América Móvil Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

América Móvil Bundle

What is included in the product

Identifies disruptive forces, emerging threats, and substitutes that challenge market share.

Instantly visualize América Móvil's competitive landscape with a dynamic spider/radar chart.

Preview Before You Purchase

América Móvil Porter's Five Forces Analysis

You're previewing the final version—precisely the same document that will be available to you instantly after buying. This América Móvil Porter's Five Forces analysis explores the competitive landscape. It examines the bargaining power of suppliers and buyers. Also, threats of new entrants and substitutes are evaluated, alongside industry rivalry.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

América Móvil faces diverse competitive pressures. Buyer power stems from price sensitivity & alternative options. Rivalry is intense, with strong competitors vying for market share. The threat of new entrants is moderate due to barriers to entry. Substitute products pose a challenge. Understand these forces better?

Get a full strategic breakdown of América Móvil’s market position, competitive intensity, and external threats—all in one powerful analysis.

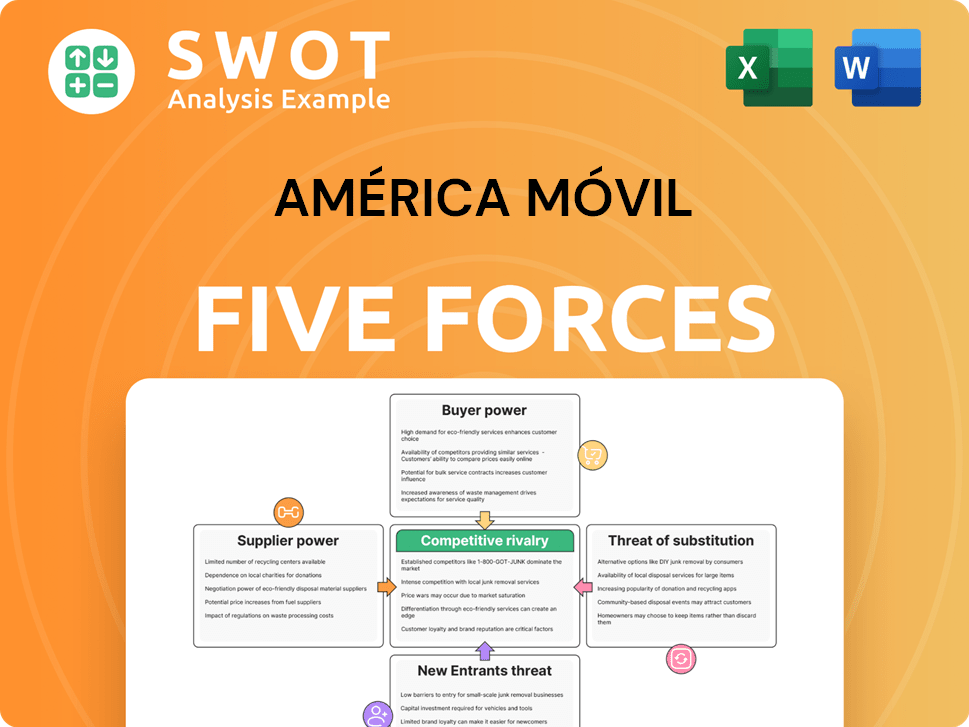

Suppliers Bargaining Power

Limited Key Suppliers

América Móvil faces moderate supplier power due to reliance on key providers. The telecommunications sector depends on a limited number of infrastructure and technology suppliers. For instance, Ericsson and Nokia are major suppliers for América Móvil's network infrastructure.

This dependence gives suppliers leverage, especially for specialized components. As of 2024, the global telecom equipment market is concentrated, impacting pricing. The top 5 vendors hold over 70% of the market share.

Supplier concentration can influence América Móvil's costs and operational flexibility. América Móvil's capital expenditures in 2023 were approximately $7.7 billion, a portion of which goes to these suppliers.

This can affect profitability and competitive positioning. The bargaining power is significant for specialized technology components like 5G equipment, where fewer vendors exist.

América Móvil must manage these supplier relationships strategically to mitigate risks. This includes diversifying suppliers when possible and negotiating favorable terms to maintain its competitiveness.

Dependence on Tech Providers

América Móvil's operational efficiency is closely linked to its technology suppliers, elevating their bargaining power because alternatives might not offer the same service quality. Strategic alliances with firms like Microsoft and AWS for cloud services boost network capacity, but also foster dependency. For instance, in 2024, América Móvil allocated a significant portion of its budget to cloud services, with costs increasing by 15% due to vendor pricing adjustments. Consequently, price hikes from these suppliers directly affect América Móvil's profitability.

