Bank of Baroda Bundle

Can Bank of Baroda Sustain Its Growth Trajectory?

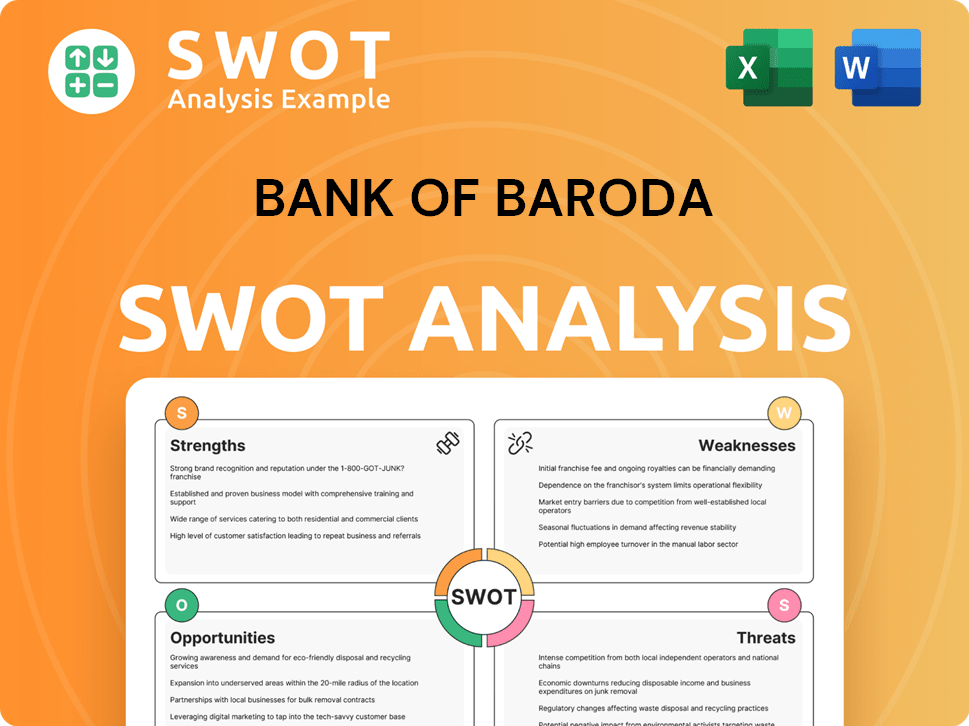

The Indian banking sector is constantly evolving, and Bank of Baroda (BOB) stands as a key player navigating this dynamic environment. Founded in 1908, BOB has a rich history and a significant presence in the Indian financial landscape. This analysis explores the Bank of Baroda SWOT Analysis to understand its strategic initiatives and future prospects.

Bank of Baroda's journey reflects India's economic progress, with its growth strategy intricately linked to the nation's financial performance. Examining BOB company analysis reveals its adaptability and commitment to innovation, crucial for maintaining its market share. This exploration will delve into BOB's expansion plans, digital transformation strategy, and how it aims to overcome challenges in the competitive banking sector India.

How Is Bank of Baroda Expanding Its Reach?

Bank of Baroda (BOB) is actively pursuing a robust expansion strategy to enhance its market presence and diversify its revenue streams. This strategy focuses on several key areas, including retail loan portfolio growth, expansion in rural and semi-urban areas, and strengthening international operations. These initiatives are designed to capitalize on emerging opportunities and maintain a competitive edge within the banking sector in India.

A core element of Bank of Baroda's growth strategy involves significant investment in digital products and services. The bank is leveraging technology to reach a wider customer base and improve operational efficiency. This includes enhancements to mobile banking applications and online loan platforms, reflecting a broader trend of digital transformation within the financial sector.

Moreover, Bank of Baroda is exploring innovative business models, such as co-lending partnerships, to extend its credit outreach. This approach aims to serve underserved segments and optimize lending processes, contributing to the bank's overall financial performance. The bank's strong capital position further supports these expansion plans.

Bank of Baroda aims for a year-on-year growth of 12-14% in its retail loan portfolio for FY25. This expansion will primarily focus on high-growth segments such as personal loans, auto loans, and home loans. This strategic focus is expected to drive significant growth in the bank's overall lending business.

The bank is concentrating on enhancing its presence in rural and semi-urban areas. This involves leveraging its extensive branch network and introducing tailored financial products. This strategy is designed to tap into the growth potential within these underserved markets, boosting BOB market share.

Bank of Baroda is looking to strengthen its international operations, particularly in regions with a significant Indian diaspora and growing trade ties. This will enable the bank to capitalize on cross-border business opportunities and diversify its revenue streams. This is a key aspect of BOB's strategic initiatives 2024.

