ENN Natural Gas(ENN NG ) Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

ENN Natural Gas(ENN NG ) Bundle

What is included in the product

Analyzes ENN NG's competitive position, including threats from rivals, suppliers, and buyers.

Instantly pinpoint vulnerabilities in ENN NG's competitive landscape with color-coded risk levels.

Preview Before You Purchase

ENN Natural Gas(ENN NG ) Porter's Five Forces Analysis

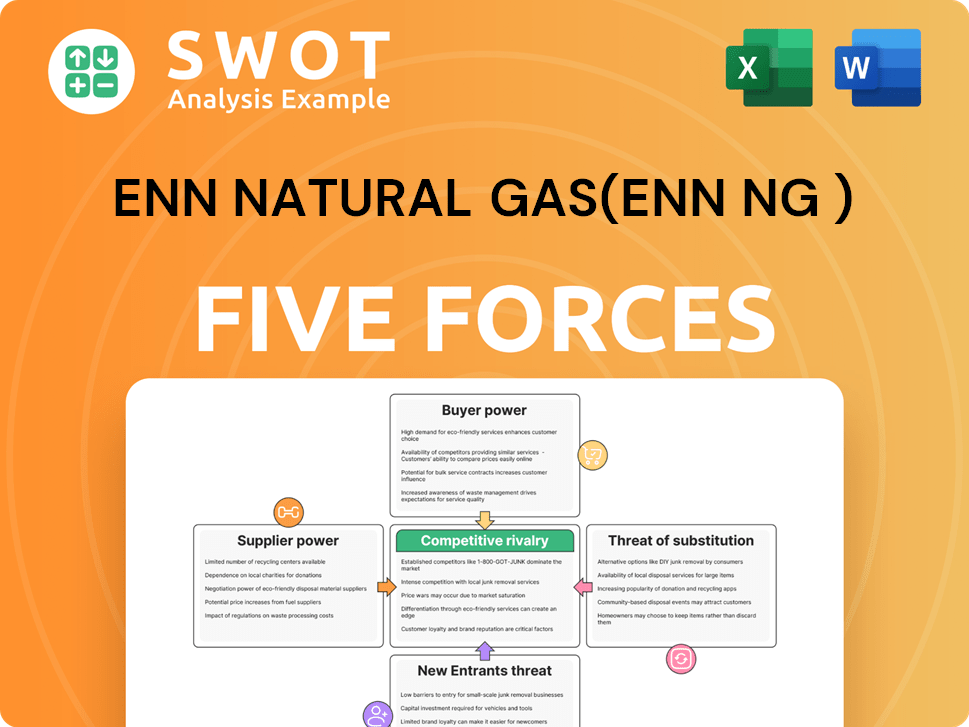

This preview reveals the complete ENN Natural Gas Porter's Five Forces analysis. The document comprehensively assesses industry rivalry, supplier power, buyer power, threat of substitutes, and threat of new entrants. This strategic analysis, fully formatted, provides actionable insights. You're viewing the exact file you will instantly download after purchase. No hidden information, just comprehensive analysis.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

ENN Natural Gas (ENN NG) faces moderate threat from substitutes due to alternative energy sources, especially renewables. Buyer power is concentrated among industrial clients, potentially squeezing margins. Supplier power is relatively low, given the diverse gas supply options available. The threat of new entrants is moderate, considering the capital-intensive nature of the industry. Competitive rivalry is intense, marked by several players.

Our full Porter's Five Forces report goes deeper—offering a data-driven framework to understand ENN Natural Gas(ENN NG )'s real business risks and market opportunities.

Suppliers Bargaining Power

Limited Number of Large Suppliers

ENN NG relies on a concentrated group of suppliers like CNPC and Sinopec. This dependence gives suppliers more leverage in pricing and contract terms. In 2024, natural gas prices fluctuated, impacting ENN NG's costs. Strategic partnerships help, but supplier power remains a factor. ENN NG's ability to negotiate favorably affects profitability.

Government Influence on Supply

The Chinese government significantly influences the natural gas market, affecting ENN NG's supplier bargaining power. In 2024, China's focus on expanding gas infrastructure, with investments expected to rise, impacts supplier negotiation abilities. This oversight, while potentially limiting supplier independence, also ensures a more stable supply. China's natural gas consumption in 2024 was about 400 billion cubic meters.

Long-Term Contracts

ENN NG's long-term contracts, like the 15-year LNG deal with ADNOC for 1 mtpa, aim to stabilize supply. These agreements, such as the one signed in 2024, help manage supplier power by locking in prices and volumes. However, they also create dependencies, potentially reducing ENN NG's ability to quickly adapt to market changes.

