DPR Construction Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

DPR Construction Bundle

What is included in the product

Tailored exclusively for DPR Construction, analyzing its position within its competitive landscape.

Swap in DPR's data for a clear view of competitive forces and easily visualize market pressures.

Preview the Actual Deliverable

DPR Construction Porter's Five Forces Analysis

This preview offers the full DPR Construction Porter's Five Forces analysis you'll receive. The document presented here is identical to the one you'll download instantly post-purchase. It's a comprehensive, ready-to-use resource detailing the competitive landscape. You'll get the fully formatted analysis without any changes. No extra steps, just immediate access.

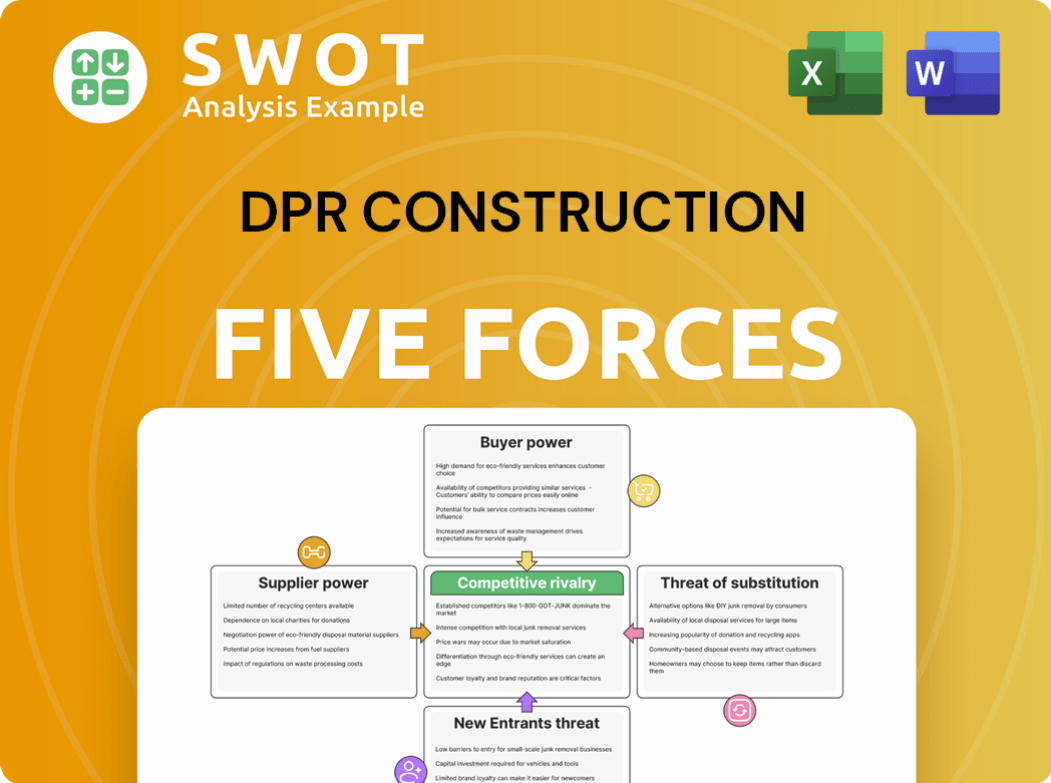

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

DPR Construction faces complex industry dynamics. Buyer power, influenced by project size & client negotiating strength, impacts profitability. Supplier bargaining power, especially for materials & skilled labor, also plays a significant role. The threat of new entrants, while moderated by high barriers, remains a factor. Substitute threats, though limited, exist in alternative construction methods. Competitive rivalry within the construction sector is notably intense.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore DPR Construction’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Expertise

Suppliers with specialized expertise, offering unique components or services, hold significant power. DPR Construction relies on specialized materials and expertise for projects in advanced technology and life sciences. Limited supplier options for these items diminish DPR's leverage. For instance, in 2024, the cost of specialized construction materials increased by approximately 7%. This impacts project costs.

Supplier Consolidation

Supplier consolidation significantly boosts their bargaining power. When a few major entities control essential construction materials, such as steel or concrete, they gain leverage to set prices and conditions. This can directly affect DPR's project expenses, especially in a market where material costs are volatile. In 2024, steel prices fluctuated, impacting construction budgets. Monitoring these costs is vital.