The bank is aggressively promoting its digital products, including mobile banking applications and online loan platforms. This push aims to reach a wider, tech-savvy customer base and improve customer engagement. This is a crucial part of Bank of Baroda's digital transformation strategy.

Strategic Partnerships and Capital Strength

Bank of Baroda is exploring new business models, such as co-lending partnerships with NBFCs, to expand its credit outreach. This approach allows the bank to reach underserved segments and optimize lending processes. The bank's Capital Adequacy Ratio (CRAR) stood at 16.31% as of December 2023, providing a strong foundation for these expansion initiatives.

- Co-lending partnerships to expand credit reach.

- Focus on underserved segments.

- Optimized lending processes.

- Strong CRAR to support growth.

Bank of Baroda SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Bank of Baroda Invest in Innovation?

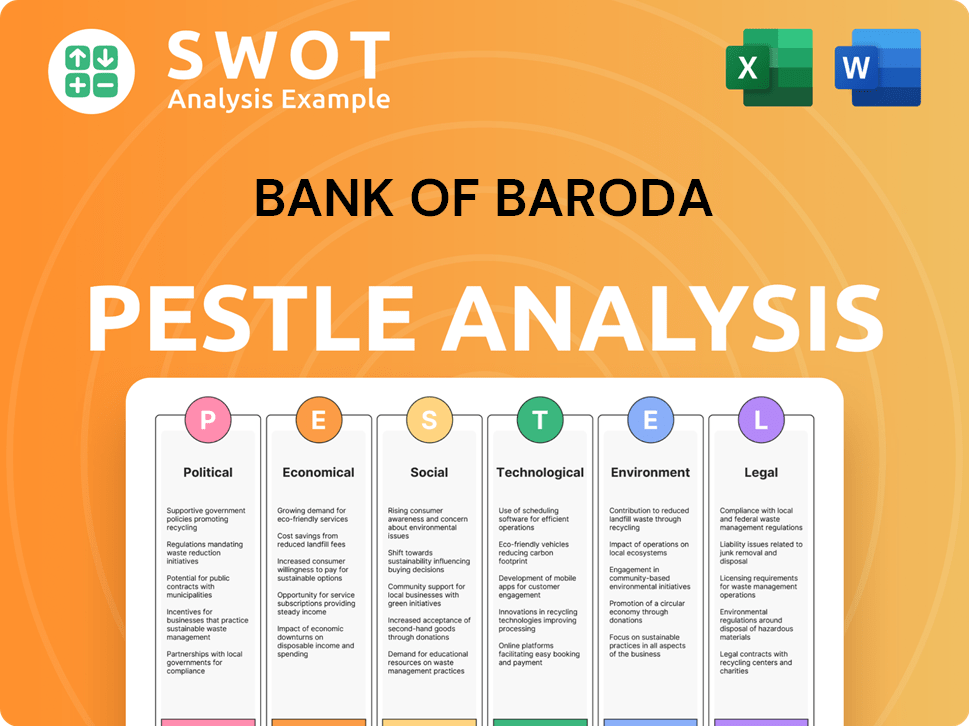

The Brief History of Bank of Baroda reveals a strong commitment to innovation and technology as key drivers for sustained growth and enhanced customer experience. This approach is central to the bank's strategic initiatives, positioning it to meet evolving customer needs in the dynamic Indian banking sector. The bank's focus on digital transformation, automation, and cutting-edge technologies underscores its dedication to staying competitive and relevant in the financial landscape.

The bank is actively investing in digital transformation, with a strong emphasis on automation and the adoption of cutting-edge technologies. A significant part of its strategy involves leveraging Artificial Intelligence (AI) and Machine Learning (ML) for data analytics, fraud detection, and personalized product offerings. This data-driven approach aims to improve operational efficiency and tailor services to individual customer needs. The bank is also exploring blockchain technology for secure and transparent transactions, although specific implementations are still in nascent stages.

The bank's digital initiatives include the revamp of its mobile banking application, 'bob World', to offer a seamless and comprehensive digital banking experience. This platform integrates various services, from account management and payments to loan applications and investment options. Bank of Baroda is also focused on enhancing its cybersecurity infrastructure to protect customer data and ensure secure digital transactions. Their commitment to innovation is further demonstrated by their efforts to digitize internal processes, aiming for a paperless and more efficient operational environment.

Digital Transformation Investments

The bank is making substantial investments in digital technologies to enhance its services. This includes upgrading core banking systems and implementing new digital platforms.

AI and ML Integration

AI and ML are being integrated for data analytics to improve decision-making. These technologies are also used for fraud detection and personalized customer offerings.

