Alta Equipment Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Alta Equipment Group Bundle

What is included in the product

Detailed analysis of each competitive force, supported by industry data and strategic commentary.

Swap in your own data, labels, and notes to reflect current business conditions.

What You See Is What You Get

Alta Equipment Group Porter's Five Forces Analysis

You're viewing the complete Alta Equipment Group Porter's Five Forces analysis. This in-depth examination of industry competitiveness, threat of new entrants, bargaining power of suppliers/buyers, and rivalry is all ready for immediate use. The preview you see provides the full, unedited document. It is immediately available for download and review once the purchase is complete. This comprehensive analysis is exactly what you'll receive—fully formatted and ready to use.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

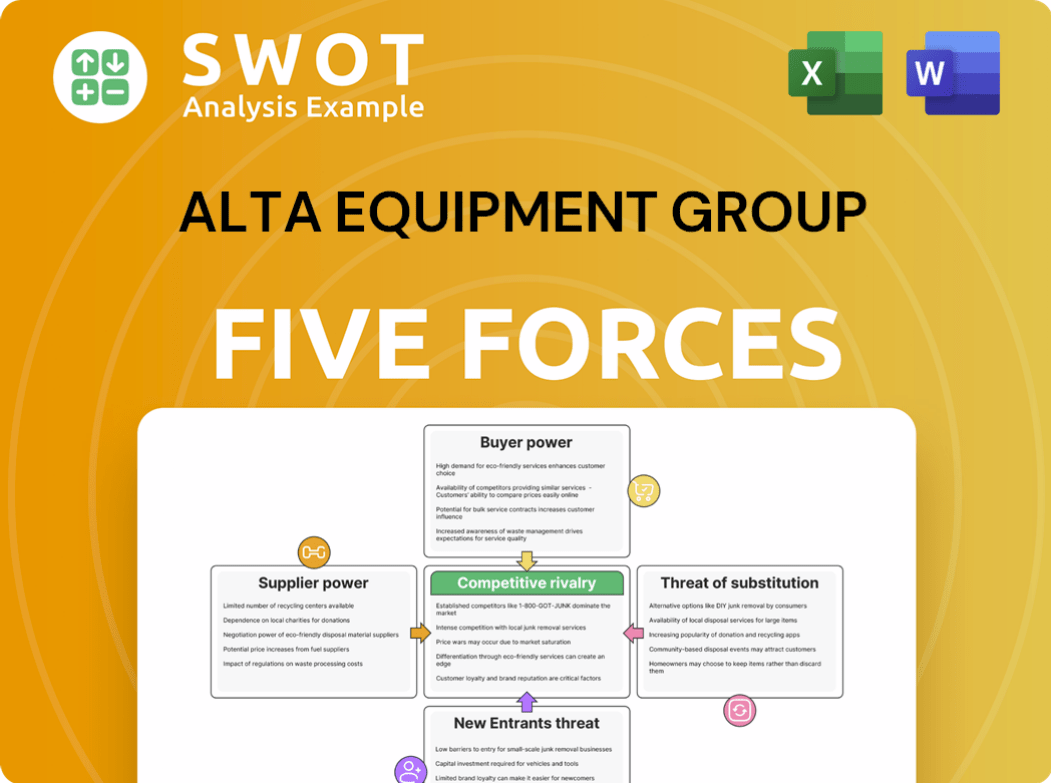

Alta Equipment Group faces a mixed competitive landscape. Buyer power is moderate, influenced by customer concentration and switching costs. Supplier power varies, reflecting equipment specialization. New entrants face high barriers due to capital needs and brand recognition. Substitute threats are present, driven by evolving technologies. Rivalry is intense, shaped by market consolidation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Alta Equipment Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Concentration

The construction equipment sector faces supplier concentration, with a few major players dominating the market. This structure grants suppliers substantial pricing power, directly influencing Alta Equipment Group's profitability. Caterpillar, Komatsu, and Volvo, for instance, collectively command a significant market share. In 2024, these manufacturers' consolidated revenue exceeded $100 billion.

Dependence on Key Brands

Alta Equipment Group's reliance on key suppliers, like Volvo and Hyster-Yale, is a significant factor. This dependence creates vulnerability to supply chain disruptions or price hikes. For example, in 2024, supply chain issues impacted equipment availability across the industry. Their role as exclusive distributors offers some protection, but also ties their fortunes to these brands. This means Alta's success is closely linked to its suppliers' performance and strategies.

Product Differentiation

Alta Equipment Group faces supplier bargaining power, particularly where product differentiation exists. The industrial and construction equipment market is competitive, with differentiation based on technology and performance. Suppliers with unique tech, like those in advanced construction tech, can exert pricing pressure. In 2024, the global construction equipment market was valued at $140 billion, highlighting the stakes.

