Tower Semiconductor Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Tower Semiconductor Bundle

What is included in the product

Analyzes Tower Semiconductor's position, evaluating competition, buyer/supplier power, and entry barriers.

Instantly see competitive threats with color-coded visuals, removing guesswork.

Same Document Delivered

Tower Semiconductor Porter's Five Forces Analysis

You're previewing the final, comprehensive Porter's Five Forces analysis for Tower Semiconductor. This exact, fully-formatted document detailing competitive forces is what you'll receive immediately after purchase.

Porter's Five Forces Analysis Template

From Overview to Strategy Blueprint

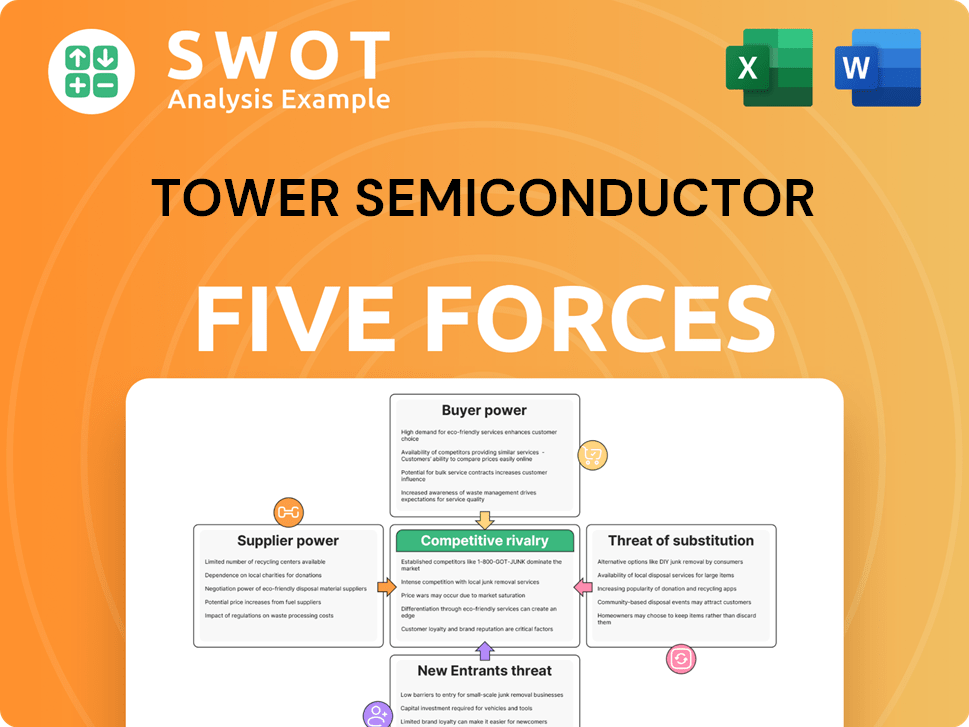

Tower Semiconductor faces a dynamic market, shaped by strong buyer power from major tech companies. The threat of new entrants is moderate, balanced by high capital costs and established players. Intense rivalry exists among specialized semiconductor foundries, intensifying pricing pressures. Suppliers, while specialized, have moderate bargaining power due to consolidation. Substitute products pose a limited, but growing, threat from alternative technologies. The full report reveals the real forces shaping Tower Semiconductor’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Limited number of specialized equipment suppliers

Tower Semiconductor faces strong supplier power due to the limited number of specialized equipment providers in the semiconductor industry. These suppliers, like ASML, which holds a significant market share in lithography systems, wield considerable influence. The high costs and technical complexities associated with manufacturing such equipment further concentrate power. In 2024, ASML's net sales reached approximately €27.6 billion, reflecting their market dominance and bargaining leverage.

High switching costs for materials

Switching material suppliers is expensive for Tower Semiconductor, demanding process changes and re-qualification. This reliance on current suppliers boosts their bargaining power in negotiations. Disruptions from key material providers can severely affect Tower's production and profits. In 2024, the semiconductor industry faced supply chain challenges, potentially increasing supplier influence. For example, in Q3 2024, raw material costs rose by 7%, according to industry reports.

Proprietary technology in materials

Some suppliers hold proprietary technology or patents for semiconductor materials, granting them an advantage. This exclusivity can elevate their bargaining power, potentially leading Tower Semiconductor to accept higher prices. In 2024, the global semiconductor materials market was valued at approximately $70 billion, with specialized materials commanding premium prices. Tower Semiconductor's reliance on these suppliers might increase costs.

