First Solar Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

First Solar Bundle

What is included in the product

Analyzes First Solar's competitive position, considering supplier/buyer power, and entry barriers.

Swap in your own data to reflect current business conditions, avoiding the need to manually update figures.

Preview the Actual Deliverable

First Solar Porter's Five Forces Analysis

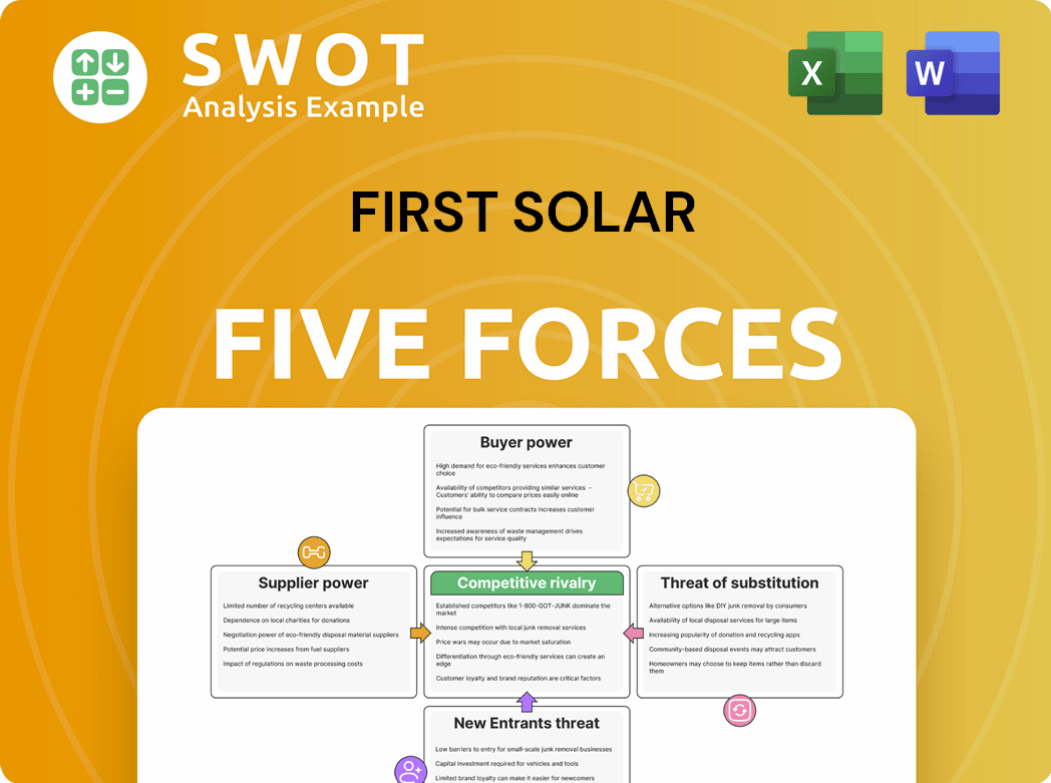

This preview details the complete First Solar Porter's Five Forces Analysis. The document examines competitive rivalry, supplier power, and other key forces.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

Analyzing First Solar's competitive landscape via Porter's Five Forces reveals key industry dynamics. Supplier power impacts profitability, especially with material costs. Buyer power stems from project developers and government incentives. The threat of new entrants is moderate, influenced by capital needs. Substitute threats arise from alternative energy sources. Competitive rivalry is high, driven by industry growth and competition.

Unlock key insights into First Solar’s industry forces—from buyer power to substitute threats—and use this knowledge to inform strategy or investment decisions.

Suppliers Bargaining Power

Limited Supplier Base

First Solar's dependence on a few suppliers for crucial components like cadmium telluride (CdTe) and specialized glass gives these suppliers leverage. This concentration can elevate costs and disrupt supply chains. Notably, a large portion of their CdTe comes from a single source. In 2024, First Solar's cost of revenue was approximately $2.8 billion, indicating the impact of material costs.

Specialized Components

First Solar faces substantial supplier power due to the specialized nature of its thin-film module components. Switching suppliers is costly, with qualification processes potentially costing over $2 million and taking months. This specialization bolsters existing suppliers' negotiation leverage. In 2024, First Solar's cost of sales was approximately $2.2 billion, highlighting the impact of supplier costs.

