Fannie Mae Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Fannie Mae Bundle

What is included in the product

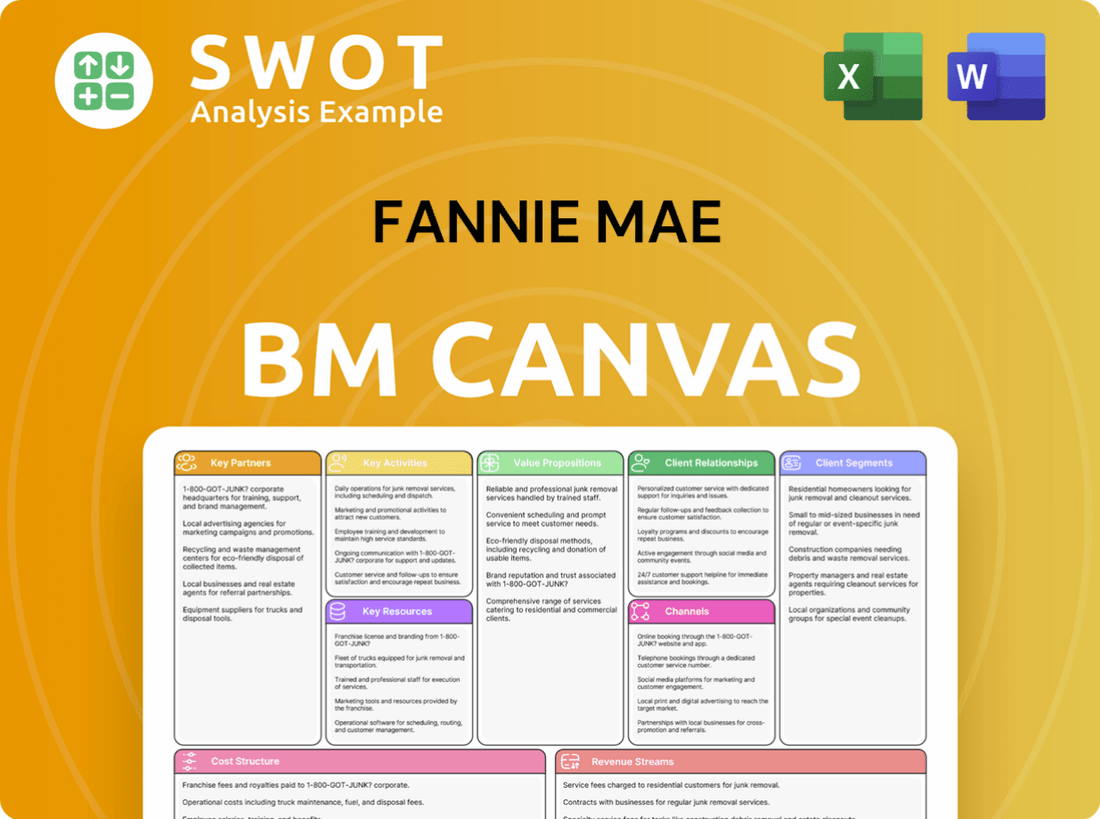

Fannie Mae's BMC is a comprehensive model detailing customer segments, channels & value propositions.

Condenses company strategy into a digestible format for quick review.

Full Document Unlocks After Purchase

Business Model Canvas

This preview displays the genuine Fannie Mae Business Model Canvas document you'll receive. It's the complete file, formatted professionally, ready for immediate use. After purchase, you'll download the same document, entirely unlocked. It includes all sections as you see here—no hidden content. The document is fully editable and easily shared.

Business Model Canvas Template

Fannie Mae's Business Model Unveiled!

Explore Fannie Mae's strategic framework with our Business Model Canvas. This tool dissects the company’s value proposition, customer segments, and key activities.

Understand how Fannie Mae navigates the mortgage market and generates revenue streams.

The canvas reveals critical partnerships and cost structures driving its operational efficiency.

Analyze Fannie Mae's business model in detail, and how it interacts with its environment.

Unlock strategic insights and apply them to your own investment decisions or business strategies.

Ready to dive deeper? Gain access to the complete Fannie Mae Business Model Canvas!

