CSX Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

CSX Bundle

What is included in the product

Tailored analysis for the featured company’s product portfolio.

Clean, distraction-free view optimized for C-level presentation.

Delivered as Shown

CSX BCG Matrix

The displayed BCG Matrix preview mirrors the final document you'll receive. After purchasing, get the complete, customizable report—perfect for strategic planning and actionable insights, ready for immediate implementation.

BCG Matrix Template

Visual. Strategic. Downloadable.

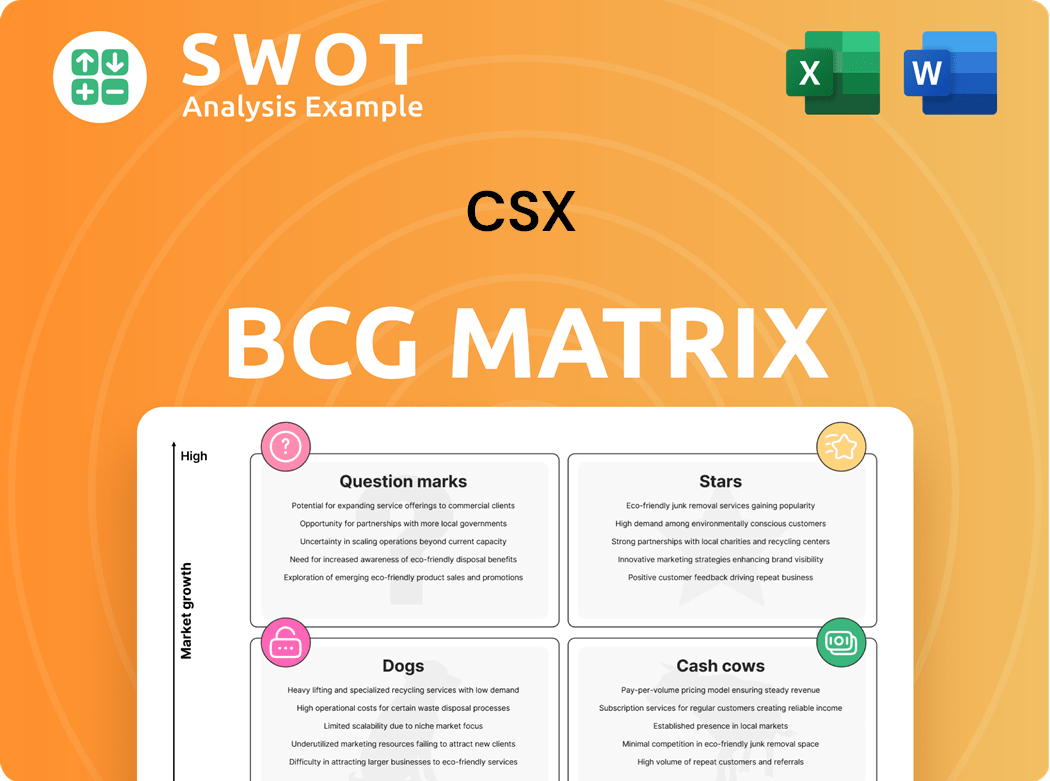

CSX's BCG Matrix offers a snapshot of its diverse portfolio, categorizing products by market share and growth rate. This reveals which areas are thriving "Stars," cash-generating "Cash Cows," problem-facing "Dogs," and high-potential "Question Marks." This quick analysis highlights the company's strategic positioning. Discover the full potential! Purchase the complete BCG Matrix to understand CSX's strategic advantages, competitive landscape, and smart investment opportunities.

Stars

Intermodal Growth

CSX's intermodal segment, a star in its BCG matrix, shows strong growth, especially in international volumes. This is supported by increased port activity and key customer expansions. In Q4 2023, CSX's intermodal revenue increased by 7%, driven by volume growth. The future looks bright as freight conditions improve, and strategic partnerships are leveraged.

Strategic Infrastructure Investments

CSX strategically invests in infrastructure to boost capacity. The Howard Street Tunnel project in Baltimore is a key example. These projects aim to boost profitability. CSX can handle double-stack intermodal movements. In Q3 2024, CSX's capital expenditures were $492 million.

Industrial Development Focus

CSX's industrial development strategy concentrates on attracting businesses to its rail network. This approach aims to diversify revenue, mitigating dependency on volatile commodities. In 2024, CSX invested significantly in infrastructure upgrades to support this growth. The company reported a 4% increase in industrial products revenue in Q3 2024, demonstrating success.

