Ameren Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Ameren Bundle

What is included in the product

Tailored exclusively for Ameren, analyzing its position within its competitive landscape.

Quickly identify market threats with dynamic charts and pressure assessments.

Preview the Actual Deliverable

Ameren Porter's Five Forces Analysis

You're previewing the complete Ameren Porter's Five Forces analysis. This fully-formatted document details the competitive forces at play. It includes thorough analysis of each force affecting Ameren. The document you see is the exact file you'll download upon purchase. There are no differences; use it immediately.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

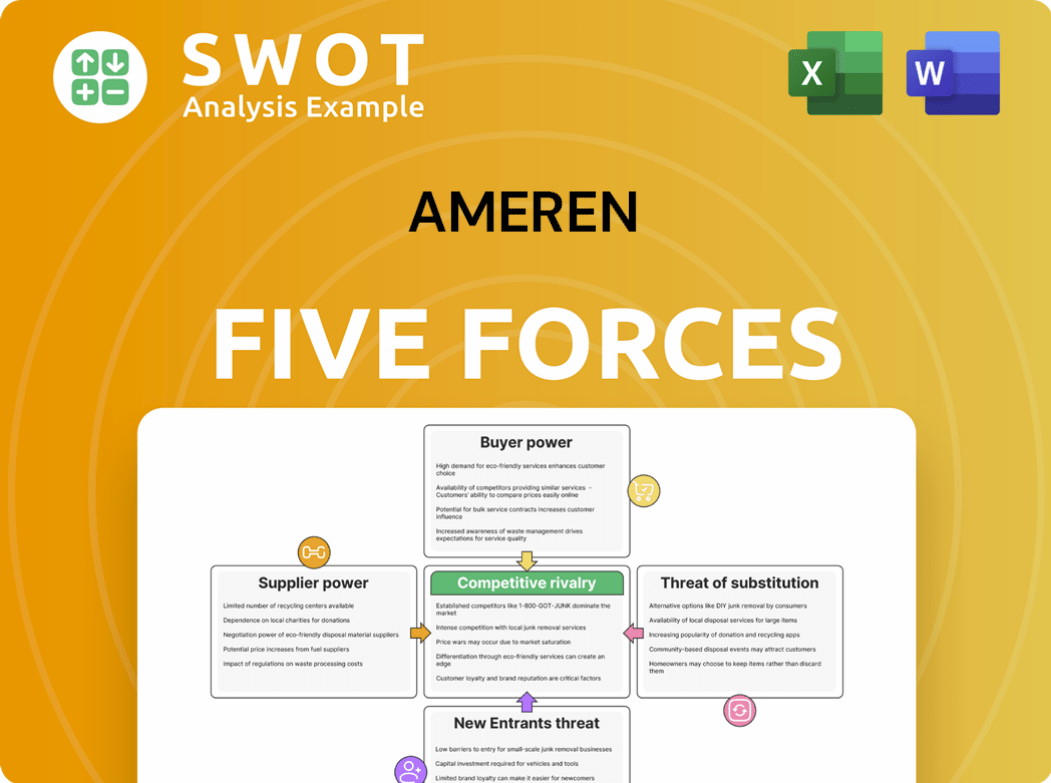

Ameren's competitive landscape is shaped by several key forces. Buyer power is moderate due to regulated pricing. Supplier power from fuel sources is a constant factor. The threat of new entrants is low given high barriers. Substitute threats, like renewable energy, are rising. Industry rivalry is intense among existing utilities.

Ready to move beyond the basics? Get a full strategic breakdown of Ameren’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited Number of Suppliers

Ameren faces challenges due to a limited number of suppliers, particularly for specialized equipment. In 2024, the utility sector heavily depends on 3-4 global manufacturers for crucial infrastructure components. This dependency gives suppliers significant bargaining power, potentially increasing Ameren's expenses. This situation can also affect project schedules.

Fuel Supplier Dependencies

Ameren's fuel supply chain faces risks due to supplier concentration. In 2024, Ameren sourced coal from just 3 regional suppliers and natural gas from 2. This limited supplier base increases the risk of supply disruptions. These conditions may lead to price volatility, impacting Ameren's operational costs. The company's reliance on these entities gives them considerable bargaining power.

High Switching Costs

Switching suppliers for crucial utility equipment presents significant expenses. In 2024, estimated switching costs for infrastructure components ranged from $2.7 million to $8.5 million. These high expenses diminish Ameren's flexibility. This reliance on existing suppliers boosts their bargaining power.

