Northfield Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Northfield Bank Bundle

What is included in the product

Analyzes Northfield Bank's position by evaluating competition, buyers, suppliers, and new threats.

Easily adjust competitive force weights for Northfield Bank. Visualize changing pressures with dynamic charts.

What You See Is What You Get

Northfield Bank Porter's Five Forces Analysis

This preview is the full Northfield Bank Porter's Five Forces Analysis. The detailed assessment of competitive forces you see is what you'll receive immediately after purchase. It's a complete, ready-to-use document, professionally analyzed and formatted. There are no differences; what you see is what you get. Download and utilize the exact same file upon completion.

Porter's Five Forces Analysis Template

From Overview to Strategy Blueprint

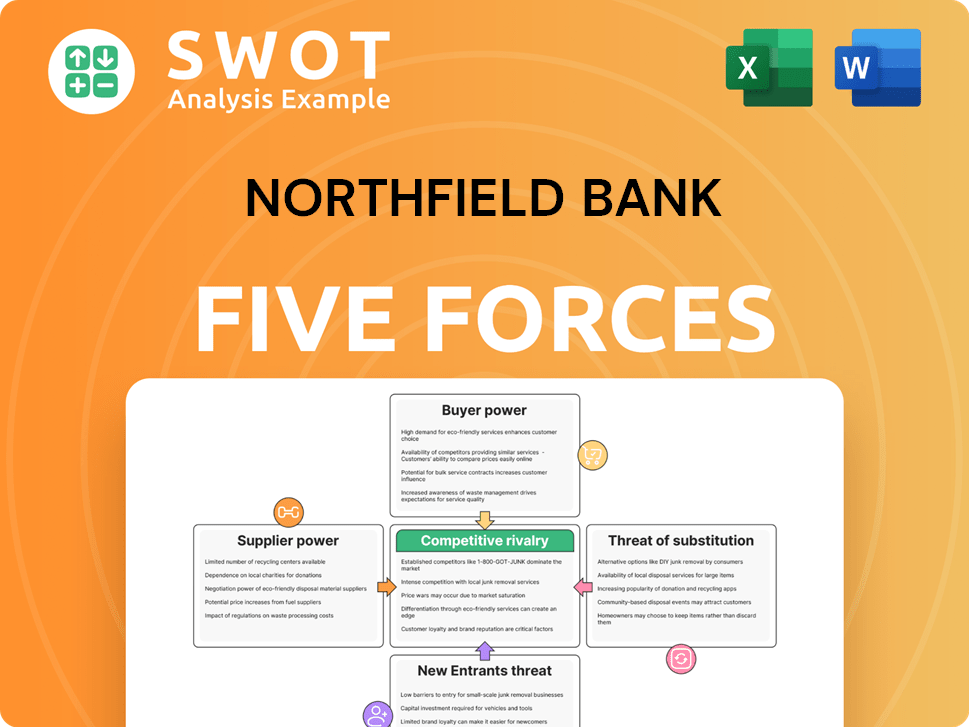

Northfield Bank faces competitive pressures in its industry, including moderate rivalry. Buyer power is somewhat concentrated, influencing pricing strategies. The threat of new entrants is moderate, given regulatory hurdles. Substitute products, like online banking, pose a manageable threat. Supplier power, primarily from labor, is also moderate.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Northfield Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Concentration

The bargaining power of suppliers to Northfield Bank is generally low. Suppliers like tech providers serve many banks, reducing their dependence on one client. The banking industry's diverse options for technology and services further diminish individual supplier power. In 2024, the financial services technology market is highly competitive, with numerous vendors. This competition limits any single supplier's ability to dictate terms to Northfield Bank.

Technology Costs

Suppliers of crucial tech and software hold some power over Northfield Bank. The bank's heavy reliance on tech for cybersecurity and digital platforms gives vendors leverage. Northfield can counter this by choosing vendors wisely and negotiating hard. Having multiple vendors ensures competitive pricing; in 2024, banks spent an average of 10% of their revenue on technology.

Labor Market Dynamics

Employees, especially those with specialized skills, are key suppliers. The bargaining power of skilled employees is moderate, especially for roles like IT and wealth management. Northfield Bank must offer competitive compensation to attract talent. The average salary for a bank teller in New York City was $40,000 in 2024, reflecting the need to stay competitive.

