ProAssurance Bundle

What's the Story Behind ProAssurance Company?

Ever wondered how a company becomes a cornerstone of the healthcare industry? ProAssurance Company's journey is a testament to resilience and strategic growth. From its humble beginnings, it has evolved into a leading insurer, protecting those who heal. Dive into the ProAssurance SWOT Analysis to understand its strategic position.

ProAssurance's story begins in 1976, born from the need for stable healthcare liability insurance. The company's evolution showcases how it has adapted and expanded its offerings, including medical professional liability and risk management solutions. Understanding the ProAssurance history reveals a commitment to its mission and a deep understanding of the needs of healthcare providers. This brief overview of ProAssurance highlights its significant impact on the insurance landscape.

What is the ProAssurance Founding Story?

The story of ProAssurance Company, a key player in the healthcare liability insurance sector, began in 1976. It was founded as Mutual Assurance in Birmingham, Alabama. This launch was a direct response to the instability in the medical malpractice market during the 1970s.

The founders, which included physicians, aimed to create a financially stable insurance company. Their goal was to defend against baseless claims rather than settling them for convenience. The company issued its first policy on April 1, 1977. This marked the beginning of ProAssurance history.

Initially structured as a mutual insurer, policyholders were the owners. In 1991, Mutual Assurance transitioned to a publicly owned company, changing its name to Medical Assurance, Inc. The name ProAssurance was officially adopted in June 2001, following the merger of Medical Assurance, Inc. and Professionals Group, Inc. This merger was a significant step in the company's growth.

Key Events in ProAssurance's Founding and Evolution

The company's journey reflects strategic responses to market needs and a commitment to financial strength.

- 1976: Mutual Assurance is established in Birmingham, Alabama, to address the medical malpractice crisis.

- 1977: The first insurance policy is issued, marking the operational start.

- 1991: Mutual Assurance demutualizes and becomes Medical Assurance, Inc.

- 2001: Medical Assurance, Inc. merges with Professionals Group, Inc., and adopts the name ProAssurance. This merger enhanced its financial position and industry leadership.

Professionals Group, Inc. originated from the Brown-McNeeley Fund, established in Michigan in 1975. This fund provided medical professional liability insurance. The merger in 2001 was crucial for nationwide expansion. It also strengthened the company's financial position and industry leadership. For more insights into how ProAssurance approaches its market, consider exploring the Marketing Strategy of ProAssurance.

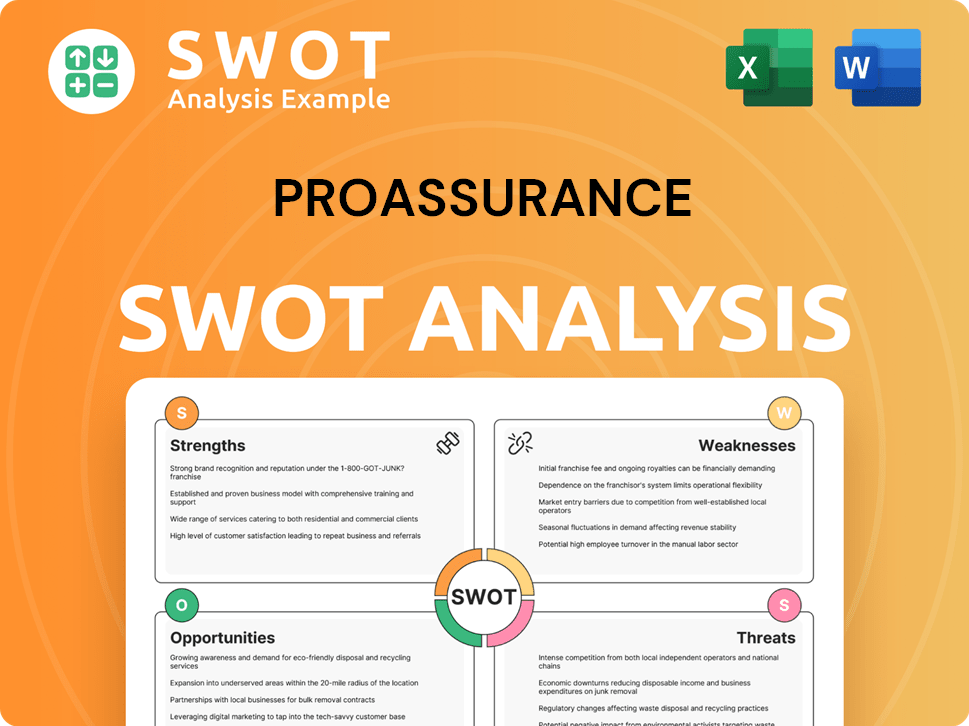

ProAssurance SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of ProAssurance?