Mobile Banking Enhancement

The 'bob World' app is being enhanced to offer a comprehensive digital banking experience. This includes a wide range of services, from account management to investment options.

Cybersecurity Focus

Significant efforts are being made to enhance cybersecurity infrastructure. This is crucial for protecting customer data and ensuring secure digital transactions.

Blockchain Exploration

The bank is exploring the potential of blockchain technology for secure and transparent transactions. This is part of its broader innovation strategy.

Process Digitization

Internal processes are being digitized to create a paperless and more efficient operational environment. This improves overall operational efficiency.

Key Technology Initiatives and Their Impact

The implementation of these technologies has a direct impact on the bank's financial performance and market position. The focus on digital transformation is designed to improve customer satisfaction, operational efficiency, and overall profitability. These initiatives are also expected to contribute to the bank's competitive advantage in the banking sector in India.

- AI-driven Analytics: Enhances risk management and customer service.

- Mobile Banking: Increases customer engagement and transaction volumes.

- Cybersecurity Upgrades: Protects customer assets and maintains trust.

- Blockchain Pilots: Streamlines transaction processes and reduces costs.

Bank of Baroda PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Bank of Baroda’s Growth Forecast?

The financial outlook for Bank of Baroda (BOB) appears promising, with several indicators pointing towards sustained growth. The Bank of Baroda growth strategy seems to be yielding positive results, as evidenced by recent financial performance. This positive trend suggests a robust financial future for the bank, supported by strategic initiatives and a focus on key growth areas.

For the third quarter of fiscal year 2024, BOB demonstrated strong financial performance. The bank's net profit surged by 16% year-on-year, reaching ₹4,579 crore. This significant increase underscores the effectiveness of the bank's strategies and its ability to capitalize on market opportunities. The positive financial results reflect the bank's commitment to enhancing its financial performance and expanding its market presence.

Analysts generally hold a positive view on Bank of Baroda's future performance, citing its strong asset quality and improving profitability. The bank's strategic focus on retail credit and digital banking is expected to further bolster its revenue streams and profitability in the coming years, contributing to the overall BOB market share.

BOB's net interest income experienced a substantial increase, rising by 26.7% to ₹11,101 crore. This growth highlights the bank's ability to effectively manage its interest-earning assets and liabilities. This rise in net interest income reflects the bank's success in optimizing its financial strategies and improving its overall profitability.

The bank aims for a credit growth of 13-14% for the full fiscal year 2024. This target indicates the bank's confidence in its ability to expand its lending activities and support economic growth. Achieving this growth rate will be crucial for sustaining the bank's positive financial trajectory.

The gross non-performing assets (GNPA) ratio decreased to 2.92% in Q3 FY24, down from 3.01% in Q2 FY24. This improvement demonstrates the bank's effective risk management practices and its ability to recover or resolve stressed assets. The decline in GNPA reflects the bank's efforts to maintain a healthy balance sheet.

Net non-performing assets (NNPA) also improved, reaching 0.67% in Q3 FY24, compared to 0.73% in the previous quarter. This reduction in NNPA further strengthens the bank's financial position. The improvement in asset quality contributes to better financial stability and investor confidence.

BOB's commitment to digital transformation and customer-centric strategies is expected to drive future growth. The bank's focus on technology and innovation, as detailed in Revenue Streams & Business Model of Bank of Baroda, is likely to enhance its competitive advantage and operational efficiency. These initiatives are designed to improve customer experience and streamline banking processes.

