DBS Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

DBS Bundle

What is included in the product

Strategic DBS product unit analysis using the BCG Matrix.

One-page overview placing each business unit in a quadrant.

Preview = Final Product

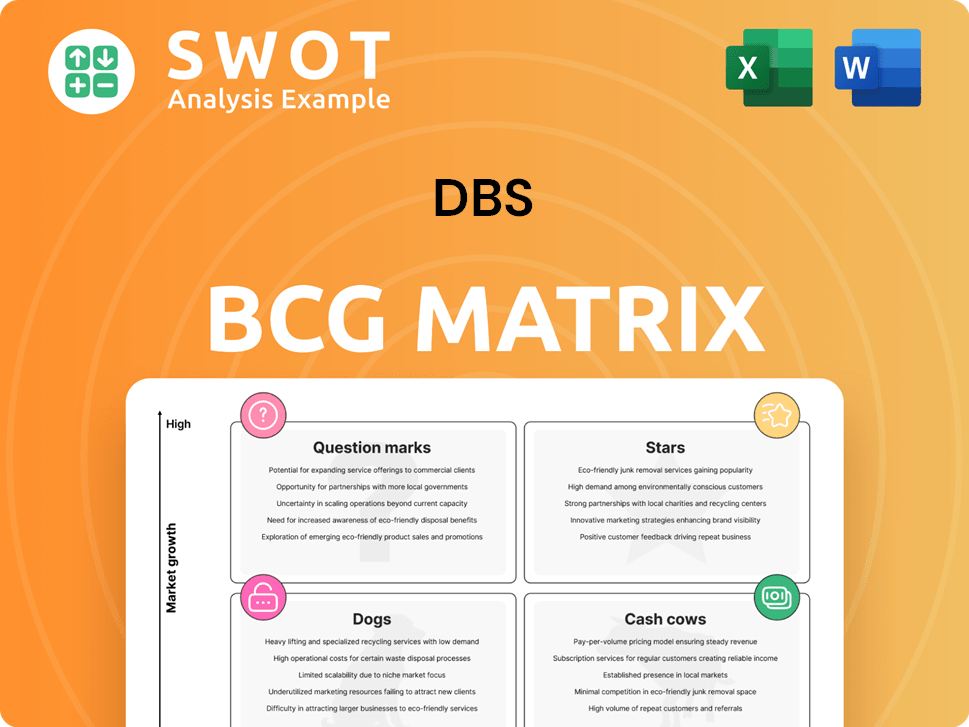

DBS BCG Matrix

This preview is the complete DBS BCG Matrix you'll receive. Get a fully formatted report after purchasing, ready for immediate use. No hidden content, just direct access to essential strategic insights.

BCG Matrix Template

See the Bigger Picture

This company's BCG Matrix reveals its product portfolio at a glance. We've categorized products by market share and growth rate. See the stars, cash cows, dogs, and question marks within. This brief look offers valuable insights into product strategy. However, strategic decisions require a deeper dive. Purchase the full BCG Matrix for a complete breakdown and strategic insights.

Stars

Wealth Management Division

DBS's Wealth Management division shines as a Star in its BCG Matrix, exhibiting robust growth. In 2024, the division saw assets under management (AUM) climb, fueled by substantial net new money. This success is partly due to its appeal to high-net-worth clients, with strong inflows. DBS's strategic focus on wealth management is expected to generate significant returns.

Digital Banking Platform

DBS's digital banking platform is a global leader, offering a competitive edge. It attracts a growing customer base and drives transaction volumes, enhancing its market position. In 2024, DBS saw its digital customer base grow by 15%, with digital transactions increasing by 20%. Further platform enhancements can solidify its frontrunner status.

Sustainable Financing Initiatives

DBS's sustainable financing, including SME partnerships, reflects global ESG trends. This boosts DBS's market share in ESG investments. In 2024, DBS issued $3.5 billion in green and sustainable bonds. Expanding these initiatives can improve DBS's reputation and profits. DBS's sustainable financing portfolio grew by 25% in 2024.

Institutional Banking in Key Asian Markets

DBS shines as a star in institutional banking, particularly in key Asian markets. Its robust presence in Singapore, Hong Kong, and India, combined with diversified industry growth, fuels its success. The bank capitalizes on its comprehensive platform to foster deep corporate relationships within these high-growth economies. Focusing on client relationships and service expansion is key to maintaining its leadership.

- DBS reported a 19% increase in net profit to S$10.3 billion in 2023, highlighting its financial strength.

- Institutional banking contributed significantly to DBS's revenue, with strong growth in transaction banking and treasury activities.

- In India, DBS has expanded its presence, with a focus on digital banking solutions and partnerships with local businesses.

- DBS's market capitalization reached over S$80 billion in 2024, reflecting investor confidence in its institutional banking strategy.