The early years of ProAssurance Company, then known as Medical Assurance, Inc., were marked by strategic growth and expansion. This involved a series of acquisitions designed to broaden its market presence and strengthen its financial position within the medical professional liability sector. These early moves set the stage for the company's future development and its evolution into a major player in healthcare liability insurance.

In 1999, Medical Assurance acquired Medical Defense Associates, enhancing its presence in Missouri. The company continued its expansion by acquiring Dependable Protective Mutual in 2000 and OUM in 2001. These acquisitions were crucial for establishing a solid foundation for future growth.

A key milestone occurred in June 2001 when Medical Assurance merged with Professionals Group to form ProAssurance Corporation. This merger was pivotal, setting the stage for significant nationwide expansion. It also strengthened the company's balance sheet and positioned it for industry leadership.

By 2005, ProAssurance had over $3.2 billion in assets and gross written premiums exceeding $750 million. The company had licenses to operate in more than 45 states. ProAssurance was recognized as the fourth largest writer of medical professional liability insurance.

In 2005, ProAssurance acquired NCRIC Group, Inc., expanding its reach in Washington, D.C., and the Mid-Atlantic states. The company continued its acquisitive strategy in 2006 by acquiring Physicians Insurance Company of Wisconsin, Inc. (PIC Wisconsin).

In 2008, ProAssurance acquired Mid-Continent General Underwriters and Georgia Lawyers Insurance Company (GLIC). A significant acquisition in 2009 was Podiatry Insurance Company of America (PICA). The company entered the Texas market in 2010.

The Certitude program, a partnership with Ascension Health, was launched in 2010. In 2013, ProAssurance acquired Medmarc Insurance Group. By 2014, ProAssurance became the majority capital provider to Syndicate 1729 at Lloyd's of London.

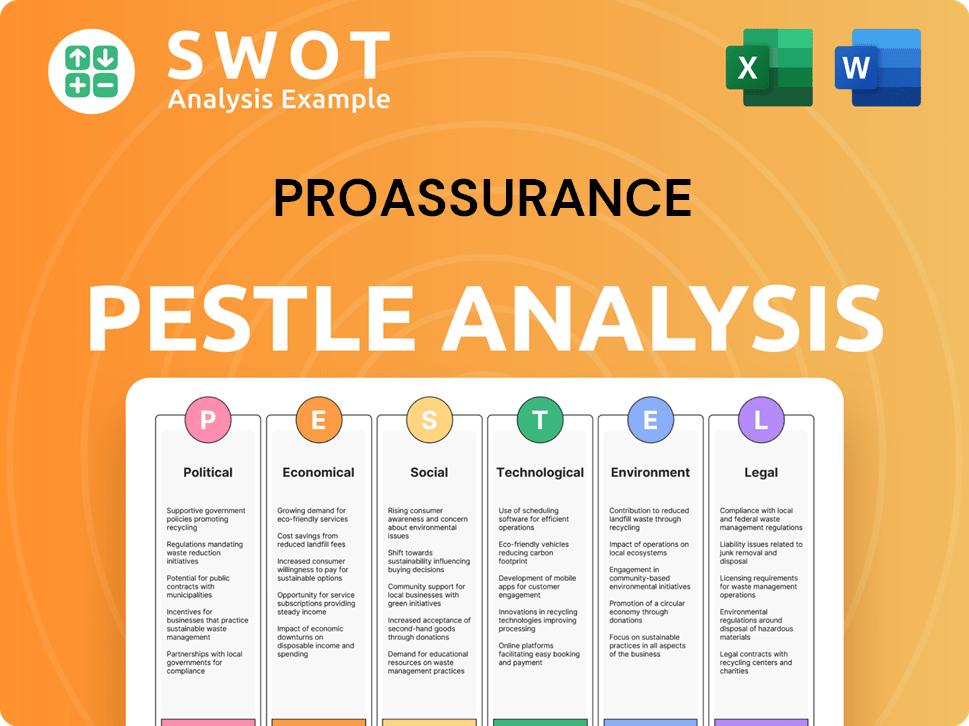

ProAssurance PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in ProAssurance history?