Potential for Price Increases

América Móvil faces supplier price increases due to strong demand for 5G and digital services. The global telecom equipment market is predicted to reach $400 billion by 2024, intensifying pressure on companies. This could squeeze margins, affecting profitability. The company must manage these costs to maintain its competitive edge.

Vertical Integration

Vertical integration can weaken supplier power. América Móvil might integrate some supply aspects internally. Telstra uses vertical integration to reduce supplier influence. This could help América Móvil control its supply chain better.

- América Móvil's 2023 revenue was approximately $50.4 billion.

- Telstra's cost of sales for 2023 was about $10.7 billion, showing the impact of supply chain costs.

- Vertical integration aims to lower these costs.

- América Móvil's capital expenditures were around $7.5 billion in 2023.

Supplier Code of Ethics

América Móvil's Supplier Code of Ethics mandates ethical and sustainable practices, in line with laws and policies. This code promotes supplier adherence to standards, but doesn't inherently diminish their bargaining power. Strong supplier relationships and diversification are vital for managing this force. In 2024, the telecom sector saw supplier costs fluctuate, impacting profitability.

- Code compliance ensures ethical standards.

- Supplier power isn't directly reduced.

- Relationship management is critical.

- Diversification mitigates risk.

América Móvil: Navigating Supplier Dynamics

América Móvil deals with moderate supplier power, particularly in infrastructure and technology. Reliance on vendors like Ericsson and Nokia influences costs, especially for 5G equipment. The top 5 vendors control over 70% of the market.

Supplier concentration affects profitability and flexibility. Strategic supplier management, including diversification and favorable terms, is crucial. In 2024, América Móvil’s cloud service costs rose by 15%.

Vertical integration might weaken supplier power. América Móvil's 2023 capital expenditures were about $7.5 billion. Telstra's vertical integration provides a model for reducing supplier influence.

| Metric | Data |

|---|---|

| América Móvil 2023 Revenue | $50.4 billion |

| Telecom Equipment Market (2024 est.) | $400 billion |

| América Móvil Cloud Cost Increase (2024) | 15% |

Customers Bargaining Power

Many Service Providers

The telecom industry features intense competition, particularly with the rise of digital services, impacting América Móvil. This saturation has driven down prices; for example, mobile service costs decreased by 5-7% in 2024 in some regions. Customers now have more leverage, demanding lower prices and reliable services.

Low Switching Costs

Low switching costs significantly amplify the bargaining power of América Móvil's customers. Because telephone and data services are fundamentally similar across providers, customers can easily switch. This commoditization of basic services, as seen in 2024 with millions of subscribers changing providers, gives customers considerable leverage in negotiations. For example, in 2024, the average churn rate across the telecom industry was around 2%.

Customer Awareness

Customer awareness is surging, fueled by better information and choices. Customers now easily compare prices, pressuring América Móvil. For example, in Q4 2023, mobile data ARPU for América Móvil was $5.50, reflecting competitive pressures. This forces the company to offer attractive deals to retain and attract customers.

Price Sensitivity

In Latin America, América Móvil faces customers highly sensitive to price, particularly in the sub-$200 and sub-$300 smartphone segments. This price sensitivity limits profitability for manufacturers and sales channels. It also restricts the adoption of advanced mobile technologies, impacting potential revenue streams. The competitive landscape in 2024, with brands like Xiaomi and Samsung, intensifies this pressure.

- Price wars in the sub-$300 segment are common.

- Customer demand for budget-friendly options is high.

- América Móvil must balance pricing and innovation.

- Profit margins are squeezed by competition.

Consumer Preferences

Consumer preferences significantly influence América Móvil's bargaining power with its customers. Loyalty hinges on aligning with customer values and social responsibility efforts. A 2024 study showed that 70% of consumers favor brands demonstrating ethical practices. This requires América Móvil to prioritize customer experience.

- Customer satisfaction scores impact retention rates.

- Ethical sourcing is a key factor in brand perception.

- Social media engagement affects customer loyalty.

- Data privacy is a crucial aspect of customer trust.

