Visa Bundle

How did a simple credit card revolutionize global finance?

Journey back to 1958, when Bank of America's BankAmericard sparked a financial revolution that would eventually become Visa. This bold initiative introduced the first consumer credit card program in the U.S., forever changing how we pay. From its humble beginnings in Fresno, California, Visa's mission was to create a universal payment solution, a vision that would reshape the world of commerce.

This Visa SWOT Analysis will delve into the fascinating Visa history, exploring the Visa company's evolution from its early days to its current status as a global payments giant. Discover the key milestones, the Visa founder's vision, and the strategic decisions that propelled Visa credit card to the forefront of the financial industry. Learn about Visa's impact on electronic payments and the historical events that shaped its journey.

What is the Visa Founding Story?

The story of the [Company Name] began on September 18, 1958, when Bank of America (BofA) introduced the BankAmericard credit card program in Fresno, California. This marked the initial step in what would become a global financial powerhouse. This early initiative set the stage for the Visa history we know today.

Joseph P. Williams, from BofA's Customer Services Research Group, spearheaded this effort. His goal was to simplify the payment process by replacing multiple credit accounts with a single, versatile credit card. This vision laid the groundwork for the Visa company's future.

BofA directly issued and managed these cards. The initial rollout, however, faced challenges. The program's evolution from a single bank's offering to a global network is a key part of the Visa timeline.

Early Days of Visa

The BankAmericard program started with a massive distribution of 65,000 unsolicited credit cards in Fresno.

- By March 1959, the program expanded to San Francisco and Sacramento.

- By June, BofA was distributing cards in Los Angeles.

- By October, over 2 million credit cards were in circulation across California, accepted by 20,000 merchants.

- The initial rollout faced challenges, including credit card fraud, leading to changes in management.

The BankAmericard aimed to be a universally accepted payment solution. Dee Hock, who later played a crucial role in Visa's evolution, joined the program in 1968. Hock recognized the issues arising from Bank of America licensing the BankAmericard program to other financial institutions. He noticed problems with 'interchange' transactions between banks.

In 1970, BofA gave up direct control. National BankAmericard Inc. (NBI), a cooperative of issuer banks, was formed to manage the program. Dee Hock became its president and CEO. This cooperative model was a significant shift, paving the way for Visa's journey to becoming a global brand. For more insights into the company's growth, you can explore the Growth Strategy of Visa.

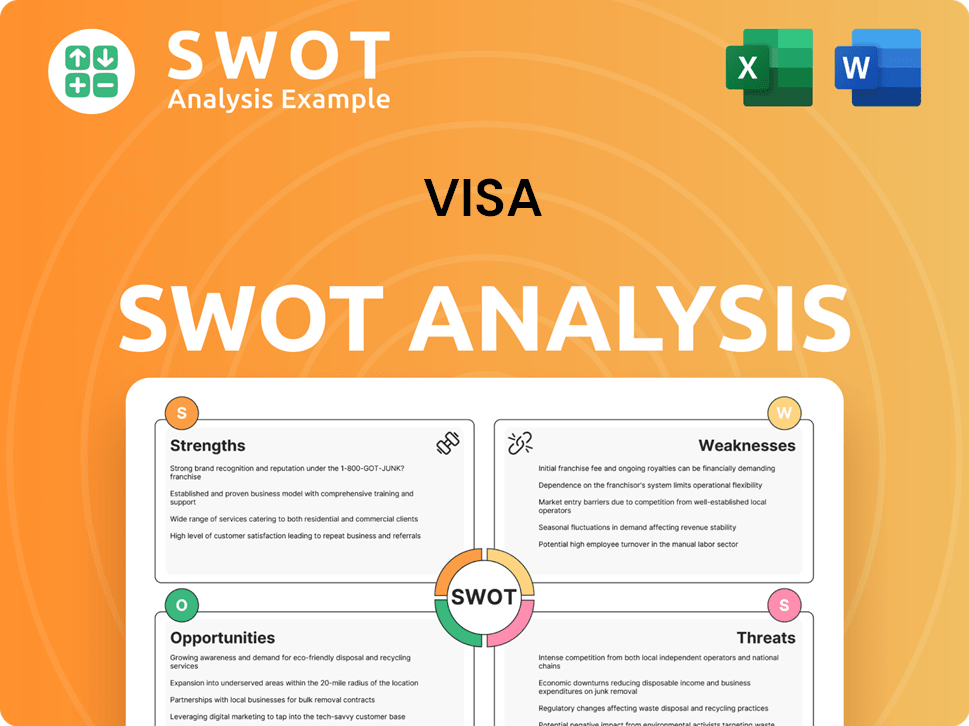

Visa SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of Visa?