The ProAssurance Company has a rich ProAssurance history, marked by strategic moves and a commitment to the Medical professional liability sector. Key decisions have propelled the company to its current standing as a significant player in the Healthcare liability insurance market.

| Year | Milestone |

|---|---|

| 2021 | Acquired NORCAL Group, becoming the third-largest writer of medical professional liability insurance by U.S. market share. |

| 2024 | Implemented new integrated policy, claims, risk management, and billing systems. |

| Ongoing | Focus on disciplined underwriting and rate adequacy to maintain profitability. |

ProAssurance has consistently focused on innovation to improve its operations and services. The implementation of new integrated systems in early 2024 demonstrates its commitment to technological advancement, paving the way for future innovations.

Technology Integration

ProAssurance invested in new integrated policy, claims, risk management, and billing systems, launched in early 2024. These systems are designed to improve efficiency and streamline operations.

AI and Data Analytics

The company is exploring the use of AI and data analytics in underwriting and claims processes. This is aimed at enhancing profitability and productivity.

Workflow Solutions

ProAssurance plans to launch a state-of-the-art workflow solution and online portal. This will further streamline processes and improve user experience.

Straight-Through Processing

The company aims to implement straight-through processing technologies. This is expected to reduce costs and improve operational efficiency by 2025.

ProAssurance Company has navigated various challenges, including market downturns and industry-specific issues. The company's response to the COVID-19 pandemic and ongoing market challenges reflects its adaptability.

Market Volatility

The company faces challenges from market downturns and the evolving landscape of Medical professional liability. These factors require continuous adaptation and strategic planning.

Industry Challenges

ProAssurance deals with rising losses, staffing shortages, and changes in healthcare delivery. The company is responding with disciplined underwriting.

Financial Performance

Renewal pricing remained strong at 8% for Q4 2024 and 9% for the full year. The Specialty P&C segment combined ratio improved by 3.9 percentage points in Q4 2024 and 4.8 percentage points for the full year.

