Vanquis Banking Group Bundle

Can Vanquis Banking Group Navigate the Financial Landscape?

Vanquis Banking Group, a specialist bank focused on the UK and Ireland, offers crucial financial services to a customer base often underserved by traditional lenders. Formerly known as Provident Financial plc, the company rebranded in early 2023, marking a strategic shift towards its core banking operations. This transformation has been essential as the group redevelops its customer offerings and adjusts its pricing strategies.

Despite reporting a statutory loss in 2024, primarily due to one-off expenses, Vanquis Banking Group demonstrated resilience by exceeding its cost-saving targets. The group’s strategic delivery is on track, returning to profitability and growing gross customer interest-earning balances in Q1 2025. To gain a deeper understanding of its operations, explore Vanquis Banking Group SWOT Analysis and how this specialist bank, including its Vanquis Bank credit card and Vanquis credit card, generates revenue and aims for sustainable growth in a competitive market.

What Are the Key Operations Driving Vanquis Banking Group’s Success?

The core operations of Vanquis Banking Group revolve around providing financial products to underserved customers. They offer credit cards, loans, and savings accounts under various brands, including Vanquis and Moneybarn. Their value proposition centers on helping individuals build or rebuild their credit profiles, which sets them apart in the financial market.

The group's strategic focus includes robust underwriting processes, customer service, and digital platforms. They are actively investing in technology, with the 'Gateway' program aiming to create a scalable, digital-first platform. This initiative is expected to deliver significant cost efficiencies, demonstrating a commitment to operational excellence and customer experience.

The group has transitioned to a traditional bank model, relying on retail deposits, securitization, and liquidity facilities. This diversified funding base supports its operations and growth strategy. This approach, along with its focus on a specific customer segment, defines its unique position compared to its competitors. To gain a better understanding of the competitive environment, consider exploring the Competitors Landscape of Vanquis Banking Group.

Vanquis Banking Group offers credit cards and loans designed for individuals who may have difficulty accessing mainstream financial services. These products aim to help customers improve their credit scores. The group also provides secured vehicle finance through Moneybarn.

The 'Gateway' program is a key initiative, scheduled for completion by mid-2026, designed to enhance digital capabilities. This program aims to provide a scalable, digital-first platform to support growth and deliver an additional £23-28 million in cost efficiencies. The development of a new Vanquis mobile app is planned for implementation in Q2 2025.

Vanquis Banking Group is enhancing its customer service capabilities through AI and digital tools. AI-automated complaint logging has significantly reduced unprocessed complaints. By the end of 2024, the number of unprocessed complaints was reduced to 5,600, down from 14,400 in December 2023.

The group's funding model is based on retail deposits, securitization, and liquidity facilities. This diversified approach supports its lending activities. This transition to a traditional bank model supports sustainable growth and financial stability.

Key Operational Highlights

The group's operations are underpinned by a focus on underserved customers, technology enhancements, and a diversified funding model. These elements contribute to the group's ability to serve its target market effectively.

- Credit cards and loans for credit-challenged customers.

- The 'Gateway' technology program for digital transformation.

- AI-driven improvements in customer service and complaint handling.

- A funding model based on retail deposits and securitization.