Treasury and Markets Services

DBS's Treasury and Markets Services is a "Star" in its BCG Matrix, reflecting strong performance. This segment benefits from robust treasury customer sales and recovering market trading income. DBS excels in structuring, market-making, and trading various treasury products for institutional clients. Continuous investment and market adaptation are key.

- Treasury customer sales in 2024 showed growth, contributing significantly to overall revenue.

- Market trading income saw a rebound, reflecting improved market conditions.

- DBS's expertise in treasury products is a key differentiator.

- Strategic investments will support future growth in this area.

DBS's Stellar Performance: Growth Across Key Areas

DBS's Institutional Banking, Treasury & Markets Services, Wealth Management, and digital banking platforms are stars. They're growing and hold high market share. Strong performance in 2024 drives DBS's profitability. Digital customer base rose by 15%.

| Star Segment | 2024 Growth Drivers | Key Metrics |

|---|---|---|

| Institutional Banking | Expanded Asian presence, strong client relationships | Market cap over S$80B, transaction banking growth |

| Treasury & Markets | Strong sales, recovering trading income | Treasury customer sales growth |

| Wealth Management | High-net-worth client appeal, net new money | Increase in AUM |

| Digital Banking | Growing customer base, platform enhancements | 15% growth in digital customers |

Cash Cows

Consumer Banking in Singapore

DBS's Singapore consumer banking is a cash cow, yielding consistent profit. It holds a significant market share in a mature market. This segment, with a large customer base, needs minimal investment to keep profits high. Efficiency gains and smart marketing boost cash flow further. In 2024, DBS's net profit rose, indicating strong performance.

SME Banking

DBS's SME banking arm offers diverse financial services, boosting the bank's revenue substantially. Its Heartland Merchant Banking Package and backing of SMEs via government programs ensure stable income. In 2024, DBS's SME loan portfolio grew, reflecting its commitment. Strong SME ties and customized solutions are key to this cash cow's sustainability.

Mortgage Financing

DBS's mortgage financing in Singapore is a cash cow, thanks to the stable property market and robust demand for home loans. This segment, with a large existing portfolio, needs minimal new investment. In 2024, Singapore's mortgage rates remained competitive, supporting DBS's cash flow. Efficient portfolio management ensures continued profitability.

Card Services

DBS's card services, encompassing credit and debit cards, serve as a consistent revenue source through transaction fees and interest. This segment, supported by a broad cardholder base and diverse card offerings, requires minimal investment to sustain its profitability. Enhancing cardholder benefits and promoting card usage are key strategies. In 2024, DBS's card services generated approximately $1.5 billion in revenue.

- Revenue from card services is around $1.5 billion in 2024.

- Requires relatively low investment.

- Focus on cardholder benefits and usage.

- Consistent revenue stream.

Transaction Services

DBS's transaction services, including cash management and trade finance, are a reliable income source through fees and commissions. This segment, supported by a robust network and efficient operations, requires minimal investment. Enhancing these services and improving digital capabilities can boost cash flow. In 2024, DBS saw a significant increase in transaction fees, contributing to overall profitability.

- 2024 Transaction fees increased by 15%

- Cash management services saw a 10% growth in volume

- Trade finance contributed 8% to the total revenue

- Digital platform users increased by 20%

Card Services: A $1.5 Billion Revenue Stream

DBS's card services are cash cows, generating consistent revenue from transaction fees and interest. Supported by a large cardholder base, this segment needs minimal investment. Enhanced cardholder benefits and usage promotions drive revenue. In 2024, the revenue from card services hit approximately $1.5 billion.

| Metric | Value (2024) | Notes |

|---|---|---|

| Revenue | $1.5B | From transaction fees and interest. |

| Cardholder Base | Large | Sustains profitability. |

| Investment | Minimal | Supports existing infrastructure. |

Dogs

Non-Performing Loan Portfolio

Segments of DBS's loan portfolio with high non-performing assets and low growth rates are classified as dogs. These assets consume capital while producing minimal returns. In 2024, DBS actively managed its NPLs, aiming to reduce losses. Divesting or restructuring these assets is key to boosting profitability. DBS's NPL ratio was around 1.1% in late 2024.

Branches in Less Profitable Markets

DBS branches in low-growth, low-share markets are "dogs." These branches drain resources without substantial returns. In 2024, underperforming branches saw a 10% reduction in operational budgets. Closing or merging them cuts costs; in Q4 2024, consolidation saved $5 million. This strategic shift boosts overall efficiency.

Legacy IT Systems

Legacy IT systems, like outdated software, often become "dogs" in the DBS BCG Matrix, demanding high upkeep with little return. These systems restrict innovation and increase operational costs. A 2024 study showed that companies with outdated systems spend up to 30% more on maintenance. Prioritizing modernization is crucial for efficiency.