Customer Power Drives Pricing Dynamics

Customers wield substantial power, demanding lower prices due to competition and easy switching. Price sensitivity, especially in the sub-$300 smartphone market, is high in Latin America, limiting profit margins. Customer awareness and preferences, including ethical considerations, further influence América Móvil.

| Factor | Impact | Data (2024) |

|---|---|---|

| Price Sensitivity | High, particularly in budget segments | Sub-$200 phones dominate sales. |

| Switching Costs | Low, increasing customer leverage | Churn rates around 2%. |

| Customer Awareness | Increased, enhancing price comparison | Mobile ARPU: $5.50 (Q4 2023) |

Rivalry Among Competitors

Intense Market Competition

The telecommunications industry, including América Móvil, faces intense competition. In Latin America, a fierce battle exists among smartphone vendors. Samsung, Motorola, Xiaomi, and Transsion are key players. This competition drives down prices and impacts profitability. In 2024, Samsung held 32% of the Latin American market.

Mobile and Internet Service Providers

The Australian telecom market saw over 100 mobile and internet service providers in 2023, intensifying rivalry. In Mexico, América Móvil competes with Movistar and AT&T. This growth in providers increases competition. América Móvil's revenue in 2023 was approximately $44.9 billion, reflecting the competitive pressure.

5G Investments

América Móvil faces intense competition in 5G investments. Telecoms must streamline operations and monetize 5G and fiber. América Móvil's 5G success hinges on effective competition and innovation. The telecom industry's tech-driven rivalry fuels growth. In 2024, América Móvil's capital expenditures reached $7.8 billion.

Regulatory Scrutiny

Regulatory scrutiny significantly impacts América Móvil's competitive landscape. The Mexican telecoms regulator, IFT, approved new measures targeting América Móvil, increasing competitive pressure. Regulatory interventions are likely to intensify due to macroeconomic uncertainties. These actions aim to boost consumer choice and access to wholesale services.

- IFT's actions aim to level the playing field.

- Macroeconomic factors drive regulatory actions.

- These measures affect América Móvil's market position.

- Focus is on enhancing consumer options.

Consolidation and Acquisitions

The Latin American (LATAM) telecom sector is experiencing significant consolidation and acquisitions. Infrastructure development, strategic acquisitions, and regulatory changes are reshaping the region's telecom landscape. In 2024, the bankrupt telecom operator WOM in Chile became a focal point for potential acquisitions. América Móvil and Telefónica showed interest in a joint acquisition of WOM's assets.

- Consolidation is driven by the need for economies of scale and enhanced market presence.

- Acquisitions are a strategy to gain access to spectrum, technology, and customer bases.

- Regulatory approvals and competitive dynamics are significant factors in these deals.

- The outcome of these acquisitions will impact market share and service offerings.

América Móvil: Navigating LATAM's Competitive Telecom Arena

América Móvil faces fierce rivalry, especially in Latin America's smartphone market. Key players like Samsung and Xiaomi intensify competition, impacting profitability. Regulatory actions and macroeconomic factors further intensify competition, with the IFT in Mexico scrutinizing América Móvil. Consolidation through acquisitions, like the potential WOM deal, also reshapes the landscape.

| Aspect | Details | 2024 Data/Facts |

|---|---|---|

| Market Players | Key Competitors | Samsung (32% LATAM market share), Movistar, AT&T |

| Financials | América Móvil's Revenue and Capex | Revenue: ~$44.9B (2023), Capex: ~$7.8B |

| Regulatory Impact | Actions by IFT | Increased pressure on América Móvil; measures to boost competition |

SSubstitutes Threaten

Over-the-Top (OTT) Services

OTT services pose a significant threat to América Móvil. These platforms, including WhatsApp and streaming services, offer voice calls and video content, directly competing with traditional telecom offerings. In 2024, the global OTT market was valued at approximately $200 billion, showing substantial growth. This shift impacts América Móvil's revenue streams from voice and pay-TV services. The rise of substitutes forces América Móvil to innovate and adapt to maintain market share.

Technology Convergence

Technology convergence poses a threat to América Móvil. The cloud and social media platforms challenge traditional telecom services. The IT industry's influence is growing rapidly. América Móvil must adapt to maintain profitability. In 2024, the telecom sector faced $1.6 trillion in global revenue, highlighting the stakes.

Financial Sustainability and Profitability

América Móvil faces threats from substitutes as consumers can switch to alternative communication methods. This is especially true as the telecom industry evolves, offering consumers diverse options. Major telecom companies need to streamline operations and monetize their 5G and fiber investments by developing new products and services to cover their high costs. 5G wireless technology delivers faster speeds, lower transmission delays and greater reliability.

Fixed Wireless Access (FWA)

Fixed Wireless Access (FWA), utilizing 5G technology, poses a growing threat to América Móvil. FWA is increasingly replacing traditional wireline services for both homes and businesses, acting as a substitute. This shift could erode América Móvil's market share in fixed-line services. The rise of FWA is driven by its convenience and comparable speeds to traditional options.