Regulatory Compliance

Regulatory compliance, dictated by bodies like the FDIC, significantly impacts Northfield Bank. These regulators act as suppliers of operational standards, wielding considerable power. Banks face substantial penalties, such as fines exceeding $100,000 for each violation, for non-compliance. Meeting regulatory demands necessitates considerable investment in infrastructure and expertise.

- FDIC insured deposits totaled $9.4 trillion in Q4 2023.

- Banks spent an average of 5-10% of their revenue on compliance in 2024.

- The average fine for regulatory breaches in the banking sector was $2.5 million in 2024.

Service Provider Agreements

Northfield Bank's reliance on external service providers, like data processors or consultants, influences supplier bargaining power. This power hinges on the uniqueness of the services and the availability of alternatives. For instance, the global market for IT outsourcing reached $482.6 billion in 2024, signaling considerable supplier options. To mitigate this, the bank should diversify its supplier network and negotiate flexible contracts.

- Supplier concentration impacts negotiating leverage.

- Contract flexibility is vital for adapting to market changes.

- Diversification reduces dependence on single suppliers.

- Competitive bidding can secure better terms.

Bank's Supplier Power Dynamics: A Quick Look

Northfield Bank's supplier power varies. Tech and service providers have less power due to market competition. Specialized skills like IT give employees moderate bargaining power. Regulatory bodies, like the FDIC, wield strong influence.

| Supplier Type | Bargaining Power | 2024 Data Points |

|---|---|---|

| Tech Providers | Low | Market size $1.2T, average bank tech spend 10% of revenue. |

| Skilled Employees | Moderate | Avg. teller salary $40K in NYC. |

| Regulatory Bodies | High | Avg. fine for breaches $2.5M. |

Customers Bargaining Power

Customer Switching Costs

Individual customers typically have low bargaining power because of low switching costs. Customers can readily switch to other financial institutions. In 2024, the average customer churn rate in the banking sector was around 5%. Northfield Bank must focus on customer retention through personalized service and competitive offerings. This approach helps to counteract customer mobility.

Interest Rate Sensitivity

Customers show high sensitivity to interest rates, a key factor in the current economy. They readily move deposits to banks with better rates. Northfield Bank needs strategic deposit rate management to attract and keep deposits while ensuring profits. This includes closely tracking competitor rates and market shifts. In 2024, the Federal Reserve's actions significantly impacted interest rates, influencing customer behavior. For example, data from the FDIC shows that in Q3 2024, the average savings account interest rate was 0.46%, and the average money market account rate was 0.71%.

Loan Demand

Borrowers, especially commercial clients, wield moderate bargaining power, particularly during periods of weak loan demand. For instance, in 2024, a slowdown in economic activity led to increased competition among banks, intensifying the pressure to offer favorable loan terms. Northfield Bank must carefully balance attracting borrowers with maintaining prudent lending practices and profitability. This is crucial as net interest margins, a key profitability indicator, were already under pressure in the first half of 2024. Building strong client relationships and offering flexible loan products can bolster its competitive edge. This strategy helped Northfield Bank maintain a stable loan portfolio throughout 2024.

Digital Banking Expectations

Customers now demand easy-to-use digital banking. Banks lacking this risk losing clients to those with better platforms. Northfield Bank needs to constantly upgrade its digital services. AI-driven hyper-personalization is a key differentiator.

- 77% of U.S. adults use online banking.

- 56% of consumers would switch banks for a better digital experience.

- Banks are increasing their IT spending by 8% annually to improve digital platforms.

- Personalized banking experiences can boost customer satisfaction by up to 20%.

Service Fees and Transparency

Customers are becoming more fee-conscious and expect clear banking practices. Hidden charges and bad service can push clients to other banks. Northfield Bank needs transparent fees and great customer service to keep customers and boost its brand. Emotional banking, building strong customer relationships, is growing in importance.

- In 2024, 65% of consumers switched banks due to unexpected fees or poor service, as reported by a consumer banking survey.

- Transparent fee structures have increased customer satisfaction by 30% in the banking sector.

- Banks focusing on customer experience saw a 20% rise in customer retention rates in 2024.

- Emotional banking strategies have improved customer loyalty by 25% in various financial institutions.

Bank's 2024 Strategy: Digital, Fees, and Rates

Individual customers' power is low due to easy bank switching; in 2024, churn was ~5%.

Interest rate sensitivity is high, requiring strategic deposit management.