Supplier Switching Costs

Switching suppliers presents significant challenges for Alta Equipment Group, increasing supplier power. Retraining staff, reconfiguring service operations, and potentially losing customer loyalty are involved. These costs make it difficult for Alta to change suppliers readily. The company's reliance on specific parts and brand recognition further elevates these switching costs. Alta's operating expenses in 2024 totaled $1.2 billion, a 10% increase from the prior year, reflecting these operational dependencies.

- Alta's 2024 operating expenses: $1.2 billion.

- Increase in operating expenses: 10%.

- Switching suppliers involves retraining and reconfiguration.

- Customer loyalty tied to specific brands impacts switching.

Impact of Tariffs and Trade Policies

Tariffs and trade policies significantly impact Alta Equipment Group's supplier costs. Expanded tariffs on Chinese-made components, as of March 2024, are increasing input costs for industrial equipment producers in the U.S., potentially leading to higher prices for Alta. Trade policy uncertainty further complicates supplier relationships, making cost management challenging. These factors can reduce profit margins and impact competitiveness.

- As of Q1 2024, tariffs on steel and aluminum have increased input costs by 10-15% for some manufacturers.

- Supply chain disruptions due to trade tensions have led to a 5-8% increase in lead times for critical components.

- The U.S. government implemented new tariffs on specific Chinese goods in 2024, increasing costs for equipment manufacturers.

Alta's Supplier Risks: Concentration, Costs & Vulnerability

Suppliers hold considerable power over Alta Equipment Group, particularly due to industry concentration and product differentiation. Reliance on key suppliers creates vulnerability to price hikes and supply chain disruptions, increasing operational expenses.

Switching costs, including retraining and potential loss of customer loyalty, further strengthen suppliers' position. Tariffs and trade policies add to cost pressures, impacting profitability.

These factors require Alta to manage supplier relationships strategically to mitigate risks.

| Factor | Impact | Data (2024) |

|---|---|---|

| Supplier Concentration | Higher Pricing Power | Top 3 manufacturers' revenue > $100B |

| Switching Costs | Reduced Flexibility | OpEx $1.2B, up 10% |

| Trade Policies | Increased Costs | Tariffs increased costs up to 15% |

Customers Bargaining Power

Customer Concentration

Alta Equipment Group operates across construction, material handling, and agriculture. If a few major clients account for a large part of Alta's revenue, their influence on pricing increases significantly. This customer concentration gives them more leverage. In 2024, the top 10 customers may represent over 30% of sales, indicating high buyer power.

Rental vs. Purchase Options

Customers' bargaining power is shaped by choices: rental or purchase. Rentals' appeal, due to cost and flexibility, grows across sectors. In 2024, the equipment rental market in North America was valued at roughly $58.8 billion. This rising demand may shift power toward customers. They can readily switch rental providers.

Availability of Alternatives

Customers of Alta Equipment Group have several equipment options, boosting their power. Competitors such as United Rentals and Sunbelt Rentals force Alta to stay competitive. The industry's fragmented nature further strengthens customer influence. United Rentals reported ~$13.4 billion in total revenue for 2023, showing strong competition.

Switching Costs

Switching costs significantly impact customer bargaining power. For equipment like forklifts, switching is easy, but for specialized mining equipment, costs rise. Alta can build loyalty through service; in 2024, service revenue accounted for 20% of total revenue. Strong customer relationships also help.

- Switching costs vary widely based on equipment type.

- Specialized equipment increases switching costs.

- Service packages enhance customer loyalty.

- Alta's service revenue percentage in 2024.

Impact of Economic Conditions

Economic conditions significantly influence customer bargaining power. Downturns heighten price sensitivity, impacting investment decisions. In 2024, factors like interest rates and political uncertainty affected construction spending. Alta's strategies for profitability are tested by these economic shifts.

- In 2024, construction spending growth slowed, impacting equipment sales.

- Elevated interest rates increased the cost of capital for customers.

- Political uncertainty influenced investment decisions.

- Alta's financial performance in 2024 reflected these economic pressures.

Alta's Customer Dynamics: Power, Market & Costs

Alta's customer power is high, influenced by concentrated sales and equipment choices. Rental demand surged, with the North American market at $58.8B in 2024. Switching costs vary, affecting customer influence.

