Sabra Health Care REIT Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Sabra Health Care REIT Bundle

What is included in the product

Tailored exclusively for Sabra, analyzing its position within its competitive landscape.

Clean, simplified layout—ready to copy into pitch decks or boardroom slides.

Full Version Awaits

Sabra Health Care REIT Porter's Five Forces Analysis

You're viewing the complete Sabra Health Care REIT Porter's Five Forces analysis. This is the final, ready-to-use document you will receive instantly after purchase. The analysis covers all five forces impacting Sabra. It's professionally formatted and ready for immediate use.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

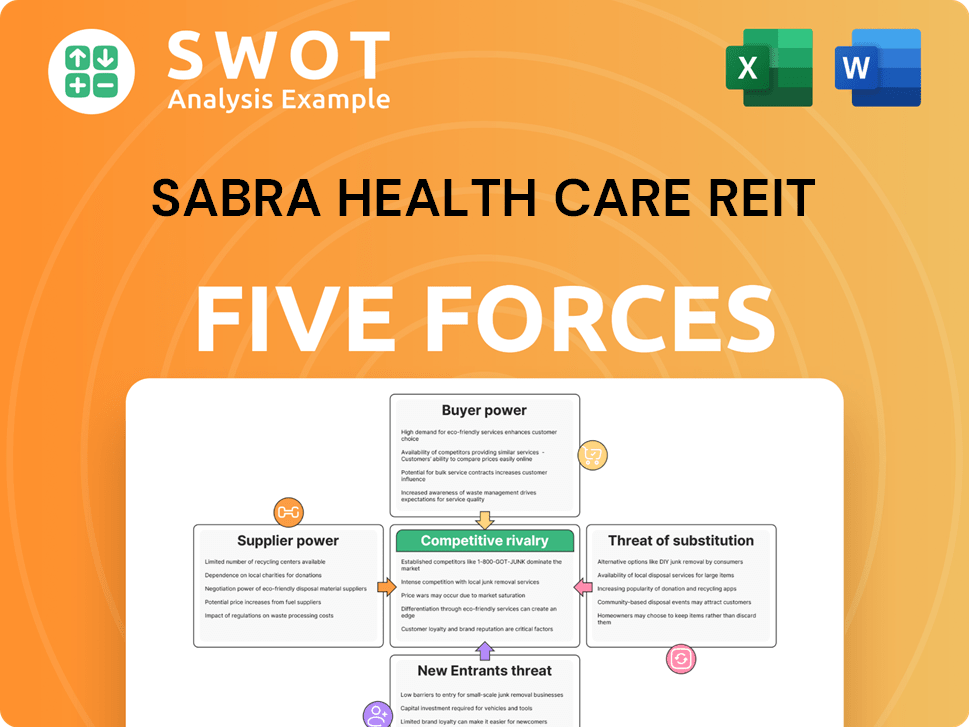

Sabra Health Care REIT faces moderate competition, largely due to the fragmented nature of the healthcare real estate market. Buyer power is significant, with healthcare providers negotiating lease terms. Supplier power is generally low due to the availability of diverse real estate options. The threat of new entrants is moderate, offset by regulatory hurdles and capital requirements. Substitutes, like alternative healthcare models, pose a moderate threat.

This preview is just the beginning. Dive into a complete, consultant-grade breakdown of Sabra Health Care REIT’s industry competitiveness—ready for immediate use.

Suppliers Bargaining Power

Limited specialized suppliers

Sabra Health Care REIT faces suppliers of property maintenance and medical equipment. The market for highly specialized suppliers in healthcare is often concentrated. Limited options can increase supplier bargaining power. For instance, in 2024, the cost of medical equipment rose by approximately 5%, impacting operational costs.

Regulatory compliance costs

Suppliers of regulated healthcare goods/services (medical tech, construction) face high compliance costs. These costs raise prices for Sabra, increasing supplier power. Healthcare's complexity shrinks the supplier pool. In 2024, healthcare spending in the US reached ~$4.8 trillion.

Labor market for healthcare staff

Sabra Health Care REIT is indirectly affected by the labor market for healthcare staff, as the operators of its facilities are the ones who employ these professionals. A competitive job market for nurses and therapists can drive up labor costs for these operators. In 2024, nursing salaries rose, with some states experiencing double-digit percentage increases, potentially straining operators' finances. This can influence their capacity to meet lease commitments, indirectly affecting Sabra. Staffing agencies and recruitment firms gain leverage in this scenario.