Impact of Tariffs

Tariffs on imported materials significantly affect supplier power. For instance, steel tariffs can boost costs, reducing DPR's bargaining power. In 2024, the US imposed tariffs on various goods, including those from Canada and China. This can lead to higher prices and less flexibility. Reciprocal tariffs further complicate negotiations, potentially increasing project expenses.

Labor Availability

DPR Construction's bargaining power with suppliers is significantly influenced by labor availability. Suppliers offering skilled labor gain leverage in a market facing shortages. The construction sector struggles with a talent gap, and suppliers bundling materials with installation services have increased bargaining power. This dynamic is reflected in project costs, with skilled labor's premium impacting overall expenses. Labor costs in construction rose by 6.4% in 2024, reflecting this trend.

- Labor shortages drive up project costs.

- Suppliers with skilled labor services are in demand.

- Bundled services increase supplier bargaining power.

- Construction labor costs rose by 6.4% in 2024.

Supply Chain Resilience

Suppliers with resilient supply chains have significant bargaining power. Ongoing global conflicts and extreme weather events continue to disrupt supply chains. Suppliers who can guarantee timely delivery are in a stronger position. For example, in 2024, the construction industry faced significant material price fluctuations due to geopolitical instability and climate change impacts. This increased supplier influence.

- Geopolitical tensions, especially with China, Russia, and Iran, caused supply chain disruptions.

- Extreme weather events, such as droughts, further strained supply chains.

- Suppliers with diversified sourcing were better positioned.

Supplier Dynamics: Impact on Construction Costs

Suppliers with unique expertise, materials, and services exert considerable influence over DPR Construction. Consolidation among suppliers, especially of essential materials, boosts their leverage to dictate prices and terms, directly impacting project costs. The construction sector's labor shortages and resilient supply chains amplify supplier power, as demonstrated by rising labor costs.

| Factor | Impact on DPR | 2024 Data |

|---|---|---|

| Specialized Materials | Reduced leverage, higher costs | Specialized material costs rose ~7%. |

| Supplier Consolidation | Increased project expenses | Steel prices fluctuated significantly. |

| Labor Availability | Higher labor costs | Construction labor costs +6.4%. |

Customers Bargaining Power

Project Scale

DPR Construction's large projects, like those in healthcare and tech, elevate customer power. Clients, investing substantial capital, gain significant negotiation leverage. For instance, a 2024 report indicated that large construction projects saw an average cost overrun of 10-15%, giving clients a strong bargaining position. This is because they can push for better terms and pricing.

Switching Costs

Low switching costs amplify customer power. Customers easily move to alternatives, boosting their leverage. In 2024, the construction industry saw a 10% rise in project cancellations, showing heightened customer mobility. Specialized services and solid relationships can counter this trend.

Market Concentration

DPR Construction's customer bargaining power is influenced by market concentration. A concentrated customer base, where a few clients account for a large portion of revenue, enhances customer leverage. In 2024, if a few major clients represented a significant percentage of DPR's projects, their ability to negotiate prices would increase. Diversifying the client base mitigates this risk; for example, expanding into new geographic markets or sectors can reduce dependency on a few key customers. The goal is to maintain a balanced portfolio to limit any single customer's influence.

Economic Conditions

Economic conditions significantly influence customer power, particularly during downturns. Customers gain leverage in uncertain economies, delaying or reducing projects, and thus demanding better prices. Post-election economic shifts impact project financing, with uncertainty causing project delays and potentially reducing overall construction spending. The construction industry saw a 4.4% decrease in spending in December 2023, reflecting economic pressures. This trend suggests customers held more power.

- Economic downturns amplify customer bargaining power.

- Post-election, financing uncertainties can stall projects.

- Construction spending decreased by 4.4% in December 2023.

- Customers may seek lower prices or terms due to economic uncertainty.

Demand for Specific Expertise

Customers demanding niche construction expertise wield less influence. DPR Construction's specialization in intricate projects, particularly for tech and life sciences, offers some protection. This is because fewer firms have the required skills. For instance, the construction market was valued at $1.5 trillion in 2024.

- Specialized skills reduce customer power.

- DPR's niche focus offers insulation.

- Fewer contractors possess necessary expertise.

- The construction market was at $1.5T in 2024.