Access to LNG Terminals

ENN Natural Gas (ENN NG) gains some bargaining power over suppliers through its access to LNG receiving terminals. This access enables ENN to diversify its gas sources, potentially securing more favorable pricing. The Zhoushan terminal, for example, enhances ENN's ability to import gas, reducing reliance on domestic suppliers. Long-term supply deals, facilitated by terminal access, further strengthen ENN's position. However, terminal capacity and efficiency are key factors.

- ENN's Zhoushan LNG terminal has a throughput capacity of 3 million tons per year.

- In 2024, ENN signed a deal to import LNG from Qatar for 15 years.

- China's LNG imports in 2024 are projected to be around 70 million tons.

Geopolitical Factors

Geopolitical factors greatly influence ENN Natural Gas's suppliers. China's significant reliance on foreign gas, reaching 40.9% in 2024, elevates supplier power. Trade tensions and global instability can disrupt gas supplies, impacting ENN NG. This can also lead to price fluctuations and supply chain challenges.

- China's dependency on foreign gas was 40.9% in 2024.

- Geopolitical events can disrupt supply chains.

ENN NG's Supplier Dynamics: Power & Pricing

ENN NG faces supplier power from entities like CNPC and Sinopec, impacting pricing. China's market influence and infrastructure investments affect negotiation dynamics. Long-term contracts and LNG terminals provide some leverage.

| Factor | Impact | Data (2024) |

|---|---|---|

| Supplier Concentration | Higher supplier power | CNPC, Sinopec dominate. |

| Govt. Influence | Stable supply, limited supplier indep. | China gas consumption ~400 BCM. |

| Long-Term Contracts | Price/volume certainty | 15-yr LNG deal with ADNOC. |

| Terminal Access | Diversification, better pricing | Zhoushan terminal capacity 3 mtpa. |

Customers Bargaining Power

Diverse Customer Base

ENN NG's diverse customer base, which includes residential, commercial, and industrial users, impacts its bargaining power. ENN Natural Gas Co., Ltd. (stock code: 600803.SH) operates 260 gas projects across 21 provinces in China. The company serves over 30 million households and more than 250,000 commercial clients. This widespread distribution limits any single customer's influence, supporting a stronger market position.

Switching Costs for Residential Customers

Residential customers of ENN NG encounter notable switching costs due to the established natural gas infrastructure. Replacing gas pipelines is inconvenient, and alternatives like LPG must be significantly cheaper to justify a switch. This inertia grants ENN NG some bargaining power, allowing it to maintain customer loyalty. The average residential natural gas price in China was approximately $12.5 per million BTU in 2024.

Price Sensitivity of Industrial Customers

Industrial customers, especially those in energy-intensive sectors, are very price-sensitive regarding natural gas. In 2024, with corporate profits under pressure, cost control became crucial, dampening the demand for additional gas. Downstream gas consumption’s weak enthusiasm and limited market demand for incremental gas enhance customer bargaining power. This enables them to negotiate prices or explore alternatives, thus increasing their leverage.

Government Regulation of Tariffs

Government regulations on natural gas tariffs significantly influence ENN NG's pricing flexibility, directly affecting customer bargaining power. City gas operators, including ENN NG, face public and regulatory pressure to maintain reasonable prices. Transparency in tariff setting, with disclosed gas procurement costs, further shapes this dynamic. In 2024, China's natural gas consumption reached approximately 390 billion cubic meters.

- Regulatory Impact: Government oversight limits pricing freedom.

- Public Scrutiny: High tariffs invite stricter regulations.

- Transparency: Cost disclosures influence pricing.

- Market Context: China's 2024 gas consumption data.

Demand Growth in China

The surge in natural gas demand within China, fueled by stringent environmental regulations and robust economic expansion, is diminishing the bargaining power of ENN NG's customers. China's natural gas consumption is projected to rise by 6.5% this year, reaching approximately 456 billion cubic meters (bcm). This upward trend is supported by strategic import initiatives, ensuring a steady customer base for ENN NG. Natural gas is poised to become a more integral part of China's evolving energy landscape.

- Demand Increase: China's natural gas consumption expected to grow by 6.5% in 2024.

- Consumption Volume: Anticipated to reach around 456 bcm this year.

- Strategic Imports: Efforts to secure supply through imports.

- Role in Energy: Natural gas is set to play a larger role.