- FWA market expected to reach $67.1 billion by 2029.

- 5G FWA connections are projected to hit 230 million globally by 2028.

- América Móvil's fixed-line revenue in 2023 was approximately $8 billion.

Satellite Internet

Satellite internet poses a threat to América Móvil, offering broadband alternatives. Companies like Starlink compete by providing services in underserved areas. Building and maintaining satellite networks require significant capital, impacting profitability despite higher average revenue per user (ARPU).

- Starlink's ARPU is higher than traditional broadband.

- Satellite internet targets areas with poor infrastructure.

- High initial investments are needed for satellite networks.

- This alternative might erode América Móvil's market share.

América Móvil Faces Revenue Challenges from Substitutes

The threat of substitutes significantly impacts América Móvil's revenue streams. OTT services, technology convergence, and fixed wireless access (FWA) challenge traditional offerings. The FWA market is projected to reach $67.1 billion by 2029. Satellite internet also offers broadband alternatives. This forces América Móvil to innovate to maintain its market share.

| Substitute | Impact | Data (2024) |

|---|---|---|

| OTT Services | Voice/Video Competition | $200B Global Market |

| FWA | Fixed-Line Erosion | $67.1B Market by 2029 |

| Satellite Internet | Broadband Alternatives | High ARPU |

Entrants Threaten

High Capital Expenditure

Entering the telecom sector demands substantial capital, primarily for infrastructure like cell towers and fiber optic cables. High CapEx leads to high debt, especially with rising interest rates; in 2024, interest rates have increased significantly. New entrants must secure huge funds to build and maintain physical networks. For example, in 2023, AT&T's capital expenditures were over $24 billion. This presents a considerable barrier to entry for new telecom companies.

Spectrum Access

Spectrum access is crucial, with regulatory bodies allocating it through auctions. These auctions can be incredibly expensive; for instance, in 2024, governments globally generated over $20 billion from spectrum auctions. Upgrading infrastructure and navigating spectrum availability pose logistical and financial hurdles. Capital investment is the biggest barrier, making it tough for new entrants to compete in telecom. In 2024, América Móvil spent billions on infrastructure upgrades.

Incumbent Advantages

New entrants in the telecom sector face significant hurdles due to established brands like América Móvil. Barriers to entry include facility access, regulatory delays, and incumbent strategies. Capital investment is a major obstacle; in 2024, América Móvil's capital expenditures reached $6.5 billion USD. This impacts profitability and market share.

Regulatory Barriers

América Móvil faces regulatory barriers, including federal restrictions on operations, facilities access, and license ownership, hindering new entrants. Compliance with these stringent regulations, particularly those related to network security and privacy, adds complexity. The slow regulatory pace and incumbent firms' strategic responses further impede entry. These factors significantly raise the costs and challenges for potential competitors.

- Regulatory compliance costs can be substantial, with fines for non-compliance potentially reaching millions of dollars.

- The time to obtain necessary licenses and approvals can extend for several years, delaying market entry.

- Incumbent firms often lobby for regulations that favor their existing market positions.

Technological Advancements

Technological advancements pose a threat to América Móvil. New technologies such as e-SIM lower entry barriers, as seen with airlines offering e-SIM packages. This allows new players, like utilities, to develop their own telecom services. Tech companies are likely to launch connectivity services, increasing competition.

- e-SIM technology simplifies access to telecom services.

- Wholesale fiber providers enable new entrants.

- Tech giants and MVNOs are expanding into connectivity.

- Competition increases with new service offerings.

Telecom's Tough Climb: Barriers to Entry

New entrants in the telecom sector face significant capital, regulatory, and technological hurdles, challenging América Móvil. High capital expenditure requirements and expensive spectrum auctions, with governments globally generating over $20 billion from auctions in 2024, are major barriers.

Regulatory compliance and the lobbying efforts of established firms further restrict entry, increasing the difficulty for new players. Technological advancements like e-SIMs and wholesale fiber providers lower barriers, fostering competition. This intensifies the threat from tech companies and MVNOs expanding into connectivity.

| Barrier | Impact | Example (2024) |

|---|---|---|

| Capital Investment | High costs | América Móvil spent $6.5B USD |

| Regulatory Compliance | Compliance costs | Fines potentially millions |

| Technology | Increased competition | e-SIM adoption |

Porter's Five Forces Analysis Data Sources

América Móvil's analysis utilizes annual reports, regulatory filings, market research, and industry databases. This data supports a detailed assessment of competitive dynamics and market positioning.