Century Aluminum Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Century Aluminum Bundle

What is included in the product

Analyzes competitive pressures, supplier & buyer power, threats & entry barriers specific to Century Aluminum.

Instantly analyze competitive pressures with a dynamic, color-coded threat level system.

Preview the Actual Deliverable

Century Aluminum Porter's Five Forces Analysis

This is the complete Porter's Five Forces analysis of Century Aluminum. The document you see is the identical file you'll receive after purchase. It provides a comprehensive overview of the industry's competitive landscape. Ready for download, analyze, and use right away. No alterations needed.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

Century Aluminum faces a complex landscape. Buyer power, fueled by pricing pressures, is a key factor. Supplier influence, particularly raw material costs, also shapes profitability. Competition is fierce from global aluminum producers. The threat of substitutes, like plastics, adds another dimension. New entrants present a moderate risk, dependent on capital requirements.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Century Aluminum’s competitive dynamics, market pressures, and strategic advantages in detail.

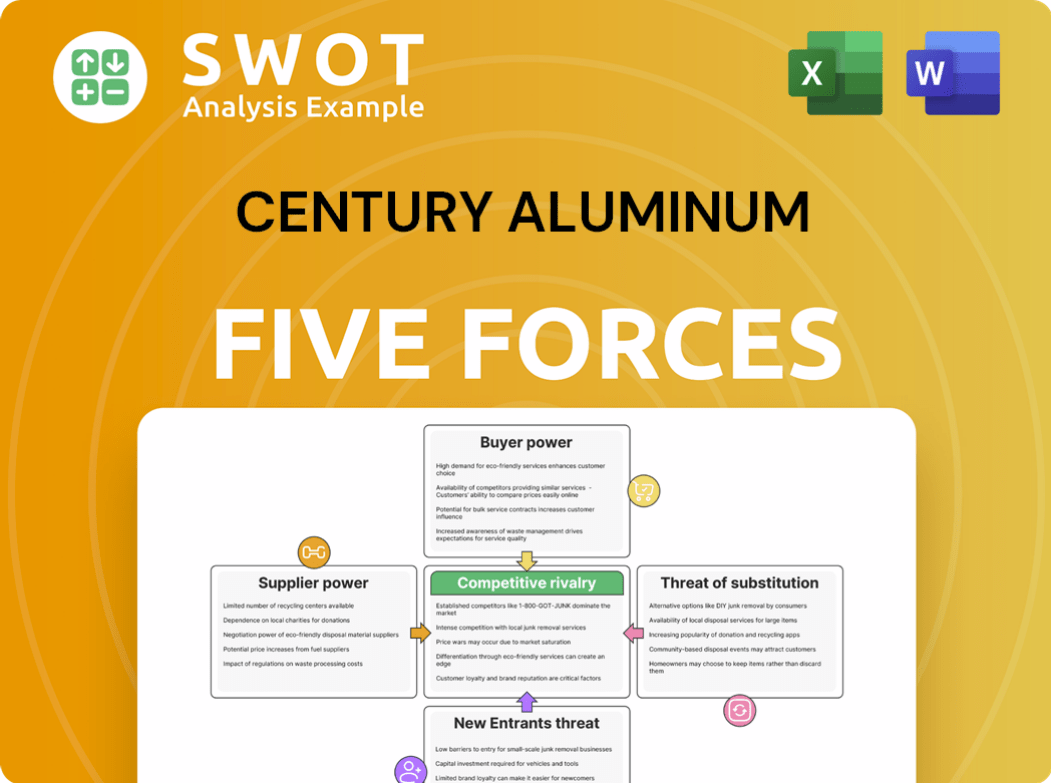

Suppliers Bargaining Power

Limited Supplier Base

Century Aluminum's reliance on a few bauxite and alumina suppliers, mainly in Australia, Brazil, China, and Guinea, gives these suppliers leverage. With limited options, Century is vulnerable to price hikes or supply disruptions. In 2024, Australia and China accounted for over 60% of global alumina production, highlighting the concentration. Suppliers’ power is amplified by geographic risks.

Long-Term Contracts

Century Aluminum reduces supplier power with long-term contracts, typically spanning 5-7 years. These agreements often feature fixed pricing, securing a substantial portion of their supply. For example, in 2024, a significant 65% of their raw material purchases were under such contracts. However, this strategy may limit flexibility if market dynamics shift.