Customer Power Dynamics in the Natural Gas Market

ENN NG's bargaining power is influenced by customer diversity and switching costs, with residential customers facing higher barriers. Industrial customers, focused on cost control, have more leverage, especially as demand and market conditions fluctuate. Government regulations and transparency in pricing also affect customer bargaining power, which is counterbalanced by rising natural gas demand in China, projected to increase consumption by 6.5% in 2024.

| Factor | Impact | Data (2024) |

|---|---|---|

| Customer Base | Diverse, limiting individual power | 30M+ households, 250K+ commercial clients |

| Switching Costs | High for residential; low for industry | Avg. residential price: ~$12.5/mmBTU |

| Regulation | Limits pricing flexibility | China's natural gas consumption: ~390 bcm |

| Demand | Rising, reducing customer power | Projected growth: 6.5% to ~456 bcm |

Rivalry Among Competitors

Fragmented Market

The natural gas market in China shows fragmentation, with many players, including ENN Energy's rivals. ENN's competitors are Datang, Shenergy, China Gezhouba, and Zhejiang Zheneng. This leads to heightened competition. In 2024, ENN Energy's revenue was about 110 billion yuan, reflecting the competitive landscape.

State-Owned Enterprises (SOEs)

Competition from state-owned enterprises (SOEs) significantly impacts ENN NG. SOEs in China's gas market, like PetroChina, benefit from resources and government backing. These advantages give them a competitive edge over private firms. For example, in 2024, PetroChina's revenue was CNY 3.4 trillion, showcasing its market influence.

Geographic Competition

Competition for ENN Natural Gas is fierce in specific areas. ENN NG operates 260 projects across 21 Chinese provinces. The company serves over 30 million homes and 250,000+ businesses. Competition's intensity depends on regional economies and regulations.

Integrated Energy Solutions

ENN Natural Gas's (ENN NG) push into integrated energy solutions significantly alters competitive dynamics. The company is actively involved in integrated energy, using low-carbon sources like solar and biomass. This move places ENN NG in direct competition with firms offering similar integrated services, increasing rivalry. To stay ahead, ENN NG must differentiate itself and offer competitive pricing.

- 2024 saw a 15% rise in integrated energy solutions market.

- Companies offering similar services include China General Nuclear Power Group (CGN) and China Resources Power.

- Competitive pricing is crucial, with average solar energy costs dropping 10% in 2024.

- Differentiation might include focusing on specific low-carbon sources or geographic markets.

Privatization and Integration

The privatization of ENN Energy and its integration with ENN NG are poised to significantly alter the competitive dynamics. This strategic move aims to fortify ENN NG's market position amid evolving conditions, fostering efficient resource allocation. Enhanced integration should allow for seamless business operations, potentially increasing market share. However, this could also introduce market uncertainties, impacting existing competitors.

- ENN Energy's revenue in 2024: Approximately $25 billion.

- ENN NG's market capitalization in 2024: Around $10 billion.

- Expected synergy benefits from integration: Estimated at 10% cost reduction.

- Major competitors in the natural gas distribution market: China Resources Gas, China Gas.

ENN NG Faces Intense Market Competition

Competitive rivalry in ENN Natural Gas's market is high due to numerous players and market dynamics. ENN faces competition from SOEs like PetroChina, which had a 2024 revenue of CNY 3.4 trillion. ENN NG's expansion into integrated energy solutions intensifies competition, especially against companies like CGN.

| Aspect | Details | 2024 Data |

|---|---|---|

| ENN NG Revenue | Approximate Revenue | 110 billion yuan |

| Integrated Energy Market | Growth Rate | 15% increase |

| Solar Energy Cost | Average price reduction | 10% decrease |

SSubstitutes Threaten

Coal

Coal presents a notable substitute for natural gas, especially in power generation and industrial applications. Switching to natural gas offers a quick way to reduce emissions from coal by 50%. However, the lower costs and availability of coal in certain areas can hinder ENN NG's market growth. In 2024, coal consumption in China, a key market, reached about 4.6 billion metric tons, impacting natural gas demand.

Electricity

Electricity poses a significant threat to ENN NG, particularly in heating and cooling. Solar and other renewable energy sources are increasingly used to generate electricity, providing alternatives to natural gas. The adoption of electric systems reduces natural gas reliance; for example, the U.S. residential sector's natural gas consumption decreased by 5.5% in 2024 due to electrification trends.

Renewable Energy Sources

Renewable energy sources, like solar and wind, are becoming attractive alternatives to natural gas. Biogas, a quickly producible alternative, is gaining traction for individual and community use. Government support accelerates this shift, increasing the threat. In 2024, renewable energy's share of global electricity generation rose, pressuring natural gas demand.

Liquefied Petroleum Gas (LPG)

Liquefied Petroleum Gas (LPG) poses a significant threat to ENN Natural Gas (ENN NG) as a substitute. LPG, particularly propane, is easily accessible and used where natural gas pipelines are absent. It is derived from natural gas processing and crude oil refining. LPG's portability and ease of use make it a strong competitor.

- In 2024, global LPG consumption was approximately 300 million metric tons.

