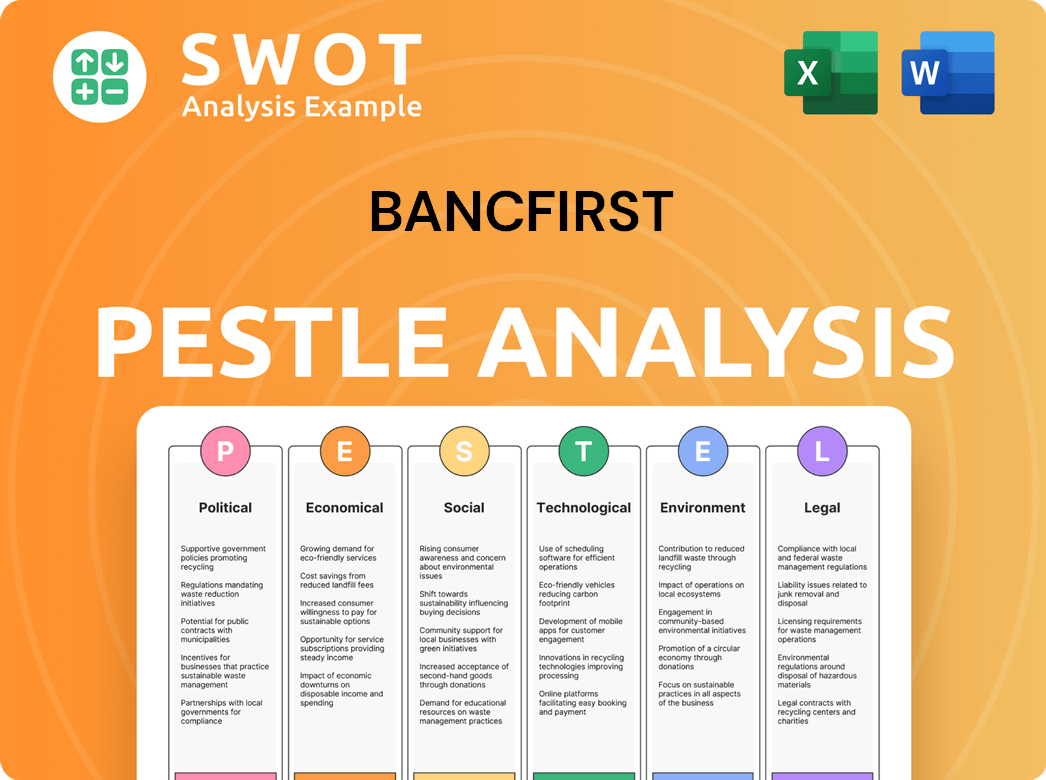

BancFirst PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is BancFirst’s Growth Forecast?

The financial outlook for BancFirst Corporation is positive, with consistent growth and strategic initiatives driving its performance. The company's ability to increase net interest income and maintain a strong net interest margin highlights its effective management and market position. These factors contribute to the overall BancFirst growth strategy and support its long term growth potential.

For the fiscal year ending December 31, 2024, BancFirst reported a net income of $216.4 million, or $6.44 diluted earnings per share. This represents an increase from $212.5 million, or $6.34 per diluted share, in 2023. The company's strategic planning includes a focus on expanding its loan portfolio and managing its deposit base effectively, which has led to increased net interest income.

Looking ahead to 2025, BancFirst's financial performance remains robust. The first quarter of 2025 saw a net income of $56.1 million, or $1.67 per diluted share, surpassing the $50.3 million, or $1.50 per diluted share, reported in Q1 2024. This sustained performance is a key indicator of the company's BancFirst future prospects and its ability to navigate the financial landscape.

In 2024, BancFirst achieved a net income of $216.4 million, or $6.44 per diluted share. This represents a slight increase from the $212.5 million, or $6.34 per diluted share, reported in 2023. The increase was driven primarily by higher net interest income and effective cost management.

BancFirst's Q1 2025 results showed continued strength, with a net income of $56.1 million, or $1.67 per diluted share. This is a significant increase compared to the $50.3 million, or $1.50 per diluted share, reported in Q1 2024. The growth was supported by a steady net interest margin of 3.70%.

