Erin Energy Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Erin Energy Bundle

What is included in the product

Analyzes competitive forces like buyers/suppliers, rivals, and new entrants that affected Erin Energy.

Swap in your own data, labels, and notes to reflect the specific Erin Energy situation.

Preview the Actual Deliverable

Erin Energy Porter's Five Forces Analysis

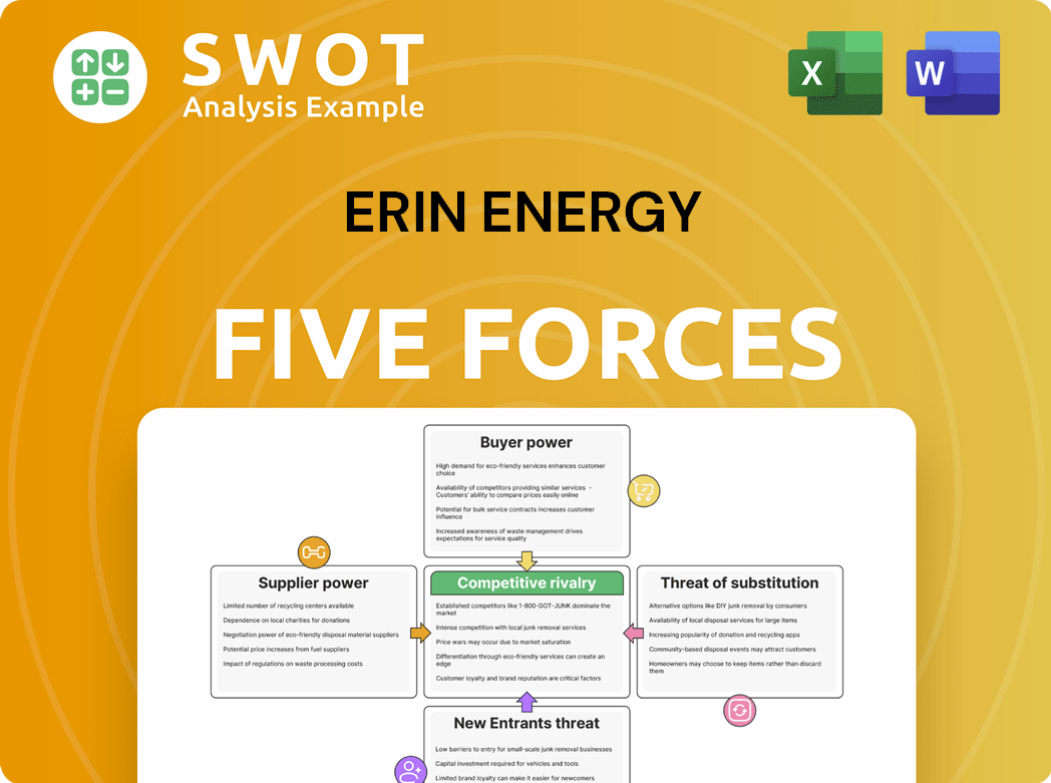

This preview details Erin Energy's Porter's Five Forces. It covers competitive rivalry, supplier power, buyer power, threat of substitutes, and threat of new entrants.

The analysis examines each force's influence, providing a comprehensive understanding of the industry's landscape. It includes key factors and potential impact on the company's strategy.

You're previewing the final version—precisely the same document that will be available to you instantly after buying.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

Erin Energy faced considerable challenges. Its bargaining power of suppliers was moderate due to specialized equipment. Buyer power, largely oil purchasers, presented a strong force. The threat of new entrants was low, influenced by high capital needs. Substitute products were a potential concern. Competitive rivalry within the oil industry remained intense.

Ready to move beyond the basics? Get a full strategic breakdown of Erin Energy’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Limited supplier options

Erin Energy, operating in sub-Saharan Africa, faced limited supplier choices for specialized oil and gas equipment and services. This constraint amplified supplier bargaining power. For example, in 2024, the cost of specialized drilling equipment in this region might be 15-20% higher due to fewer vendors. This situation allows suppliers to dictate terms more favorably.

Geographic concentration of suppliers

Erin Energy's suppliers' geographic concentration could amplify their bargaining power. Disruption in key regions directly impacts operations, increasing supplier leverage. Consider the logistical complexities and potential political risks tied to Erin Energy's operational areas. For example, in 2018, Nigeria, where Erin Energy had significant operations, faced logistical challenges impacting oil production.