Long-Term Contracts

Ameren significantly reduces supplier bargaining power through long-term contracts. These contracts, often spanning 7-10 years, with major suppliers of equipment and fuel, are critical for stability. The company's strategy helps to shield it from short-term fluctuations. This approach offers pricing and supply assurance.

- Ameren's long-term contracts span 7-10 years with key suppliers.

- These contracts reduce immediate supplier leverage.

- They provide stability in pricing and supply.

- This strategy helps to offset potential supplier pressures.

Regulatory Scrutiny

Regulatory scrutiny significantly influences Ameren Porter's supplier relationships. The Illinois Commerce Commission (ICC) and other regulatory bodies oversee Ameren's procurement and investments. This oversight limits the company's ability to fully pass supplier cost increases to consumers. It encourages efficient supply chain management to maintain profitability.

- ICC's oversight ensures fair practices.

- Cost recovery is limited by regulatory constraints.

- Efficiency in procurement is a key focus.

- Ameren must optimize supplier negotiations.

Supplier Power Dynamics at Play

Ameren contends with supplier bargaining power due to limited supplier options and specialized equipment needs. Dependence on few providers for critical components and fuel, as seen with sourcing from only 2-3 entities in 2024, elevates this power. Long-term contracts and regulatory oversight help mitigate these pressures.

| Factor | Impact | 2024 Data/Details |

|---|---|---|

| Supplier Concentration | High bargaining power | 3-4 global manufacturers for key equipment; 2-3 fuel suppliers |

| Switching Costs | Reduce flexibility | $2.7M-$8.5M estimated for infrastructure components. |

| Mitigating Strategies | Reduce immediate supplier leverage | 7-10 year contracts, regulatory oversight by ICC |

Customers Bargaining Power

Regulated Market

Ameren, as a regulated utility, faces limited customer bargaining power. The company's service areas are exclusive, reducing customer choices. This regulatory framework ensures a stable customer base. In 2024, Ameren's revenue was approximately $8.3 billion, reflecting its market position.

Switching to Alternatives

Customers' power to switch to alternatives is limited. Most rely on Ameren for electricity and natural gas. Some may use alternative energy sources, but switching is often restricted. Regulatory frameworks and infrastructure limit widespread changes. Ameren's market position is therefore strengthened. In 2024, residential customer churn rates averaged around 1-2%.

Price Sensitivity

Ameren faces price-sensitive customers, impacting regulatory decisions. Rising costs, including a 2024 increase in wholesale prices, will likely push up electricity bills. The Illinois Commerce Commission (ICC) must balance Ameren's profits and consumer affordability. In 2023, residential customers paid an average of 16.8 cents per kilowatt-hour.

Demand Response Programs

Ameren's demand response programs give customers some control over energy use, incentivizing them to cut back during peak times. These programs slightly shift customer power, but their impact is contained. Participation and demand reduction remain relatively small.

- Ameren's 2024 programs include options for residential and commercial customers to reduce energy use during peak hours, offering bill credits or other incentives.

- In 2024, peak demand savings from these programs were estimated to be around 2-3% of total peak load.

- Participation rates in these programs typically range from 5-10% of eligible customers in 2024.

- The financial impact on Ameren's revenues is limited, as the incentives are partially offset by reduced energy sales during peak times.

Economic Development

Ameren actively supports economic development, which significantly impacts its customer base and the bargaining power of customers. By aiding businesses in expansion or relocation within its service areas, Ameren indirectly boosts customer demand. This strategic involvement helps stabilize and potentially increase its customer base. However, this requires balancing the energy needs of both new and existing customers, which affects pricing and service agreements.

- Ameren's economic development initiatives aim to attract new businesses.

- This directly increases the demand for its services.

- In 2024, Ameren invested $100 million in grid modernization.

- This investment supports increased capacity for new customers.