As of March 31, 2025, BancFirst's total assets reached $14.0 billion, reflecting a $483.7 million increase from December 31, 2024. Loans grew by $69.6 million to $8.1 billion, and deposits increased by $408.2 million to $12.1 billion during the same period. The company's total stockholders' equity was $1.7 billion as of March 31, 2025.

BancFirst plans to continue regular dividend payments in 2025, backed by anticipated positive net income. The company's dividend payout ratio of 25.5% in 2024 indicates ample room for future increases, with a forward dividend yield of 1.69% as of April 2025. This underscores BancFirst's commitment to shareholder value and financial stability.

The company's strategic focus on managing its loan portfolio and deposit base, along with its investment in technology, supports its BancFirst market position and future expansion plans. For a deeper understanding of BancFirst's customer base and market approach, consider reading about the Target Market of BancFirst.

Revenue Growth Analysis

BancFirst's revenue growth is primarily driven by increased net interest income, supported by higher loan volumes and overall growth in earning assets. The net interest margin has remained stable, showcasing effective financial management.

Impact of Interest Rates

BancFirst's performance is influenced by interest rate fluctuations. The company manages its interest rate risk through various strategies, including adjusting loan and deposit rates to maintain profitability. The company's financial results review shows resilience in managing these impacts.

Digital Banking Initiatives

Investment in technology and digital banking initiatives is a key component of BancFirst's strategic planning. These investments aim to enhance customer experience, improve operational efficiency, and support customer acquisition strategies. This includes improvements in mobile banking and online services.

Loan Portfolio Performance

The performance of BancFirst's loan portfolio is a critical factor in its financial results. The company focuses on maintaining a diversified loan portfolio and employing robust risk management approaches to mitigate potential credit risks. BancFirst's loan portfolio performance is a key indicator of its overall financial health.

Mergers and Acquisitions Strategy

BancFirst may consider mergers and acquisitions as part of its growth strategy to expand its market presence and enhance its service offerings. This strategic approach supports the company's long term growth potential and competitive landscape.

Risk Management Approach

BancFirst employs a comprehensive risk management approach to safeguard its financial stability. This includes managing credit risk, interest rate risk, and operational risks. The company's strong risk management approach helps ensure its continued success.

