AGCO Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

AGCO Bundle

What is included in the product

Analyzes the competitive environment, revealing AGCO's position against rivals, suppliers, and buyers.

Customizable pressure levels—allowing you to adjust to different market dynamics.

Preview Before You Purchase

AGCO Porter's Five Forces Analysis

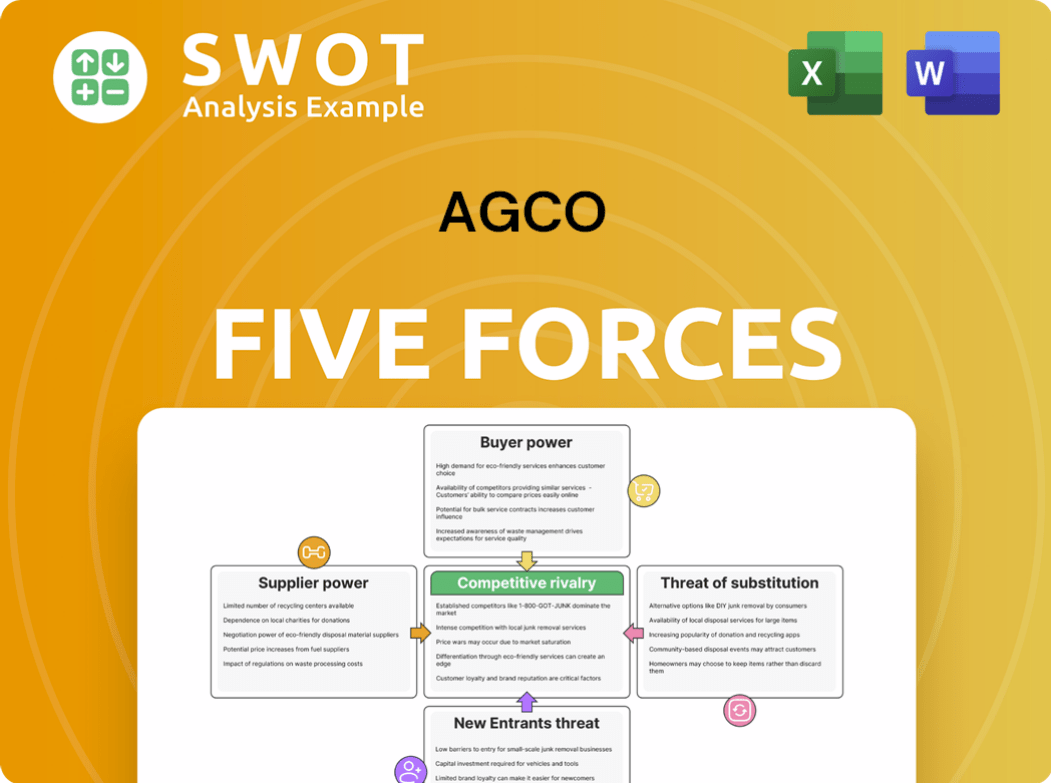

This preview showcases AGCO's Porter's Five Forces Analysis. You're seeing the complete, ready-to-use document. It details industry rivalry, and supplier & buyer power. The analysis covers threat of substitutes and new entrants. After purchase, you'll get this exact file.

Porter's Five Forces Analysis Template

Go Beyond the Preview—Access the Full Strategic Report

AGCO faces a complex competitive landscape. Buyer power is moderate, influenced by farm size and market concentration. Supplier bargaining power is also moderate due to diverse input providers. The threat of new entrants is relatively low, given high capital requirements. Substitute products, like used equipment, pose a moderate threat. Competitive rivalry is intense, shaped by major players.

The complete report reveals the real forces shaping AGCO’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentrated Supplier Base

AGCO depends on suppliers for parts and materials, and their concentration can create supplier power. Key suppliers, especially those with unique offerings, can control pricing and terms. In 2024, AGCO's cost of goods sold was significantly impacted by supplier pricing. For example, the cost of steel increased by 15% due to supplier market control.

Supplier Switching Costs

Switching suppliers can be a significant challenge for AGCO, involving costs and time. Building new supplier relationships, ensuring quality, and integrating components create friction. This dynamic favors existing suppliers, potentially leading AGCO to accept less favorable terms. In 2024, AGCO spent $12.6 billion on production costs, highlighting the impact of supplier relationships. The costs of switching can include expenses for new equipment or processes.

Impact of Supplier Consolidation

The agricultural equipment sector has witnessed supplier consolidation, reducing choices and boosting the remaining suppliers' bargaining power. Mergers or acquisitions within the supplier base allow them to dictate pricing and supply terms. This can pressure AGCO's profit margins. For example, the cost of raw materials like steel, a key input, saw increases in 2024, impacting AGCO's production costs. AGCO needs to proactively manage these shifts to secure competitive sourcing.