Economies of scale in supply

Larger suppliers, such as those providing medical equipment or pharmaceuticals, often leverage economies of scale, potentially increasing their bargaining power. This concentration can make REITs, like Sabra, more dependent, especially for large-volume purchases. For example, in 2024, the top three pharmaceutical companies controlled about 30% of the global market. Sabra, with its extensive portfolio, may be significantly influenced by these major players.

- Concentrated Supply: Large suppliers have significant market share.

- Volume Dependence: Sabra's needs can increase reliance on key suppliers.

- Pricing Influence: Suppliers can impact operational costs.

- Market Dynamics: Reflects broader industry trends.

Geographic concentration of suppliers

Sabra Health Care REIT's reliance on suppliers could be impacted by their geographic concentration. If key suppliers are limited to specific areas where Sabra operates, their bargaining power rises. This is particularly relevant if local regulations or licensing further limit the supplier pool. For example, in 2024, areas with strict healthcare facility regulations might see fewer qualified suppliers, increasing costs. This concentration could affect Sabra's operational expenses and profitability.

- Supplier availability can be limited by geographic location.

- Local regulations can restrict the number of suppliers.

- This situation could increase supplier bargaining power.

- Sabra's operational costs could be affected.

Supplier Dynamics Impacting Operational Costs

Sabra relies on healthcare suppliers, facing concentrated markets for specialized goods. Limited supplier options, especially with rising costs, bolster their power. In 2024, medical equipment costs increased by 5%, impacting Sabra's operational expenses.

Healthcare compliance costs and a smaller supplier pool further amplify supplier influence, as seen in the $4.8 trillion US healthcare spending in 2024. Labor market dynamics also play a part, with rising nursing salaries indirectly affecting Sabra through operator costs.

Larger suppliers leverage economies of scale, impacting Sabra, especially with major pharmaceutical firms controlling approximately 30% of the global market in 2024. Geographic concentration of suppliers, particularly where regulations are strict, can also heighten their bargaining power, potentially increasing Sabra's operational expenses.

| Factor | Impact | 2024 Data |

|---|---|---|

| Concentration | Raises Supplier Power | Top 3 Pharma: 30% market share |

| Cost Increases | Higher Operational Costs | Med. Equip. +5% |

| Regulations | Limits Suppliers | Strict licensing in some areas |

Customers Bargaining Power

Operator concentration

Sabra Health Care REIT's reliance on healthcare operators for lease revenue creates a dynamic of operator concentration. In 2024, a substantial portion of Sabra's income came from a limited number of key operators. This concentration gives these operators leverage in lease negotiations. For example, if a single operator accounts for over 10% of revenue, their decisions significantly impact Sabra's financial performance. This operator concentration can pressure Sabra to offer favorable lease terms to retain key tenants.

Government reimbursement pressures

Government programs like Medicare and Medicaid are key revenue sources for skilled nursing and senior housing facilities. In 2024, Medicare spending is projected to reach $973 billion, a significant portion of operator revenue. Changes in reimbursement rates directly affect operator profitability. This increases customer power, impacting Sabra's lease terms.

Tenant financial health

The financial stability of Sabra's healthcare operator tenants directly impacts their bargaining power. Financially distressed operators, facing issues like low occupancy or increased expenses, can seek rent reductions. In 2024, Sabra's portfolio occupancy was around 77%, highlighting the importance of tenant health. Lease defaults and bankruptcies can significantly hurt Sabra's revenue streams.

Availability of alternative properties

The bargaining power of Sabra's customers, healthcare operators, is affected by alternative property availability. An oversupply of similar healthcare facilities gives operators more options, strengthening their negotiation position. New construction or conversions can also boost supply, impacting operators' leverage. For instance, in 2024, the healthcare real estate market saw fluctuations, with some areas experiencing increased supply.

- Increased supply can lead to lower rental rates.

- Operators can seek out better lease terms.

- Sabra faces pressure to remain competitive.

- Market dynamics can shift bargaining power.

Lease term length

The length of lease terms significantly affects the bargaining power between Sabra Health Care REIT and its customers. Shorter lease terms empower operators with more frequent chances to renegotiate, strengthening their position. Conversely, longer lease terms offer Sabra stability but may expose them to risks if market conditions shift unfavorably. Sabra's weighted average lease term was 7.7 years in 2023. This balance is crucial.

- Shorter Lease Terms: Increase operator's bargaining power.

- Longer Lease Terms: Provide Sabra with stability.

