Applied Materials Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Applied Materials Bundle

What is included in the product

Detailed analysis of each competitive force, supported by industry data and strategic commentary.

Duplicate tabs for different scenarios, helping to explore various market possibilities.

Full Version Awaits

Applied Materials Porter's Five Forces Analysis

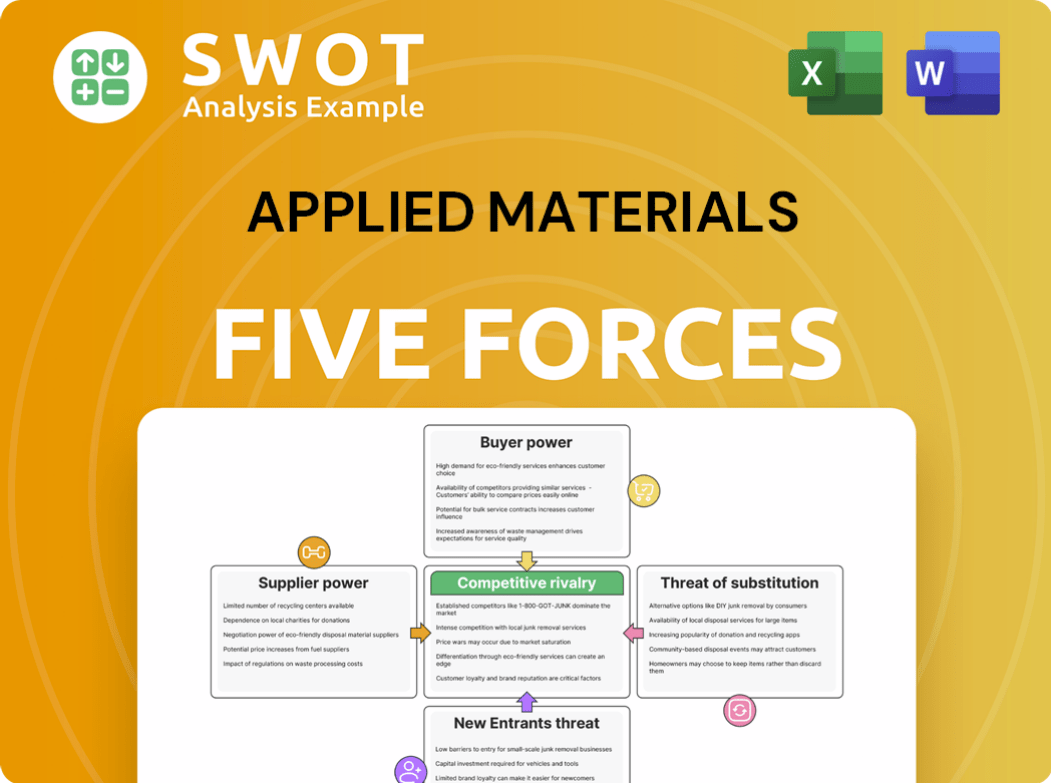

The preview showcases the complete Porter's Five Forces analysis of Applied Materials, including its competitive landscape.

This analysis examines the intensity of rivalry, threat of new entrants, and bargaining power of suppliers and buyers.

It also assesses the threat of substitute products or services within the semiconductor industry.

This document is the same professionally written analysis you'll receive—fully formatted and ready to use.

The insights presented here are identical to the ones you will access instantly after purchase.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Applied Materials (AMAT) operates in a highly competitive semiconductor equipment market, significantly influenced by powerful buyers like major chipmakers. Supplier power is moderate, with concentration among key component providers. The threat of new entrants is relatively low due to high barriers, including capital intensity and technology. Substitute products pose a limited threat, as specialized equipment has few direct replacements. Rivalry is intense, driven by a few dominant players vying for market share and innovation leadership.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Applied Materials’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited critical supplier options

Applied Materials depends on specialized suppliers for components and materials, though alternative options may be limited. This scarcity gives suppliers some pricing and contract leverage. Suppliers hold more power when their offerings are unique. For instance, in 2024, Applied Materials' cost of revenues was $17.07 billion, reflecting supplier influence.

Supplier concentration varies

Applied Materials operates within a sector where supplier concentration varies. If key inputs are controlled by a few suppliers, they gain leverage. This is particularly true for specialized components. In 2024, the semiconductor equipment market saw shifts in supplier dynamics. Switching costs also affect supplier power.