- Propane's price volatility can impact its competitiveness against natural gas.

- LPG is used in residential, commercial, and industrial sectors, creating direct competition.

- The ease of switching between LPG and natural gas increases the threat.

Substitute Natural Gas (SNG)

Substitute Natural Gas (SNG) poses a moderate threat to ENN Natural Gas. SNG, derived from sources like coal and biofuels, can replace natural gas in existing infrastructure. The viability of SNG as LNG or CNG in transport is growing, potentially reducing demand for traditional fuels. However, SNG's market share is still small, with natural gas dominating the energy sector.

- China's SNG production capacity reached approximately 15 billion cubic meters in 2024.

- The global SNG market is projected to grow at a CAGR of around 6% from 2024 to 2030.

- The cost of SNG production is higher than natural gas, but is decreasing.

- SNG's adoption is driven by environmental regulations and energy security concerns.

Substitutes Squeeze Natural Gas Demand

Multiple substitutes challenge ENN NG's market position. Coal, a direct competitor, impacts natural gas demand, especially in key markets like China, where coal consumption hit 4.6 billion metric tons in 2024. Renewable energy sources, such as solar and wind, are increasing their market share. Moreover, LPG competes directly, with 2024's global consumption reaching approximately 300 million metric tons.

| Substitute | Impact on ENN NG | 2024 Data/Fact |

|---|---|---|

| Coal | High | China's coal consumption: ~4.6B metric tons |

| Renewables | Moderate | Rising share in global electricity generation |

| LPG | Moderate | Global LPG consumption: ~300M metric tons |

Entrants Threaten

High Capital Requirements

The natural gas distribution sector requires substantial upfront investments in infrastructure, including pipelines, storage, and terminals. Building such extensive networks demands considerable capital, acting as a major hurdle for newcomers. For example, in 2024, pipeline projects often cost billions, with the Mountain Valley Pipeline estimated at over $7.2 billion. Without guaranteed returns, new entrants face high financial risks.

Regulatory Hurdles

The natural gas industry faces significant regulatory hurdles, making it tough for new players to enter. Complex licensing and permitting processes are common, increasing the time and money needed to get started. Government control over natural gas prices can limit ENN NG's ability to set their own prices, affecting customer bargaining power. These regulations act as barriers, reducing the attractiveness of entering the market.

Established Infrastructure

ENN Natural Gas (ENN NG) faces threats from new entrants, but its established infrastructure poses a significant barrier. Existing players like ENN NG, with its 81,604 kilometers of pipeline network in China as of 2023, have strong customer relationships. The cost and time required to build a competing pipeline network are substantial. This makes it difficult for new competitors to gain market share.

Access to Supply

For new entrants, securing a reliable natural gas supply is a major hurdle. This is because established firms like ENN Natural Gas (ENN NG) often have long-term contracts and strong supplier relationships. ENN has strategically secured its supply through deals. These include agreements with major players like Chevron, Total, and Origin. These agreements allow ENN to purchase 1.44 million tons of LNG annually.

- Long-term contracts give ENN NG a competitive edge in securing gas supply.

- New entrants struggle to compete with the established supply chains.

- Without guaranteed supply, new entrants are at a disadvantage.

- ENN's supply deals with Chevron, Total, and Origin secure LNG.

Economies of Scale

Existing companies in the natural gas sector, like ENN, often benefit from economies of scale. This advantage stems from their ability to procure, distribute, and operate at lower costs due to their size. ENN, for example, was among the initial privately owned gas distributors in China, giving it a head start. This established scale provides a significant cost advantage, making it challenging for new entrants to compete effectively.

- Procurement: Larger companies can negotiate better prices for natural gas.

- Distribution: Established infrastructure reduces per-unit distribution costs.

- Operations: Efficient operations lead to lower overhead expenses.

- ENN's Early Entry: ENN's early entry into the market gave it a competitive edge.

ENN NG: Entry Barriers & Competitive Edge

Threats from new entrants to ENN Natural Gas (ENN NG) are moderate. High infrastructure costs, with pipeline projects costing billions, limit entry. Regulatory hurdles and securing a reliable gas supply further restrict new competitors. ENN NG's established pipelines and contracts provide strong defenses.

| Barrier | Impact on New Entrants | ENN NG Advantage |

|---|---|---|

| High Capital Costs | Significant investment needed. | Established infrastructure. |

| Regulatory Hurdles | Complex and time-consuming. | Existing licenses and permits. |

| Supply Chain | Difficult to secure supply. | Long-term supply contracts. |

Porter's Five Forces Analysis Data Sources

Our ENN NG Porter's Five Forces analysis utilizes annual reports, industry research, and market analysis reports. We incorporate financial data, regulatory filings, and competitor analysis to gain insights.