Partnerships

DUS Lender Network

Fannie Mae's Delegated Underwriting and Servicing (DUS) lender network is crucial for multifamily loan origination and servicing. These lenders offer essential local market expertise and customer relationships. In 2024, the DUS network facilitated over $55 billion in multifamily lending volume. Fannie Mae collaborates with these lenders to broaden its product offerings and enhance underwriting standards.

Federal Housing Finance Agency (FHFA)

The Federal Housing Finance Agency (FHFA) is crucial for Fannie Mae, establishing its regulatory landscape. In 2024, FHFA set a $70 billion loan purchase cap per Enterprise, with at least 50% mission-driven. For 2025, this cap increases to $73 billion, retaining the 50% mission-driven minimum. This partnership ensures Fannie Mae's compliance and strategic direction.

Community Development Financial Institutions (CDFIs)

Community Development Financial Institutions (CDFIs) are crucial partners for Fannie Mae, especially in underserved areas. They collaborate to identify loan eligibility and acquisition methods. The 2025-2027 Duty to Serve plan focuses on innovative housing solutions. Fannie Mae's partnership with CDFIs is key to expanding access to housing. In 2024, Fannie Mae invested $1.1 billion in CDFIs.

Housing Finance Agencies (HFAs)

Housing Finance Agencies (HFAs) are crucial state-level partners, aiming to increase affordable housing. Fannie Mae collaborates with HFAs, broadening affordable homeownership access for various income levels. This partnership enhances the availability of mortgages, supporting borrowers in achieving their homeownership goals. Fannie Mae actively innovates with HFAs and CDFIs, strengthening services for low- to moderate-income borrowers.

- In 2024, Fannie Mae and Freddie Mac supported over 1.4 million first-time homebuyers.

- HFAs issued $85 billion in bonds in 2023, funding affordable housing initiatives.

- Fannie Mae's HFA Advantage program offers lower mortgage rates.

Mortgage Servicers

Mortgage servicers are crucial partners for Fannie Mae, handling loan portfolios, borrower interactions, and loss mitigation. The Servicer Total Achievement and Rewards (STAR) Program highlights top performers. In February 2025, Fannie Mae revealed its 2024 STAR Program results. Twenty-nine mortgage servicers were recognized for their performance.

- STAR Program recognizes high-performing servicers.

- 29 servicers were recognized in 2024.

- Servicers manage loan portfolios.

- They work with borrowers.

Key Alliances Fueling Housing Initiatives

Fannie Mae's key partnerships encompass diverse entities. These include DUS lenders for origination and servicing, with over $55 billion in 2024 multifamily lending volume. Collaborations with CDFIs, and HFAs are key to affordable housing expansion, with $1.1 billion invested in CDFIs during 2024. Mortgage servicers also play a crucial role, managing loan portfolios, and 29 servicers were recognized in 2024.

| Partners | Focus | 2024 Data |

|---|---|---|

| DUS Lenders | Multifamily Lending | $55B+ volume |

| CDFIs | Affordable Housing | $1.1B investment |

| HFAs | Affordable Homeownership | $85B bonds (2023) |

Activities

Mortgage Purchases

A key activity for Fannie Mae involves buying mortgages from lenders, giving them funds to make more loans. Fannie Mae then bundles these mortgages, creating mortgage-backed securities (MBSs). In 2024, they acquired about 778,000 single-family purchase loans. About half of these loans supported first-time homebuyers.

Securitization

Fannie Mae's securitization process involves pooling mortgages into mortgage-backed securities (MBSs) for investors. This is a key activity, ensuring liquidity in the housing market. In 2024, they guaranteed roughly $3.3 trillion in outstanding MBSs. Fannie Mae guarantees against losses from defaults on these MBSs, retaining credit risk.

Risk Management

Managing credit risk is vital; this includes evaluating loan quality and setting guarantee fees. Fannie Mae uses credit risk transfer programs to mitigate risk. They also offer multi-language resources for lenders. Fannie Mae partners with lenders to reduce risk, enhancing quality and oversight. In 2024, Fannie Mae's CRT programs transferred $1.2 trillion in credit risk.

Affordable Housing Initiatives

Fannie Mae's key activities include promoting affordable housing. They support Low-Income Housing Tax Credit (LIHTC) investments and offer products like HomeReady. A notable initiative is the HomeReady $2,500 credit, assisting very low-income first-time homebuyers with down payments or closing costs. This credit applies to loans where at least one borrower is a first-time homebuyer, starting March 1, 2025. These efforts aim to increase homeownership opportunities.