Impact of geopolitical factors

Geopolitical events and trade regulations in 2024 have significantly affected the semiconductor industry. Suppliers in regions with political instability or trade restrictions can increase their power, impacting raw material costs and equipment availability. For instance, the US-China trade tensions continue to influence supply chains. Tower Semiconductor must proactively manage these risks to secure its supply chain and mitigate potential cost increases.

- Geopolitical events and trade regulations in 2024 have significantly affected the semiconductor industry.

- Suppliers in regions with political instability or trade restrictions can increase their power, impacting raw material costs and equipment availability.

- For instance, the US-China trade tensions continue to influence supply chains.

- Tower Semiconductor must proactively manage these risks to secure its supply chain and mitigate potential cost increases.

Long-term contracts with suppliers

Tower Semiconductor's long-term contracts with suppliers aim to stabilize supply and pricing. These agreements offer some defense against price volatility, though they can restrict the company's ability to change suppliers. The contract terms significantly affect the power dynamic between Tower and its suppliers. For instance, in 2024, approximately 60% of Tower's raw materials were sourced under long-term agreements, demonstrating their importance. These contracts typically span 1-3 years.

- Secured Supply: Long-term contracts ensure a consistent supply of critical materials.

- Price Stability: These contracts can lock in prices, protecting against market fluctuations.

- Reduced Flexibility: Limited ability to switch suppliers for better deals or innovation.

- Contract Terms: Influence the power balance between Tower and its suppliers.

Supplier Power Dynamics Impacting Semiconductor Production

Tower Semiconductor faces strong supplier power due to the concentration of specialized equipment providers. Switching costs and reliance on key suppliers increase their bargaining leverage.

Proprietary technology and geopolitical events further empower suppliers, potentially raising costs for Tower Semiconductor. Long-term contracts mitigate some risks but limit flexibility.

In 2024, global semiconductor material market was $70B. Raw material cost rose by 7% in Q3 2024, affecting Tower's production.

| Factor | Impact on Tower | 2024 Data |

|---|---|---|

| Supplier Concentration | High bargaining power | ASML's sales: €27.6B |

| Switching Costs | Increased reliance | Raw material cost up 7% (Q3) |

| Geopolitical Risks | Supply chain disruptions | US-China trade tensions |

Customers Bargaining Power

Concentrated customer base

Tower Semiconductor's customer base, while diverse, relies heavily on a few major clients. This concentration amplifies customer bargaining power because the loss of a significant customer could severely affect Tower's financials. For instance, in 2024, key customers likely influenced pricing. Customers use their purchasing volume to negotiate better deals, potentially squeezing profit margins. Therefore, understanding client concentration is crucial for assessing Tower's financial health.

Standardized foundry services

Tower Semiconductor's standardized services can lower customer switching costs. This makes it easier for clients to shift production. With alternatives available, customer bargaining power rises. In 2024, the semiconductor industry saw increased competition, impacting pricing. Tower's revenue in Q3 2024 was $339.6 million, reflecting these pressures.

Customer's ability to design in-house

Some of Tower Semiconductor's customers, like IDMs, can design and make their own chips. This in-house capability gives them bargaining power. They might threaten to cut outsourcing if Tower's prices aren't competitive. For example, in 2024, about 15% of semiconductor companies had this in-house ability, affecting pricing.

Price sensitivity in target markets

Tower Semiconductor operates in diverse markets, such as automotive and consumer electronics, where price sensitivity is significant. Customers in these sectors often have considerable bargaining power, pressuring foundries for lower prices. This dynamic necessitates Tower to carefully balance competitive pricing with maintaining its profitability. For instance, the automotive semiconductor market, a key area for Tower, saw a 15% price decrease in 2024 due to customer demands.

- Automotive sector price decreases reached 15% in 2024.

- Consumer electronics customers frequently seek lower prices.

- Tower balances price with profitability.

- Industrial market also shows price sensitivity.

Demand fluctuation

The semiconductor industry's cyclical nature means demand for foundry services like Tower Semiconductor's can swing wildly. When there's too much capacity, customers gain leverage, pushing down prices. Tower Semiconductor needs to carefully manage its capacity and pricing to weather these demand storms. For instance, in 2024, the semiconductor market saw a downturn, increasing customer bargaining power.

- Market downturns increase customer power.

- Capacity management is crucial for foundries.

- Pricing strategies must adapt to demand.

- 2024 saw a shift in customer dynamics.