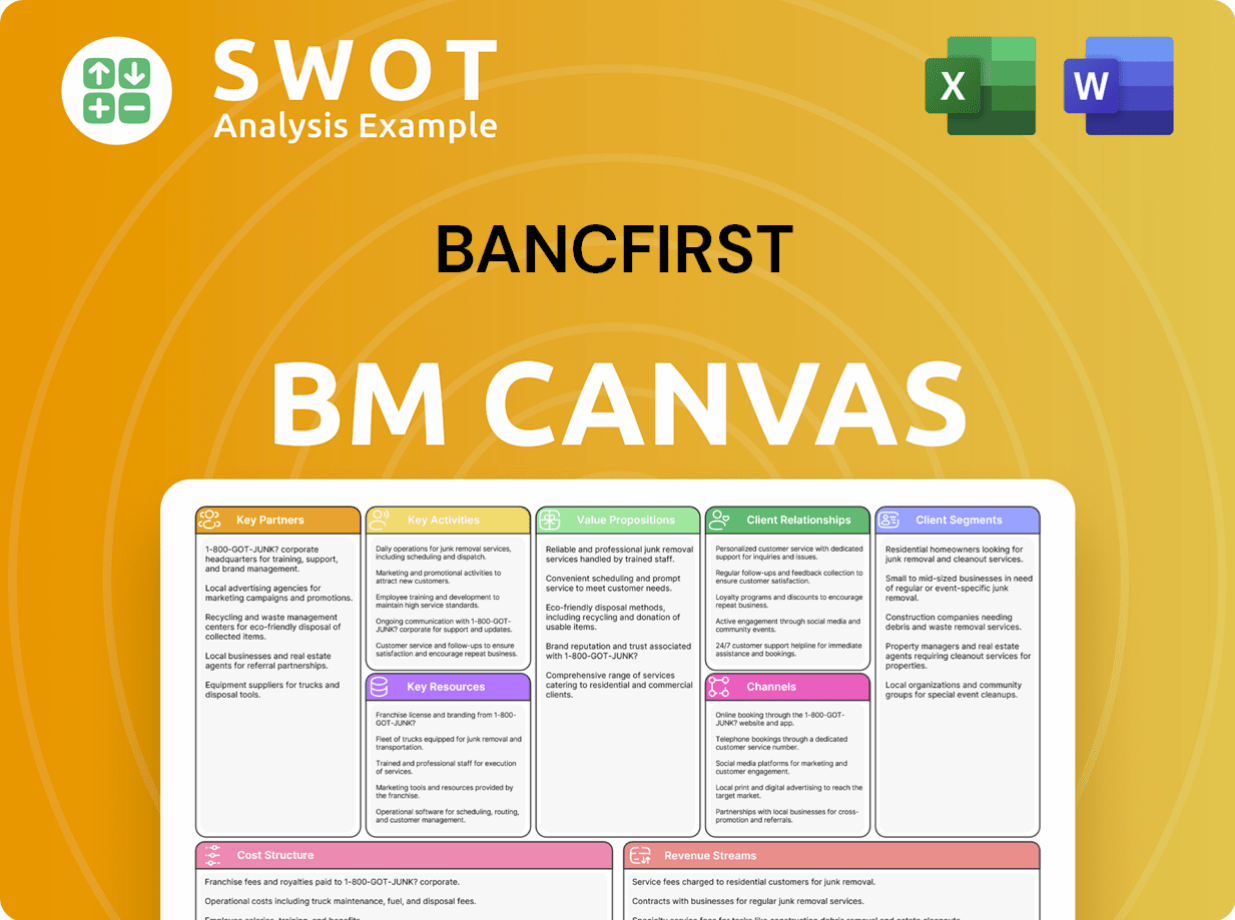

BancFirst Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow BancFirst’s Growth?

The BancFirst growth strategy faces several potential risks and obstacles that could influence its future prospects. The competitive banking landscape, especially in Oklahoma and North Texas, presents a significant challenge. Furthermore, interest rate fluctuations and credit risks tied to its loan portfolio are key concerns.

Regulatory changes and compliance costs also pose considerable challenges. The company's financial performance is subject to economic downturns, particularly impacting credit quality and loan demand. Adapting to technological advancements and evolving customer expectations is crucial for sustained growth.

The company's ability to maintain its market position and achieve its strategic planning goals depends on effectively managing these risks. The increasing likelihood of an economic slowdown, as noted by CEO David Harlow, adds further complexity to the outlook for 2025.

Competitive Pressure

The banking sector in Oklahoma and North Texas is highly competitive, involving local, regional, and national financial institutions. This competition can affect interest rates, fees, and service quality. Strong competition can limit BancFirst's ability to expand and maintain profitability, influencing its BancFirst market position.

Interest Rate Fluctuations

Changes in market interest rates directly impact the company's net interest margin, posing a significant risk to profitability. Rising interest rates can increase funding costs and potentially reduce loan demand. Conversely, falling rates can compress margins, influencing BancFirst financial performance.

Credit and Lending Risks

BancFirst's substantial real estate loan portfolio exposes it to credit and lending risks. Market downturns can adversely affect this portfolio, leading to increased loan defaults and charge-offs. Economic volatility, especially in the energy sector, may influence loan demand and credit quality, impacting BancFirst loan portfolio performance.

Regulatory Risks

The company faces extensive regulation by federal and state authorities, increasing compliance costs. Changes in laws and regulations could limit business operations. For instance, a $4.4 million expense was incurred in Q1 2025 due to the Volcker Rule. These regulatory pressures affect BancFirst strategic planning.

Customer Concerns

Recent bank failures and negative media attention have heightened customer concerns, potentially affecting deposit levels. Maintaining customer trust is crucial for financial stability and growth. Addressing these concerns is vital for BancFirst customer acquisition strategies and retention.

Efficiency Ratio

The company's efficiency ratio was above 55% in Q1 2025, with banks generally aiming for ratios below 50%. A high efficiency ratio indicates higher operating costs relative to revenue, potentially impacting profitability. Improving this ratio is essential for optimizing BancFirst financial results review.