Increasing Demand for Solar

The rising demand for solar energy strengthens suppliers. Solar manufacturers compete for resources. Global solar PV capacity is projected to hit 4,800 GW by 2030, per the IEA. This boosts suppliers' bargaining power, enabling better terms in 2024.

Potential for Forward Integration

Suppliers possess the option of forward integration, possibly entering solar module manufacturing and competing directly with First Solar. This strategic move could amplify suppliers' influence, reshaping the competitive landscape. The feasibility of forward integration hinges on factors like access to capital and technological capabilities. The solar industry witnessed fluctuations in module prices, with average prices around $0.20-$0.25/watt in 2024.

- Technological advancements may lower the barriers for suppliers to enter the manufacturing sector.

- Access to capital is crucial for suppliers aiming to establish manufacturing facilities.

- The profitability of solar module manufacturing influences suppliers' decisions to integrate forward.

- Government incentives and policies can either encourage or discourage forward integration.

Strategic Relationships

First Solar strategically manages supplier relationships to counter supplier power. These strong partnerships help ensure a steady supply of materials, and potentially better prices. For example, one of First Solar's partners is building a new facility to support its Louisiana panel manufacturing site. This approach reduces the impact of supplier bargaining power.

- First Solar's strategic partnerships include long-term supply agreements.

- These agreements help to stabilize the supply chain.

- A new facility in Louisiana supports First Solar's 3.5-GW solar panel site.

- These relationships help manage costs and supply chain risks.

Supplier Power Dynamics in Solar Manufacturing

First Solar's reliance on specialized suppliers for key components, such as cadmium telluride (CdTe), gives suppliers considerable leverage, potentially increasing costs. The ability to switch suppliers is limited by high costs and lengthy qualification processes. The rising demand for solar energy worldwide further strengthens suppliers’ negotiating power, especially amid the projected growth to 4,800 GW by 2030.

| Aspect | Details |

|---|---|

| Cost of Revenue (2024) | ~$2.8 billion |

| Cost of Sales (2024) | ~$2.2 billion |

| Average Module Prices (2024) | $0.20-$0.25/watt |

Customers Bargaining Power

Large-Scale Customers

First Solar's main customers are major project developers and utilities, giving them strong bargaining power. For example, a large customer like Lighthouse BP can negotiate favorable terms. In 2024, First Solar's top 10 customers represented approximately 60% of total net sales. However, no single customer represents over 25% of their sales, limiting concentration risk.

Price Sensitivity

Customers in the solar industry are highly price-sensitive, focusing on cost and efficiency when selecting module options. This price sensitivity pushes First Solar to offer competitive prices, potentially impacting profit margins. Solar module prices have plummeted; IRENA reports a nearly 90% drop in the last decade, making solar cost-effective. This trend, coupled with government incentives, gives customers considerable bargaining power.

Switching Costs

Switching costs for customers are generally low. They can easily switch between solar module suppliers. In 2024, the solar industry saw increased competition. This led to price drops and technological advancements, making it easier for customers to switch. For instance, the average price of solar panels decreased by 10-15% in the first half of 2024.

Geographic Diversification

First Solar's broad geographic reach and diverse customer base serve as a buffer against customer bargaining power in certain areas. With projects spread across different countries, First Solar isn't overly reliant on any single market. This diversification helps to balance the influence of any one customer or region. For example, in 2024, First Solar has projects in the United States, Japan, and Australia.

- Geographic diversification reduces customer concentration risk.

- A broad customer base limits the impact of pricing pressure from any single buyer.

- First Solar's varied project locations enhance its resilience.

- This strategy supports stable revenue streams.

Long-Term Contracts

First Solar's long-term contracts with customers affect their bargaining power. These agreements offer stability, lessening immediate buyer pressure. The company's substantial order backlog, reaching to 2030, reflects this strategy. This helps shield them from fluctuating prices and buyer demands.

- Order Backlog: 73.3 gigawatts.

- Backlog Value: $21.7 billion.

- Contract Duration: Extends to 2030.