- HomeReady credit provides $2,500 for VLIP first-time homebuyers.

- LIHTC investments are also a key part of Fannie Mae's affordable housing efforts.

- This initiative aims to lower barriers to homeownership.

- Eligibility for the VLIP credit begins with deliveries on March 1, 2025.

Market Analysis and Forecasting

Fannie Mae conducts market analysis and forecasting, offering crucial insights for its strategies. The Economic and Strategic Research (ESR) Group at Fannie Mae gives forward-looking perspectives on housing trends. Their forecasts help shape the real estate industry's direction. In 2024, Fannie Mae’s ESR group predicted mortgage rates would remain elevated.

- Fannie Mae's ESR Group forecasts are a key resource.

- They analyze factors impacting the housing market.

- In 2024, they predicted mortgage rates above 6%.

- This helps the industry and Fannie Mae plan.

Key Actions and 2024 Data

Fannie Mae's core actions involve purchasing, securitizing, and guaranteeing mortgages. In 2024, they bought about 778,000 single-family purchase loans, supporting market liquidity. Managing credit risk through programs like Credit Risk Transfer is another key function, which transferred $1.2 trillion in risk.

| Key Activity | Description | 2024 Data |

|---|---|---|

| Mortgage Acquisition | Buying mortgages from lenders. | 778,000 single-family purchase loans |

| Securitization | Bundling mortgages into MBSs. | $3.3T in outstanding MBSs guaranteed |

| Credit Risk Management | Mitigating risk through various programs. | $1.2T in risk transferred via CRT |

Resources

Financial Capital

Fannie Mae's financial capital is crucial for operations. This includes buying mortgages, creating mortgage-backed securities (MBS), and managing potential losses. In 2024, net income hit $17.0 billion, boosting net worth to $94.7 billion by year-end.

Fannie Mae's financial health is supported by strong revenues. Net revenues reached $29.1 billion. These revenues are largely from guaranty fees on its $4.1 trillion guaranty book of business, showing financial strength.

Guarantee Book of Business

Fannie Mae's guarantee book of business is a significant key resource. This generates continuous revenue through guaranty fees. In 2024, $29.1 billion in revenue came from its $4.1 trillion guaranty book. About 99% of its multifamily book used lender loss-sharing, and 31% had credit risk transfer.

Technology and Data Analytics

Technology and data analytics are crucial for Fannie Mae's operations, especially for underwriting and risk management. The Valuation Modernization Plan uses data analysis and technology to modernize valuation. Solutions like Desktop Underwriter (DU) and Desktop Originator (DO) are integrated within Encompass. In 2024, Fannie Mae's investments in technology reached $1.5 billion.

Relationships with Lenders

Fannie Mae heavily relies on its relationships with lenders to function effectively. Their Delegated Underwriting and Servicing (DUS) lender network is essential for originating mortgages and distributing Fannie Mae's offerings. In 2024, these partnerships were vital in providing liquidity across different housing sectors. Fannie Mae actively expanded its product range and strengthened its underwriting through these lender collaborations.

- DUS lenders are key for mortgage sourcing.

- Relationships support product distribution and innovation.

- These partnerships provided significant liquidity in 2024.

- Underwriting was strengthened through lender collaboration.

Skilled Workforce

Fannie Mae relies on a skilled workforce to handle its intricate processes such as underwriting and risk management. Midwest Loan Services earned the Fannie Mae STAR™ Performer recognition in 2024 for General Servicing. This shows their dedication to operational excellence, compliance, and customer service. A capable team is crucial for Fannie Mae's success.

- Fannie Mae's 2024 net worth was approximately $58.8 billion.

- Midwest Loan Services manages over $350 billion in mortgage servicing.

- STAR™ Performer status highlights top-tier service quality.

- The mortgage servicing market is valued at trillions of dollars.

