Diamondback Energy Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Diamondback Energy Bundle

What is included in the product

Tailored analysis for Diamondback's portfolio, highlighting investment, hold, or divest strategies.

Printable summary optimized for A4 and mobile PDFs allows for easy sharing.

Delivered as Shown

Diamondback Energy BCG Matrix

The Diamondback Energy BCG Matrix preview mirrors the final document you'll receive. Purchase grants immediate access to a ready-to-use report for strategic insights. It's designed for clarity, offering actionable analysis for your needs. You'll get the complete, downloadable, professionally formatted matrix. This ensures consistent quality from preview to use.

BCG Matrix Template

Unlock Strategic Clarity

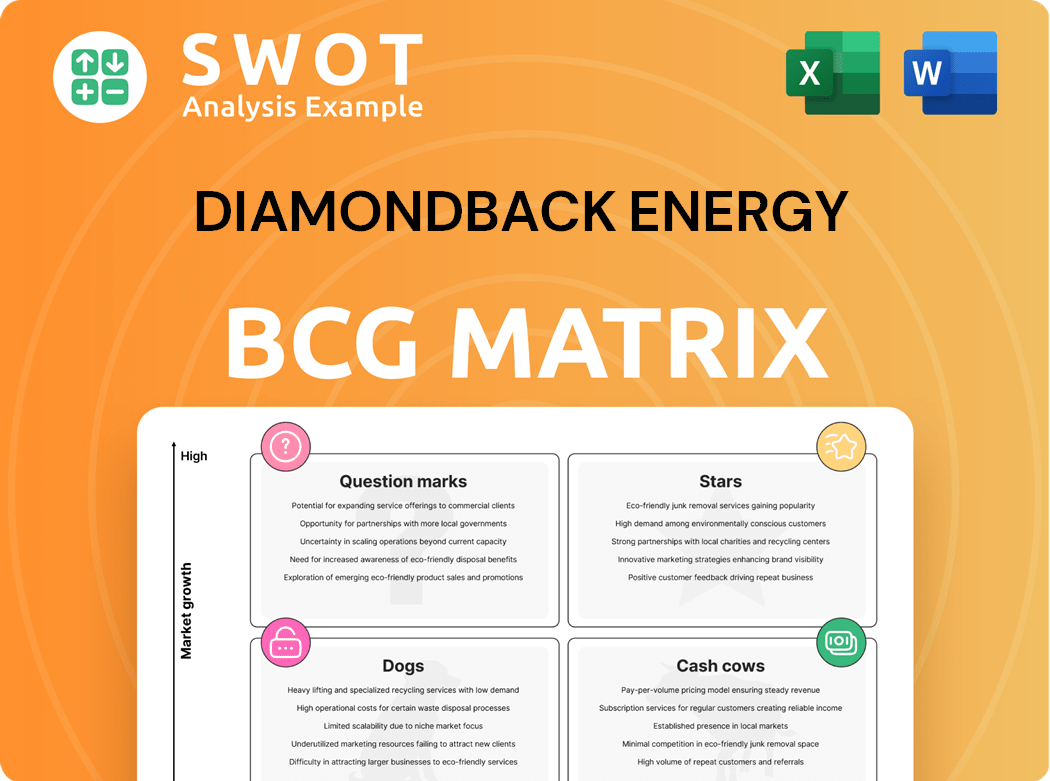

Diamondback Energy's BCG Matrix offers a glimpse into its diverse portfolio. Identifying "Stars" and "Cash Cows" is key for growth. This strategic tool helps understand resource allocation. See how each product fits into the market dynamics. This preview provides only the basic insights.

Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Permian Basin Dominance

Diamondback Energy shines in the Permian Basin, especially in the Midland Basin, as a top onshore oil and gas producer. They hold vast acreage, focusing on formations like Spraberry and Wolfcamp. This gives them access to the basin's rich resources and good financial returns. In 2024, Diamondback's production reached approximately 270,000 barrels of oil equivalent per day, solidifying its Permian dominance.

Strategic Acquisitions

Diamondback Energy strategically boosts growth via acquisitions. The Endeavor merger and Double Eagle IV Midco LLC deal expanded assets. This increased drilling locations and operational scale. The Endeavor acquisition created a leading Permian position of about 722,000 net acres. In 2024, Diamondback's market cap reached $38 billion.

Operational Efficiency

Diamondback Energy excels in operational efficiency, cutting costs and boosting output. They've lowered well costs in the Midland Basin to $555-$605 per lateral foot, a 7% year-over-year decrease. These improvements enhance capital efficiency and boost production. Faster drilling times and standardized designs further reduce costs.

Strong Financial Performance

Diamondback Energy shines as a "Star" in the BCG matrix, thanks to its impressive financial performance in 2024. They've generated record cash flow and boosted net income, which is great news for investors. The company's low breakeven costs and shareholder return program further solidify its strong position in the market.