Navigating Customer Power in Solar Energy

First Solar faces customer bargaining power, especially from large project developers and utilities. Price sensitivity and easy switching between suppliers enhance this power. However, geographic reach, a diverse customer base, and long-term contracts mitigate customer influence.

| Factor | Impact | Mitigation |

|---|---|---|

| Price Sensitivity | High pressure on margins. | Competitive pricing, cost efficiencies. |

| Switching Costs | Low; easy supplier changes. | Product differentiation, value-added services. |

| Customer Concentration | Risk from major buyers. | Diversified customer base, long-term contracts. |

Rivalry Among Competitors

Intense Competition

The solar industry is fiercely competitive, with many manufacturers battling for market share. First Solar faces substantial rivalry, predominantly from crystalline silicon module producers. In 2024, the global solar panel market was dominated by Chinese companies, which accounted for over 80% of global solar panel manufacturing capacity. This intense competition puts pressure on pricing and innovation.

Price Competition

Price competition significantly impacts First Solar's profitability. The solar industry's overcapacity leads to aggressive pricing strategies among manufacturers. This can squeeze profit margins, as companies vie for market share. For example, in 2024, the average selling price per watt for solar modules decreased, reflecting intense price pressure.

Technological Innovation

Technological innovation fuels intense competition in the solar industry, pushing companies to enhance module efficiency and cut expenses. First Solar, a key player, leverages its distinct thin-film CdTe tech. This technology offers advantages like a smaller carbon footprint and superior high-temperature performance. In 2024, First Solar's module efficiency averaged around 19%, with ongoing efforts to boost this further, thus intensifying the rivalry.

Global Expansion

Solar companies are aggressively expanding worldwide, intensifying competition in diverse markets. The global shift toward clean energy makes solar power a crucial player. This expansion increases the number of competitors in different areas. In 2024, the global solar market is projected to reach $290 billion.

- Increased global solar installations in 2024 are estimated at 400-450 GW.

- Key markets experiencing significant growth include the US, China, and India.

- Competition is fierce, with companies like First Solar, and others vying for market share.

- This global expansion is driven by declining solar panel costs and supportive government policies.

Dominant Players

Competitive rivalry intensifies with the presence of major players. First Solar, a leading firm, exhibits strong competitive dynamics. Its solid financial position and profitable operations are key. First Solar's market share is approximately 50% in the US market as of Q1 2024.

- First Solar's revenue increased to $795 million in Q1 2024.

- The company's gross margin was 40% in Q1 2024.

- First Solar's cash and marketable securities totaled $1.6 billion.

Solar Industry: Fierce Competition Ahead

Competitive rivalry in the solar industry is marked by intense competition and price wars. Overcapacity and falling prices are significant challenges. First Solar contends with aggressive pricing and technological advances, especially from Chinese manufacturers.

| Metric | 2024 Data | Notes |

|---|---|---|

| Global Solar Market Size | $290 billion | Projected market size in 2024 |

| Global Solar Installations | 400-450 GW | Estimated increase in 2024 |

| First Solar Market Share (US) | ~50% (Q1 2024) | Dominant position in the US market |

SSubstitutes Threaten

Crystalline Silicon Modules

Crystalline silicon modules present a significant threat as a substitute for First Solar's thin-film modules. These modules compete directly, offering an alternative technology with specific benefits. They can be cheaper due to Chinese state support and economies of scale. In Q3 2024, the average selling price of crystalline silicon modules was around $0.18/W, while First Solar's was slightly higher. This price difference gives crystalline silicon a competitive edge.

Alternative Renewable Energy

The threat of substitutes for First Solar includes alternative renewable energy sources. These include wind, hydro, and geothermal, which can diminish the demand for solar modules. In 2024, wind and hydro accounted for a significant portion of renewable energy generation, posing a substitution risk. Emerging renewable technologies also challenge solar power's dominance. For example, in 2024, geothermal capacity grew, offering another alternative.

Energy Storage Solutions

Energy storage solutions, such as batteries, pose a threat to First Solar by enhancing the competitiveness of alternative energy sources. Pairing solar installations with energy storage systems makes them more reliable. This can potentially diminish the demand for First Solar's products. In 2024, the global energy storage market is valued at over $20 billion, demonstrating the growing importance of these alternatives.

Emerging Technologies

Emerging technologies pose a threat to First Solar. Perovskite solar cells, with their potential for higher efficiency and lower costs, are a key concern. This could lead to a shift in market share. Commercialization progress is a factor.

- Perovskite cells could reach 30% efficiency by 2024.