- 2023 Weighted Average Lease Term: 7.7 years.

Healthcare Real Estate: Operator Power Dynamics

Sabra's customers, healthcare operators, have notable bargaining power. Operator concentration, with key tenants like those contributing over 10% of revenue, gives them leverage in lease negotiations. Government programs, such as Medicare's projected $973 billion spending in 2024, also influence operator profitability and thus their power. Factors like alternative property availability and lease terms further affect this dynamic.

| Factor | Impact on Operator Power | 2024 Data Point |

|---|---|---|

| Operator Concentration | Higher Power | Key tenants >10% revenue |

| Government Programs | Indirect Impact | Medicare ~$973B spending |

| Occupancy Rates | Impact tenant health | Sabra's ~77% |

Rivalry Among Competitors

Fragmented market

The healthcare REIT market presents a fragmented landscape. Sabra Health Care REIT competes with many REITs and private investors. In 2024, the healthcare REIT sector saw over $10 billion in transactions. This fragmentation can increase acquisition costs and lower yields.

Geographic overlap

Sabra Health Care REIT faces intense competition from other REITs and investors within its geographic markets. This overlap in focus leads to heightened competition for both tenants and potential property acquisitions. To succeed, REITs like Sabra might need to offer better lease terms or pay more for properties. In 2024, the healthcare REIT sector saw rising acquisition costs due to competition.

Focus on specific property types

Sabra Health Care REIT faces intense competition from REITs and investors targeting similar healthcare property types. This rivalry is particularly strong for prime skilled nursing and senior housing assets. In 2024, the senior housing sector saw significant investment, with transactions totaling over $8 billion. Competition drives the need for Sabra to offer competitive lease terms and acquisition strategies.

Capital availability

Capital availability significantly shapes the competitive dynamics within the REIT sector. Sabra Health Care REIT's ability to access capital at favorable terms directly affects its competitive positioning. Strong financial health allows for property acquisitions and development. This impacts Sabra's capacity to grow and compete effectively.

- Sabra's Q1 2024 net income was $63.3 million.

- As of Q1 2024, Sabra had $1.5 billion in available liquidity.

- Sabra's ability to issue equity and debt influences its competitive edge.

- Access to capital enables strategic investments and market expansion.

Regulatory changes

Regulatory shifts significantly affect healthcare REITs. Changes in healthcare laws and policies can reshape the competitive landscape. Some REITs may find new opportunities, while others might face hurdles. Adapting swiftly to these changes gives REITs a competitive edge. For instance, in 2024, the Centers for Medicare & Medicaid Services (CMS) implemented several changes impacting reimbursement rates, necessitating strategic adjustments by REITs like Sabra Health Care REIT.

- CMS updates in 2024 influenced facility reimbursements.

- REITs must navigate evolving compliance requirements.

- Adaptability is key to maintaining market position.

- Regulatory impacts vary by healthcare segment.

Healthcare REIT Dynamics: Sabra's Competitive Landscape

Sabra competes fiercely within a fragmented healthcare REIT market. Competition drives up acquisition costs and shapes lease terms. The availability of capital and regulatory changes also affect Sabra's competitive positioning.

| Factor | Impact on Sabra | 2024 Data |

|---|---|---|

| Competition | Higher costs, tighter margins | Over $10B in sector transactions |

| Capital | Influences growth, acquisition | Q1 Liquidity: $1.5B |

| Regulations | Requires strategic adaptation | CMS reimbursement changes |

SSubstitutes Threaten

Home healthcare

The increasing popularity of home healthcare poses a threat to skilled nursing facilities. As of 2024, the home healthcare market is valued at over $100 billion, reflecting its growth. This trend is fueled by technological advancements and the preference for care at home. Home healthcare offers a more convenient and often more affordable alternative, impacting demand for traditional facilities.

Assisted living alternatives

Independent and assisted living communities present a substitute for skilled nursing facilities. These options cater to seniors needing daily activity assistance without intensive medical care. In 2024, the assisted living market was valued at approximately $100 billion, showing its growing appeal. Seniors often prefer these communities for a more independent lifestyle, impacting skilled nursing facility demand.

Outpatient care

The rise of outpatient care poses a threat to Sabra Health Care REIT. Increasingly, services like diagnostics and treatments are moving outside hospitals. This shift potentially lowers demand for inpatient stays, impacting Sabra's SNF portfolio. In 2024, outpatient visits continued to rise, reflecting this trend.