Impact of raw material costs

Raw material costs, like those for silicon wafers, significantly influence supplier pricing. Suppliers might increase prices, squeezing Applied Materials' profit margins. For example, in 2024, silicon prices saw a 10% increase. Applied Materials counters this with long-term deals and diversified sourcing.

Vertical integration by suppliers

If suppliers integrate forward, their bargaining power could rise. They might favor their own needs or offer better prices to Applied Materials' rivals. This is less probable in the specialized equipment sector. Applied Materials' revenue in 2024 was about $6.7 billion.

- Forward integration can shift power dynamics.

- Suppliers might favor internal needs.

- Competitive pricing could impact Applied Materials.

- Specialized areas limit this risk.

Long-term relationships mitigate risk

Applied Materials likely prioritizes long-term supplier relationships to secure a reliable supply chain and favorable terms. These relationships can mitigate the risk of suppliers exploiting their position. Building trust and mutual benefits are key to these partnerships. This approach is critical in the semiconductor industry. In 2024, Applied Materials spent $14.3 billion on materials, parts, and services.

- Long-term contracts help stabilize supply chains.

- Strong relationships reduce supplier opportunism.

- Mutual benefits foster trust and cooperation.

- This strategy is vital in a volatile market.

Supplier Dynamics Impacting Costs and Stability

Applied Materials faces supplier power, influenced by component uniqueness and market concentration. In 2024, silicon price increases and material costs ($14.3B) highlighted this. Long-term contracts and relationships are crucial to mitigate supplier leverage, especially in the volatile semiconductor market.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Supplier Uniqueness | Increases power | Specialized components |

| Material Costs | Affects margins | $17.07B cost of revenues |

| Mitigation | Builds stability | $14.3B spent on materials |

Customers Bargaining Power

Concentrated customer base

Applied Materials faces a concentrated customer base dominated by major semiconductor manufacturers. These large customers, such as TSMC, Intel, and Samsung, have considerable purchasing power. In 2024, TSMC accounted for approximately 26% of Applied Materials' sales. This concentration allows these customers to negotiate favorable pricing and terms, impacting Applied Materials' profitability.

High switching costs for customers

While customers hold some sway, the high costs of switching equipment vendors limit their power. Integrating new equipment is complex and time-consuming, creating "stickiness." This gives Applied Materials some protection. In 2024, Applied Materials reported $26.7 billion in net sales, showing its market position. The company's strong customer relationships also add to this advantage.

Importance of equipment performance

The performance of Applied Materials' equipment is vital for its customers' manufacturing. Poor equipment performance gives customers leverage to negotiate prices or seek improvements. For example, in 2024, Applied Materials' revenue was $6.71 billion in Q1 alone. Customers' bargaining power increases with any performance shortcomings.

Customer profitability affects leverage

The profitability of Applied Materials' customers, like semiconductor manufacturers, significantly impacts their bargaining power. Customers experiencing economic downturns or reduced demand often seek to cut costs, including negotiating lower prices for equipment. This can put pressure on Applied Materials' margins and profitability, especially in competitive markets. For example, in 2024, the semiconductor industry faced fluctuating demand, influencing customer negotiation strategies.

- Semiconductor industry's cyclical nature impacts customer bargaining power.

- Economic downturns drive customers to seek price reductions.

- Applied Materials' margins can be squeezed by customer demands.

- Competitive market dynamics intensify price negotiations.

Customization and collaboration

Applied Materials frequently works hand-in-hand with its customers, designing solutions tailored to their specific needs. This collaborative approach fosters strong relationships, making it less appealing for customers to seek alternatives from rivals. Customization establishes a mutual reliance between Applied Materials and its clients. In 2024, Applied Materials reported a revenue of approximately $26.6 billion, demonstrating the scale of these customer relationships.

- Customer-Specific Solutions: Applied Materials offers highly customized products.

- Partnership Approach: The company emphasizes collaboration with clients.

- Retention Benefits: Customization increases customer loyalty.

- Mutual Dependence: These relationships create a reliance on both sides.