Borrowers have moderate power, especially in weak loan demand times, where net interest margins were already pressured in the first half of 2024.

| Aspect | Impact | Northfield Bank Action |

|---|---|---|

| Digital Banking | Essential for retaining customers; 77% use online banking | Upgrade digital services, AI-driven personalization |

| Fee Transparency | Crucial; 65% switched due to unexpected fees in 2024 | Transparent fees, great customer service |

| Interest Rates | High sensitivity to rates impacting deposits | Strategic deposit rate management |

Rivalry Among Competitors

Intense Local Competition

Northfield Bank operates in a highly competitive market, especially within the New York and New Jersey metropolitan area, facing off against numerous banks and credit unions. This intense rivalry can trigger price wars, increasing marketing costs, and squeezing profit margins. In 2024, the average net interest margin for banks in this region remained under pressure due to competition. To thrive, Northfield Bank must distinguish itself through excellent service, unique products, or a robust community presence.

Dominance of Large Banks

The competitive landscape in banking is shaped by the dominance of national banks. These giants possess substantial resources, enabling them to provide diverse services and invest heavily in technology. In 2024, the top 10 U.S. banks held over 50% of total banking assets. Northfield Bank faces the challenge of differentiating itself from these larger competitors. Northfield must leverage its local expertise and personalized customer service to compete.

Digital Disruption

Fintech firms and digital banks challenge traditional banking. They provide innovative services with lower costs and flexibility. In 2024, digital banking adoption grew, with over 60% of U.S. adults using online banking monthly. Northfield Bank must adapt, investing in tech and partnering with fintechs to stay competitive. Northfield Bank's 2023 annual report shows increasing digital transactions, highlighting the need for digital transformation.

Market Consolidation

The banking sector is seeing significant consolidation, with mergers and acquisitions reshaping the competitive landscape. Larger banks are buying smaller ones, leading to increased market concentration. This trend intensifies competition, as bigger players leverage greater resources and scale. Northfield Bank needs to stay adaptable and efficient to compete in this evolving environment.

- In 2024, M&A activity in the U.S. banking sector reached $40 billion.

- Consolidation can lead to reduced competition and potentially higher prices for consumers.

- Northfield Bank's strategic focus on customer service can be a differentiator.

- Efficiency improvements are crucial for Northfield to compete effectively.

Interest Rate Environment

Fluctuating interest rates heavily influence competitive rivalry within the banking sector. Banks like Northfield Bank fiercely compete for both deposits and loans, making them sensitive to rate changes. In 2024, the Federal Reserve's actions directly impacted these dynamics. Northfield Bank must carefully manage its assets and liabilities to stay competitive.

- Federal Reserve raised interest rates in 2024, impacting borrowing costs.

- Banks adjusted deposit rates to attract customers.

- Northfield Bank's profitability depends on its interest rate spread.

- Competition for loans intensified as rates rose.

Banking's $40B Shakeup: Northfield's Strategy

Competition in Northfield Bank's market is fierce, involving many banks and digital rivals. National banks and fintech firms drive this, increasing pressure. In 2024, M&A in the U.S. banking sector reached $40 billion, reshaping the landscape.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Rivalry Intensity | High, driven by national banks & fintechs | M&A: $40B in U.S. banking sector |

| Market Dynamics | Consolidation & rate-sensitive | Fed raised rates impacting borrowing costs |

| Northfield Response | Adapt & differentiate through service | Digital banking monthly usage over 60% |

SSubstitutes Threaten

Fintech Payment Systems

Fintech firms present a significant threat to Northfield Bank, offering payment alternatives like PayPal and Zelle. These platforms, with their user-friendly interfaces and lower costs, lure customers away from traditional banking. In 2024, digital payments in the US are projected to reach $10.4 trillion, highlighting the shift. Northfield Bank must adopt digital payment solutions to stay competitive.

Peer-to-Peer Lending

Peer-to-peer (P2P) lending platforms present a threat to Northfield Bank by offering an alternative to traditional loans. These platforms connect borrowers and lenders directly, often with better terms and quicker approvals. To compete, Northfield Bank must improve its lending processes and offer competitive rates. In 2024, P2P lending volume reached $1.5 billion, showing its growing market share.

Credit Unions

Credit unions pose a threat to Northfield Bank due to their similar offerings at potentially lower costs. They attract customers with member-focused service and favorable rates. Northfield Bank needs to highlight its unique strengths, such as specialized services, to compete. In 2024, credit unions held over $2 trillion in assets, indicating their growing market presence.