Telehealth

Telehealth poses a threat to Sabra Health Care REIT as it offers alternatives to traditional care settings. Telehealth technologies are expanding access to healthcare services and enabling remote monitoring of patients' health. This shift can decrease the demand for in-person visits to healthcare facilities. These trends can impact the occupancy rates and revenue of skilled nursing and senior housing facilities.

- The global telehealth market was valued at $62.6 billion in 2023.

- The telehealth market is projected to reach $324.7 billion by 2030.

- Telehealth adoption rates increased significantly during the COVID-19 pandemic.

Community-based services

Community-based services pose a threat to Sabra Health Care REIT. These services, including adult day care and senior centers, offer alternatives to traditional care. They provide social interaction and assistance with daily living, potentially attracting residents away from Sabra's facilities. This shift can impact Sabra's occupancy rates and revenue.

- In 2024, the U.S. adult day care market was valued at approximately $2.5 billion.

- Senior centers served over 1 million older adults in 2023.

- These services are often more affordable, with costs ranging from $75 to $200 per day, versus $200+ for nursing homes.

- The increasing preference for aging in place further fuels this trend.

Healthcare's Shifting Sands: Substitutes Emerge

Substitutes like home healthcare, assisted living, and outpatient care pose risks. Telehealth's growth further challenges traditional facilities. Community services add to these pressures.

| Substitute | Market Value (2024) | Key Trend |

|---|---|---|

| Home Healthcare | $100B+ | Tech advancements, convenience |

| Assisted Living | $100B | Independent lifestyle |

| Telehealth (2023) | $62.6B | Remote healthcare expansion |

Entrants Threaten

High capital requirements

Developing or acquiring healthcare properties requires substantial capital investment. High capital requirements discourage new entrants, as evidenced by the $1.6 billion in assets Sabra Health Care REIT had in 2024. Securing financing is challenging for newcomers. The healthcare REIT market's high barriers limit new players.

Regulatory hurdles

The healthcare industry is tightly regulated, posing a substantial barrier. New entrants face intricate licensing, zoning, and compliance standards, increasing costs and time. These regulatory demands can slow down market entry. In 2024, healthcare regulation compliance costs increased by 10-15% for many providers.

Established relationships

Established players like Sabra Health Care REIT benefit from strong relationships. Sabra has built trust with healthcare operators and lenders. New entrants face challenges in gaining this industry confidence. These existing connections provide a competitive edge. For example, Sabra's portfolio includes over 400 properties as of 2024.

Economies of scale

Sabra Health Care REIT, like other large REITs, enjoys significant economies of scale. These advantages include lower property management costs and more favorable financing terms. New entrants often struggle to match these efficiencies, especially concerning acquisition costs. Achieving a competitive cost structure requires substantial scale, which can be a barrier.

- Sabra's market cap was approximately $3.2 billion as of early 2024, reflecting its size advantage.

- Larger REITs can secure financing at lower interest rates, impacting profitability.

- New entrants may face higher initial capital expenditure requirements.

Brand recognition

Established REITs, like Sabra Health Care REIT, possess significant brand recognition, a valuable asset in attracting both tenants and investors. This recognition stems from years of operating in the healthcare real estate sector, building trust and a solid reputation. New entrants face the challenge of competing with this established brand presence, which requires substantial investment in marketing and branding initiatives to gain visibility and credibility. Building a strong brand is crucial for attracting high-quality tenants and securing favorable investment terms, which can be a significant hurdle for newcomers.

- Sabra's market capitalization was approximately $2.89 billion as of May 2024.

- The healthcare REIT sector has a strong presence, with a total market capitalization of over $400 billion.

- New entrants often spend millions on marketing to build brand awareness.

- Established REITs benefit from existing relationships with healthcare providers.

Barriers to Entry: A Moderate Threat

The threat of new entrants to Sabra Health Care REIT is moderate due to high barriers. Substantial capital investment is needed; Sabra had $3.2B market cap in early 2024. Regulatory hurdles, like compliance costs (10-15% increase in 2024), also hinder entry.

| Factor | Impact | Example (2024) |

|---|---|---|

| Capital Requirements | High Barrier | Sabra's $3.2B Market Cap |

| Regulations | Increased Costs | 10-15% Rise in Compliance |

| Brand Recognition | Competitive Edge | Sabra's strong reputation |

Porter's Five Forces Analysis Data Sources

This Sabra analysis leverages SEC filings, healthcare industry reports, and financial statements to analyze competitive forces.