- 2024 Net Cash from Operations: $6.4 billion

- 2024 Adjusted Free Cash Flow: $4.0 billion

- Attractive Free Cash Flow Yield

Commitment to Shareholder Returns

Diamondback Energy prioritizes shareholder returns, a key aspect of its strategy. The company has consistently boosted its base dividend, showcasing financial health and investor commitment. This approach includes significant share repurchases, signaling confidence in future performance. In 2024, Diamondback increased its base dividend by 11%, to $1.00 per share quarterly.

- Increased Dividend: 11% increase in base dividend in 2024.

- Share Repurchases: Significant number of shares repurchased.

- Dividend: $1.00 per share quarterly.

Diamondback's 2024: Cash, Dividends, and Dominance!

Diamondback Energy's "Star" status in 2024 is fueled by its financial prowess and high market share within the Permian Basin. The company's high growth and financial returns are sustained by impressive cash flow. This strength is evident through a growing dividend and shareholder-focused actions.

| Metric | Value (2024) | Details |

|---|---|---|

| Net Cash from Operations | $6.4 billion | Demonstrates strong operational efficiency |

| Adjusted Free Cash Flow | $4.0 billion | Supports shareholder returns and reinvestment |

| Dividend Increase | 11% | Reflects financial health and commitment |

Cash Cows

Established Production Base

Diamondback Energy's established Permian Basin production is a solid cash flow source. These fields require less capital to maintain, fitting the cash cow profile. The Permian Basin is crucial, with the EIA predicting approximately 105 Bcf/d in 2025. In 2024, Permian production averaged about 90 Bcf/d, highlighting its importance.

Midland Basin Assets

Diamondback Energy's Midland Basin assets are prime cash cows, thanks to lower costs and known geology. Their experience here leads to efficient production and consistent cash flows. In Q3 2023, Diamondback's production in the Midland Basin was 260.5 Mboe/d. They have 1,310 horizontal locations there.

Infrastructure and Midstream Assets

Diamondback Energy's infrastructure and midstream assets are a stable cash source. These include gathering systems and processing facilities. They support production and generate revenue. The company spent $14 million on midstream in 2024. This investment ensures consistent cash flow.

Long-Life Reserves

Reserves with long production lives and low decline rates are considered cash cows. These assets produce steady cash flow with minimal additional investment. Diamondback Energy's long inventory life supports this classification. In 2024, Diamondback reported robust financial results.

- Diamondback's inventory life is around 18 years at $50/bbl oil price.

- This long life indicates stable, predictable cash flow.

- Minimal investment is needed to maintain production.

- The assets are a source of consistent revenue.

Royalty Interests

Diamondback Energy's royalty interests, primarily through its stake in Viper Energy (VNOM), represent a cash cow in its BCG matrix. This segment provides a stable income stream due to its diverse Permian Basin assets. In 2024, Viper Energy reported strong financial results. It generated significant free cash flow, supporting consistent shareholder returns.

- Viper Energy's Q1 2024 production averaged 31.5 thousand barrels of oil equivalent per day.

- Royalty interests require minimal capital, enhancing profitability.

- These assets deliver consistent cash flow.

- Diamondback benefits from this low-cost, high-margin business.

Stable Cash Flow: Permian Assets Powering Performance

Diamondback Energy's cash cows provide stable cash flow, especially from Permian assets. These assets need minimal extra capital, like its Midland Basin operations producing 260.5 Mboe/d in Q3 2023. Royalty interests, via Viper Energy, offer further consistent income; Q1 2024 production was 31.5 Mboe/d.

| Asset Type | Key Feature | 2024 Data |

|---|---|---|

| Permian Production | Established, low capital | 90 Bcf/d average |

| Midland Basin | Efficient, known geology | 260.5 Mboe/d (Q3 2023) |

| Royalty Interests (Viper) | Low cost, high margin | 31.5 Mboe/d (Q1 2024) |

Dogs

Delaware Basin Assets (Select)

Diamondback Energy's Delaware Basin assets are crucial, yet not all perform equally. Some Delaware Basin assets might be considered "dogs" due to lower production or higher costs. Certain assets produce around 9,000 barrels per day. This is in contrast to the higher-performing Midland Basin assets.

Older, Less Efficient Wells

Older wells at Diamondback Energy, categorized as "Dogs," show declining production and rising expenses. Workovers or enhanced methods may be needed to sustain profitability. Midland Basin well costs dropped to $555-$605 per lateral foot, a 7% decrease year-over-year. These wells face challenges despite cost reductions.

Non-Core Acreage

Non-core acreage, like Diamondback's Delaware Basin assets, often falls into the "Dog" category within the BCG Matrix. These areas may have limited drilling prospects. Diamondback's 2024 deal with TRP Energy, exchanging 33,000 acres and $238 million for Midland Basin land, exemplifies this strategy. This move reallocates resources to higher-potential areas.

