Equity Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Equity Bank Bundle

What is included in the product

Analyzes Equity Bank's competitive forces, market dynamics, and position within its landscape.

Swap in Equity Bank-specific data for tailored strategic insights.

Preview the Actual Deliverable

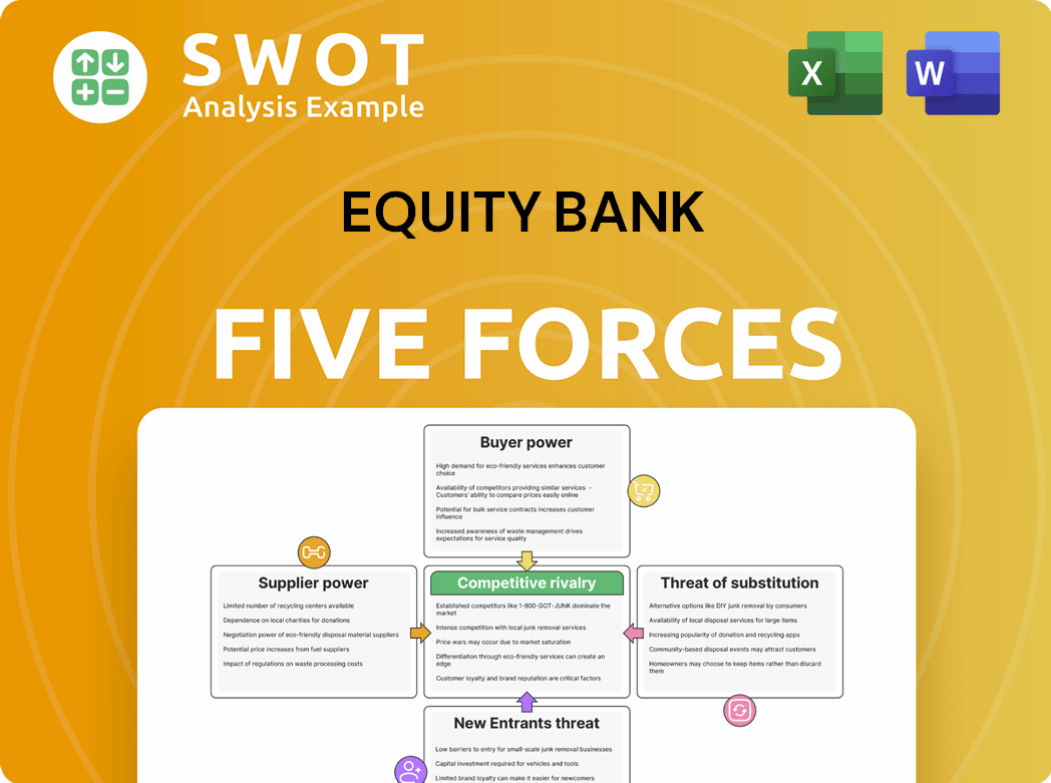

Equity Bank Porter's Five Forces Analysis

This preview provides a full Equity Bank Porter's Five Forces analysis. The document outlines competitive rivalry, bargaining power of suppliers/buyers, threats of new entrants/substitutes.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Equity Bank faces diverse competitive pressures. Buyer power, stemming from customer choice, influences its profitability. The threat of new entrants and substitutes adds to market complexity. Competition among existing players is fierce, shaped by diverse financial offerings. Understanding these forces is critical for strategic positioning and investment.

The complete report reveals the real forces shaping Equity Bank’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Switching Costs

Equity Bancshares generally faces low supplier bargaining power, particularly for generic goods, due to its ability to switch providers. However, specialized services, such as core banking software, could give suppliers more leverage, increasing potential switching costs. Equity Group's diverse procurement, highlighted by their online pre-qualification, suggests a broad supplier base. In 2024, Equity Group's total assets were over $10 billion, indicating substantial purchasing power that further reduces supplier influence.

Number of Suppliers

Equity Bancshares' bargaining power with suppliers is generally strong due to a diverse supplier base. The bank's ability to negotiate is enhanced by having multiple options for goods and services. Equity's 2024 10-K showed employee growth, yet this doesn't imply supplier concentration. A wide range of suppliers keeps costs competitive.

Supplier Concentration

Supplier concentration affects Equity Bancshares' bargaining power. If few suppliers control essential services, their leverage increases. For example, core banking systems have limited providers. Equity's SEC 10-K doesn't specify supplier concentration. However, the banking sector's reliance on key tech vendors is a concern. In 2024, vendor costs could significantly impact profitability.

