Capital One Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Capital One Bundle

What is included in the product

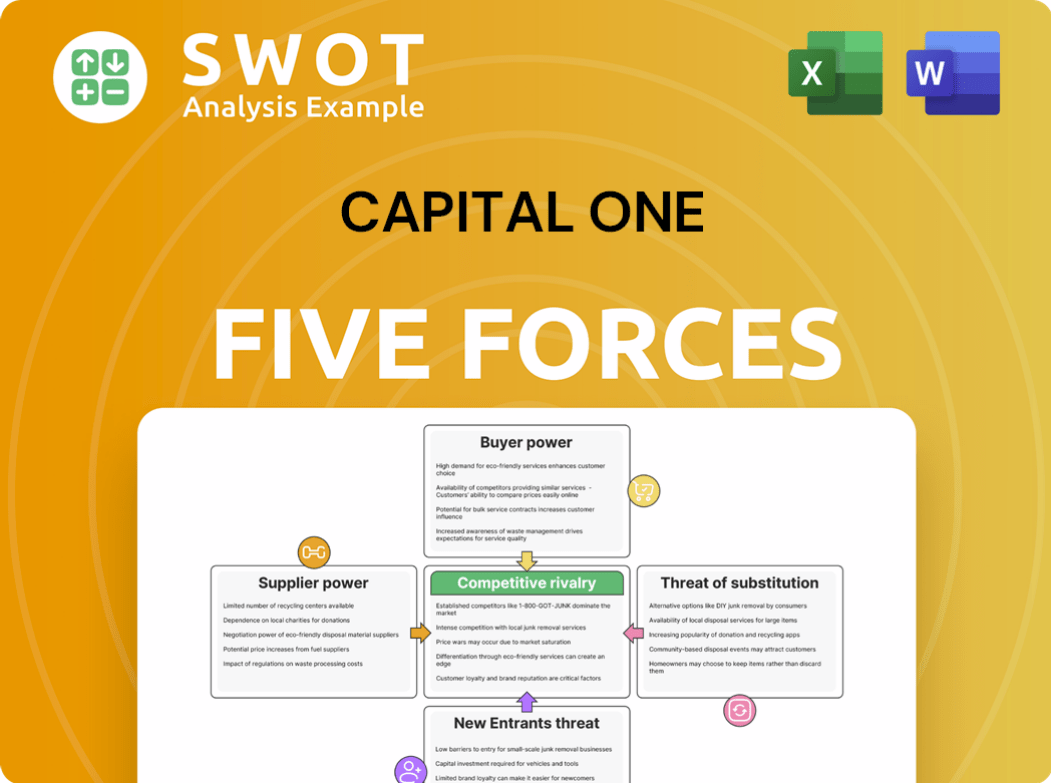

Analyzes Capital One's competitive environment, including rivalries, buyer power, and potential market entrants.

Quickly understand strategic pressure with an intuitive spider chart.

What You See Is What You Get

Capital One Porter's Five Forces Analysis

This is the complete Capital One Porter's Five Forces analysis. The preview showcases the identical, professionally written document you'll receive. It's fully formatted and ready for immediate use. No alterations are needed; the document is ready to download right after purchase. Expect no surprises; it's the same comprehensive analysis.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

Capital One's competitive landscape is shaped by diverse forces. Bargaining power of buyers, like consumers, is moderately high due to competitive credit card options. Threat of new entrants remains moderate, facing established brands and regulatory hurdles. The intensity of rivalry among existing competitors is high, fueling innovation and marketing. Supplier power, particularly from payment networks, is significant. The threat of substitute products, such as digital payment platforms, is growing.

This preview is just the starting point. Dive into a complete, consultant-grade breakdown of Capital One’s industry competitiveness—ready for immediate use.

Suppliers Bargaining Power

Limited Banking Technology Providers

Capital One faces concentrated power from banking tech providers like Fiserv and FIS. These firms offer essential services, including core processing and digital platforms. Switching costs are high, reducing Capital One's ability to negotiate favorable terms. In 2024, Fiserv's revenue was approximately $19.9 billion, reflecting their market dominance.

Dependence on Core Banking Software

Capital One's reliance on external vendors for core banking software significantly elevates supplier power. Outsourcing key systems like core transaction processing and digital banking platforms creates dependency. A system failure could severely impact Capital One's operations. In 2024, Capital One's IT spending reached approximately $5.5 billion, underscoring this dependence.

High Switching Costs

Changing core banking systems is costly, with expenses potentially reaching $250 million. Software licensing alone can cost $5-15 million. Implementation services can range from $20-50 million. These high costs reduce Capital One's ability to switch suppliers. This situation increases the bargaining power of the technology providers.