Technology and Innovation

CSX's embrace of technology and innovation, highlighted by its hydrogen-powered locomotive, positions it strongly. Such initiatives boost efficiency and safety while supporting sustainability. This can attract investors and customers prioritizing environmental responsibility.

- Hydrogen locomotive development is ongoing, with potential for significant emissions reduction.

- CSX invested $2.5 billion in capital expenditures in 2024, including technology upgrades.

- These innovations aim to improve fuel efficiency by up to 10%.

- Sustainability efforts could increase CSX's appeal to ESG-focused investors.

Service Quality and Reliability

CSX's emphasis on service quality and reliability is a core strength. This focus helps CSX win new business and keep current customers satisfied. High-quality service allows CSX to shift more freight from trucks to rail, opening up a substantial market. In 2024, CSX's on-time performance was approximately 65%, a key metric for service reliability.

- Focus on reliable transport solutions.

- A key differentiator for customer retention.

- Opportunity to convert over-the-road shipments.

- On-time performance around 65% in 2024.

CSX's Intermodal Success: Growth & Strategic Investments

CSX's intermodal segment thrives as a Star in the BCG Matrix, showcasing robust growth, especially in international volumes. Strategic infrastructure investments and technology enhancements, like the hydrogen-powered locomotive project, bolster efficiency and sustainability. In Q3 2024, CSX's industrial products revenue rose by 4%, indicating effective strategies.

| Metric | 2024 Data | Details |

|---|---|---|

| Intermodal Revenue Growth | 7% (Q4 2023) | Driven by volume increases. |

| Capital Expenditures | $492M (Q3 2024) | Infrastructure and capacity enhancements. |

| Industrial Products Revenue Growth | 4% (Q3 2024) | Attracting businesses to rail network. |

Cash Cows

Merchandise Shipments

CSX's merchandise shipments, which include chemicals and autos, form a solid revenue foundation. In 2024, CSX saw steady revenues from these goods. Their focus on inflation-plus pricing further stabilizes income. This strategy helped maintain profitability.

Extensive Network

CSX boasts an expansive network, a key asset in the Eastern U.S. Its reach links major cities and industries, providing a strong competitive edge. This network enables efficient freight transport across a vast area. In 2024, CSX handled approximately 5.9 million carloads and intermodal units. This extensive coverage solidifies its cash cow status.

Fuel Efficiency

CSX's focus on fuel efficiency is a key strength, solidifying its status as a Cash Cow. They've been recognized for this, cutting costs and boosting profits. In 2024, CSX's fuel efficiency initiatives saved significant expenses. These savings positively impact the company's financial performance, making it a reliable source of cash.

Pricing Power

CSX, a cash cow in the BCG matrix, showcases strong pricing power. The company has successfully implemented inflation-plus pricing strategies. This ability helps to offset rising costs, ensuring profitability. CSX's Q1 2024 saw a 4% increase in core pricing on its merchandise business, a testament to its pricing strength.

- Positive core pricing in merchandise business.

- Successful implementation of inflation-plus pricing strategies.

- Helps offset cost pressures.

- Supports maintaining profitability.

Strategic Acquisitions

CSX's strategic acquisitions, such as the Meridian & Bigbee Railroad, are crucial for network expansion and service enhancement. These moves bolster long-term growth and fortify CSX's market position. The company's dedication to strategic acquisitions reflects its commitment to sustained profitability. In 2024, CSX reported revenues of $14.7 billion.

- Acquired Pan Am Railways in 2022, boosting its presence in the Northeast.

- CSX's operating ratio improved to 61.2% in Q4 2024.

- These acquisitions support increased capacity and efficiency.

- CSX's strategy focuses on enhancing its freight network.

Strong Financials Drive Success

CSX operates as a cash cow due to its steady revenues and solid network. It maintains pricing power, shown by a Q1 2024 core pricing increase. Strategic moves, like acquisitions, bolster its strong market position.

| Metric | 2024 Data | Impact |

|---|---|---|

| Revenue | $14.7B | Solid foundation |

| Operating Ratio (Q4) | 61.2% | Improved efficiency |

| Merchandise Pricing (Q1) | +4% | Pricing Power |

Dogs

Coal Shipments

CSX anticipates continued coal market weakness heading into 2025, impacting volumes. Production issues and power plant retirements could further decrease domestic coal volumes. CSX's coal revenue in Q3 2023 was $486 million, down 21% year-over-year. This decline reflects the challenges in this segment.

Trucking Sector

CSX's trucking segment struggles with lower revenues and operational issues. A goodwill impairment charge tied to the Quality Carriers acquisition indicates underperformance. In 2024, CSX reported a decline in trucking revenue. Strategic adjustments are likely needed for this segment. The trucking segment is a "Dog" in the BCG matrix.