- Production costs of perovskites could be 20% lower than silicon by 2024.

- Investments in perovskite technology reached $1 billion globally in 2024.

- The market share of traditional solar cells could drop by 5% by 2024.

Hydrogen and Nuclear Energy

Hydrogen and nuclear energy present potential threats as substitutes for solar, although their widespread adoption faces challenges. Developments in these fields could offer alternative clean energy solutions, impacting solar's market share. The cost-effectiveness and scalability of hydrogen and nuclear technologies will be critical factors. However, solar energy's declining costs and increasing efficiency continue to be competitive advantages.

- Nuclear energy accounted for about 19% of U.S. electricity generation in 2023.

- The global hydrogen market was valued at $130 billion in 2023.

- Solar energy costs have decreased by over 80% in the last decade.

- Nuclear power plants have high upfront costs and long construction times.

Substitutes Challenge Solar's Dominance

The threat of substitutes for First Solar is significant. Crystalline silicon modules remain cheaper, with average selling prices around $0.18/W in Q3 2024. Wind, hydro, and geothermal pose substitution risks, accounting for a significant portion of renewable energy. Energy storage solutions, like batteries (a $20B+ market in 2024), enhance the competitiveness of alternative sources.

| Substitute | Impact | 2024 Data |

|---|---|---|

| Crystalline Silicon | Direct competition | $0.18/W average price |

| Wind/Hydro | Alternative renewables | Significant generation share |

| Energy Storage | Enhances alternatives | $20B+ global market |

Entrants Threaten

High Capital Requirements

The solar manufacturing sector demands substantial upfront capital, acting as a significant hurdle for newcomers. First Solar, for instance, needs massive initial investments for its panel production. As of 2024, setting up a new solar manufacturing plant could cost between $500 million and $1.2 billion, making entry difficult.

Technological Expertise

Manufacturing solar modules demands specialized know-how. First Solar's expertise in thin-film tech and patents creates a barrier. New entrants face challenges replicating this, hindering market entry. In 2024, First Solar's R&D spending was $170 million, showing its dedication to innovation. This technological advantage helps them stay competitive.

Economies of Scale

Established solar manufacturers like First Solar leverage economies of scale, creating a significant barrier for new entrants. This advantage stems from lower production costs per unit due to large-scale operations. In 2024, First Solar's module production capacity reached 11.8 GW, demonstrating its operational scale. New entrants struggle to compete with these established cost structures.

Government Regulations

Government regulations significantly shape the solar industry, influencing the entry of new competitors. Incentives like tax credits and subsidies, alongside renewable energy mandates, can attract new entrants. These policies can lower initial investment costs and create market demand, making entry more appealing. However, complex regulations and compliance costs can also act as barriers.

- In 2024, the US Inflation Reduction Act continues to offer substantial tax credits for solar projects, boosting market attractiveness.

- EU's Green Deal and similar initiatives globally are driving renewable energy mandates, increasing demand.

- Stringent permitting processes and interconnection standards can increase the complexity for new entrants.

- Changes in government support can shift market dynamics rapidly, impacting investment decisions.

Brand Recognition

First Solar benefits from strong brand recognition, especially within the US solar manufacturing sector. This established reputation and existing customer relationships create a significant barrier for new competitors. New entrants often struggle to quickly build the trust and market presence that First Solar has cultivated over years. This gives First Solar a competitive advantage in attracting and retaining customers.

- First Solar has a strong brand, making it hard for new companies to compete.

- They are well-known in the US solar market.

- Building trust takes time, which helps First Solar.

- This brand recognition helps keep customers.

Solar Startup Hurdles: High Costs & Scale

The solar industry sees high upfront costs, making it tough for new companies to enter. First Solar’s massive investments in its plants, which could cost up to $1.2 billion in 2024, demonstrate the capital intensity. Specialized tech and economies of scale also help established firms like First Solar.

| Barrier | Description | Impact |

|---|---|---|

| Capital Costs | High initial investment; manufacturing plant may cost up to $1.2 billion | Limits new entrants. |

| Tech & Scale | First Solar's tech know-how & large-scale operations | Difficult for newcomers to match. |

| Government Influence | Tax credits and regulations (e.g., IRA) | Can attract or deter entry. |

Porter's Five Forces Analysis Data Sources

The analysis utilizes financial reports, market research, and industry publications.