Concentrated Market of Infrastructure Suppliers

Capital One faces a concentrated technology and infrastructure market. The top three providers hold a significant market share, impacting Capital One's choices. This concentration increases reliance on these key suppliers, reducing negotiation leverage. Limited alternatives mean accepting supplier-set terms.

- 2024: Top 3 cloud providers (AWS, Azure, Google Cloud) control ~65% of global market share.

- Capital One's IT spending: Over $5 billion annually, making it a significant buyer.

- Limited supplier options: Fewer vendors means less competitive pricing for Capital One.

- Negotiating power: Capital One must often accept standard terms, impacting costs.

Suppliers' Innovation Capabilities

Capital One's competitive advantage hinges on its suppliers' innovation capabilities. Suppliers' ability to innovate significantly impacts Capital One's edge in the market. With financial institutions increasingly depending on fintech innovation from suppliers, maintaining strong supplier relationships is critical. This reliance bolsters suppliers' bargaining power, influencing Capital One's operational strategies. For instance, in 2024, fintech spending is projected to reach $170 billion, highlighting the importance of supplier innovation.

- Fintech spending is projected to reach $170 billion in 2024.

- Supplier innovation directly affects Capital One's competitive edge.

- Strong supplier relationships are crucial for fintech advancements.

- Reliance on suppliers strengthens their bargaining power.

Capital One's Supplier Dynamics: A $170B Fintech Impact

Capital One faces substantial supplier power, primarily from banking tech providers and IT vendors. High switching costs, potentially up to $250 million, and limited alternatives for core systems like transaction processing and digital platforms reduce Capital One's negotiation leverage.

The concentration in the technology market further enhances supplier power, with a few dominant firms holding a large market share. In 2024, fintech spending is projected to reach $170 billion, underscoring the importance of supplier innovation, which directly impacts Capital One's competitive edge and operational strategies.

Capital One's reliance on suppliers for innovation, particularly in fintech, elevates their bargaining position, influencing costs and strategic decisions. Strong supplier relationships are critical for fintech advancements. The top 3 cloud providers (AWS, Azure, Google Cloud) control approximately 65% of global market share in 2024.

| Aspect | Details |

|---|---|

| Key Suppliers | Fiserv, FIS, Cloud Providers (AWS, Azure, GCP) |

| Market Concentration | Top 3 Cloud Providers: ~65% market share (2024) |

| 2024 Fintech Spending | Projected to reach $170 Billion |

Customers Bargaining Power

Customer Price Sensitivity

Customers are highly price-sensitive, especially regarding interest rates, fees, and rewards. With rising living costs, consumers actively seek better deals. In 2024, the Federal Reserve's rate hikes influenced consumer spending and borrowing. Capital One must offer competitive terms to attract and retain customers, impacting its pricing power.

Availability of Alternatives

Customers wield significant power due to the abundance of alternatives. They can easily switch between major banks, credit unions, and fintech firms. Neobanks are a growing threat, offering competitive rates; in 2024, digital banking users grew by 15%. This competition pushes Capital One to keep its offerings appealing to retain customers.

Access to Information

Customers' access to information on financial products is now unprecedented. Online platforms and comparison websites provide easy access, empowering informed decisions. This transparency lets customers negotiate better terms. For example, in 2024, online banking adoption reached 70% among U.S. adults, increasing price sensitivity.

Switching Costs

Switching costs for customers in the financial sector are notably low, bolstering their bargaining power. Digital banking and mobile payment solutions have simplified the process of changing financial providers, reducing friction. This ease of switching necessitates that Capital One consistently offers competitive value to retain its customer base. For instance, a 2024 study indicates that 68% of consumers are open to switching banks for better rates or services.

- Ease of Switching

- Digital Banking Impact

- Competitive Pressure

- Customer Retention

Demand for Personalized Services

Capital One faces strong customer bargaining power due to the demand for personalized services. Customers now expect tailored financial solutions, which increases their influence on product offerings. Modernizing banking platforms requires a focus on customer preferences to ensure usability. Capital One must adapt to evolving customer needs to retain its base.

- Personalized services are crucial for customer retention, especially with younger demographics.

- Capital One's digital banking services are used by over 60% of its customer base.

- Customer satisfaction scores significantly impact the adoption of new financial products.

- Investment in customer-centric technology helps Capital One stay competitive.