Impact of Supplier Inputs on Equity's Services

The bargaining power of suppliers significantly impacts Equity Bancshares. Suppliers, like those providing ICT equipment, exert more influence when their services are critical for Equity's operations. Equity's reliance on these suppliers, especially for essential services like online banking applications, increases their leverage. This affects costs and service delivery. For instance, the online pre-qualification application emphasizes the need for reliable ICT equipment.

- ICT equipment like desktops, laptops, and printers are crucial.

- Essential services like online banking applications increase suppliers' leverage.

- The bargaining power of suppliers significantly impacts Equity Bancshares.

- This affects costs and service delivery.

Availability of Substitute Inputs

Equity Bancshares' bargaining power with suppliers is weakened if there are readily available substitute inputs. If alternatives exist, like various cloud storage providers, Equity can switch without major problems. But, if inputs are specialized or patented, substitution becomes tough, potentially increasing supplier power. The financial sector's move toward AI means AI service providers might gain leverage if substitutes are scarce.

- In 2024, the cloud computing market is valued at over $600 billion globally, indicating many providers.

- Patented technologies can limit substitution options, increasing supplier power.

- The AI market in banking is projected to reach $3.4 billion by 2025, highlighting potential supplier influence.

- Equity Bancshares' ability to diversify its tech suppliers will be crucial.

Supplier Power Dynamics: A Look at the Numbers

Equity Bancshares generally holds strong supplier bargaining power due to a diversified supplier base and substantial purchasing power. This allows for competitive pricing and reduced supplier influence, particularly for generic goods. Specialized services and concentrated markets, such as core banking software, can increase supplier leverage, potentially impacting costs.

| Factor | Impact | 2024 Data |

|---|---|---|

| Supplier Diversity | Lowers Bargaining Power | Cloud computing market over $600B |

| Specialized Services | Raises Bargaining Power | AI in banking to reach $3.4B by 2025 |

| Procurement | Influences Costs | Equity Group's $10B+ in assets |

Customers Bargaining Power

Customer Switching Costs

High switching costs reduce customer power, benefiting Equity Bancshares. Superior service and loyalty programs can create "sticky" relationships. However, digital banking reduces these costs. In 2024, digital banking adoption rose, with 60% of US adults using mobile banking weekly. Smooth digital experiences are crucial for retention.

Number of Customers

A broad customer base dilutes individual influence. Equity Bancshares caters to diverse clients, including businesses and individuals. This fragmentation limits any single customer's ability to affect pricing or terms. Equity Bank's community focus creates loyalty, but also price sensitivity. In 2024, Equity Bancshares reported serving over 600,000 customers.

Customer Price Sensitivity

Customer price sensitivity significantly influences Equity Bank's profitability. Customers' willingness to switch banks for lower fees, especially for basic services, heightens price pressure. However, for complex services, price sensitivity decreases. Deloitte's 2024 outlook suggests banks must rethink noninterest income due to price sensitivity. In 2023, average checking account fees were $15.14 monthly.

Availability of Information

Customers' bargaining power increases with information access, especially regarding banking services and pricing. Online comparison tools and financial literacy initiatives enable informed decisions, pushing for better value. Digital banking, including AI assistants, enhances money management and awareness. This shift is evident in 2024, with 70% of consumers using online banking platforms.

- 70% of consumers use online banking platforms in 2024, increasing their access to information.

- Financial literacy initiatives have grown by 15% in the past year, empowering customers.

- AI banking assistants adoption has grown by 20% in 2024, enhancing customer awareness.

Customer Volume

Large customers, particularly businesses with substantial deposit accounts or borrowing needs, wield considerable bargaining power. Equity Bancshares may need to offer preferential rates or customized services to attract and retain these high-value clients. The SEC 10-K report highlights a focus on commercial banking, indicating commercial loans are a significant portfolio portion. This implies large commercial clients likely have greater power.

- Commercial loans comprised 66% of Equity Bancshares' total loan portfolio in 2024.

- The bank's net interest margin in 2024 was 3.55%, potentially influenced by rates offered to large clients.

- Deposits from commercial clients often exceed those from retail, increasing their influence.