Assets with High Environmental Liabilities

Assets with high environmental liabilities are considered Dogs in Diamondback Energy's BCG matrix. These properties often face remediation costs or regulatory issues that diminish their value. For the full year ended 2024, Diamondback allocated $221 million for infrastructure and environmental spending. The financial burden can exceed revenue potential, making them less attractive.

- High remediation costs.

- Regulatory compliance issues.

- Diminished asset value.

- Potential for negative returns.

Marginal Gas Production

In Diamondback Energy's BCG matrix, marginal gas production assets fall into the "Dogs" category, especially if natural gas prices stay low. These assets, heavily reliant on natural gas, might not generate enough revenue to cover operational expenses and investments. The fourth quarter of 2024 saw natural gas prices at a mere $0.48 per Mcf, which indicates the challenges these assets face. This makes them less attractive compared to other, more profitable ventures within the company.

- Low Natural Gas Prices: A key factor impacting profitability.

- Revenue Challenges: Difficulty covering operating costs and capital expenditures.

- Q4 2024 Data: Average unhedged realized prices: $0.48 per Mcf of natural gas.

Diamondback's Assets: Low Output, High Costs

Dogs in Diamondback's portfolio include assets with low output, high expenses, and high environmental liabilities. Older wells show declining production, with remediation costs adding to financial burdens. Marginal gas production assets, like those seeing Q4 2024 prices of $0.48/Mcf, also fall into this category.

| Category | Characteristics | Financial Impact |

|---|---|---|

| Asset Type | Delaware Basin, Older Wells, Gas Assets | Low Production, High Costs, Environmental Liabilities |

| Performance | Declining Production | Reduced Revenue |

| 2024 Data Points | Q4 2024 Gas Price: $0.48/Mcf, Environmental Spending: $221M | Lower profitability |

Question Marks

Emerging Technologies (Carbon Capture)

Diamondback's CCS investments are a question mark in its BCG matrix. Success hinges on tech, regulation, and demand. In 2024, CCS projects faced high costs and policy uncertainty. Diamondback's gas power and land management focus may lower costs. CCS market was valued at $3.6 billion in 2023.

Alternative Energy Ventures

Diamondback Energy's forays into alternative energy, like solar or wind, are positioned as question marks in its BCG matrix. These ventures could diversify revenue and lower its carbon footprint. However, they face considerable risks and uncertainties. Diamondback is also exploring gas power generation and land management, targeting cost reductions. In 2024, Diamondback's total revenue was $8.2 billion.

New Formation Exploration

New formation exploration means Diamondback Energy looks for oil and gas in new areas. This involves high risk but could lead to major new reserves. In 2024, Diamondback plans testing in Wolfcamp D and Upper Spraberry. These tests help assess potential production and profitability. Diamondback spent $2.4 billion on exploration and development in 2023.

Direct Lithium Extraction

Direct Lithium Extraction (DLE) is considered a "Question Mark" for Diamondback Energy in a BCG matrix. TerraLithium, an Oxy subsidiary, partnered with BHE Renewables in June 2024. This joint venture aims to commercialize DLE, extracting high-purity lithium from geothermal brine. DLE could be a high-growth, low-share venture, requiring significant investment with uncertain returns.

- Joint venture formed in June 2024.

- Focus on extracting lithium from geothermal brine.

- DLE technologies are patented.

- Significant investment and uncertain returns.

Overseas Expansion

In Diamondback Energy's BCG matrix, overseas expansion is classified as a Question Mark. This is because, while the company's primary focus is the Permian Basin, venturing into international markets introduces uncertainty. Such expansion could unlock access to new reserves and growth prospects, potentially increasing the company's value. However, international ventures also bring substantial risks.

These risks include political instability, economic fluctuations, and operational challenges. The success of these ventures is not guaranteed, and significant investment is needed. Diamondback's strategic decision to expand internationally would need careful evaluation.

As of late 2024, Diamondback's financial reports show a strong performance in the Permian Basin. Any international move would be a high-stakes bet. The company's current market capitalization reflects its Permian-focused success.

The decision to expand internationally hinges on Diamondback's risk appetite and strategic vision. The potential rewards must be weighed against the inherent uncertainties of global operations. The company's board of directors will play a vital role in this decision-making process.

- Risk: Political and economic instability in new markets.

- Opportunity: Access to untapped oil and gas reserves.

- Financial Consideration: High capital investment required.

- Strategic Challenge: Balancing growth with risk management.

Overseas Expansion: A Risky Gamble?

Diamondback Energy's overseas expansion is a "Question Mark" in its BCG matrix. International ventures present both opportunities and considerable risks, like instability and economic shifts. In 2024, the company is evaluating international expansion opportunities. The decision balances growth prospects with risk management.

| Aspect | Details | 2024 Data |

|---|---|---|

| Risk | Political/economic instability | Increased volatility |

| Opportunity | Access to new reserves | Strategic growth |

| Investment | Capital Needs | High |

BCG Matrix Data Sources

This Diamondback Energy BCG Matrix is based on company financials, industry research, and market analysis for precise strategic assessments.