Economic factors, like slowed construction spending, impact customer price sensitivity. Elevated interest rates increased the cost of capital for customers. Alta's strategies are tested by economic shifts.

| Factor | Impact | 2024 Data |

|---|---|---|

| Customer Concentration | Increases buyer power | Top 10 customers: >30% of sales |

| Rental Market | Provides alternatives | North American market: ~$58.8B |

| Switching Costs | Influences loyalty | Variable based on equipment type |

Rivalry Among Competitors

Market Fragmentation

The equipment rental and sales market is very fragmented, featuring many local and national firms. This leads to strong competition, impacting pricing and profit margins. Alta must stand out with excellent service, diverse products, or broader geographic reach. Intense rivalry can decrease profitability; for instance, in 2024, the industry saw a 2-3% margin squeeze.

Presence of Major Players

Major players like United Rentals and Sunbelt Rentals create intense rivalry. These firms have extensive networks and brand recognition. Alta faces challenges in competing on price. In 2024, United Rentals reported a revenue of approximately $14.4 billion. Regional differences in figures were significant.

Competition in Product Support

Product support, crucial for revenue, faces fierce rivalry. Customers have repair and maintenance choices, intensifying competition. Alta, to retain and expand, needs a robust service network. Competitive pricing and service quality are essential for success. In 2024, the parts and service segment represented a significant portion of Alta's revenue, highlighting its importance.

Impact of Equipment Oversupply

An oversupply of new equipment intensifies competition, potentially squeezing prices and profit margins. In 2024, Alta, like other dealers, faced overstocked dealer channels, particularly affecting its Construction segment. This situation likely contributed to the decrease in Alta's gross profit margin reported in Q3 2024. Normalizing equipment supply will be critical for improving Alta's competitive position in 2025.

- Pricing Pressure: Oversupply can force dealers to lower prices.

- Margin Impact: Reduced prices directly affect gross margins.

- 2024 Context: Industry overstocking was a key issue.

- Future Outlook: Normalization is key for 2025.

Acquisition-Driven Growth

Alta Equipment Group's growth strategy, heavily reliant on acquisitions, significantly ramps up competitive rivalry. Integrating these acquired companies and achieving the anticipated synergies present considerable challenges. Alta competes with other industry players also pursuing acquisition-driven expansion, vying for similar targets and market share.

However, Alta's exclusive distribution agreements with its original equipment manufacturer (OEM) partners in its operational areas provide a competitive advantage. This exclusivity shields Alta from direct competition and bolsters its market share in a sector largely shaped by consolidation. For instance, in 2023, Alta made several acquisitions, including Flagler Construction Equipment, to strengthen its presence in the Florida market.

- Acquisition Focus: Alta's strategy increases competition.

- Integration Challenges: Synergies are hard to achieve.

- Competitive Landscape: Other firms also pursue acquisitions.

- Strategic Advantage: Exclusive distribution boosts market share.

Equipment Market: Margin Decline & Rivalry

Competitive rivalry in the equipment market is high, with numerous players. Pricing pressure and margin squeezes are common; the industry saw a 2-3% margin decline in 2024. Alta's growth via acquisitions intensifies competition.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Margin Squeeze | Reduced profitability | Industry margin decrease of 2-3% |

| Key Competitors | Intense rivalry | United Rentals revenue approx. $14.4B |

| Acquisition Strategy | Increased competition | Alta's acquisitions increased in 2023-2024 |

SSubstitutes Threaten

Equipment Rental vs. Ownership

Customers have the option to rent equipment instead of buying, which acts as a substitute for Alta's sales. The rising rental rate, influenced by cost and flexibility, impacts Alta's sales revenue. The construction and industrial equipment rental sector reached a 57.0% penetration rate in 2024, exceeding pre-pandemic levels. This shift presents a challenge to Alta's equipment sales model.

Used Equipment Market

The used equipment market presents a significant threat to Alta Equipment Group. This market offers customers a cheaper alternative to buying new equipment, potentially decreasing demand for Alta's new equipment sales. In 2024, Alta's used equipment sales experienced substantial growth, increasing by 25.1% to reach $298.1 million, indicating the market's strength. This robust market could divert customers from purchasing new equipment.

Technological Advancements

Technological advancements present a significant threat of substitution for Alta Equipment Group. New technologies, including automation and AI, can diminish the demand for conventional equipment. The substitution threat intensifies if Alta fails to adapt its offerings to incorporate these emerging technologies and satisfy changing customer demands. A 2024 NIST report indicates that while 72% of industrial equipment manufacturers aim to increase automation investments by 2025, only 38% feel their training programs are sufficient. This indicates a considerable risk if Alta doesn't invest in these areas.