The early growth and expansion of the Visa company were marked by significant technological advancements and strategic international moves following the formation of National BankAmericard Inc. (NBI) in 1970. This period was crucial for establishing Visa's footprint in the burgeoning electronic payments sector. Key developments included the launch of the electronic authorization system and the first electronic clearing and settlement system, which provided the necessary scale and security for the industry.

In 1973, Visa launched its electronic authorization system, later known as VisaNet, which was a pivotal moment in its Visa history. This was quickly followed by the introduction of the industry's first electronic clearing and settlement system. These innovations were essential for handling the increasing volume of electronic transactions efficiently and securely, setting the stage for future growth.

The Visa company expanded internationally in 1974, with the establishment of the International Bankcard Company (IBANCO) to manage international programs. This strategic move aimed to unite all international networks under a single global entity. The rebranding of National BankAmericard as Visa U.S.A. and IBANCO as Visa International in 1977, with the name conceived by Dee Hock, signified universal acceptance.

To attract a broader customer base, Visa diversified its product line to include credit, debit, prepaid, and commercial cards. This strategy helped Visa penetrate different market segments and increase its user base. By expanding its offerings, Visa aimed to cater to a wider range of financial needs and preferences.

Global transaction volume exceeded $1 trillion for the first time in 1990, demonstrating significant financial growth. The company maintained a strong annual growth rate throughout the 2000s, with consistent revenue increases. This growth was supported by strategic partnerships and increased user numbers, solidifying Visa's position in the global payments industry. For more insights, check out the Marketing Strategy of Visa.

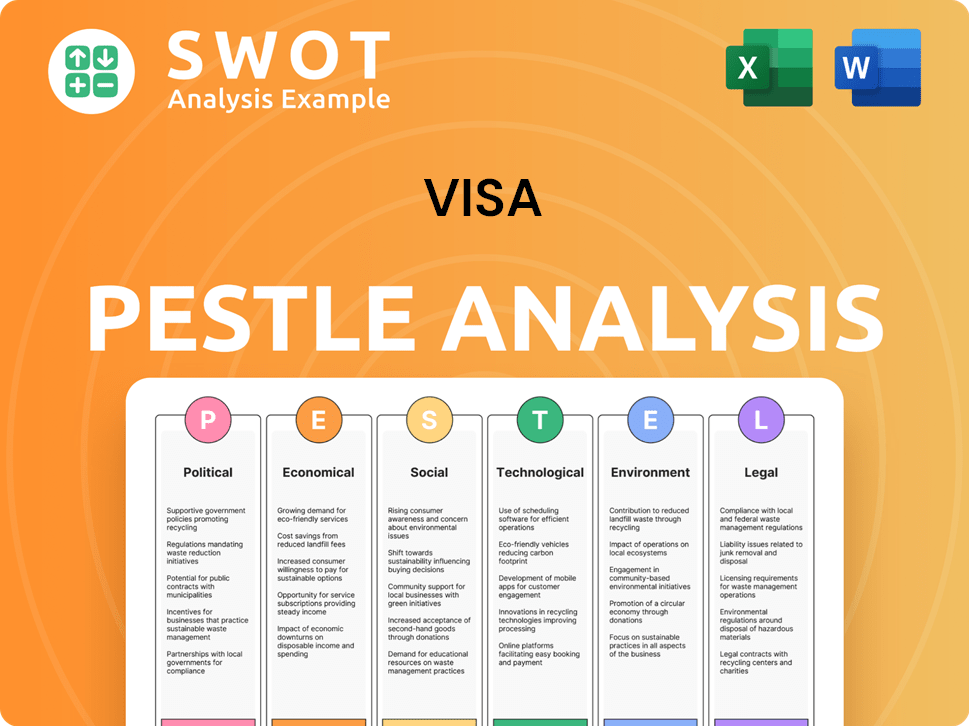

Visa PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in Visa history?