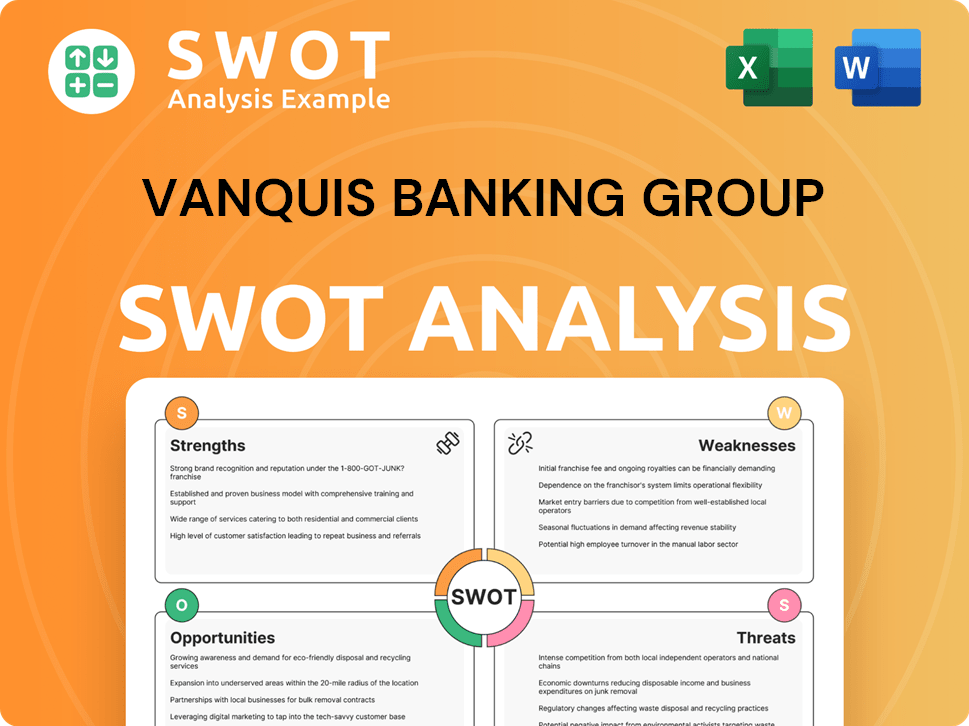

Vanquis Banking Group SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Vanquis Banking Group Make Money?

The primary revenue streams for Vanquis Banking Group stem from its lending activities, with a significant portion generated by the Credit Cards segment. The company's financial performance in 2024 reflects strategic adjustments and market dynamics. Understanding these revenue sources and monetization strategies is crucial for assessing the company's financial health and future prospects.

Vanquis Banking Group's main sources of income include interest earned from credit cards, personal loans, and vehicle finance. Despite facing economic challenges, the company has implemented initiatives to optimize revenue. These efforts, combined with strategic product offerings, aim to enhance profitability and maintain a competitive edge in the financial services market.

In 2024, the total income for Vanquis Banking Group decreased by 6.2% to £458.5 million from £488.8 million the previous year. Net interest income also fell by 5.1% to £420.0 million from £442.6 million. However, interest income increased by 2% to £565.4 million, driven by repricing initiatives in Credit Cards and Vehicle Finance, and increased Liquid Asset Buffer income.

Monetization Strategies

Vanquis Banking Group employs several strategies to generate revenue and maximize profitability. These strategies focus on customer acquisition, product innovation, and efficient financial management. The company's approach includes offering tailored credit products and optimizing existing offerings.

- Offering tailored credit products with varying APRs and credit limits to its target customer base.

- Launching balance transfer products to attract new customers and retain existing ones.

- Re-launching existing customer propositions with a strong risk-adjusted margin.

- Exploring opportunities for further revenue optimization in Credit Cards.

In Q1 2025, gross customer interest-earning balances grew by 0.2% to £2,313 million, or 2.4% excluding a personal loan portfolio sale. Second Charge Mortgage balances continued to grow, reaching nearly £300 million by the end of Q1 2025. For more detailed insights into the company's growth strategy, you can read about the Growth Strategy of Vanquis Banking Group.