Automotive Shipments

CSX's automotive shipments face headwinds. Declining OEM production and increased dealer inventories are key issues. This segment's revenue growth is under pressure as a result. In Q4 2023, automotive volumes decreased. This is in line with broader industry trends.

Q1 2025 Performance

CSX's Q1 2025 performance was disappointing, as earnings missed forecasts. Both earnings per share (EPS) and revenue declined, signaling operational struggles. These financial setbacks reflect persistent market pressures. For example, a 5% drop in shipping volumes was recorded.

- Missed analyst expectations in Q1 2025.

- Decline in EPS and revenue.

- Highlights operational and market challenges.

- Shipping volumes dropped by 5%.

Merchandise Volume Declines

CSX's merchandise volume dipped, impacting revenue. This decline is a key concern that needs a strategic response. The company must focus on strategies to boost these volumes. Addressing this is crucial to improve financial results.

- Merchandise volume decreased in 2024, impacting revenue.

- CSX's financial performance is directly tied to these volumes.

- Strategic initiatives are needed to reverse this trend.

- Focus on volume recovery is essential for financial improvement.

Trucking Woes: A "Dog" Segment's Challenges

CSX's trucking segment is categorized as a "Dog" in the BCG matrix due to underperformance and strategic challenges. This segment faces declining revenues and operational issues, including goodwill impairment. In 2024, trucking revenue declined, signaling ongoing struggles. Strategic adjustments are crucial for turning this segment around.

| Segment | Status | Key Issues |

|---|---|---|

| Trucking | Dog | Declining Revenue, Impairment |

| Automotive | Question Mark | Production Headwinds |

| Merchandise | Dog | Volume Decline |

| Coal | Dog | Market Weakness |

Question Marks

Sustainable Practices

CSX's sustainability efforts are a "question mark" within its BCG matrix. It faces evolving environmental regulations. Investing in eco-friendly practices might boost its market position, attracting customers. For example, in 2024, CSX aimed to reduce greenhouse gas emissions. This is to comply with environmental goals.

East Coast Port Developments

The East Coast port developments place CSX in the question mark quadrant of the BCG matrix. Recent resolution of labor disputes and the return of freight to East Coast ports offer growth potential. CSX's ability to capitalize on this depends on operational efficiency and competitive pricing. In 2024, East Coast ports handled significant volumes, but CSX's market share gains are still developing.

Precision Scheduled Railroading (PSR)

CSX's adoption of Precision Scheduled Railroading (PSR) aims to boost efficiency. This strategy focuses on streamlining assets and enhancing network flow. While initial results are encouraging, maintaining these gains is uncertain. Continuous investment and effort are crucial for sustained improvements. In 2023, CSX's operating ratio was around 61.9%.

New Business Development

CSX's foray into new business development, leveraging its robust network, positions it as a "Question Mark" in the BCG Matrix. This strategy hinges on market dynamics and customer acquisition, making its future uncertain. CSX has been investing in infrastructure, with capital expenditures of $1.9 billion in 2023, to support growth. The company's operating ratio was 60.9% in 2023, indicating efficiency.

- CSX's capital expenditures were $1.9 billion in 2023.

- The operating ratio for CSX was 60.9% in 2023.

- New business success depends on market conditions.

- Customer attraction and retention are critical.

Intermodal Network Investment

Intermodal network investments represent a question mark in CSX's BCG Matrix. Elevated spending aims to fuel growth, but tangible benefits are anticipated from 2026 onwards. The timing and magnitude of returns hinge on effective management and strategic execution. These investments are crucial for enhancing CSX's competitive positioning.

- Anticipated benefit timeframe: 2026.

- Focus: Intermodal network investment.

- Strategic necessity: Competitive enhancement.

- Investment impact: Growth driver.

Navigating Regulations: A Rail Giant's Path

CSX's sustainability initiatives are a question mark due to environmental regulations. Investments in eco-friendly practices could boost market position. East Coast port developments also place CSX in this quadrant.

| Aspect | Details | Impact |

|---|---|---|

| Sustainability | Focus: Emission reduction targets | Evolving environmental laws are shaping this area |

| Port Developments | Labor disputes resolved; freight returns | Growth depends on efficiency and pricing |

| Business Development | Leveraging network for new ventures | Market dynamics and customer retention |

BCG Matrix Data Sources

The CSX BCG Matrix leverages SEC filings, financial databases, and market reports, providing comprehensive insights for each strategic segment.