The Visa history is marked by several pivotal moments that have shaped its trajectory from a regional payment system to a global financial powerhouse. From its early days to its current status, the Visa company has consistently adapted and expanded its services to meet the evolving needs of the financial industry. The Visa timeline reflects a commitment to innovation and a strategic vision that has driven its remarkable growth.

| Year | Milestone |

|---|---|

| 1973 | Launched VisaNet, the world's first electronic authorization, clearing, and settlement system, revolutionizing transaction processing. |

| 1975 | Introduced the first debit card, expanding its product offerings and revenue streams. |

| 1976-1977 | Rebranded from BankAmericard to Visa, signaling its global ambitions and commitment to universal acceptance. |

| 2007 | Merged regional businesses worldwide to form Visa Inc., streamlining operations and enhancing global reach. |

| March 18, 2008 | Completed one of the largest initial public offerings (IPOs) in U.S. history, raising $17.9 billion and accelerating global expansion. |

| 2016 | Acquired Visa Europe Ltd., consolidating its operations into a truly global company. |

| January 2024 | Acquired Pismo, a global cloud-native issuer processing and core banking platform, to enhance technological capabilities. |

Visa's evolution has been fueled by continuous innovation in payment technologies and security measures. The company has consistently invested in cutting-edge solutions, including blockchain, artificial intelligence (AI), and cybersecurity, to enhance the security and efficiency of its network. These innovations are critical in combating fraud and adapting to the ever-changing landscape of digital payments.

VisaNet

VisaNet, launched in 1973, was a groundbreaking innovation, being the first electronic authorization, clearing, and settlement system. This system drastically improved transaction speed and efficiency, setting a new standard in the payment industry.

Debit Card Introduction

The introduction of the first debit card in 1975 was a strategic move that expanded Visa's product offerings. This innovation provided consumers with a new way to manage their finances and contributed significantly to Visa's revenue streams.

Rebranding to Visa

The rebranding from BankAmericard to Visa in 1976-1977 was a pivotal moment. This change signaled Visa's global aspirations and commitment to universal acceptance, laying the groundwork for its international expansion.

Technological Investments

Visa consistently invests in advanced technologies like blockchain, AI, and cybersecurity. These investments enhance network security and efficiency, helping to combat fraud and adapt to the evolving digital landscape.

Acquisition of Pismo

The acquisition of Pismo in January 2024, a cloud-native issuer processing platform, is a strategic move. This acquisition strengthens Visa's technological capabilities and supports its ability to offer innovative financial solutions.

AI-Driven Fraud Detection

Visa leverages AI to enhance fraud detection and prevention. This includes using machine learning to identify and mitigate fraudulent activities in real-time, protecting both consumers and merchants.

Despite its successes, Visa has faced several challenges, including intense competition and regulatory scrutiny. The financial services industry is highly competitive, with major players like Mastercard and American Express constantly vying for market share. Furthermore, fintech startups pose new competitive threats, requiring Visa to continually innovate and adapt its strategies. For more insights into the company's structure, you can read about the Owners & Shareholders of Visa.

Market Competition

Visa faces stiff competition from established players like Mastercard and American Express. This competition drives the need for constant innovation and strategic initiatives to maintain market share and profitability.

Fintech Disruption

Fintech startups are emerging as significant competitors, introducing new payment methods and technologies. These companies challenge Visa to adapt and innovate to remain relevant in the evolving financial landscape.

Regulatory Scrutiny

Visa has faced regulatory scrutiny regarding interchange fees and anti-competitive behavior. Addressing these concerns requires transparency and continuous improvement in compliance programs.

Cybersecurity Threats

The rise of cybercrime and sophisticated fraud attempts pose a constant challenge. Visa invests heavily in cybersecurity measures and fraud detection technologies to protect its network and users.

Economic Downturns

Economic downturns can impact consumer spending and transaction volumes. Visa must navigate these periods by adjusting its strategies and maintaining financial stability.

Geopolitical Risks

Geopolitical events can disrupt operations and impact market access. Visa's suspension of business in Russia in March 2022 demonstrates the impact of such risks.