Key Resources: Capital, Tech, and Partnerships

Key resources for Fannie Mae involve financial capital, generating revenue, and a robust guarantee book. They also include technology for underwriting and risk management, and partnerships with lenders. Additionally, Fannie Mae relies on a skilled workforce for operational success.

| Resource | Description | 2024 Data |

|---|---|---|

| Financial Capital | Funds for mortgage purchases, MBS, and managing losses. | $17.0B net income, $94.7B net worth |

| Revenue Generation | Income sources from guaranty fees, etc. | $29.1B in net revenues |

| Guarantee Book | Mortgage portfolio generating revenue via fees. | $4.1T guaranty book |

| Technology | Tools for underwriting and data analysis. | $1.5B invested in tech |

| Lender Relationships | Network for mortgage origination and distribution. | Vital for 2024 liquidity |

| Workforce | Skilled staff for processes. | Midwest Loan Services STAR™ Performer |

Value Propositions

Liquidity in the Mortgage Market

Fannie Mae injects liquidity into the mortgage market by buying mortgages from lenders. This support allows lenders to offer more mortgages, boosting homeownership. In 2024, Fannie Mae supplied $381 billion in liquidity. This funding facilitated roughly 1.4 million home purchases and refinances.

Affordable Housing

Fannie Mae actively promotes affordable housing. They offer initiatives and products to help lower-income families achieve homeownership and rent quality housing. In 2024, Fannie Mae pushed its SDW and SIA programs for multifamily borrowers. These efforts use private financing to boost workforce and affordable housing. Their goal is to increase mortgage credit access nationwide.

Risk Management and Stability

Fannie Mae's risk management stabilizes the mortgage market by setting loan standards, reducing defaults. In 2024, nearly all of Fannie Mae's multifamily guaranty book used lender loss-sharing agreements. This strategy, including credit risk transfers, decreases risk. Partnering with lenders boosts quality and oversight, securing certainty.

Standardized Loan Products

Fannie Mae's standardized loan products simplify mortgage origination through consistent guidelines. These products, tailored to various borrower needs, support responsible lending and a stable housing market. In 2024, Fannie Mae's efforts included expanding access to homeownership with innovative mortgage options. This approach benefits both lenders and borrowers, fostering a healthy market.

- Standardized loan products streamline mortgage processes.

- They support responsible lending practices.

- Fannie Mae offers diverse mortgage options.

- These options aim to broaden homeownership.

Access to Capital Markets

Fannie Mae's ability to securitize mortgages is a cornerstone of its value proposition, linking the mortgage market with the vast capital markets. This process attracts investors, boosting the availability of funds for mortgages. Fannie Mae buys mortgages from lenders, taking on the credit risk, and then turns these mortgages into mortgage-backed securities (MBSs). In 2024, the total outstanding MBSs issued by Fannie Mae and Freddie Mac reached approximately $5.8 trillion, underscoring their critical role.

- Securitization connects mortgage market to capital markets.

- Fannie Mae issues mortgage-backed securities (MBSs).

- Enterprises retain the credit risks.

- In 2024, MBSs totaled around $5.8 trillion.

Fannie Mae: Stabilizing the Housing Market

Fannie Mae's value lies in creating a stable, liquid mortgage market. They offer consistent loan products that support responsible lending. This aids in expanding homeownership opportunities. As of Q4 2024, Fannie Mae's mortgage portfolio was approximately $3.9 trillion.

| Value Proposition | Description | 2024 Data |

|---|---|---|

| Liquidity Provision | Provides funds to lenders for mortgage lending. | $381B in liquidity. |

| Affordable Housing | Supports homeownership for lower-income families. | SDW & SIA programs. |

| Risk Management | Stabilizes the market through loan standards. | $5.8T MBS outstanding. |

Customer Relationships

Automated Underwriting Systems

Fannie Mae's Desktop Underwriter (DU) streamlines loan assessment for lenders. DU, integrated with Encompass, offers detailed eligibility and risk evaluations. It speeds up processes for property value, income, and employment verification. DU facilitates Day 1 Certainty, reducing reps and warrants. In 2024, this boosted efficiency and cut processing times by up to 20% for participating lenders.

Lender Training and Support

Fannie Mae provides comprehensive training and support to lenders. The Originating and Underwriting Learning Center offers guideline clarifications. In 2024, Fannie Mae's resources included multi-language support. This helps lenders navigate complex regulations effectively. This support system ensures compliance and efficiency.

Housing Counseling Resources

Fannie Mae prioritizes customer relationships by backing housing counseling, aiding informed borrower decisions, and preventing foreclosures. The HomeReady $2,500 credit is offered to very low-income first-time homebuyers for down payments or closing costs. Starting March 1, 2025, at least one borrower must be a first-time homebuyer to qualify for the VLIP LLPA Credit. In 2024, approximately 40% of first-time homebuyers utilized down payment assistance programs.