Applied Materials: Customer Power & Sales Dynamics

Applied Materials faces significant customer bargaining power due to a concentrated customer base, with major semiconductor manufacturers like TSMC holding considerable influence. TSMC accounted for around 26% of Applied Materials' sales in 2024. However, the high switching costs somewhat limit this power, creating "stickiness".

| Aspect | Details | 2024 Data |

|---|---|---|

| Customer Concentration | Key clients like TSMC dominate sales | TSMC: ~26% of sales |

| Switching Costs | High costs limit customer bargaining power | Complex integration of new equipment |

| Revenue | Applied Materials' total revenue | ~$26.7B in 2024 |

Rivalry Among Competitors

Intense competition in the industry

The semiconductor equipment industry is fiercely competitive. Applied Materials faces strong rivals, impacting pricing and innovation. This rivalry is evident in the constant push for market share. In 2024, Applied Materials' revenue was approximately $26.6 billion, highlighting the stakes. The competitive landscape demands constant adaptation and improvement.

Key competitors include ASML and Lam Research

Applied Materials contends with strong rivals like ASML and Lam Research. These firms offer analogous equipment and services, heightening competition. For example, ASML's 2024 revenue reached approximately €27.6 billion, highlighting the scale of competition. Tokyo Electron is also a major player. The dynamics among these competitors are crucial.

Focus on innovation and technology

Applied Materials faces intense competition, pushing it to invest heavily in R&D. Innovation is key to differentiating products and attracting customers. The company's R&D spending in fiscal year 2024 was approximately $2.8 billion. Continuous innovation is vital to maintaining its market share.

Price competition exists

Price competition in the semiconductor equipment industry, though tempered by technological innovation, remains a factor. Applied Materials, like its rivals, must contend with price pressures, particularly during economic slowdowns when customers scrutinize spending. The company's ability to balance cutting-edge technology with competitive pricing is crucial for maintaining market share. For example, in 2024, Applied Materials' gross margin was around 46%, indicating the company's ability to manage pricing effectively despite competitive pressures. This balance is vital for long-term profitability and growth.

- Price competition can intensify during economic downturns.

- Applied Materials must balance innovation with competitive pricing.

- Gross margin is a key indicator of pricing effectiveness.

- Customers' cost reduction pressures impact pricing strategies.

Importance of customer relationships

Customer relationships are crucial in competitive markets, and Applied Materials prioritizes them. They aim for long-term partnerships and excellent support to keep customers. This focus helps Applied Materials stand out from competitors. Their strong relationships act as a key differentiator, securing business. In 2024, Applied Materials reported customer satisfaction rates above 90%.

- High customer retention rates, often exceeding industry averages.

- Significant repeat business from existing clients.

- Positive customer testimonials and referrals.

- Investment in customer service and support infrastructure.

Applied Materials: Navigating the Semiconductor Showdown

Competitive rivalry at Applied Materials is intense, driven by firms like ASML and Lam Research. These companies compete fiercely on product innovation and market share. Applied Materials' ability to navigate this competition, and maintain healthy margins, is key to its success. In 2024, Applied Materials' gross margin stood at approximately 46%, indicating efficient management amid rivalry.

| Metric | Applied Materials (2024) | Competitor Example |

|---|---|---|

| Revenue | $26.6B | ASML: €27.6B |

| R&D Spending | $2.8B | Lam Research: $1.8B |

| Gross Margin | 46% | Lam Research: ~47% |

SSubstitutes Threaten

Limited direct substitutes

Applied Materials faces limited direct substitutes due to its specialized offerings in semiconductor and display manufacturing. The company's unique equipment and processes are crucial for these industries. This specialized nature reduces the risk of customers switching to alternative solutions. In 2024, the semiconductor equipment market, where Applied Materials is a key player, grew, indicating strong demand and limited viable substitutes. The company reported $6.7 billion in revenue in Q1 2024.

Alternative manufacturing technologies

Alternative manufacturing technologies pose a long-term threat to Applied Materials. New chip architectures or manufacturing processes could reduce the need for their equipment. While not an immediate concern, they require monitoring. For instance, in 2024, investment in advanced packaging technologies increased, potentially changing equipment demand.

In-house development by customers

Large customers like Intel might develop some equipment internally, reducing reliance on Applied Materials. This strategy demands considerable investment and expertise. In 2024, Intel's R&D spending was approximately $18 billion. This threat is more potential than a current widespread issue. Most customers lack the resources to replicate Applied Materials' comprehensive offerings.

Software and process optimization

Software and process optimization poses a threat to Applied Materials. Advances in these areas can boost the efficiency of existing equipment, potentially reducing the need for new purchases. This indirect substitution affects demand by postponing the need for new investments in equipment. These improvements allow companies to get more out of their current resources. This can be seen in the semiconductor industry, where optimizing processes has extended the lifespan of older fabs.