Ameren: Market Dynamics & Financial Snapshot

Ameren's customer bargaining power is low due to its regulated monopoly. Customer alternatives are restricted, which reinforces Ameren's market position. The Illinois Commerce Commission (ICC) regulates pricing, balancing profits and affordability, which is shown by 2023's average rate of 16.8 cents per kWh.

| Aspect | Details | 2024 Data |

|---|---|---|

| Revenue | Ameren's Total Revenue | Approximately $8.3 billion |

| Customer Churn | Residential customer churn rate | Averaged around 1-2% |

| Demand Savings | Peak demand reduction | Estimated 2-3% of total peak load |

Rivalry Among Competitors

Regional Monopolies

Ameren often functions as a regional monopoly, particularly in Missouri and Illinois, where it supplies electricity and natural gas. This structure significantly reduces direct competition from other utility providers. However, this dominant position means Ameren is heavily regulated by state authorities like the Missouri Public Service Commission and the Illinois Commerce Commission. In 2024, Ameren reported approximately $8 billion in revenue, highlighting its substantial market presence despite regulatory constraints.

Competition for Economic Development

Ameren actively competes to draw new businesses to its service areas. It battles against other regions and utilities, aiming to attract companies expanding or relocating. Competitive rates and dependable service are crucial, influencing Ameren's investments. In 2024, the utility sector saw a 7% increase in business relocation projects. This intensifies the need for Ameren to offer attractive incentives.

Focus on Infrastructure

Competitive rivalry in Ameren Porter's infrastructure is intense. The main competition is over grid modernization investments. Ameren battles other utilities for regulatory approvals. Securing these investments is key for enhancing reliability and integrating renewables. In 2024, Ameren invested heavily in grid upgrades.

Renewable Energy

Ameren faces heightened competition in renewable energy. The shift towards cleaner energy sources intensifies rivalry in developing and acquiring renewable assets. This competition impacts project costs and timelines significantly. For example, in 2024, the U.S. solar market is expected to have a capacity of 32 GW.

- Increased competition drives down profit margins.

- Project delays can occur due to the competition.

- The energy mix is also affected.

- Ameren must strategically manage its renewable energy investments.

Regulatory Approvals

Ameren faces competition in regulatory approvals and rate adjustments. The company actively competes with stakeholders to achieve favorable regulatory outcomes. These regulatory battles directly affect Ameren's financial health and strategic plans. Securing approvals for projects, like infrastructure upgrades, is crucial for growth. Regulatory decisions significantly influence investment returns and operational strategies.

- In 2024, regulatory battles could impact Ameren's project timelines.

- Rate adjustments are key for maintaining financial stability.

- Ameren's ability to adapt to regulatory changes is critical.

- Favorable outcomes support long-term investments.

Ameren's Competitive Battles: Grid, Renewables, and Regulations

Ameren faces intense competitive rivalry across multiple fronts. Competition drives down profit margins and can lead to project delays. The energy mix is also affected by this competition.

| Area of Competition | Impact | 2024 Data Point |

|---|---|---|

| Grid Modernization | Investment delays | Ameren invested heavily in 2024 |

| Renewable Energy | Affects project costs | U.S. solar capacity expected at 32 GW |

| Regulatory Approvals | Impacts timelines | Regulatory battles could impact project timelines |

SSubstitutes Threaten

Energy Efficiency

Energy efficiency initiatives present a moderate threat to Ameren. Programs promoting conservation lower overall energy use. Ameren supports these, but adoption could reduce demand for electricity and natural gas. For example, residential energy efficiency programs saw a 10% increase in participation in 2024. This could impact Ameren’s revenues.

Renewable Energy

On-site renewable energy poses a threat to Ameren Porter. Customers with solar panels or renewable sources decrease their reliance on Ameren. Government incentives and falling tech costs boost adoption. For example, residential solar capacity grew by 30% in 2024. This trend impacts Ameren's revenue.

Alternative Fuels

The threat of substitutes for Ameren Porter is currently limited, particularly concerning alternative fuels. Adoption of propane or biofuels is restricted within Ameren's service areas. Natural gas remains the primary fuel for heating and industrial use. In 2024, natural gas prices were relatively stable compared to other energy sources, reducing the incentive for widespread substitution.

Demand Response

Demand response programs present a substitute for Ameren Porter's electricity during peak times. These programs reduce electricity usage during peak hours, potentially decreasing the need for new power plants. The effectiveness of demand response is constrained by customer participation and the length of peak demand events. For instance, Ameren Illinois has been actively promoting demand response programs to manage peak loads.

- Ameren Illinois's peak demand in 2023 was approximately 7,000 MW.

- Demand response programs can reduce peak demand by up to 10-15%.

- Participation rates in demand response programs are typically around 10-20% of eligible customers.