Client Leverage: Shaping Construction Outcomes

Customer bargaining power significantly affects DPR Construction, particularly in large projects. Clients often have considerable leverage due to high capital investments and the availability of alternative contractors. Economic conditions amplify this power, with downturns and financing uncertainties giving customers more negotiating strength. In 2024, the construction industry faced a landscape where clients could readily seek better terms or even delay projects.

| Factor | Impact on Customer Power | 2024 Data |

|---|---|---|

| Project Size | High investment, more leverage | Large projects cost overrun: 10-15% |

| Switching Costs | Low costs increase power | 10% rise in cancellations |

| Economic Conditions | Downturns increase power | 4.4% spending decrease in December 2023 |

Rivalry Among Competitors

Market Share

DPR Construction competes fiercely for market share with giants like Jacobs Engineering and Aecom. These firms, along with Barton Malow, create a competitive landscape. In 2024, DPR's market share is approximately 10.5% of total industry revenue. DPR is recognized as a Rising Star in the construction sector.

Industry Growth Rate

Slower industry growth intensifies competition among construction firms. Construction spending for nonresidential buildings is expected to slow in 2025 and 2026. With less overall market expansion, DPR Construction and its competitors must fight harder for each project. According to the Dodge Construction Network, nonresidential building starts are forecast to decline by 3% in 2024.

Differentiation

Differentiation strategies can lessen competitive rivalry. DPR Construction distinguishes itself through technically complex and sustainable projects. This focus helps them stand out in the market. However, the construction industry is becoming more competitive. The adoption of new technologies is crucial, with the global construction market valued at $15.2 trillion in 2024.

Technological Adoption

Technological adoption intensifies rivalry among construction firms. The industry is rapidly integrating technologies like BIM and robotics. Strategic tech investment is becoming a key differentiator. DPR Construction, like its competitors, must invest to stay competitive. The global construction robotics market is projected to reach $2.8 billion by 2024.

- BIM adoption rates are increasing, with over 70% of large firms using it.

- Robotics in construction is growing at a CAGR of 10% annually.

- Digital twins are being adopted by 35% of construction companies.

- Automation is expected to reduce labor costs by 15% in the next 5 years.

Backlog and Project Pipeline

Healthy backlogs can reduce competitive rivalry. Construction firms benefit from solid backlogs, with 8-9 months of secured work in the EU and the US. The DMI's lag suggests a strong project pipeline for 2025 and 2026, assuming economic stability. This pipeline eases immediate competition by providing a buffer of secured projects.

- Construction backlogs in the EU and US provide a buffer against immediate competitive pressures.

- The Design-Manufacturing Index (DMI) indicates a robust pipeline for future projects.

- A strong project pipeline may alleviate some short-term rivalry.

Construction Market Dynamics: DPR's Competitive Landscape

Competitive rivalry for DPR Construction is high, with key players like Jacobs Engineering and Aecom vying for market share. Slowing industry growth and technological advancements amplify this competition. DPR's focus on complex projects and tech adoption, while the global construction market reached $15.2T in 2024, attempts to differentiate itself.

| Metric | Data |

|---|---|

| DPR Market Share (2024) | 10.5% |

| Nonresidential Building Start Decline (2024 Forecast) | 3% |

| Global Construction Market Value (2024) | $15.2T |

SSubstitutes Threaten

Design-Build Alternatives

Design-build methods offer an alternative to traditional project delivery, acting as a substitute. This approach is vital for creating adaptable environments. In 2024, design-build projects accounted for over 40% of non-residential construction. These projects address seismic events, extreme weather, and evolving patient needs. This method is increasingly popular due to its efficiency and adaptability.

Modular Construction

Modular and prefabricated construction presents a viable substitute to traditional construction methods. This approach, where building components are assembled off-site, offers standardized production. This can lead to quicker project timelines and reduced expenses. In 2024, the modular construction market was valued at approximately $157 billion globally, showcasing its growing importance.

Renovation vs. New Construction

Renovating existing structures presents a viable alternative to new construction. Due to rising interest rates and economic uncertainty, developers and buyers are increasingly prioritizing renovations and retrofits. In 2024, the renovation market is estimated at $450 billion, showing its significant impact. The construction market encompasses various projects, from new builds to renovations.

In-House Construction

Some clients might opt for in-house construction, a potential threat to DPR Construction. Large tech companies, like Apple or Google, often have internal teams, reducing their reliance on external contractors. This shift can diminish DPR's market share, especially in the tech sector, where these clients are prevalent. The in-house approach allows for greater control and potentially lower costs, if managed effectively.