Customer Power Shifts Bank's Profitability

Customers' bargaining power impacts Equity Bank's profitability. The rise of online banking and financial literacy, with 70% of consumers using online platforms in 2024, enhances customer awareness. Commercial clients, contributing 66% of the loan portfolio in 2024, have significant influence. Banks must adapt to customer price sensitivity.

| Factor | Impact | Data (2024) |

|---|---|---|

| Online Banking Adoption | Increased customer knowledge | 70% of consumers |

| Commercial Loans | Client bargaining power | 66% of loan portfolio |

| Financial Literacy Growth | Empowered customers | 15% increase |

Rivalry Among Competitors

Number of Competitors

The Kenyan banking sector is fiercely competitive, featuring many institutions. This environment demands that Equity Bank distinguishes itself through competitive offerings. Strategies include diversifying products and expanding regionally to gain market share. In 2024, the banking sector saw increased competition with many new entrants.

Industry Growth Rate

Slower industry growth often leads to fiercer competition among banks like Equity Bank. Economic downturns or regulatory shifts can significantly affect the banking industry's expansion rate. The Deloitte 2024 banking outlook highlights a tough macroeconomic environment anticipated for 2025. This suggests banks will likely face heightened rivalry. In 2024, the banking sector saw fluctuating growth, with some regions experiencing slower expansion, intensifying competition.

Product Differentiation

If banking services are seen as the same, competition focuses on price, potentially hurting profits. Equity Bancshares must set itself apart through innovation, service, or special skills. Equity Bank's review shows competitive rates and flexible loans as strengths. They also emphasize personalized service and understanding the local economy. In 2024, Equity Bancshares reported a net interest income of $644.4 million.

Switching Costs

Low switching costs intensify competitive rivalry in banking. Because customers can easily move, Equity Bancshares faces pressure to retain them. The rise of digital banking has made it easier for customers to switch. Fintechs and neobanks are upping the ante. Equity Bancshares must enhance its digital offerings to stay competitive.

- Average bank customer churn rate is around 10-15% annually.

- Digital banking adoption increased by 20% during 2024.

- Fintechs have captured 5-10% of the banking market in 2024.

- Banks are investing heavily, with 2024 digital transformation budgets increasing by 15%.

Strategic Stakes

Equity Bank faces high strategic stakes in a competitive landscape. Aggressive moves are driven by the need to gain market share and expand. Equity Bancshares' plans, including mergers like the NBC Corp deal in Oklahoma, highlight this. The bank's strategic focus is evident in its financial performance and growth initiatives.

- Market share growth is a key strategic objective for Equity Bank.

- Expansion into new regions drives competitive behavior.

- Mergers and acquisitions are part of Equity Bank's strategy.

- Financial performance supports strategic growth initiatives.

Kenyan Banking Sector: Navigating the Competition

Equity Bank operates within a highly competitive Kenyan banking sector, marked by numerous institutions vying for market share. Intense competition necessitates product diversification and regional expansion strategies. In 2024, the industry saw fluctuating growth rates and an influx of new entrants, intensifying rivalry.

Price-based competition and low switching costs, exacerbated by digital banking advancements, pose significant challenges. To counter, Equity Bancshares must prioritize innovation, personalized service, and enhanced digital offerings. The average customer churn rate hovers around 10-15% annually, underlining the need for customer retention efforts.

Strategic stakes are high, driving aggressive moves such as mergers and acquisitions aimed at market share growth. Digital transformation budgets increased by 15% in 2024 as banks invested in technology. Equity Bank's actions are driven by strategic financial performance and expansion.

| Metric | 2023 Data | 2024 Data (Projected) |

|---|---|---|

| Banking Sector Growth | 5% | 4% (Slower) |

| Digital Banking Adoption | +15% | +20% |

| Fintech Market Share | 4% | 5-10% |

SSubstitutes Threaten

Availability of Substitutes

The threat of substitutes is significant for Equity Bank. Options like credit unions and fintech companies offer similar services. These alternatives can impact Equity Bancshares' market share. Digital banking competition, with fintechs, forces innovation. In 2024, fintech funding reached $51 billion globally.

Switching Costs

Low switching costs intensify the threat of substitutes for Equity Bank. Customers can readily move their funds to alternative providers, so Equity Bancshares must focus on customer retention. Digital payment platforms and online lenders have simplified the process, reducing switching costs significantly. In 2024, digital banking adoption rose by 15% globally. AI-driven personalization in finance could boost loyalty but also expose better alternatives.

Relative Price Performance

If substitutes offer better value, customers might switch. Equity Bancshares must keep its pricing and services competitive. The Equity Bank Review highlights competitive interest rates, but fees and convenience are also vital. In 2024, the average bank fee was $10.85, and Equity Bank must strive to be below that.