Supplier's control over key resources

Suppliers with control over crucial resources like drilling rights or specialized tech wield significant power. This is especially true in the oil and gas sector, where these assets are vital. For instance, in 2024, the cost of advanced drilling equipment rose by about 7%. Assessing the criticality and uniqueness of these resources is vital for understanding their leverage.

Switching costs for Erin Energy

High switching costs boost supplier power; if Erin Energy faced these, it would be vulnerable. These costs include changing equipment or retraining staff, impacting both finances and operations. For example, if Erin Energy had specialized equipment, switching suppliers would be expensive. This would increase supplier influence over pricing and terms.

- High switching costs amplify supplier leverage, impacting negotiation dynamics.

- Financial and operational constraints tied to switching enhance supplier control.

- Specialized equipment requirements further elevate supplier bargaining power.

- This vulnerability affects pricing and the terms of supply agreements.

Impact of supplier costs on Erin Energy's profitability

Supplier costs significantly impact Erin Energy's profitability. If these costs form a large part of total expenses, suppliers gain substantial influence. Erin Energy would be highly sensitive to price hikes or changing supplier terms, directly squeezing profit margins. For example, in 2024, fluctuations in raw material prices could severely affect operational costs.

- High supplier costs increase operating expenses.

- Price changes directly affect profit margins.

- Suppliers' power is amplified by cost proportion.

Supplier Power: A 2024 Impact on Operational Costs

Erin Energy faced strong supplier bargaining power due to limited choices and specialized needs. High switching costs and reliance on critical resources further empowered suppliers. In 2024, these factors significantly influenced operational costs and profitability.

| Factor | Impact on Erin Energy | 2024 Data |

|---|---|---|

| Supplier Concentration | Reduced Negotiation Power | Equipment costs up 15-20% |

| Switching Costs | Increased Vulnerability | Specialized tech cost rose by 7% |

| Cost of Goods Sold (COGS) | Margin Squeeze | Raw material price fluctuations |

Customers Bargaining Power

Concentrated customer base

A concentrated customer base, where a few large customers account for a significant portion of Erin Energy's sales, increases buyer power. These large customers can exert pressure on pricing and contract terms. Evaluate the distribution of Erin Energy's customer base. For instance, if 80% of sales come from 3 clients, buyer power is high. This was the case in 2016, with a few key offtakers influencing contract terms.

Customer price sensitivity

Customer price sensitivity is crucial for Erin Energy. If customers are price-sensitive, they switch if prices increase. This limits Erin's ability to charge premium prices. Consider the competitive landscape. In 2024, oil prices fluctuated, impacting customer price sensitivity and the company's pricing power.

Availability of alternative suppliers

The availability of alternative suppliers significantly impacts customer power. If numerous oil and gas suppliers exist, customers gain more bargaining power, able to switch easily. This reduces Erin Energy's negotiation strength. In 2024, the global oil market featured diverse suppliers, increasing customer options and leverage.

Customer's access to information

Customers equipped with extensive market data, including prices, production costs, and supplier options, wield significant bargaining power. Transparency allows customers to negotiate better deals. Information access has reshaped this dynamic. In 2024, online retail sales reached $1.1 trillion in the US, showing customer control. This reflects the power of informed consumers.

- Online retail sales in the US reached $1.1 trillion in 2024.

- Transparency in markets empowers customers.

- Information access reshapes customer power.

Customer's ability to vertically integrate

If Erin Energy's customers could vertically integrate, meaning they could produce their own oil and gas, their bargaining power would surge. This threat of backward integration restricts Erin Energy's ability to set prices. This is especially pertinent for major energy consumers, like large industrial firms or utilities. The capacity for customers to self-supply alters the supply-demand dynamics. In 2024, crude oil prices fluctuated, impacting profitability and highlighting the importance of customer relationships.

- Vertical integration allows customers to bypass Erin Energy.

- It increases their negotiation leverage.

- Price sensitivity becomes a key factor.

- The threat of self-production impacts pricing.