- In 2024, companies invested heavily in software to improve equipment performance, extending the lifespan of existing equipment.

- Process optimization led to 10-15% efficiency gains in some fabs, reducing the need for new equipment.

- The market for software-based efficiency solutions grew by 12% in 2024, indicating the increasing importance of this threat.

- Applied Materials’ competitors are also investing in software and process optimization technologies to maintain their market share.

Materials science advancements

Advancements in materials science pose a long-term threat. These breakthroughs could create new materials. These materials may need different manufacturing processes. This could make some of Applied Materials' equipment less useful.

- In 2024, Applied Materials invested $2.5 billion in R&D.

- Materials science R&D spending globally reached $300 billion.

- New materials could disrupt the semiconductor industry.

- Applied Materials' revenue in 2024 was $26.6 billion.

Applied Materials: Facing the Substitute Threat

The threat of substitutes for Applied Materials is multifaceted, involving both direct and indirect competition. Software and process optimization significantly impact demand, with the market for such solutions growing by 12% in 2024. Alternative technologies and large customer in-house development present potential challenges, though not immediately widespread.

| Substitute Type | Impact | 2024 Data |

|---|---|---|

| Software/Process Optimization | Reduces need for new equipment | 12% market growth for efficiency solutions |

| Alternative Technologies | Long-term equipment changes | $2.5B R&D investment by Applied Materials |

| In-House Development | Reduced reliance on AMAT | Intel's $18B R&D spend |

Entrants Threaten

High barriers to entry

The semiconductor equipment industry is tough to break into. Big money is needed, along with specialized tech skills and existing customer trust. Newcomers face an uphill battle. This makes it hard for others to challenge Applied Materials. In 2024, the capital expenditure of Applied Materials was about $1.1 billion.

Patents and intellectual property

Applied Materials and its rivals have extensive patents and intellectual property, hindering new entrants from creating similar tech. This intellectual property significantly raises the entry barrier. Patent protection is a key factor, with Applied Materials having approximately 11,700 active patents worldwide as of 2024. This protects its innovations and market position.

Economies of scale

Applied Materials benefits from economies of scale, crucial for manufacturing and R&D. Established companies have cost advantages, making it hard for new entrants. For example, in 2024, Applied Materials invested heavily in advanced manufacturing, increasing efficiency. Scale is a significant barrier to entry in this industry.

Established customer relationships

Applied Materials benefits from established customer relationships, a significant barrier for new entrants. These relationships, built over years, foster trust and loyalty, making it difficult for newcomers to compete. Customers in the semiconductor industry often prefer proven suppliers for critical equipment and services, which is the core of Applied Materials’s business. The company reported a revenue of $6.71 billion in Q1 2024, emphasizing its strong customer base.

- Customer loyalty reduces switching costs.

- Long-term contracts enhance stability.

- Established trust and reliability.

- New entrants face high barriers.

Regulatory hurdles and compliance

Regulatory hurdles and compliance significantly impact the threat of new entrants in the semiconductor industry. Navigating the complex web of regulations poses a considerable challenge for newcomers. Compliance with these standards increases both the cost and complexity of market entry. This regulatory burden acts as a substantial barrier, potentially deterring new firms from entering the field.

- The semiconductor industry faces various compliance requirements.

- Compliance increases the cost of market entry.

- Regulations act as a barrier to entry.

- New entrants must navigate complex rules.

Semiconductor Equipment: High Barriers to Entry

The semiconductor equipment industry poses high entry barriers due to capital needs, intellectual property, and economies of scale. Applied Materials’ $1.1B in capital expenditures in 2024 showcases these challenges. Regulatory compliance further complicates market entry for newcomers.

| Factor | Impact on New Entrants | Data Point (2024) |

|---|---|---|

| Capital Requirements | High Investment Needed | $1.1B (CapEx) |

| Intellectual Property | Patents Hinder Entry | ~11,700 Patents |

| Economies of Scale | Cost Advantages | Revenue of $6.71B (Q1) |

Porter's Five Forces Analysis Data Sources

This analysis utilizes public filings (SEC), market research reports, and industry news for comprehensive insights. These diverse sources support assessments of rivalry, bargaining power, and threat dynamics.