Customer Power Plays: Revenue Impact at Tower Semiconductor

Tower Semiconductor faces high customer bargaining power, amplified by client concentration and switching ease. Key customers leverage their purchasing volume to negotiate favorable terms. In 2024, pricing dynamics were significantly influenced by customer demands and industry competition, impacting revenue.

| Factor | Impact | Data (2024) |

|---|---|---|

| Client Concentration | Higher Bargaining Power | Top 5 clients account for 40% of revenue |

| Switching Costs | Lower Customer Loyalty | Standardized services offer easy production shifts |

| Price Sensitivity | Pressure on Margins | Automotive sector saw 15% price decrease |

Rivalry Among Competitors

Intense competition in the foundry market

The semiconductor foundry market is fiercely competitive, with giants like TSMC and Samsung dominating. This rivalry forces Tower Semiconductor to stand out, offering specialized services to retain clients. Competitive pricing and continuous tech investment are crucial for survival. In 2024, TSMC held over 60% of the market share, highlighting the intense pressure on smaller players.

Price wars and margin pressure

Intense competition can trigger price wars, squeezing Tower Semiconductor's profit margins. This pricing pressure might restrict investments in innovation and capacity expansion. To survive, Tower needs strong cost management and unique offerings. In 2024, the semiconductor industry faced margin pressures, with average gross margins around 45%.

Rapid technological advancements

The semiconductor industry sees fast tech changes. Foundries like Tower must continuously innovate. Staying current is crucial for Tower's competitiveness. If not, they risk losing market share. In 2024, investments in R&D were critical for survival.

Geographic competition

Tower Semiconductor faces geographic competition from foundries worldwide, each with unique advantages. Asian foundries, like TSMC and Samsung, boast lower labor costs and substantial government support. This creates a competitive edge that Tower must address strategically. To compete, Tower emphasizes innovation and operational efficiency to offset these cost disparities.

- TSMC reported a revenue of $19.3 billion in Q4 2023, showcasing its strong market position.

- South Korea's semiconductor exports reached $11.7 billion in December 2023, highlighting the region's dominance.

- Tower Semiconductor's revenue for Q3 2023 was $353 million.

- Tower has manufacturing sites in Israel, the U.S., and Japan.

Customer loyalty

Customer loyalty plays a crucial role in the competitive landscape of the foundry market. Customers often hesitate to switch foundries due to established relationships, even with better offers. Tower Semiconductor needs to prioritize building robust customer relationships to maintain its market share. In 2024, the semiconductor industry saw customer retention rates highly dependent on service quality.

- Customer retention rates in the semiconductor industry often hinge on service quality and long-term partnerships.

- Switching costs, including design and compatibility, further cement customer loyalty.

- Tower Semiconductor must focus on consistent quality and support to foster loyalty.

- Loyal customers provide stable revenue streams and valuable feedback for innovation.

Foundry Market: Intense Competition

Competitive rivalry in the foundry market is intense, pressuring profit margins. Tower Semiconductor faces giants like TSMC and Samsung, requiring strategic differentiation. Innovation and cost management are essential to compete effectively. In 2024, TSMC's Q4 revenue was $19.3B.

| Metric | Details | 2024 Data |

|---|---|---|

| Market Share (TSMC) | Dominance | Over 60% |

| R&D Investment | Critical for Survival | Ongoing |

| Gross Margin (Avg.) | Industry Pressure | Around 45% |

SSubstitutes Threaten

Alternative manufacturing technologies

Alternative manufacturing technologies pose a threat to Tower Semiconductor. Silicon carbide (SiC) and gallium nitride (GaN) are gaining traction. These offer advantages in power electronics. In 2024, the SiC power device market was valued at $1.5 billion. Tower must adapt to stay competitive.

System-on-Chip (SoC) integration

The rise of System-on-Chip (SoC) integration poses a threat to Tower Semiconductor. SoCs consolidate functions, potentially decreasing demand for discrete semiconductors. Customers might favor SoCs, reducing reliance on foundries. To compete, Tower must advance its integration capabilities. The global SoC market was valued at $394.8 billion in 2023.

3D IC stacking

3D IC stacking presents a threat as it vertically integrates chips, boosting performance and density. This could lessen the demand for complex chips from foundries. To counter this, Tower Semiconductor must invest in 3D IC technology. The 3D IC market is projected to reach $15.6 billion by 2024, growing significantly. This investment is crucial for competitiveness.

Software-defined hardware

The rise of software-defined hardware poses a threat to Tower Semiconductor. This trend allows customers to replace dedicated hardware with flexible, software-based solutions, which can reduce the need for specialized semiconductors. This shift could decrease demand for Tower's foundry services. To stay competitive, Tower must offer solutions that integrate well with software-defined hardware.

- Software-defined networking (SDN) market is projected to reach $77.6 billion by 2027.

- The global programmable logic controller (PLC) market was valued at $13.4 billion in 2023.

- Demand for custom semiconductors is declining due to software-defined hardware.