Customer Power: Impacting Energy's Bottom Line

Customer bargaining power significantly influences Erin Energy's financial performance. Factors like a concentrated customer base and price sensitivity intensify customer leverage, impacting pricing. The availability of alternative suppliers also shapes customer power. Ultimately, customer access to data and the potential for vertical integration are key.

| Factor | Impact on Erin Energy | 2024 Data/Insight |

|---|---|---|

| Concentration | High buyer power | 2016: 80% sales from few clients |

| Price Sensitivity | Limits pricing | Oil price fluctuations in 2024 |

| Alternatives | Increased buyer power | Diverse global suppliers in 2024 |

Rivalry Among Competitors

High number of competitors

The oil and gas sector, especially in sub-Saharan Africa, is crowded. This boosts rivalry among numerous companies. It often results in price wars, squeezing profit margins. For example, in 2024, marketing costs surged by 15% due to fierce competition. This intense competition is a major challenge.

Slow industry growth

Slow industry growth often leads to fiercer competition among companies. In stagnant markets, firms battle for existing customers, increasing rivalry. Erin Energy faced this challenge. The oil and gas sector's growth in its operational areas was likely limited, intensifying competition. This environment likely led to price wars or increased marketing efforts.

High exit barriers

High exit barriers, like specialized equipment or long-term contracts, trap firms in the market, intensifying competition. This can cause oversupply and lower prices. Evaluate how easily businesses can leave the industry. For example, the airline industry's high asset specificity often leads to continued operations despite losses, intensifying rivalry. In 2024, the airline industry faced persistent price wars due to these factors.

Low product differentiation

Low product differentiation intensifies competitive rivalry. When products, like crude oil, are nearly identical, price becomes a key differentiator. This encourages businesses to compete aggressively on price. Differentiation strategies are critical to success.

- Crude oil prices in 2024 fluctuated, impacting profitability.

- Companies focused on operational efficiency to cut costs.

- Diversifying into differentiated products helped mitigate risks.

- Strong branding and customer service became vital.

Significant overcapacity

Significant overcapacity in the oil and gas market fuels fierce competition, pushing companies to leverage their assets, often leading to price declines and profit erosion. This intensifies existing rivalries. For instance, in 2024, global oil production reached approximately 100 million barrels per day, slightly exceeding demand, which put pressure on prices. This dynamic forces businesses to compete aggressively.

- Assess capacity utilization rates within the sector.

- Analyze the impact of oversupply on pricing models.

- Review the strategic responses of key competitors.

- Track global demand versus supply dynamics.

Oil & Gas Price Wars: A Fierce Battleground

Intense rivalry in the oil and gas sector, particularly in sub-Saharan Africa, often leads to aggressive price wars, impacting profit margins. Low product differentiation and overcapacity exacerbate competition, compelling firms to compete fiercely on price. High exit barriers keep firms in the market, intensifying rivalry, like the 15% surge in marketing costs in 2024.

| Factor | Impact | Example (2024) |

|---|---|---|

| Overcapacity | Price Pressure | Global oil production ~100M bpd |

| Product Similarity | Price Focus | Crude oil as a commodity |

| Exit Barriers | Sustained Rivalry | Specialized equipment, contracts |

SSubstitutes Threaten

Availability of alternative energy sources

The shift towards alternative energy sources significantly impacts the oil and gas industry. Solar and wind power are becoming increasingly competitive, reducing reliance on traditional fuels. For instance, in 2024, global renewable energy capacity additions surged, signaling a clear trend. This substitution threat grows with technological advancements and cost reductions in renewables.

Price performance of substitutes

If substitutes provide better value, customers may switch. This is especially true for those focused on price. Track the costs and performance of alternatives. For example, solar and wind costs have decreased significantly. In 2024, renewable energy adoption rose, impacting oil and gas demand.

Switching costs to substitutes

The threat of substitutes in the energy sector is amplified by low switching costs. If customers find it easy to switch to alternative energy, the threat is high. Think of solar panels; the move is becoming easier and cheaper. Government policies, like tax credits, also make switching more attractive. For example, in 2024, the US government offered substantial incentives for renewable energy adoption.

Level of product differentiation

The threat of substitutes for oil and gas is influenced by product differentiation. When oil and gas products are highly differentiated, the threat of substitutes decreases because they offer unique features. However, for general energy needs, differentiation is limited, increasing the likelihood of alternatives. Focusing on niche applications where oil and gas have a distinct advantage can mitigate this threat.