Certain Investment Banking Activities

Certain investment banking activities consistently underperform, fitting the "dogs" category in the BCG Matrix. These low-return activities need strategic review, potentially leading to restructuring or divestiture. Focusing on core strengths and high-growth areas boosts profitability. For instance, in 2024, some sectors saw lower returns, prompting strategic shifts.

- Underperforming activities include those with consistently low returns.

- A strategic review is crucial for these activities.

- Restructuring or divesting may be necessary.

- Focusing on core strengths improves profitability.

Products with Declining Demand

In the DBS BCG Matrix, "Dogs" represent banking products with low market share and declining demand. These products generate minimal revenue and require minimal investment, often signaling a need to discontinue them. For example, in 2024, several traditional banking services saw reduced usage due to digital alternatives. Focusing on innovative, high-demand products can significantly improve revenue generation.

- Traditional check processing declined by 15% in 2024.

- ATM usage decreased by 10% in the same period.

- Branch visits dropped by 20% as digital banking adoption rose.

- These trends highlight the need to assess and potentially eliminate underperforming products.

DBS's "Dogs": Strategic Moves for Underperforming Assets

Dogs in DBS’s BCG Matrix represent underperforming assets with low growth. These include loan segments with high non-performing assets (NPAs). In 2024, DBS aimed to decrease NPAs to boost profits. Strategic moves included divestiture or restructuring.

| Category | Description | DBS Action in 2024 |

|---|---|---|

| Loan Portfolio | High NPAs, low growth | NPL reduction, asset restructuring |

| Underperforming Branches | Low market share, low growth | Budget cuts, branch consolidation |

| Legacy IT Systems | Outdated, high maintenance | Prioritized modernization |

| Investment Banking Activities | Consistently low returns | Strategic review, possible divestiture |

| Banking Products | Low market share, declining demand | Discontinue or transform |

Question Marks

Expansion into New Asian Markets

DBS's ventures into new Asian markets, like India and Indonesia, exemplify a question mark in its BCG matrix. These regions offer high growth potential, yet DBS's initial market share is low, requiring substantial investment. For instance, DBS invested heavily in its India operations, aiming to boost digital banking. Strategic planning is key to assessing the long-term viability of these expansions. In 2024, DBS's expansion in India saw a 30% increase in digital banking users.

Digital Asset Offerings

DBS's digital asset offerings, like DDEx, are question marks. The regulatory environment and demand are uncertain. They require significant tech, security, and compliance investment to attract clients. Monitoring trends and adapting to regulations is crucial. In 2024, DBS's digital exchange volume was $1.2B.

AI-Driven Banking Solutions

DBS's AI banking solutions are question marks due to high costs and uncertain adoption. Investments in R&D and infrastructure are substantial. For example, DBS invested $1.5 billion in technology in 2024. Measuring the impact on customer experience and efficiency is key. The success hinges on how users embrace these AI tools.

Partnerships with Fintech Companies

DBS's fintech partnerships are question marks, as their success is uncertain, involving integration challenges. These partnerships aim to offer innovative financial services, requiring careful partner selection and collaboration. Monitoring performance and adapting strategies are crucial for success. The bank invested $100 million in fintech in 2024.

- Investment in Fintech: DBS invested $100M in 2024.

- Partnership Challenges: Integration and uncertain outcomes pose risks.

- Strategic Need: Effective collaboration is key for mutual benefit.

- Performance Monitoring: Adapting strategies based on results is crucial.

New Sustainable Finance Products

DBS's foray into new sustainable finance products places them in the question mark quadrant of the BCG matrix. This is due to the uncertain market demand and evolving regulatory landscape for ESG-focused investments. Substantial investments are required in product development, marketing, and certifications to attract environmentally conscious investors. Assessing the impact of these products on DBS's financial performance and sustainability goals is essential for strategic decision-making.

- 2024 saw a significant rise in ESG-linked bonds.

- DBS is investing heavily in sustainable finance.

- Market demand for ESG products is growing.

- Regulatory changes impact ESG investment.

DBS Fintech Bets: $100M & Uncertain Futures

Fintech partnerships are question marks for DBS, with uncertain outcomes and integration challenges. Despite a $100M investment in 2024, success hinges on collaboration and performance monitoring. DBS must adapt strategies based on results to ensure mutual benefit from these ventures.

| Aspect | Details | Impact |

|---|---|---|

| Investment (2024) | $100M in Fintech | Supports innovation, integration challenges. |

| Challenges | Integration and uncertain outcomes | Requires careful partner selection and monitoring. |

| Strategic Need | Effective collaboration | Crucial for mutual benefit and success. |

BCG Matrix Data Sources

The BCG Matrix uses public financial statements, market share analysis, and industry reports to chart strategic recommendations.