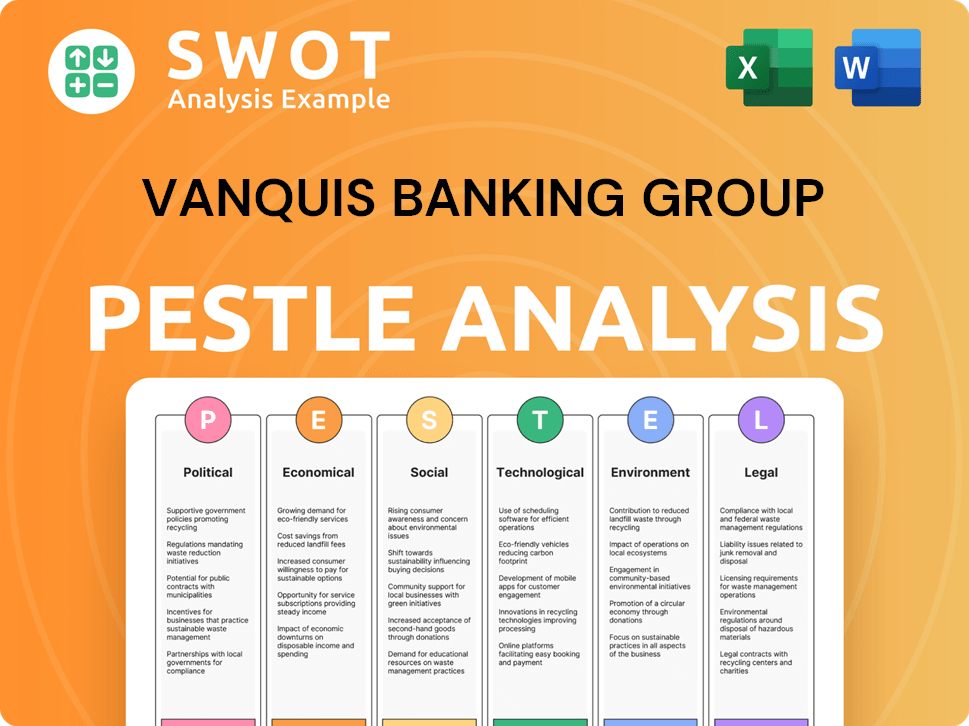

Vanquis Banking Group PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Vanquis Banking Group’s Business Model?

The year 2024 was a crucial period for Vanquis Banking Group, marked by significant efforts to reposition the company for sustainable growth. This involved a comprehensive review of its financial position, leading to adjustments in historical balances and a clearer understanding of its financial health. The company also focused on addressing underlying structural issues, simplifying its operational model, and expanding its product offerings to better serve its customer base.

A key strategic move was the comprehensive review of its balance sheet, which led to a revaluation of historical balances and a clearer financial position. This included a £28.9 million loss from a detailed Vehicle Finance receivables review in the first half of 2024. The group also addressed underlying structural issues, simplified its operating model, refreshed its strategy, and expanded its product range.

Despite these strategic initiatives, the company faced operational challenges, including a widening of its pretax loss to £136.3 million in 2024. This was significantly impacted by the Vehicle Finance Stage 3 receivables review and a £71.2 million goodwill write-off related to Moneybarn. Despite these challenges, Vanquis Banking Group continues to adapt and innovate to maintain its position in the market.

Vanquis Banking Group's turnaround in 2024 highlighted significant progress in its repositioning efforts. The company focused on reviewing its balance sheet and addressing structural issues. This included a revaluation of historical balances to provide a clearer financial picture.

The company undertook a comprehensive review of its balance sheet. It also simplified its operating model and refreshed its strategy. These strategic moves were aimed at improving the company's financial position and operational efficiency.

Vanquis Banking Group focuses on the financially underserved market, a niche where mainstream lenders are less active. The company's technology transformation program, 'Gateway,' aims to enhance efficiency. These initiatives reinforce its business model and competitive edge.

The company reported a pretax loss of £136.3 million in 2024, impacted by specific financial reviews. Complaint costs increased by 66% to £47.4 million. The group achieved substantial cost savings, exceeding £64 million by the end of 2024.

Operational Challenges and Strategic Responses

Vanquis Banking Group faced increased complaint costs, rising by 66% to £47.4 million in 2024, primarily due to unmerited claims. The company implemented AI-automated complaint logging to manage the backlog and reduce processing fees. These measures are part of a broader effort to improve operational efficiency and customer service.

- The company experienced a significant widening of its pretax loss to £136.3 million in 2024.

- Complaint costs rose by 66% to £47.4 million, mainly due to an increase in unmerited claims.

- The group implemented AI-automated complaint logging to manage the backlog and reduce processing fees.

- Vanquis Banking Group achieved cost savings exceeding £64 million by the end of 2024.

Vanquis's competitive advantage lies in its specialized focus on the financially underserved market, a segment where mainstream lenders are less active. The company's technology transformation program, 'Gateway,' is designed to enhance efficiency and scalability, providing a digital-first platform. The group has also achieved substantial cost savings, exceeding £64 million by the end of 2024, with further savings targeted for 2025. For more insights into the overall approach, consider reading about the Marketing Strategy of Vanquis Banking Group.