Dependence on Specific Regions

Century Aluminum's dependence on regions like Latin America and Southeast Asia for alumina creates supplier power. Political instability, stricter environmental rules, and logistical hurdles in these areas increase supply risk. A disruption in these regions could greatly affect Century's output and expenses. For instance, in 2024, alumina prices fluctuated due to regional supply chain issues.

Potential Price Volatility

The prices of key raw materials like bauxite and alumina are volatile, affecting Century Aluminum's profitability. Transportation costs also introduce uncertainty. Managing this volatility is crucial for maintaining stable profit margins. For example, in 2024, alumina prices fluctuated significantly.

- Bauxite prices are influenced by global supply and demand dynamics.

- Alumina price volatility impacts production costs directly.

- Transportation costs can vary based on fuel prices and shipping availability.

- Effective hedging strategies are key to mitigating these risks.

Supplier Integration

Century Aluminum's relationship with Glencore, its primary alumina supplier and a major purchaser of its North American production, is complex. This integration, though potentially stabilizing supply, creates significant reliance on Glencore. Any operational or financial challenges at Glencore could directly impact Century. This close relationship warrants careful monitoring.

- Glencore supplied approximately 80% of Century's alumina needs in 2024.

- Glencore's revenue in 2024 was around $221 billion.

- Century's reliance on Glencore increases its vulnerability to supplier-related risks.

Supplier Risks Loom for Aluminum Producer

Suppliers hold considerable power over Century Aluminum, especially for alumina and bauxite. Dependence on key suppliers, such as Glencore, can lead to vulnerability. Long-term contracts and hedging mitigate some risks, but price volatility remains a concern.

| Factor | Impact on Century | 2024 Data |

|---|---|---|

| Concentration of Suppliers | Raises costs, disrupts supply | China/Australia ~60% of alumina production |

| Contractual Agreements | Provides stability, limits flexibility | 65% of raw materials under contract |

| Glencore's Influence | Supplier risk, potential disruptions | Glencore supplied ~80% of alumina |

Customers Bargaining Power

Concentrated Customer Base

Century Aluminum faces a concentrated customer base, primarily in automotive, packaging, and construction. These sectors account for a large portion of revenue, providing significant bargaining power to customers. In 2024, the automotive industry's aluminum demand saw fluctuations impacting pricing. This customer concentration increases vulnerability to industry-specific downturns, as seen in construction's recent slowdown. Century's financials reflect these pressures; specifically, 2024's profit margins were influenced by customer negotiations and market dynamics.

Price Sensitivity

Aluminum product pricing is volatile, impacting customer price sensitivity. Century Aluminum's ability to raise prices is limited by market share risk. In 2024, aluminum prices fluctuated, with LME prices around $2,300-$2,500/metric ton. Century must balance profitability and customer retention.

Long-Term Supply Agreements

Century Aluminum's long-term supply deals, especially in automotive and packaging, shape customer bargaining power. These agreements offer demand and pricing stability. They also cap Century's ability to profit from quick market changes. Contract terms greatly affect Century's revenue; in 2024, such contracts influenced roughly 60% of sales.

Switching Costs Assessment

Switching costs for Century Aluminum's customers, such as those in the automotive or construction sectors, involve re-qualifying new aluminum suppliers, which can be time-consuming. Contractual penalties also influence switching decisions, but these are often manageable. However, customers may switch if they can secure better pricing or superior product quality. Century Aluminum's ability to retain customers depends on its ability to maintain a competitive advantage.

- Re-qualification can take several months, impacting timelines.

- Contractual penalties vary, but may not always deter a switch.

- Aluminum prices in 2024 averaged around $2,500 per metric ton.

- Customer switching is more likely if competitors offer lower prices or better products.

Product Standardization

The aluminum market's product standardization, particularly for basic ingots, elevates customer bargaining power. This lack of differentiation allows customers to easily compare prices and switch suppliers. Century Aluminum faces pressure to offer competitive pricing due to this. To mitigate this, they can focus on specialized products and services.

- Standard aluminum ingot prices in 2024 fluctuated, with premiums over the London Metal Exchange (LME) price being a key factor.

- Century Aluminum's financial reports for 2024 highlight the importance of product mix in profitability, indicating strategic shifts towards higher-value offerings.

- Market analysis in late 2024 showed increased demand for specific aluminum alloys, suggesting opportunities for differentiation.