Customer Propensity to Substitute

Customer propensity to substitute varies. Younger, tech-savvy clients might embrace fintech, contrasting with older customers who favor traditional banking. Equity Bancshares must understand its customer segments, adapting its services. Digital banking shows mobile apps are vital, signaling a rise in digital substitutes. In 2024, mobile banking users surged, reflecting this shift.

- Fintech adoption rates are increasing, with 65% of adults using digital banking in 2024.

- Traditional banks face competition from neobanks, which have grown their customer base by 20% in the last year.

- Equity Bancshares needs to invest in user-friendly digital platforms to retain customers.

- The average customer now interacts with their bank via mobile apps 3-4 times a week.

Perceived Level of Product Differentiation

The threat of substitutes for Equity Bank hinges on how customers view its services. If banking feels uniform, customers might readily switch to cheaper or more convenient alternatives. Equity Bancshares must differentiate itself to combat this. Equity Group's strong brand, ranking as the 2nd strongest globally in 2024, is key.

- Customer Perception: If services seem identical, switching is easier.

- Differentiation: Equity needs to stand out to retain customers.

- Brand Strength: Equity Group's strong brand helps mitigate this threat.

- 2024 Ranking: Ranked 2nd strongest banking brand in the world.

Equity Bank: Digital Shift Challenges

The threat of substitutes is elevated for Equity Bank, with fintech adoption hitting 65% in 2024. Neobanks saw a 20% customer base increase, highlighting the competition. To compete, Equity Bank must invest in user-friendly digital platforms.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Digital Banking | Increased Competition | 65% of adults using digital banking |

| Neobanks | Customer Base Growth | 20% growth in customer base |

| Customer Interaction | Frequency of Use | Mobile app usage 3-4 times weekly |

Entrants Threaten

Barriers to Entry

High barriers to entry significantly protect Equity Bancshares from new competitors. The banking sector demands substantial capital and compliance with strict regulations. Building customer trust also takes considerable time and resources. According to the 2025 IBM outlook, regulatory pressures, while challenging, also limit the entry of new banks.

Capital Requirements

New banks face hefty capital needs to launch and comply with rules. This financial barrier curbs new entries. The Basel III Endgame, discussed in Deloitte's banking outlook, could ease capital demands. However, stricter rules may still impact major players. In 2024, the average capital requirement for new banks in Kenya is around $20 million.

Regulatory Hurdles

Equity Bank faces regulatory hurdles, making it tough for new competitors. Getting licenses and following banking rules takes time and effort, which can be a barrier. The 10x Banking report highlights the increased focus on consumer protection and AI governance, signaling more regulatory checks. This increased scrutiny can discourage new banks from entering the market. In 2024, the regulatory environment in the banking sector has become even more complex, with stricter requirements for cybersecurity and data privacy.

Brand Recognition

Equity Bank, as an established player, benefits from strong brand recognition and customer loyalty, posing a significant hurdle for new entrants. New banks face the challenge of building brand awareness and trust from scratch, requiring substantial investments in marketing and advertising. In 2024, Equity Bank was affirmed as Kenya's most valuable brand, highlighting a considerable advantage. This existing brand strength makes it difficult for new competitors to gain a foothold.

- Equity Bank's brand value in 2024 is significantly higher than its competitors.

- New entrants must spend heavily on advertising.

- Customer loyalty to Equity Bank is a key factor.

Access to Distribution Channels

New banks face challenges in accessing distribution channels, as established players like Equity Bank already have extensive networks. To reach customers, new entrants must build their own channels or team up with existing ones. Equity Bank boasts a significant advantage with its vast network, making it tough for newcomers to compete. In 2024, Equity Bank Kenya's footprint included over 212 branches, over 42,622 agents, and more than 27,291 merchants.

- Established branch networks and online platforms are a barrier.

- New entrants require their distribution channels.

- Equity Bank's extensive network provides a competitive edge.

- Equity Bank Kenya had over 212 branches in 2024.

Equity Bank: Entry Barriers Remain High

The threat from new entrants to Equity Bank is low due to high barriers. Stiff capital requirements and strict regulations, as per the 2025 IBM outlook, limit new banks. Equity Bank's strong brand, with Kenya's top brand value in 2024, and wide distribution network are also deterrents.

| Factor | Impact on Entry | 2024 Data |

|---|---|---|

| Capital Needs | High Barrier | Kenya: $20M avg. requirement |

| Brand Recognition | High Barrier | Equity: Top brand value |

| Distribution | High Barrier | Equity: 212+ branches |

Porter's Five Forces Analysis Data Sources

Our analysis uses annual reports, regulatory filings, industry research, and financial news for a well-informed perspective.