Customer Power: The Digital Shift

Customers have substantial bargaining power due to price sensitivity and easy access to alternatives. Digital platforms and financial comparison sites offer unprecedented information, driving informed decisions. Low switching costs and the demand for personalized services further strengthen customer influence.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Price Sensitivity | Influences decisions on rates, fees. | 70% of consumers compare rates online. |

| Switching Costs | Low costs boost customer bargaining power. | 68% willing to switch banks for better deals. |

| Digital Banking | Empowers informed decisions. | Online banking adoption: 70%. |

Rivalry Among Competitors

Intense Competition

The banking and financial services sector is fiercely competitive, with many entities fighting for market share. Capital One faces rivals like JPMorgan Chase, Bank of America, and Citigroup. This competition forces Capital One to differentiate. In 2024, the industry saw a squeeze on net interest margins, intensifying the need for competitive strategies.

Technological Disruption

Digital transformation is reshaping banking, and Capital One faces intense rivalry from fintechs and neobanks. These competitors offer innovative solutions, pressuring Capital One to adapt. Banks must embrace an AI-first strategy to stay competitive. In 2024, Capital One invested $7.6 billion in technology to enhance its digital capabilities.

Mergers and Acquisitions

Capital One's bid to acquire Discover, if successful, boosts its market presence, but heightens rivalry. This merger aims to challenge Visa and Mastercard, intensifying competition in the credit card sector. However, regulatory hurdles could reshape the deal's scope. In 2024, mergers and acquisitions in the financial sector are under increased scrutiny.

Focus on Innovation

Competitive rivalry significantly fuels innovation within the financial sector. Capital One faces constant pressure to innovate its products and services to stay ahead. This includes offering compelling rewards programs, competitive interest rates, and superior customer service. The need to differentiate and innovate necessitates substantial investments in R&D.

- Capital One's R&D spending in 2023 was approximately $6.5 billion, reflecting a strong commitment to innovation.

- The company launched new digital tools and features in 2024 to enhance customer experience.

- Capital One's competitors, such as Chase and American Express, also invest heavily in innovation to maintain market share.

Marketing and Customer Acquisition Costs

Capital One faces fierce rivalry, evident in high marketing and customer acquisition costs. The company spends heavily on marketing to attract customers. This spending, coupled with rewards programs, impacts profitability amid intense competition. The need to retain customers through costly marketing strategies is a constant pressure.

- Capital One's marketing expenses were substantial, reaching billions of dollars annually, reflecting the competitive landscape.

- Customer acquisition costs are high, driven by the need to offer attractive rewards and incentives to gain new customers.

- Intense competition forces continuous innovation in marketing and rewards, increasing costs.

- Profitability is directly affected by these high costs, requiring efficient operations to offset expenses.

Capital One Navigates a Competitive Tech-Driven Landscape

Capital One's competitive landscape is marked by intense rivalry with major players and fintech disruptors. The company strategically invests in technology and innovation, spending around $7.6 billion in 2024 on tech. This includes digital tools and customer experience enhancements. Mergers, like the Discover acquisition bid, aim to boost market presence amidst regulatory scrutiny.

| Factor | Impact | 2024 Data |

|---|---|---|

| Rivalry Intensity | High due to numerous competitors | Net interest margins squeezed |

| Digital Competition | Increased pressure to innovate | $7.6B tech investment by Capital One |

| M&A Activity | Reshapes market dynamics | Increased regulatory scrutiny |

SSubstitutes Threaten

Rise of Fintech Platforms

Fintech platforms and digital payment solutions are increasingly substituting traditional banking services. The global fintech market, valued at $194.1 billion, is projected to grow substantially. These platforms offer alternatives for managing finances, payments, and credit access, posing a threat to Capital One's traditional model. In 2024, digital payments continue to surge, intensifying competition.

Mobile Payment Apps

Mobile payment apps pose a significant threat to Capital One. Apps like Apple Pay, PayPal, and Venmo offer convenient alternatives. In 2024, mobile payment transactions surged, with PayPal processing $388 billion in payments. This growth reduces reliance on traditional credit card use. The seamless payment experience offered by these apps is attractive to consumers.

Cryptocurrency and Blockchain

Cryptocurrency and blockchain pose a growing threat as substitutes to traditional banking services. The cryptocurrency market hit a $1.7 trillion market capitalization in 2024, showing significant disruptive potential. These technologies offer decentralized alternatives, appealing to customers wanting more control and flexibility. This shift could lead to increased competition for Capital One.

Peer-to-Peer Lending

Peer-to-peer (P2P) lending poses a threat to Capital One. P2P platforms offer credit alternatives, sidestepping traditional banks. The global P2P lending market is projected to reach $558.4 billion by 2027, showing significant growth. These platforms connect borrowers and lenders directly. They often provide better rates and terms.