Aluminum's Price Dance: Customer Power Plays

Century Aluminum's customer bargaining power is significant, particularly due to concentrated customer bases like automotive. Volatile aluminum prices, approximately $2,500/metric ton in 2024, increase price sensitivity. Long-term contracts and product standardization further empower customers.

| Factor | Impact | 2024 Data |

|---|---|---|

| Customer Concentration | High bargaining power | Automotive/Construction represent major revenue streams |

| Price Sensitivity | Influences negotiations | LME prices around $2,300-$2,500/metric ton |

| Contracts | Demand/pricing stability | ~60% sales via contracts |

Rivalry Among Competitors

Intense Competition

The global aluminum market is fiercely competitive. Century Aluminum competes with established firms and low-cost producers. This competition strains pricing and profit margins. In 2024, aluminum prices fluctuated due to supply chain issues and demand changes. Major players include Alcoa and Rusal, impacting Century's market position.

Large Manufacturers

Large manufacturers dominate the aluminum market, holding substantial global production capacity. Companies like Rio Tinto and Alcoa possess significant economies of scale and robust distribution networks. In 2024, Rio Tinto's aluminum production reached 3.2 million tonnes. Century Aluminum faces a challenge to differentiate itself to compete effectively against these giants.

Low-Cost Producers

Low-cost producers from China, India, and the Middle East significantly pressure Century Aluminum. These rivals have advantages in labor, energy, and regulations, enabling lower prices. In 2024, Chinese aluminum production reached approximately 43 million metric tons, impacting global prices. Century must prioritize efficiency to compete.

Technological Innovation

Technological innovation significantly shapes competition in aluminum, with Century Aluminum focusing on R&D for production and sustainability. This investment helps lower costs and boost quality, aligning with environmental standards. For example, in 2024, Century Aluminum allocated approximately $15 million towards R&D initiatives. These advancements are crucial for maintaining a competitive edge.

- R&D spending in 2024 reached approximately $15 million.

- Focus on sustainable aluminum production technologies.

- Innovations aim to reduce costs and improve product quality.

- Meeting evolving environmental standards is a key goal.

Market Share

Century Aluminum holds a relatively small market share compared to industry giants. This restricts its ability to dictate prices or secure advantageous deals. The company's position necessitates strategic growth plans to enhance its market presence and competitiveness. Century's 2024 revenue was approximately $2.3 billion, significantly less than larger rivals.

- Market share affects pricing power.

- Smaller share limits supplier negotiations.

- Strategic growth is essential.

- 2024 revenue: ~$2.3 billion.

Aluminum Market's Fierce Battle: Rivals & Price Wars

Century Aluminum faces intense rivalry in the aluminum market due to global competitors. Key rivals include Alcoa and Rio Tinto, whose 2024 revenues significantly exceed Century's $2.3B. Low-cost producers, particularly from China, also increase price pressure.

| Factor | Description | Impact |

|---|---|---|

| Major Competitors | Alcoa, Rio Tinto, Rusal | Pricing pressure, market share competition. |

| Low-Cost Producers | China, India, Middle East | Lower prices, margin reduction. |

| Market Share | Century's relatively small market share | Limits pricing power. |

SSubstitutes Threaten

Increasing Competition

Aluminum faces growing competition from substitutes like plastics and composites. These alternatives can replace aluminum in many applications, potentially lowering demand. For example, the global plastics market was valued at $620.6 billion in 2023. Century Aluminum must innovate and highlight aluminum's advantages. Continuous innovation is vital to defend its market position against these rivals.

Lightweight Materials

The rise of lightweight materials like composites and plastics poses a threat to aluminum, a key input for Century Aluminum. These materials are increasingly used in automotive and aerospace, challenging aluminum's market share. In 2024, the global lightweight materials market was valued at approximately $340 billion, growing steadily. Century Aluminum must emphasize aluminum's recyclability and strength to compete effectively.

Packaging Sector

In the packaging sector, Century Aluminum confronts substitutes like plastic and other materials. Plastic's lower cost and versatility create a significant challenge. For instance, plastic packaging accounted for over 40% of the global packaging market in 2024. To compete, Century Aluminum must highlight aluminum's recyclability and sustainability. The aluminum recycling rate is around 50% in the U.S. in 2024, a key advantage.

Automotive Sector

The automotive sector, a key aluminum consumer, faces threats from substitutes like high-strength steel and carbon fiber. These materials compete with aluminum based on performance and cost. Century Aluminum must collaborate with automakers to create aluminum-based solutions. In 2024, the global automotive aluminum market was valued at approximately $40 billion. The adoption of carbon fiber in high-end vehicles rose by 15% in 2024.