Supplier's Ability to Integrate Forward

If AGCO's suppliers could integrate forward, their bargaining power would surge, potentially turning them into rivals. This threat forces AGCO to maintain strong supplier relationships and competitive pricing to avoid being undercut. For example, Deere & Company, a competitor, has extensive supplier networks and integrated operations. In 2024, AGCO's cost of goods sold was approximately $13.5 billion, making supplier costs a significant factor.

- Threat of Integration: Suppliers becoming competitors.

- Impact on AGCO: Pressure to maintain relationships.

- Financial Implication: Supplier costs impacting profitability.

- Competitive Landscape: Deere & Company's integrated model.

Raw Material Price Volatility

AGCO faces supplier power due to raw material price volatility. Steel and rubber price fluctuations directly affect production costs. In 2024, steel prices saw about a 5% increase, impacting manufacturing. Suppliers can raise prices, squeezing AGCO's profits. Managing this is key for financial health.

- Price increases from suppliers directly affect AGCO's profitability.

- Steel prices increased by about 5% in 2024.

- Hedging strategies help mitigate these risks.

- Long-term contracts can stabilize costs.

Supplier Dynamics Impacting Costs

AGCO grapples with supplier power due to raw material and component dependencies, affecting costs. Supplier concentration and unique offerings give suppliers leverage over pricing and terms. In 2024, production costs totaled approximately $12.6 billion, significantly influenced by supplier costs.

Switching suppliers poses challenges, incurring costs and time, reinforcing existing supplier advantages. Consolidation within the supplier base reduces choices, enhancing their bargaining strength. These shifts pressure AGCO's profit margins, demanding proactive management for competitive sourcing.

The threat of suppliers integrating forward and becoming competitors requires maintaining strong supplier relationships and competitive pricing. In 2024, steel prices increased by about 5%, further impacting AGCO's manufacturing expenses. Effective risk mitigation is critical for financial stability.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Supplier Power | Influences Pricing, Terms | Production Costs: ~$12.6B |

| Switching Costs | Time, Expenses | Steel Price Increase: ~5% |

| Integration Threat | Competitive Risk | Steel impact on Production |

Customers Bargaining Power

Price Sensitivity of Farmers

Farmers' price sensitivity significantly influences AGCO. Low commodity prices in 2024, like the decrease in corn prices, pressure AGCO to offer competitive deals. The availability of used equipment and repair options intensify this sensitivity. This impacts AGCO's pricing strategies, affecting profitability in a competitive market.

Consolidation of Farms

The consolidation of farms into larger operations significantly boosts customer bargaining power. These large farms, purchasing in bulk, can demand lower prices and better terms from AGCO. This trend pressures AGCO to offer competitive deals, impacting profit margins. For instance, in 2024, the average farm size in the US grew, increasing buyer concentration.

Availability of Information

Farmers' access to product information has surged, fueled by online reviews and performance data. This increased transparency allows them to make informed choices and negotiate favorable deals. AGCO faces pressure to offer competitive pricing and demonstrate superior value, as seen in 2024 with a 3% decrease in average tractor prices due to market competition. This shift necessitates a focus on product differentiation and strong customer relationships.

Switching Costs for Buyers

Switching costs for AGCO's customers, primarily farmers, are relatively low, despite brand loyalty. Farmers can often switch brands without significant financial penalties if they find better deals or improved product features. This competitive landscape compels AGCO to focus on continuous innovation and value delivery to maintain customer loyalty. In 2024, the global agricultural machinery market was valued at approximately $130 billion, highlighting the stakes involved.

- Low switching costs empower farmers.

- AGCO must innovate to retain customers.

- Market value in 2024: $130 billion.

Financing Options

The availability of financing options strongly impacts buyer power within AGCO's market. Farmers often need financing for costly equipment; favorable terms can influence their decisions. AGCO must provide competitive financing, either directly or via partnerships, to remain attractive. This is especially vital given the high capital expenditure in agriculture.

- In 2024, AGCO's financing arm provided approximately $2.5 billion in financing.

- Competitive rates are crucial, as the average farm equipment loan term is 5-7 years.

- Partnerships with financial institutions broaden financing accessibility for customers.

- Offering flexible payment plans can boost sales, particularly during economic downturns.