- In 2024, the global market for renewable energy is projected to reach $1.5 trillion.

- The demand for specialized lubricants, a differentiated oil product, is expected to grow by 4% annually.

- Electric vehicle sales increased by 35% in 2024, signaling a shift away from gasoline.

- The cost of solar energy has decreased by 10% in the last year, making it a more viable substitute.

Substitute producers' aggressiveness

Substitute producers' aggressiveness significantly influences the threat of substitution, particularly through marketing, innovation, and pricing. A dynamic and innovative substitute industry, like renewable energy, presents a heightened risk. Monitor the strategies of companies in the renewable energy sector for insights into their competitive approaches. For example, the solar energy market has seen substantial growth.

- Solar energy capacity additions globally reached a record 351 GW in 2023.

- Investment in renewable energy totaled $366 billion in 2023.

- The cost of solar PV has decreased by over 80% in the last decade.

- Companies like Enphase and SunPower are aggressively marketing their products.

Oil & Gas: Substitutes' Rising Threat

The threat of substitutes in the oil and gas industry is considerable, especially with rising renewable energy use. Renewable energy capacity additions grew significantly in 2024, signaling a clear shift. Factors like low switching costs and government incentives accelerate this threat. Product differentiation and the aggressive marketing of alternatives further exacerbate the situation.

| Factor | Impact | 2024 Data |

|---|---|---|

| Renewable Energy Growth | Increases substitution threat | Global renewable energy market projected to reach $1.5T. |

| Switching Costs | Influence of substitution | Electric vehicle sales increased by 35%. |

| Product Differentiation | Mitigates or enhances threat | Demand for specialized lubricants grew by 4%. |

Entrants Threaten

High capital requirements

High capital requirements significantly deter new entrants in the oil and gas sector. Exploration, development, and production demand substantial financial investment, creating a formidable barrier. New ventures often struggle to secure necessary funding, particularly in today's volatile market. In 2024, the average cost to drill a single offshore well is $150 million. This financial hurdle limits competition.

Government regulations and licensing

Stringent government regulations and licensing significantly hinder new entrants. Environmental compliance and safety standards, like those enforced by the EPA, demand substantial investments. For example, in 2024, the average cost for environmental permits in the oil and gas industry was $500,000. Understanding regional regulatory environments is crucial for assessing market entry feasibility.

Access to distribution channels

Establishing access to distribution channels is a significant hurdle for new oil and gas companies. Existing firms often control pipelines and transportation networks, creating a barrier. Building these channels requires substantial investment and regulatory approvals, increasing the risk. For example, in 2024, the average cost to build a new pipeline mile was over $2 million. The logistics and infrastructure landscape heavily favors established players.

Economies of scale

Economies of scale are a significant barrier. Established firms often have cost advantages that new entrants lack. This cost advantage makes it tough for newcomers to compete on price. Analyze the existing operations' scale and the cost advantages. For example, in 2024, Tesla's production scale gave it a clear cost edge in EVs.

- High initial investment

- Strong brand reputation

- Access to distribution channels

- Government regulations

Proprietary technology

Proprietary technology can be a significant barrier to entry. If established companies possess unique technology or hold patents, it's tough for newcomers to compete. This advantage gives existing firms an edge by potentially lowering costs or offering superior products. Identifying key technologies is crucial for assessing this threat.

- Patents and Intellectual Property: These protect innovations, making it harder for others to replicate.

- Research and Development: Ongoing investment in R&D can lead to exclusive technologies.

- Technological Advantage: A company's superior technology can result in higher quality or lower costs.

- Industry Examples: Consider the tech sector, where proprietary software or hardware creates significant barriers.

Breaking In: Tough Road Ahead

New entrants face substantial hurdles. High costs and complex regulations, like those from the EPA, are significant barriers. Established firms' scale and brand reputation add to the challenge. This makes it difficult for newcomers to compete effectively.

| Barrier | Impact | 2024 Example |

|---|---|---|

| Capital Needs | High initial investment | Offshore well: $150M |

| Regulations | Complex compliance | Permits: $500K |

| Distribution | Limited access | Pipeline mile: $2M+ |

Porter's Five Forces Analysis Data Sources

For Erin Energy, our analysis draws data from SEC filings, financial news outlets, and industry reports to assess competitive dynamics.