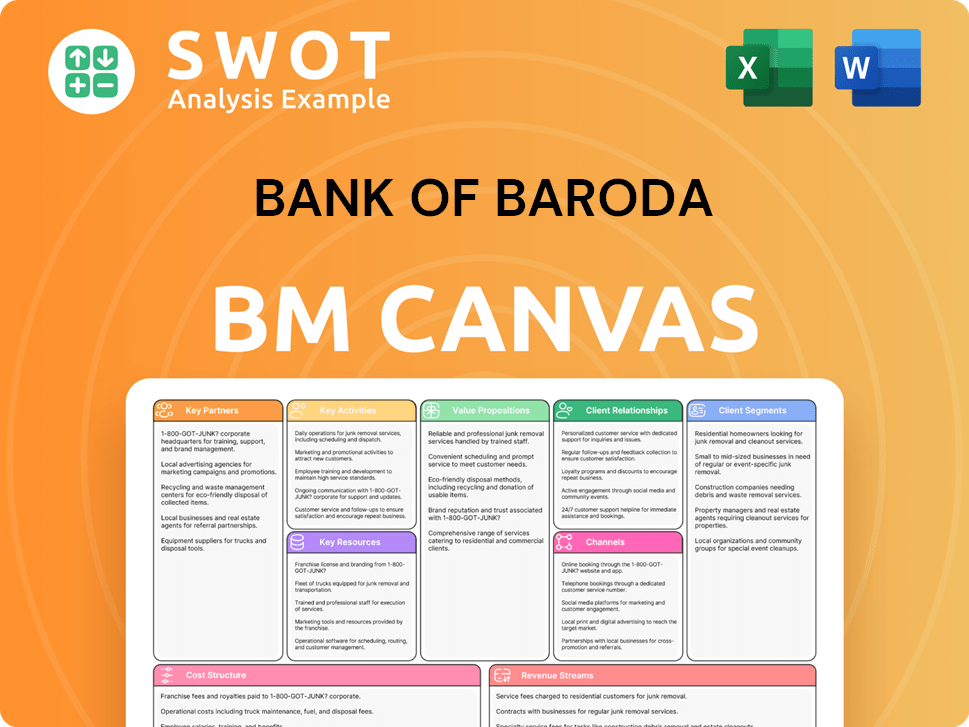

Bank of Baroda Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Bank of Baroda’s Growth?

The growth strategy of Bank of Baroda (BOB) faces several potential risks and obstacles. These challenges span market competition, regulatory changes, economic downturns, and technological disruptions. Understanding these risks is crucial for evaluating Bank of Baroda's future prospects and its ability to sustain growth in the evolving banking sector in India.

Market competition, intense regulatory changes, and economic fluctuations can significantly influence Bank of Baroda's performance. The bank must navigate these risks effectively to maintain its financial health and competitive edge. Addressing these challenges is essential for the bank's strategic initiatives and long-term success.

Bank of Baroda's future prospects depend on its ability to mitigate these risks. The bank's strategic planning must account for these factors to ensure sustainable growth and maintain its market share. This proactive approach will be critical for BOB's financial performance and overall impact on the Indian economy.

Market Competition

Intense competition from both public and private sector banks, as well as fintech companies, puts pressure on interest margins and customer acquisition costs. The Banking sector in India is highly competitive, requiring constant innovation and strategic adjustments to maintain market share. BOB must differentiate itself through superior customer service and innovative products.

Regulatory Changes

Evolving banking regulations, including those related to capital adequacy and digital banking, can impact the bank's operational flexibility and profitability. Stricter provisioning norms and new data privacy regulations necessitate significant investments in compliance. These changes require BOB to adapt quickly to maintain compliance and operational efficiency.

Economic Downturns

Economic downturns or sector-specific stresses can lead to an increase in non-performing assets (NPAs), impacting asset quality and profitability. Global economic uncertainties and domestic inflationary pressures can pose renewed challenges. Managing NPAs is crucial for maintaining a healthy balance sheet and ensuring long-term financial stability.

Technological Disruption

The rapid pace of technological disruption from agile fintech players presents an ongoing threat. BOB must continuously invest in and adapt to new technologies to avoid being outmaneuvered. This includes investing in digital infrastructure and enhancing cybersecurity measures. BOB's digital transformation strategy must be robust.

Internal Operational Hurdles

Managing a large workforce and ensuring efficient digital transformation across its extensive network can present operational hurdles. This includes training employees, upgrading systems, and streamlining processes. Efficiently managing internal operations is key to maintaining a competitive edge.

Geopolitical and Macroeconomic Instability

External factors such as geopolitical events and macroeconomic instability can impact the bank's financial performance. These factors can lead to market volatility, affecting investment portfolios and the overall economic climate. Proactive risk management and diversification strategies are necessary to mitigate these external influences.

Bank of Baroda addresses these risks through robust risk management frameworks, diversification of its loan portfolio, and continuous monitoring of market and regulatory landscapes. The bank's approach includes stringent credit appraisal processes and proactive monitoring of asset quality. These measures are crucial for maintaining financial stability and ensuring sustainable growth. BOB's approach to risk management is detailed in our analysis of Bank of Baroda's growth strategy.

BOB continues to focus on strategic initiatives to strengthen its position in the market. This includes investing in technology, expanding its digital offerings, and improving customer service. These initiatives are designed to enhance operational efficiency and improve the overall customer experience. BOB's BOB's investment in technology is significant.

Bank of Baroda Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Bank of Baroda Company?

- What is Competitive Landscape of Bank of Baroda Company?

- How Does Bank of Baroda Company Work?

- What is Sales and Marketing Strategy of Bank of Baroda Company?

- What is Brief History of Bank of Baroda Company?

- Who Owns Bank of Baroda Company?

- What is Customer Demographics and Target Market of Bank of Baroda Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.