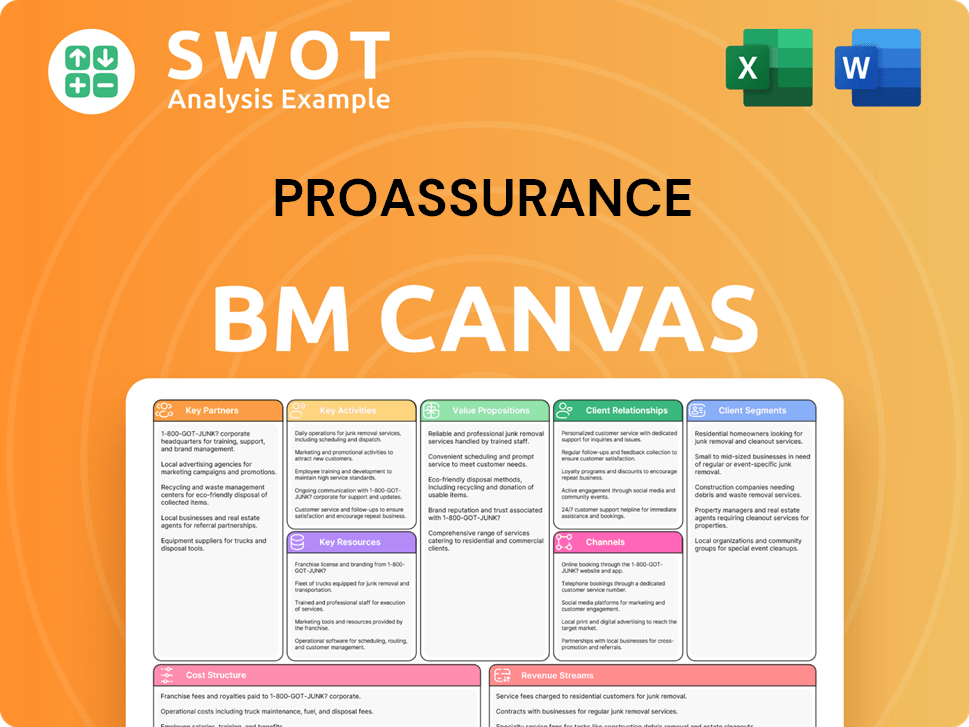

ProAssurance Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for ProAssurance?

Here's a brief overview of the ProAssurance history, highlighting key milestones of the ProAssurance Company.

| Year | Key Event |

|---|---|

| 1976 | Founded as Mutual Assurance in Birmingham, Alabama. |

| 1977 | Wrote its first policy on April 1. |

| 1991 | Demutualized and renamed Medical Assurance, Inc. |

| 1999 | Medical Assurance assumes the business of Medical Defense Associates. |

| 2001 | Medical Assurance and Professionals Group merge to form ProAssurance Corporation. |

| 2005 | Acquired NCRIC Group, Inc. |

| 2006 | Acquired Physicians Insurance Company of Wisconsin, Inc. (PIC Wisconsin). |

| 2008 | Acquired Mid-Continent General Underwriters and Georgia Lawyers Insurance Company (GLIC). |

| 2009 | Acquired Podiatry Insurance Company of America (PICA). |

| 2010 | Acquired American Physicians Service Group, Inc., entering the Texas market, and announced the Certitude program with Ascension Health. |

| 2013 | Acquired Medmarc Insurance Group, expanding into medical products and life sciences liability. |

| 2014 | Became majority capital provider to Syndicate 1729 at Lloyd's of London and acquired Eastern Insurance Holdings, Inc. |

| 2017 | Endowed the University of Alabama School of Medicine with $1.5 million for the ProAssurance Endowed Chair for Physician Wellness. |

| 2020 | Announced the acquisition of NORCAL Group and responded to the COVID-19 pandemic with premium reductions and resources. |

| 2021 | Closed the acquisition of NORCAL Group, making ProAssurance the third largest writer of medical professional liability insurance by U.S. market share. |

| 2023 | Entered a partnership with Caresyntax to provide surgical intelligence tools to insured surgeons. |

| 2024 | Implemented a new integrated policy, claims, risk management, and billing system. |

| 2025 | On March 19, 2025, The Doctors Company announced an agreement to acquire ProAssurance Corporation for $25.00 per share in cash, a transaction valued at approximately $1.3 billion. The transaction is expected to close in the first half of 2026. |

ProAssurance is focused on capturing a larger share of the medical professional liability and workers' compensation insurance markets, emphasizing profitability over growth. They prioritize rate adequacy and selective underwriting. The company leverages proprietary data and predictive analytics for enhanced risk management.

ProAssurance aims to achieve a long-term Return on Equity (ROE) of 700 basis points above the 10-year U.S. Treasury rate, which was approximately 11.6% at the end of 2024. This demonstrates a commitment to strong financial performance. Prudent investment management is also a key strategy.

The company is focused on enhancing operational efficiency through leveraging enhanced scope and scale. This approach is designed to streamline processes and improve overall performance. This is a key aspect of their long-term strategy.

The pending acquisition by The Doctors Company, expected to close in the first half of 2026, will create a combined company with approximately $12 billion in assets. This merger will solidify its position as the second-largest medical malpractice insurance company in the U.S. and the largest physician-owned carrier. The merger reflects a shared vision.

ProAssurance Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of ProAssurance Company?

- What is Growth Strategy and Future Prospects of ProAssurance Company?

- How Does ProAssurance Company Work?

- What is Sales and Marketing Strategy of ProAssurance Company?

- What is Brief History of ProAssurance Company?

- Who Owns ProAssurance Company?

- What is Customer Demographics and Target Market of ProAssurance Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.