- High-strength steel offers cost advantages.

- Carbon fiber provides weight reduction benefits.

- Aluminum's recyclability supports sustainability.

- Collaboration is key for market share.

Substitution in Construction

In construction, Century Aluminum contends with substitutes like steel, wood, and concrete. These alternatives often boast lower costs and greater availability, impacting aluminum's market share. To counter this, Century Aluminum highlights aluminum's superior durability and corrosion resistance. This strategic positioning is crucial for maintaining its competitive edge.

- Steel prices saw fluctuations in 2024, impacting construction costs.

- Wood prices varied based on supply chain issues.

- Concrete remains a widely used, cost-effective option.

- Aluminum's premium pricing requires emphasizing its unique benefits.

Aluminum's Rivals: Plastics, Steel, and Composites

Century Aluminum faces substitute threats from plastics and composites across various sectors. Plastics, like those in packaging, are cost-effective alternatives to aluminum. The automotive sector also sees competition from high-strength steel and carbon fiber. Emphasizing aluminum's recyclability and collaboration is key.

| Sector | Substitute | 2024 Data |

|---|---|---|

| Packaging | Plastics | 40%+ of packaging market |

| Automotive | High-strength steel | Price fluctuations affected costs |

| Construction | Steel | Prices varied, impacting costs |

Entrants Threaten

High Capital Investment

The aluminum industry demands hefty upfront investments for plants and equipment. This financial hurdle, a barrier to entry, shields existing players like Century Aluminum. Building a new smelter can cost billions, as seen with Alcoa's upgrades. This limits the number of new firms, reducing competition. Century Aluminum benefits from this, facing fewer new rivals.

Economies of Scale

Established aluminum producers, like Century Aluminum, leverage economies of scale to cut production costs. New companies face difficulties in rapidly reaching similar cost efficiencies, creating a disadvantage. Century Aluminum's substantial operational scale acts as a barrier to entry. For instance, in 2024, Century Aluminum's revenue was approximately $2.5 billion, reflecting its established market presence and cost advantages.

Technological Expertise

Producing aluminum demands significant technological expertise. New entrants face substantial R&D investments, raising entry barriers. Century Aluminum's established technological capabilities offer a key advantage. This includes process optimization and proprietary technologies. In 2024, the industry saw $1.5 billion in R&D spending.

Access to Raw Materials

Securing access to raw materials, such as bauxite and alumina, poses a significant hurdle for new entrants in the aluminum industry. These critical resources are often controlled by a few key suppliers, creating a barrier to entry. New companies must forge relationships with these suppliers, a process that can be both difficult and time-intensive. Century Aluminum benefits from existing, established supply agreements, giving it a competitive edge.

- In 2024, global bauxite production was estimated at 410 million metric tons.

- Alumina prices fluctuated, with significant price swings in the first half of 2024.

- Century Aluminum has long-term supply contracts, mitigating short-term price volatility.

- New entrants face high capital costs and operational complexities.

Regulatory Hurdles

The aluminum industry faces stringent environmental regulations and requires extensive permitting processes. New companies must overcome these complex and expensive regulatory barriers to enter the market. Century Aluminum's established compliance history provides a competitive advantage, deterring potential entrants. This advantage is enhanced by the significant upfront costs associated with meeting environmental standards. In 2024, environmental compliance costs have risen by approximately 10-15% for similar heavy industries.

- Environmental regulations significantly increase the cost of entry.

- Century Aluminum's compliance history acts as a barrier.

- Upfront costs and permitting requirements are substantial.

- Compliance costs are rising, making entry more difficult.

Aluminum Industry: High Hurdles for Newcomers

New aluminum industry entrants face substantial barriers due to high capital requirements and operational complexities. Established firms like Century Aluminum benefit from these hurdles, which include huge upfront investment and achieving economies of scale. This limits the number of new competitors. In 2024, new smelter projects faced delays and cost overruns.

| Barrier | Impact | 2024 Data Point |

|---|---|---|

| High Capital Costs | Limits New Entrants | Smelter construction cost: $3-5 billion |

| Economies of Scale | Cost Advantage for Incumbents | Century Aluminum's revenue: ~$2.5 billion |

| Technological Expertise | Requires R&D Investment | Industry R&D spending: ~$1.5 billion |

Porter's Five Forces Analysis Data Sources

The analysis leverages financial reports, market analysis, industry publications, and regulatory filings. This provides essential insights to map the competitive forces.