CEO David Harlow has expressed caution due to the increasing likelihood of an economic slowdown, which could impact credit quality. A downturn could lead to higher loan defaults and reduced demand for financial products. Managing credit risk and adjusting lending practices are critical for navigating potential economic challenges, influencing BancFirst long term growth potential.

Adapting to technological changes and digital banking initiatives is crucial. Investment in technology is necessary to remain competitive and meet evolving customer expectations. Failure to embrace digital transformation could lead to a loss of market share. This impacts BancFirst digital banking initiatives and overall competitiveness.

Volatility in the energy sector, especially in Oklahoma and Texas, can influence loan demand and credit quality. Economic fluctuations in this sector can affect the company's loan portfolio performance. BancFirst must closely monitor and manage its exposure to the energy sector.

The company may face challenges in its BancFirst mergers and acquisitions strategy. Integrating acquired entities, managing cultural differences, and achieving expected synergies can be complex. Successful execution of M&A activities is critical for expansion and market share growth.

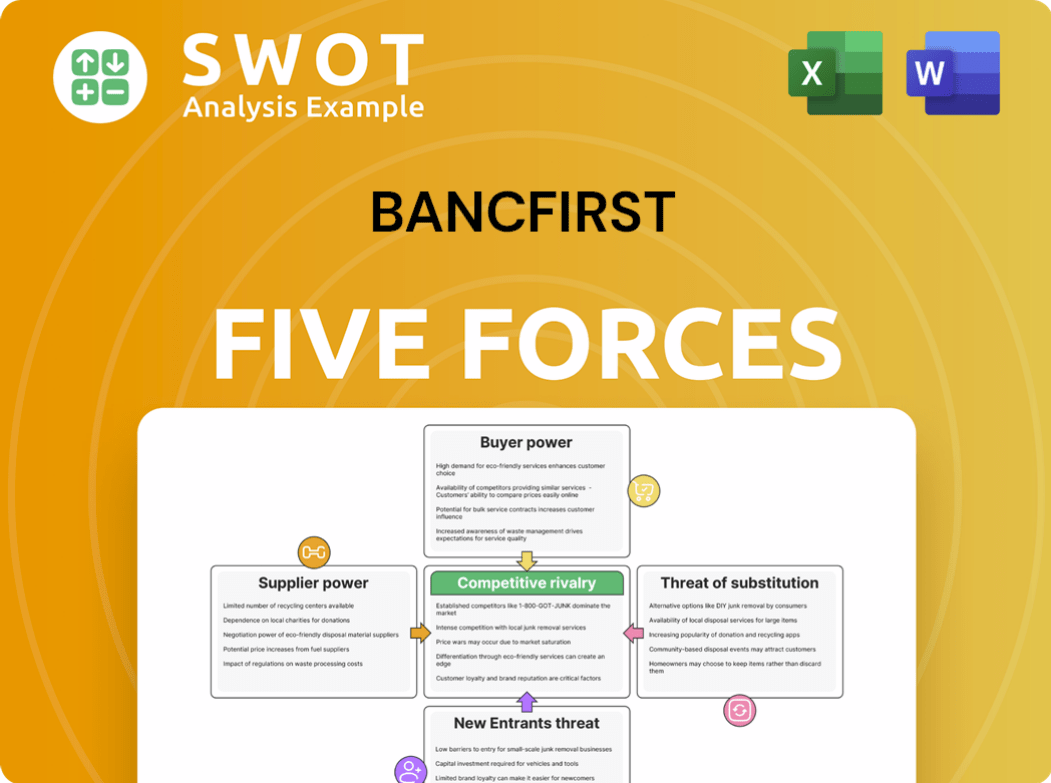

BancFirst Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of BancFirst Company?

- What is Competitive Landscape of BancFirst Company?

- How Does BancFirst Company Work?

- What is Sales and Marketing Strategy of BancFirst Company?

- What is Brief History of BancFirst Company?

- Who Owns BancFirst Company?

- What is Customer Demographics and Target Market of BancFirst Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.