Energy Storage

Energy storage technologies, especially battery energy storage systems (BESS), represent an emerging substitute for traditional energy sources like those used by Ameren Porter. BESS can store energy generated from various sources, allowing for its use during peak demand, potentially reducing reliance on the grid. The increasing cost-effectiveness of BESS technologies could intensify this threat. This shift challenges the traditional utility business model.

- In 2024, the global energy storage market was valued at approximately $20 billion.

- The BESS market is projected to grow significantly, with forecasts estimating a market size exceeding $60 billion by 2030.

- The levelized cost of storage (LCOS) for BESS has decreased substantially, making it a more competitive alternative.

- Ameren Missouri has already invested in BESS projects, such as the Taum Sauk pumped storage plant.

Ameren's Rivals: Efficiency, Renewables, and Storage

Substitutes for Ameren pose a moderate threat, primarily from energy efficiency, on-site renewables, and demand response. Energy storage technologies, like BESS, are an emerging challenge. The market value of the BESS was about $20 billion in 2024, with growth expected.

| Substitute | Threat Level | 2024 Data/Impact |

|---|---|---|

| Energy Efficiency | Moderate | Residential program participation rose by 10%. |

| On-site Renewables | Moderate | Residential solar capacity increased by 30%. |

| Demand Response | Moderate | Peak demand reduction potential is 10-15%. |

| Energy Storage (BESS) | Increasing | Global market value ≈ $20B, growing. |

Entrants Threaten

High Capital Costs

High capital costs form a substantial barrier. Building electricity infrastructure demands significant initial investment. This includes generation plants, transmission lines, and distribution networks. Ameren's established infrastructure protects its market share. The Energy Information Administration (EIA) reported in 2024 that the average cost to build a new natural gas power plant is about $800-$1,200 per kilowatt.

Regulatory Hurdles

Ameren Porter faces regulatory hurdles, a significant barrier to new entrants. Stringent requirements demand extensive approvals and compliance. The utility industry's heavy regulation complicates market entry. These processes are time-consuming, deterring potential competitors. In 2024, regulatory costs in the energy sector increased by approximately 7%, reflecting these challenges.

Economies of Scale

Ameren, like other established utilities, benefits from significant economies of scale, creating a barrier to entry. Existing infrastructure and operational size provide cost advantages. This advantage makes it challenging for new entrants to compete on price. For example, Ameren's 2024 revenue was about $8.6 billion, reflecting its scale.

Established Infrastructure

Ameren's established infrastructure poses a significant barrier to new entrants. The company's existing grid infrastructure and customer base provide a substantial competitive advantage. New entrants would face high costs and complexities in building or accessing existing networks. Ameren's 2024 capital expenditures are projected to be around $3.5 billion, reflecting its commitment to maintaining and upgrading its infrastructure. This investment further solidifies its position, making it difficult for new players to compete.

- Ameren's existing grid infrastructure represents a substantial sunk cost, creating a financial hurdle for potential competitors.

- Customer base: Ameren serves millions of customers, offering established revenue streams.

- Regulatory hurdles: New entrants must navigate complex regulatory landscapes.

- Capital requirements: Building infrastructure is expensive and time-consuming.

Market Saturation

The threat of new entrants in Ameren's market is moderate due to market saturation. The electricity and natural gas sectors within Ameren's service areas are largely established, offering limited room for new competitors. This saturation diminishes the appeal for new firms seeking to enter and gain significant market share. High initial capital costs and regulatory hurdles further deter new entrants.

- Market saturation limits growth opportunities.

- Ameren's service areas are mostly established markets.

- Limited market share gains discourage new entries.

- High costs and regulations pose barriers.

Ameren's Edge: Barriers & Data

New entrants face substantial barriers due to high infrastructure costs and regulatory hurdles, as in 2024.

Ameren's existing infrastructure, with 2024 capital expenditures around $3.5 billion, creates a significant competitive advantage.

Market saturation and established customer bases limit the attractiveness for new competitors.

| Barrier | Description | 2024 Data |

|---|---|---|

| Capital Costs | High investment needs | $800-$1,200 per kW for new gas plants (EIA) |

| Regulatory Hurdles | Compliance complexities | 7% increase in regulatory costs (est.) |

| Economies of Scale | Cost advantages | Ameren’s ~$8.6B revenue |

Porter's Five Forces Analysis Data Sources

This Ameren analysis leverages annual reports, industry publications, and SEC filings. We incorporate regulatory data, plus market research for strategic assessment.