Non-Bank Financial Institutions

Non-bank financial institutions pose a threat to Northfield Bank. These institutions, including investment firms and insurance companies, offer wealth management and investment services that can substitute traditional bank offerings. They often provide specialized expertise and a wider range of investment options.

- Investment management assets in the US reached $110.7 trillion in Q4 2023.

- Insurance companies held $37.7 trillion in assets as of Q4 2023.

- Northfield Bank needs to enhance its wealth management services.

- Comprehensive financial planning is essential to compete.

Cryptocurrencies

Cryptocurrencies and DeFi platforms pose a growing threat. They offer alternative ways to store and transfer value. The market cap of all cryptocurrencies reached over $2.5 trillion in 2024, showing significant growth. Northfield Bank must watch these trends closely.

- Cryptocurrency market cap reached over $2.5T in 2024.

- DeFi platforms provide alternative financial services.

- Blockchain technology is key for future adaptation.

Banking's Rivals: Digital Payments, P2P, Crypto

Substitutes, such as digital payments and P2P lending, challenge Northfield Bank. Fintech and P2P offer alternatives to traditional banking services. Cryptocurrencies are emerging substitutes.

| Threat | Substitute | 2024 Data |

|---|---|---|

| Digital Payments | Fintech Platforms | $10.4T in US digital payments |

| Loans | P2P Lending | $1.5B P2P lending volume |

| Value Storage | Cryptocurrencies | $2.5T crypto market cap |

Entrants Threaten

High Regulatory Barriers

The banking sector faces stringent regulations, acting as a significant hurdle for new entrants. New banks must secure multiple licenses and meet substantial capital requirements, which are costly and time-consuming. These high regulatory barriers, as of late 2024, help shield established banks like Northfield Bank. This protection is evident in the limited number of new bank charters granted annually; for example, in 2023, only a handful were approved across the U.S.

Capital Intensive

Starting a new bank demands significant capital investment. Newcomers need substantial funds to satisfy regulatory capital needs and operational costs. This high capital need discourages many potential entrants. In 2024, the FDIC insured about $9.7 trillion in deposits, showing the scale of financial commitment. This gives established banks like Northfield Bank a competitive edge.

Established Brand Loyalty

Established banks, like Northfield Bank, benefit from existing brand loyalty and customer relationships, a significant barrier for new entrants. New banks face substantial marketing and customer acquisition costs to compete. Northfield Bank leverages its strong reputation in the New York and New Jersey area. In 2024, the average cost to acquire a new banking customer was around $300-$500.

Economies of Scale

Established banks like Northfield Bank leverage economies of scale, offering services at reduced costs. New entrants face challenges competing on price due to smaller size and higher costs. Northfield Bank's infrastructure provides a notable cost advantage. This makes it harder for new players to gain market share. For instance, Northfield Bank's operational efficiency could be reflected in a lower cost-to-income ratio compared to newer, smaller banks.

- Northfield Bank's existing branch network and digital platforms contribute to operational efficiency.

- Economies of scale allow for more competitive pricing on loans and services.

- New banks might struggle to match these prices initially, impacting profitability.

- Cost-to-income ratio is a key metric to watch.

Fintech Partnerships

The threat of new entrants for Northfield Bank is influenced by fintech partnerships. While new banks face high barriers, fintech companies can enter the market by partnering with existing banks. These collaborations allow fintech firms to provide innovative services without needing a full banking license. Northfield Bank should consider partnerships to enhance its offerings and stay competitive.

- Fintech partnerships can streamline operations and reduce costs.

- By 2024, the global fintech market is projected to reach $305 billion.

- Partnerships can offer access to new customer segments.

- Northfield Bank can benefit from fintech's technological expertise.

Banking Battleground: Navigating Entry Barriers

New banks face steep regulatory and capital hurdles, limiting market entry and protecting existing players like Northfield Bank. High customer acquisition costs and established brand loyalty further deter new entrants. Strategic fintech partnerships offer both challenges and opportunities. Northfield Bank must navigate these dynamics to maintain its competitive edge.

| Factor | Impact | Data |

|---|---|---|

| Regulatory Barriers | High entry costs & delays | Limited bank charters approved in 2023 across U.S. |

| Capital Needs | Significant investment | FDIC insured $9.7T in deposits in 2024 |

| Customer Acquisition | Costly marketing | Acquiring a customer cost $300-$500 in 2024 |

Porter's Five Forces Analysis Data Sources

This analysis is based on financial statements, market reports, regulatory filings, and competitive intelligence databases.