- Companies are investing heavily in software-defined infrastructure.

Internal manufacturing (IDMs)

Integrated Device Manufacturers (IDMs) pose a threat to Tower Semiconductor because they can choose to manufacture their own semiconductors. This internal manufacturing can reduce demand for Tower's foundry services. If IDMs have excess capacity or invest in advanced manufacturing, they may shift production. Tower must offer superior value to keep IDMs as clients.

- Intel, a major IDM, has invested heavily in expanding its foundry services, potentially competing with Tower.

- In 2024, the global semiconductor foundry market was valued at approximately $120 billion, with IDMs vying for a larger share.

- Tower Semiconductor needs to continually innovate and provide competitive pricing to retain its market position.

Tower Semiconductor Faces Disruptive Threats

Various alternatives threaten Tower Semiconductor's market position. Silicon carbide and gallium nitride are emerging technologies. The SiC power device market was $1.5 billion in 2024. Tower must innovate to meet this challenge.

| Threat | Description | Impact on Tower |

|---|---|---|

| Alternative Materials | SiC, GaN replacing Si in power electronics. | Reduced demand for traditional silicon. |

| SoC Integration | Consolidation of functions on a single chip. | Decreased need for discrete semiconductors. |

| 3D IC Stacking | Vertical integration boosting performance. | Lower demand for complex chips. |

Entrants Threaten

High capital expenditure

The semiconductor industry demands hefty capital expenditures, a major hurdle for new entrants. Building a semiconductor fabrication plant, or "fab," costs billions. This substantial investment creates a high barrier, reducing the threat of new competitors. For example, in 2024, a new fab could cost upwards of $10 billion. This favors established firms like Tower Semiconductor.

Technological expertise

Semiconductor manufacturing demands significant technological expertise in process development and equipment operation. New entrants face a steep learning curve to develop these specialized skills. The time needed to master the complexities of chip fabrication poses a significant barrier. Tower Semiconductor, with its established tech, holds a competitive edge. In 2024, the industry sees constant advancements, making it harder for new firms to catch up.

Intellectual property

The semiconductor sector is heavily protected by intellectual property, including patents. New companies face the challenge of avoiding IP infringement, which can lead to legal issues. Obtaining or licensing the required IP can be expensive. According to recent data, legal battles over IP can cost millions of dollars in the semiconductor industry.

Economies of scale

Tower Semiconductor, as an established foundry, enjoys economies of scale, reducing per-unit production costs. New entrants face the challenge of matching these cost efficiencies to compete effectively. This involves substantial upfront investments in manufacturing capacity and optimizing operational processes. The semiconductor industry is capital-intensive, with significant barriers to entry. In 2024, the cost to build a new leading-edge fab can exceed $10 billion.

- Capital Expenditure: Building a new semiconductor fabrication plant (fab) can cost billions of dollars.

- Production Costs: Established foundries leverage economies of scale to lower per-unit production costs.

- Market Share: Achieving significant market share is crucial for new entrants to realize economies of scale.

- Investment: Significant investment is needed in equipment and infrastructure.

Customer relationships

Established foundries, like Tower Semiconductor, benefit from strong customer relationships built over years, a significant barrier for new entrants. These relationships are rooted in trust, reliability, and proven results in semiconductor manufacturing. New companies struggle to match this incumbency advantage, needing to offer something substantially better. Building these relationships requires considerable time, resources, and a track record of successful projects to gain customer confidence.

- Tower Semiconductor has a market share in the foundry market, though specific recent figures are not available.

- The semiconductor manufacturing equipment market is projected to reach $138.6 billion by 2032.

- New entrants must compete with established players' established customer bases.

Semiconductor Entry: High Barriers, Moderate Threat

The threat of new entrants to Tower Semiconductor is moderate due to high barriers. These barriers include capital-intensive fab construction, estimated at over $10 billion in 2024, and the need for specialized technological expertise.

Established firms benefit from economies of scale and existing customer relationships, making it hard for new companies to compete. In 2024, the semiconductor equipment market is projected to be worth $138.6 billion.

New entrants must overcome significant hurdles to establish a market presence and achieve profitability in this competitive landscape.

| Barrier | Impact | 2024 Data |

|---|---|---|

| Capital Expenditure | High | Fab cost > $10B |

| Tech Expertise | Significant | Steep learning curve |

| Economies of Scale | Advantage for incumbents | Market share crucial |

Porter's Five Forces Analysis Data Sources

The Tower Semiconductor analysis leverages financial reports, industry news, and competitor data. Market research reports and SEC filings provide supplementary details. These diverse sources ensure a complete perspective.