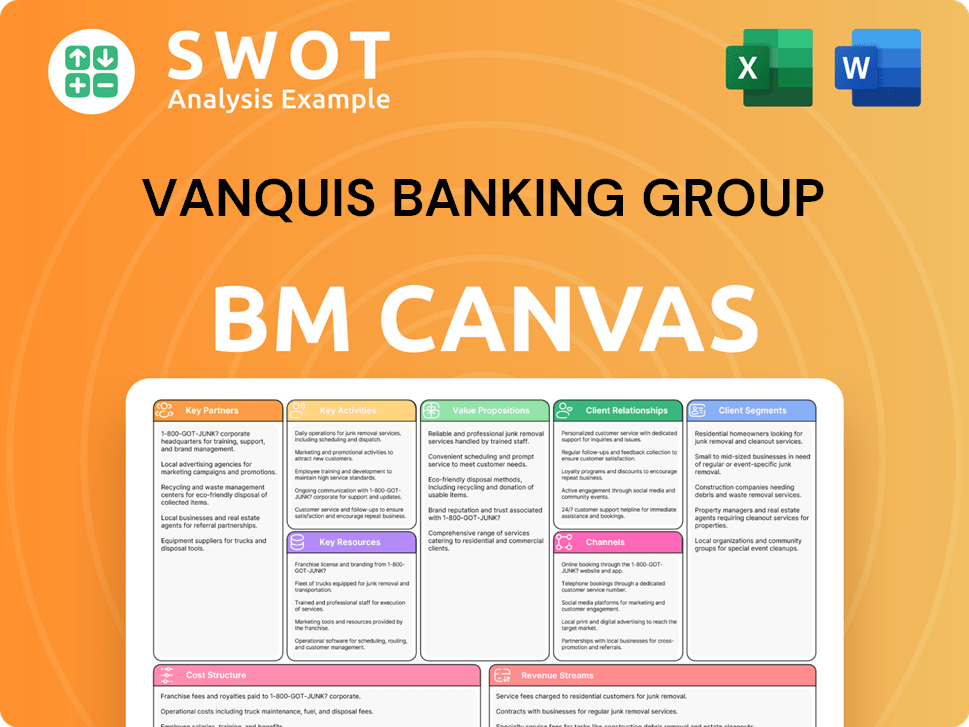

Vanquis Banking Group Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Vanquis Banking Group Positioning Itself for Continued Success?

The Vanquis Banking Group holds a unique position as the largest specialist finance provider for financially underserved customers in the UK. Despite a 4% decline in gross customer interest-earning balances in 2024, balances increased by 2% in Q4 2024 and continued to grow in January and February 2025, returning to profitability in Q1 2025. The group's retail funding rose to 92.1% in 2024, reinforcing its strong liquidity position.

Key risks include ongoing regulatory changes, particularly concerning motor finance commission disclosures. Elevated complaint costs, largely driven by unmerited claims from Claims Management Companies, also pose a challenge. Looking ahead, the company is focused on delivering a low single-digit Return on Tangible Equity (ROTE) in 2025, with a target of mid-teens ROTE by 2027 and double-digit ROTE in 2026.

The Vanquis Banking Group specializes in serving financially underserved customers in the UK. It is a significant player in the specialist finance market, focusing on credit cards, loans, and other financial products. The group's ability to return to profitability in Q1 2025 after a challenging period highlights its resilience and strategic focus.

The company faces risks from regulatory changes, particularly concerning motor finance commission disclosures. Elevated complaint costs, often driven by unmerited claims, also impact profitability. The group is actively managing these risks through engagement with regulators and legal action to protect its financial performance. Read more about the company's history in the Brief History of Vanquis Banking Group.

The group aims for a low single-digit ROTE in 2025, increasing to mid-teens by 2027 and double-digit in 2026. Strategic initiatives include refining customer propositions and growing customer engagement. A key focus is on growth in Second Charge Mortgages and Credit Cards. The 'Gateway' technology program is expected to deliver £23-28 million in cost efficiencies by mid-2026.

Retail funding reached 92.1% in 2024, demonstrating a strong liquidity position. The company is focused on sustaining and expanding its ability to generate money through cost reductions, increased income from growing interest-earning balances, and ongoing operational excellence. The company's focus is on sustainable growth and profitability.

Strategic Initiatives

The company is concentrating on several key strategic initiatives to drive future growth and profitability. These include enhancing customer propositions and improving customer experience to increase credit card utilization.

- Refining targeted customer propositions

- Growing customer engagement to drive Credit Card utilization

- Improving customer experience

- Focus on Second Charge Mortgages and Credit Cards growth

- Completion of 'Gateway' technology transformation program

Vanquis Banking Group Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Vanquis Banking Group Company?

- What is Competitive Landscape of Vanquis Banking Group Company?

- What is Growth Strategy and Future Prospects of Vanquis Banking Group Company?

- What is Sales and Marketing Strategy of Vanquis Banking Group Company?

- What is Brief History of Vanquis Banking Group Company?

- Who Owns Vanquis Banking Group Company?

- What is Customer Demographics and Target Market of Vanquis Banking Group Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.