How Farmer Power Impacts AGCO's Market

Customer bargaining power significantly shapes AGCO's market position. Price sensitivity driven by commodity fluctuations, impacted AGCO. Large farms leveraging bulk purchases demand competitive deals. Transparent information access further boosts farmer negotiation, influencing AGCO's pricing.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Price Sensitivity | Influences pricing | Corn prices decreased, pressuring deals. |

| Farm Consolidation | Increases bargaining power | US average farm size grew. |

| Information Access | Empowers informed choices | Tractor prices decreased by 3%. |

Rivalry Among Competitors

Intense Competition

The agricultural equipment sector is fiercely competitive, with multiple significant firms battling for dominance. This competition significantly impacts pricing, pushes for innovation, and emphasizes customer service. AGCO competes with industry giants like John Deere, CNH Industrial, and Kubota. For instance, in 2024, John Deere held approximately 30% of the global market share, highlighting the intense rivalry.

Market Share Concentration

Market share concentration in the agricultural equipment industry is high, fostering intense rivalry. Key players like John Deere, AGCO, and CNH Industrial compete aggressively. In Australia, these three hold a 40%-45% tractor market share. AGCO must innovate and strengthen its brand to stay competitive.

Product Differentiation

Product differentiation is key in the agricultural equipment sector. Companies like AGCO differentiate via tech, features, and performance to stand out. AGCO's R&D focuses on innovation and precision agriculture. In 2024, AGCO's R&D spending was about $300 million, reflecting its commitment.

Cyclical Industry

The agricultural equipment industry is highly cyclical. Demand swings with farm incomes, commodity prices, and weather. This leads to intense competition during downturns. AGCO needs strong cost management and financial flexibility to survive these cycles. In 2024, the global agricultural machinery market was valued at $140.8 billion.

- Market size: The global agricultural machinery market was valued at $140.8 billion in 2024.

- Cyclical nature: Demand linked to farm incomes and commodity prices.

- Competition: Intensifies during economic downturns.

- AGCO's strategy: Focus on cost control and financial resilience.

Global Presence

AGCO's competitive landscape shifts geographically. The company's global presence, particularly in EMEA, Asia, and Latin America, provides a buffer against direct competition with Deere & Co., which is dominant in North America. This strategic diversification allows AGCO to tap into diverse market opportunities. However, AGCO competes with regional manufacturers. This dynamic necessitates tailored strategies for each market.

- In 2024, AGCO reported that 55% of its net sales came from outside of North America.

- Deere & Co. generated approximately 65% of its revenue from the US and Canada in 2023.

- AGCO's revenue in the EMEA region accounted for 40% of its total sales in 2023.

Agricultural Equipment: A Fierce Battleground

Competitive rivalry in the agricultural equipment sector is extremely intense, driven by a few dominant companies. Innovation, pricing, and service are key battlegrounds. In 2024, John Deere had about 30% market share, illustrating the competition.

AGCO faces rivals like John Deere, CNH Industrial, and Kubota, needing to innovate. The industry's cyclical nature, tied to farm incomes, heightens rivalry. Diversification, with 55% of AGCO's 2024 sales outside North America, is crucial.

Geographical strategies are vital; AGCO's global reach differs from Deere's North American focus. Cost management and adaptability are essential for AGCO to survive. In 2024, AGCO's R&D spending was approximately $300 million.

| Metric | Competitor | 2024 Market Share (Approximate) |

|---|---|---|

| Global Market Share | John Deere | 30% |

| R&D Spend | AGCO | $300 Million |

| Sales Outside North America | AGCO | 55% |

SSubstitutes Threaten

Used Equipment Market

The used equipment market serves as a direct substitute for AGCO's new machinery. Farmers, especially during economic hardships, may opt for used equipment due to lower costs. In 2024, the used agricultural equipment market saw increased activity, with prices stabilizing relative to the previous year. To compete, AGCO must highlight advantages like advanced technology and warranties to justify the higher prices of new equipment. AGCO's ability to offer attractive financing options for new equipment also impacts this dynamic.

Equipment Leasing and Rental

Equipment leasing and rental pose a threat to AGCO as they offer alternatives to purchasing equipment. Farmers can utilize the latest technology without large upfront costs, potentially decreasing new machinery purchases. In 2024, the global agricultural equipment rental market was valued at approximately $12 billion. AGCO must develop competitive leasing and rental programs to stay relevant and capture market share in this evolving landscape. The agricultural equipment rental market is projected to reach $18 billion by 2030.

Repair and Refurbishment

Farmers can opt to repair or refurbish existing AGCO equipment, posing a threat to new sales. This is a budget-friendly choice, especially for older, functional machinery. In 2024, the market for agricultural equipment repair and maintenance reached $25 billion, reflecting its importance. AGCO must offer strong parts and service to compete effectively in this space.