- In 2024, the global construction market was valued at approximately $15 trillion.

- Companies like Apple have dedicated real estate and construction divisions.

- In-house construction teams can reduce project costs by 5-10%.

- The trend of in-house construction is more common in developed countries.

Material Substitutes

Material substitutes present a notable threat to DPR Construction. Alternative building materials, such as recycled concrete, steel, and wood, can reduce the reliance on virgin materials. These alternatives also help lower carbon emissions, aligning with sustainability goals. The use of renewable resources like bamboo and hemp provides even more sustainable options.

- The global green building materials market was valued at $364.8 billion in 2024.

- Recycled concrete can reduce material costs by 10-20% compared to virgin concrete.

- The use of timber in construction is projected to increase by 40% by 2028.

DPR Construction: Facing the Substitute Threat

The threat of substitutes for DPR Construction is significant due to various factors. Design-build methods, modular construction, and renovations offer alternatives. Clients' in-house construction teams pose another risk, especially in sectors like tech.

Alternative materials also threaten DPR's market position. For example, the global green building materials market was valued at $364.8 billion in 2024. The trend of using in-house teams is more common in developed countries, impacting demand for external contractors.

| Substitute Type | Description | Market Impact (2024) |

|---|---|---|

| Design-Build | Alternative project delivery method | Over 40% of non-residential projects |

| Modular Construction | Off-site component assembly | $157 billion global market |

| Renovations | Upgrading existing structures | $450 billion market |

Entrants Threaten

High Capital Requirements

High capital requirements pose a significant threat. The construction sector demands considerable upfront investment in machinery and tech. For example, in 2024, the average cost for heavy equipment like excavators was around $250,000-$750,000 each. This deters new entrants. Additionally, skilled labor costs and project financing further increase the barrier.

Established Relationships

Established relationships pose a significant threat to new entrants. DPR Construction benefits from strong client bonds, making it challenging for newcomers to compete. The construction industry's reliance on trust favors incumbents. New firms face hurdles in securing projects from clients loyal to DPR, as seen in 2024, where repeat business accounted for 65% of revenue.

Skilled Labor Shortages

New construction companies find it tough to enter the market due to a shortage of skilled workers. The industry struggles with an aging workforce and not enough young people joining. This labor gap makes it difficult for new businesses to grow quickly. In 2024, the construction sector faced a 4.4% unemployment rate, highlighting the ongoing challenge. Competition for skilled labor drives up costs, hindering new firms.

Regulatory Hurdles

The construction industry faces significant barriers due to a complex regulatory landscape. Regulatory hurdles, including local, state, and federal requirements, increase compliance costs and operational complexities for new entrants. This environment can deter new companies from entering the market. To mitigate these challenges, new firms must adapt by improving workforce training and diversifying supplier networks.

- In 2024, construction firms spent an average of 5-7% of project costs on regulatory compliance.

- Companies with robust training programs saw a 10-15% increase in project efficiency.

- Diversifying supplier networks reduced project delays by approximately 20%.

- Early procurement strategies helped new companies save up to 8% on material costs.

Technological Expertise

Technological expertise poses a significant barrier to entry for new construction firms. The adoption of advanced technologies like Building Information Modeling (BIM), artificial intelligence (AI), and digital twins is rapidly increasing within the construction industry, as of 2024. These technologies require substantial upfront investment in software, hardware, and skilled personnel. New entrants often lack the financial resources and established expertise to compete effectively in this technology-driven environment, hindering their ability to gain market share.

- BIM adoption rates have increased by 20% in the last five years.

- AI in construction is projected to reach a market size of $4.5 billion by 2028.

- Digital twins are used by 30% of construction companies, as of 2023.

- Average cost for implementing BIM software can range from $10,000 to $100,000.

DPR Construction: New Entrant Threat Analysis

The threat of new entrants to DPR Construction is moderate. High capital needs and tech adoption are barriers. However, the labor shortage and regulatory hurdles also limit new firms.

| Barrier | Impact | Data (2024) |

|---|---|---|

| Capital Costs | High | Equipment: $250K-$750K/unit |

| Tech Adoption | Moderate | BIM adoption: +20% in 5 yrs |

| Labor Shortage | Moderate | Unemployment: 4.4% |

Porter's Five Forces Analysis Data Sources

DPR's analysis uses financial reports, construction industry publications, and economic databases to assess competitive pressures.