- Market growth: The P2P lending market is expected to increase substantially.

- Competitive rates: P2P platforms often offer more favorable terms.

- Direct connection: These platforms facilitate direct interaction between borrowers and lenders.

Digital Payment Solutions

Digital payment solutions pose a considerable threat to Capital One. Platforms such as Stripe and Square are gaining traction. They facilitate online transactions, which competes with traditional banking services. These platforms offer innovative solutions and are rapidly growing.

- In 2024, the global digital payments market was valued at $8.04 trillion.

- Stripe processed over $1 trillion in payments in 2023.

- Square's revenue reached $20.3 billion in 2023.

- The digital payments sector is projected to reach $14.1 trillion by 2028.

Alternatives Challenging Capital One's Dominance

Capital One faces threats from various substitutes, including digital payments and fintech platforms. These alternatives are growing rapidly, such as the digital payments market, valued at $8.04 trillion in 2024. Cryptocurrency and P2P lending also compete by offering alternative financial solutions. This competition pressures Capital One to innovate.

| Substitute | Market Size/Value (2024) | Key Players |

|---|---|---|

| Digital Payments | $8.04 trillion | Stripe, Square, PayPal, Apple Pay |

| Fintech | $194.1 billion (Global) | Various fintech platforms |

| Cryptocurrency | $1.7 trillion (Market Cap) | Bitcoin, Ethereum, etc. |

Entrants Threaten

High Regulatory Barriers

The banking sector is heavily regulated, creating significant hurdles for new entrants. As of 2024, Basel III rules set strict capital ratios. These regulations demand substantial capital and compliance, which discourages new firms. Meeting these standards requires substantial upfront investment.

Significant Capital Requirements

New banks and financial services providers face substantial capital needs to enter the market, which includes meeting regulatory standards and financing their operations. In 2024, the average capital requirement for starting a new bank in the United States can range from $20 million to over $100 million, depending on the business model and regulatory environment. This financial barrier protects existing entities like Capital One by deterring new competitors. The high initial investment makes it difficult for new firms to compete efficiently.

Brand Recognition and Customer Loyalty

Capital One, as an established bank, enjoys robust brand recognition and customer loyalty, a significant barrier for new entrants. Their market position is strengthened by diversification, innovation, and a customer-focused strategy. In 2024, Capital One's brand value was estimated at over $20 billion, reflecting strong customer trust. The highly regulated financial sector requires substantial time and resources for newcomers to build trust and gain market share.

Technological Expertise

New entrants in the banking sector face a significant hurdle: technological expertise. Capital One, for example, heavily invests in AI, with plans to spend approximately $1.5 billion on technology in 2024. This AI-first strategy is crucial for customer engagement and efficiency. The necessity for advanced technology and digital capabilities forms a substantial barrier to entry.

- AI adoption is growing, with a projected global market size of $1.8 trillion by 2030.

- Capital One's tech spending shows the financial commitment required.

- Digital capabilities are essential for modern banking operations.

- New entrants struggle to match established players' tech infrastructure.

Economies of Scale

Existing large banks, like Capital One, leverage significant economies of scale, giving them a competitive edge in pricing and service offerings. These established institutions can spread their operational costs over a vast customer base, enhancing efficiency. New entrants often struggle to replicate this cost-effectiveness, facing a disadvantage in attracting and retaining customers. This disparity in scale presents a considerable barrier to entry within the financial sector.

- Capital One's community benefits plan is valued at $265 billion over five years, highlighting its scale.

- Economies of scale allow established banks to offer lower interest rates and fees.

- New digital banks face challenges matching the operational efficiency of traditional banks.

- Larger banks can invest more in technology and marketing to maintain their competitive advantage.

Capital One: Barriers to Entry

The threat of new entrants is moderate for Capital One due to significant barriers.

High capital requirements and regulations like Basel III, which demand substantial upfront investment, limit new competition.

Capital One's brand recognition, tech spending, and economies of scale further protect its market position.

| Barrier | Impact on Capital One | 2024 Data Point |

|---|---|---|

| Regulations | Limits new entrants | Basel III compliance costs are high |

| Capital Needs | Protects market share | New bank start-up costs $20M-$100M |

| Brand & Scale | Competitive advantage | Capital One's brand value is $20B+ |

Porter's Five Forces Analysis Data Sources

Our analysis leverages diverse data, including annual reports, financial statements, market research, and industry publications for a detailed view.