Technological Upgrades

The threat of substitutes in AGCO's market includes technological upgrades that farmers can adopt. Farmers might choose to enhance their current equipment with precision agriculture systems, rather than purchasing new machines. This approach boosts efficiency without requiring a large capital outlay. AGCO's ability to retrofit various equipment brands with technology like Precision Planting and PTx Trimble offers a competitive edge.

- Precision agriculture adoption rates continue to rise, with the global market projected to reach $12.9 billion by 2024.

- AGCO reported that its precision agriculture sales grew by 15% in 2024.

- Retrofitting existing machinery with precision technology can cost significantly less than buying new equipment.

Alternative Farming Practices

Alternative farming methods pose a threat to AGCO. Practices like no-till farming can lessen the demand for specific machinery. These shifts require AGCO to adjust its product line. Adaptations are crucial to maintain market relevance. In 2024, the adoption of no-till farming increased by 7% globally.

- No-till adoption increased demand for precision agriculture.

- AGCO needs to focus on versatile equipment.

- Market share could be impacted by the shift.

AGCO's Substitutes: Used, Rental, and Repair

AGCO faces substitute threats from used equipment and rental services, impacting new machinery sales. Farmers might choose to repair or upgrade existing equipment, affecting AGCO's revenue. Alternative farming methods and precision agriculture technology adoption also provide viable alternatives, shifting demand.

| Substitute Type | Market Size (2024) | Impact on AGCO |

|---|---|---|

| Used Equipment | Increased activity and stable prices in 2024 | Lower new machinery sales |

| Equipment Rental | $12B (global agricultural equipment rental market) | Reduced upfront costs for farmers, affecting purchases |

| Repair & Refurbish | $25B (agricultural equipment repair/maintenance market) | Decreased demand for new equipment |

Entrants Threaten

High Capital Requirements

The agricultural equipment industry has high capital requirements, a significant barrier to entry. New entrants need substantial financial resources for manufacturing and distribution. AGCO, with its established presence, benefits from this advantage. In 2024, AGCO's capital expenditures were approximately $350 million, reflecting the industry's capital-intensive nature.

Established Brand Loyalty

Farmers frequently stick with brands they know and trust, which is a considerable barrier for new competitors. Establishing a strong brand and earning farmer's trust demands substantial marketing efforts and time. AGCO's well-known brands, such as Fendt, Massey Ferguson, and Valtra, give it a significant advantage. In 2024, AGCO's marketing expenses were around $700 million, reflecting its dedication to brand building and customer loyalty.

Economies of Scale

AGCO, a major player, benefits from economies of scale. This advantage is evident in manufacturing, purchasing, and distribution, allowing for competitive pricing. New entrants face a significant hurdle to match this scale. In 2024, AGCO's revenue reached approximately $14.4 billion, showcasing its established market presence and scale advantage.

Regulatory Hurdles

The agricultural equipment sector faces strict regulations, such as emissions and safety standards. New entrants must overcome these regulatory challenges, which can be expensive. AGCO, for instance, ensures its AGCO Power engines meet emissions rules from the EU, Brazil, and the U.S. These requirements can significantly increase startup costs. In 2024, regulatory compliance costs are estimated to have risen by 7% for industry players.

- Regulatory compliance adds significant costs, impacting new entrants.

- AGCO Power engines adhere to global emissions standards.

- Compliance costs have increased by 7% in 2024.

Access to Distribution Channels

In the agricultural equipment industry, access to distribution channels is a significant barrier for new entrants. AGCO, for example, relies heavily on its established network of independent dealers and distributors. New companies face the challenge of building their own distribution systems, a costly and time-consuming process. This often involves securing agreements with dealers, which can be difficult due to existing relationships and market saturation. The difficulty in establishing effective distribution limits the threat of new entrants.

- AGCO's distribution network includes approximately 3,000 independent dealers and distributors globally.

- The cost to establish a new dealer network can range from millions to tens of millions of dollars.

- Market share is concentrated, with AGCO, Deere & Company, and CNH Industrial holding significant portions.

- New entrants must compete with established brands for dealer attention.

AGCO's Fortress: Barriers to Entry

The threat of new entrants to AGCO is moderate due to substantial barriers. High capital needs and brand loyalty favor established players. Stringent regulations and distribution challenges further deter newcomers. AGCO’s strong position limits new competition.

| Barrier | AGCO Advantage | 2024 Data |

|---|---|---|

| Capital Requirements | Established Manufacturing & Distribution | $350M CapEx |

| Brand Loyalty | Trusted Brands (Fendt, etc.) | $700M Marketing Spend |

| Economies of Scale | Competitive Pricing | $14.4B Revenue |

Porter's Five Forces Analysis Data Sources

AGCO's Porter's Five Forces assessment utilizes SEC filings, industry reports, and financial databases. These data sources provide detailed insights.