Outsourcing of Services

Customers have the option to outsource construction or material handling services, potentially bypassing the need to purchase or rent equipment from Alta Equipment Group. This shift towards outsourcing acts as a substitute, impacting the demand for equipment sales and rentals. The construction equipment rental market was valued at USD 147.4 billion in 2024, showcasing a viable alternative for companies. This market is projected to grow at a 6.2% CAGR from 2025 to 2034, suggesting a rising trend of outsourcing.

- Outsourcing provides an alternative to direct equipment ownership.

- Rental market growth indicates the increasing popularity of this substitute.

- High equipment costs drive the demand for outsourcing services.

- This substitution can directly affect Alta's revenue streams.

Alternative Construction Methods

The rise of alternative construction methods poses a threat to Alta Equipment Group. Innovations like modular construction and 3D printing may decrease the demand for traditional equipment. These methods are developing, presenting a substitution risk Alta must address.

- Modular construction market was valued at $157.1 billion in 2023.

- 3D printing in construction is projected to reach $3.9 billion by 2028.

- Alta's revenue in 2023 was $1.1 billion.

Alternatives Impacting Equipment Sales

Several factors present substitution threats to Alta Equipment Group. Outsourcing and equipment rentals offer customers viable alternatives to purchasing equipment. The construction equipment rental market was valued at $147.4 billion in 2024. These alternatives directly impact Alta's sales and rental revenue.

| Substitution Threat | Impact | 2024 Data |

|---|---|---|

| Outsourcing & Rentals | Reduced Equipment Sales | Rental Market: $147.4B |

| Used Equipment | Decreased New Sales | Used Sales Growth: 25.1% |

| Technological Advancements | Reduced Demand for Traditional Equipment | Automation Investment Aim: 72% |

Entrants Threaten

Capital Requirements

The equipment rental and sales sector demands substantial capital for machinery, facilities, and services. These high capital needs act as a significant barrier, reducing the risk from new competitors, particularly those targeting a broad market. The construction equipment rental market was valued at USD 147.4 billion in 2024. This financial commitment deters smaller firms.

Established Brand Recognition

Established companies such as United Rentals and Caterpillar have significant brand recognition and a solid customer base. New entrants face the challenge of substantial marketing and branding investments to compete effectively. Alta Equipment Group benefits from its exclusive distributor agreements, which protect its market share. In 2024, United Rentals reported revenues of $10.9 billion, highlighting the scale of established competitors.

Access to Distribution Networks

New entrants face a significant barrier: establishing distribution. Alta Equipment Group's robust network, with 22 full-service locations across 8 states, provides a competitive edge. This geographical concentration, particularly in Michigan, Ohio, and Illinois, is a key strength. Building a similar network demands substantial investment and time, making it difficult for new competitors to enter the market. In 2024, Alta's revenue was approximately $1.4 billion, highlighting the scale of their established distribution and service capabilities.

Regulatory and Licensing Requirements

Regulatory and licensing requirements pose a significant threat to new entrants in the construction equipment industry. These requirements, which can vary by region, create hurdles for new businesses. In India, for instance, the construction equipment market is projected to grow significantly. The market is expected to grow at a CAGR of 8-10% in the coming years due to infrastructure development.

- Compliance Costs: Meeting regulatory standards can be expensive.

- Time-Consuming: The process of obtaining licenses and permits takes time.

- Market Growth: India's construction equipment market is robust.

- Government Focus: Infrastructure development drives market growth.

Economies of Scale

Established companies like Alta Equipment Group benefit from economies of scale. They gain advantages in purchasing, service operations, and marketing. New entrants struggle to match the cost structure of these larger players. This makes it challenging for them to compete on price. National chains use unified technology to scale efficiently.

- Alta Equipment Group's revenue in 2023 was approximately $1.2 billion.

- Larger companies can negotiate better prices with suppliers due to higher purchasing volumes.

- Unified technology reduces operational costs, a key advantage for established firms.

- Independent rental operators often face high costs due to outdated systems.

Rental Market Hurdles: Capital & Brands

New entrants face significant obstacles, including high capital requirements and established brand recognition. The construction equipment rental market reached USD 147.4 billion in 2024, requiring substantial investment. Alta Equipment Group's distribution network provides a competitive edge.

| Barrier | Description | Impact |

|---|---|---|

| Capital Needs | High costs for equipment and infrastructure. | Deters smaller firms. |

| Brand Recognition | Established competitors have strong brands. | Requires significant marketing investment. |

| Distribution Network | Alta's extensive network. | Difficult for new entrants to replicate. |

Porter's Five Forces Analysis Data Sources

The analysis uses SEC filings, financial reports, and industry publications for detailed financial and operational insights. Market research, competitor analysis and analyst reports are key.