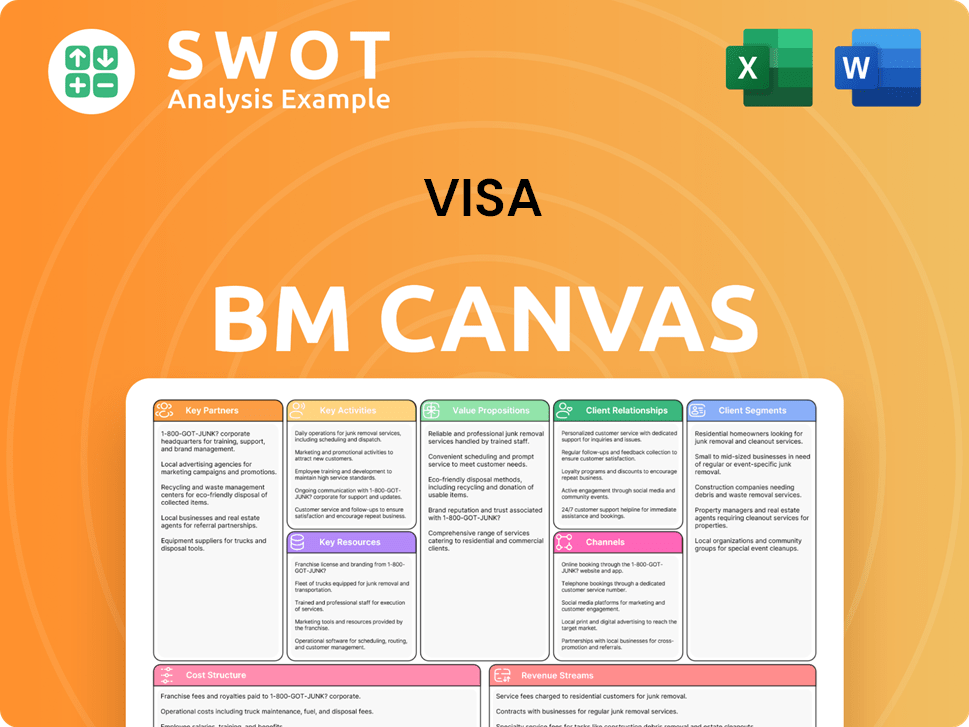

Visa Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for Visa?

The Visa company has a rich Visa history, marked by significant milestones. The Visa timeline shows its evolution from a credit card program to a global payment network. Here's a look at key moments in the company's journey.

| Year | Key Event |

|---|---|

| 1958 | Bank of America launched BankAmericard in California, the initial step in consumer credit cards. |

| 1966 | Bank of America started licensing the BankAmericard program to other financial institutions. |

| 1970 | Bank of America transitioned control of BankAmericard to a cooperative of issuer banks, leading to the formation of National BankAmericard Inc. (NBI). |

| 1973 | NBI introduced the precursor to VisaNet, an electronic authorization system, followed by the first electronic clearing and settlement system in the industry. |

| 1974 | International expansion of the payment network began. |

| 1975 | The first debit card was introduced by Visa. |

| 1976-1977 | BankAmericard was renamed Visa, reflecting a vision of universal acceptance. |

| 1990 | Visa's global transaction volume exceeded $1 trillion. |

| 2007 | Regional businesses worldwide merged to form Visa Inc. |

| 2008 | Visa Inc. went public in one of the largest IPOs in U.S. history, raising $17.9 billion. |

| 2016 | Visa acquired Visa Europe Ltd., becoming a truly global company. |

| 2020 | A program was established to help the Asia-Pacific region bolster its financial infrastructure by partnering with startups. |

| 2022 | All business operations in Russia were suspended. |

| 2024 | Fiscal full-year net revenue of $35.9 billion was reported, with 233.8 billion transactions processed. |

| January 2024 | The acquisition of Pismo, a global cloud-native issuer processing and core banking platform, was completed. |

| April 2025 | A $30 billion share buyback program was announced. |

Visa anticipates significant growth by converting approximately $18 trillion in consumer spending from cash and checks to digital payments. This shift is a major driver for the company's future expansion.

Key strategic initiatives for 2025 and beyond include international expansion, particularly in emerging markets, and further investments in digital technologies. This involves enhancing e-commerce platforms and developing new mobile payment solutions.

The payments landscape in 2025 is expected to be shaped by cardless transactions, real-time payments (RTPs), and account-to-account (A2A) transfers. Open banking payments and local consumer wallets will also gain prominence.

Generative AI (genAI) will play a crucial role in personalizing payment experiences and enhancing fraud detection. Visa is focused on implementing robust AI strategies. Cross-border money transfers and digital identity solutions are also central to Visa's future. For more information, see the Competitors Landscape of Visa.

Visa Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of Visa Company?

- What is Growth Strategy and Future Prospects of Visa Company?

- How Does Visa Company Work?

- What is Sales and Marketing Strategy of Visa Company?

- What is Brief History of Visa Company?

- Who Owns Visa Company?

- What is Customer Demographics and Target Market of Visa Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.