Servicer Engagement

Fannie Mae's Servicer Engagement focuses on improving mortgage servicing through initiatives like the STAR Program. This program aims to enhance servicing standards and reduce credit losses by fostering knowledge and excellence. The STAR Program has driven consistent servicer improvements in performance metrics and operational assessments. In 2024, Fannie Mae continued to refine its STAR Program, with over 400 servicers participating.

- STAR Program enhancements in 2024 focused on loss mitigation and borrower assistance.

- Servicer performance metrics are tracked quarterly, with reports publicly available.

- The program's impact is measured by lower delinquency rates and reduced foreclosure timelines.

- Fannie Mae provides training and resources to support servicers' success.

Market Insights and Data

Fannie Mae offers market insights and data to inform stakeholders about housing trends, aiding in decision-making. Their Economic and Strategic Research (ESR) Group forecasts upcoming trends, influencing the real estate environment. This includes predictions for home prices, mortgage rates, and sales. These insights help lenders and investors navigate the market effectively.

- In 2024, Fannie Mae predicted a slight increase in home prices.

- Mortgage rates are a key focus, with forecasts impacting affordability.

- Sales forecasts provide insight into market activity.

- The ESR group's analysis is crucial for strategic planning.

Empowering Homeownership: Programs & Resources

Fannie Mae cultivates strong relationships by supporting borrowers and lenders through programs and resources. Housing counseling and the HomeReady program offer financial assistance, promoting informed decisions and reducing foreclosures. The Servicer Engagement initiatives, such as the STAR Program, enhance servicing standards to improve mortgage servicing.

| Customer Focus | Initiatives | 2024 Impact |

|---|---|---|

| Borrowers | HomeReady Program | 40% of first-time homebuyers used down payment assistance. |

| Lenders | STAR Program | Over 400 servicers participated, improving servicing standards. |

| Market | Economic Insights | Predictions for home prices and mortgage rates helped strategic planning. |

Channels

DUS Lender Network

The DUS lender network is a crucial channel for multifamily loan originations. In 2024, Fannie Mae utilized its DUS partners to offer borrowers diverse products, enhancing underwriting. This network was instrumental in providing substantial liquidity across essential housing sectors last year. Fannie Mae's DUS program accounted for a significant portion of its multifamily lending volume. The DUS network's role underscores its importance in Fannie Mae's business model.

Correspondent Lending

Fannie Mae utilizes correspondent lenders to acquire mortgages compliant with its standards. In 2024, Fannie Mae injected $381 billion into the U.S. housing market. This supported about 1.4 million home purchases, refinances, and rental units. The Single-Family segment generates most of Fannie Mae's revenue. Correspondent lending is vital to this model.

Mortgage Brokers

Mortgage brokers act as intermediaries, originating loans that Fannie Mae may purchase. They play a crucial role in connecting borrowers with Fannie Mae's offerings. This is particularly relevant for mortgage bankers, brokers, and financial institutions. Changes were implemented in DU® on July 20, 2024. Pennymac aligned with these changes immediately. The broker channel represented 10% of total volume in 2024.

Online Platforms

Fannie Mae leverages online platforms to enhance loan processes. Key solutions like Desktop Underwriter (DU) and Desktop Originator (DO) are integrated within Encompass. These tools offer comprehensive eligibility and credit risk assessments. This approach aims to speed up processes and reduce risks.

- DU processed approximately 1.3 million loans in 2023.

- Day 1 Certainty saw a 20% increase in usage by Q4 2024.

- Encompass integration streamlined processing by 15% in 2024.

- Fannie Mae's tech investments reached $500 million in 2024.

Direct Sales (Securities)

Fannie Mae utilizes direct sales to distribute its mortgage-backed securities (MBSs) to investors. This channel involves selling MBSs directly through capital market channels, offering investors bond-like securities. In 2024, the outstanding MBS balance was approximately $3.9 trillion. These securities are backed by the credit risk of mortgages purchased from originators. Fannie Mae's direct sales strategy is a key component of its business model.

- Direct sales channels include institutional investors like pension funds and insurance companies.

- In Q1 2024, Fannie Mae issued around $100 billion in MBS.

- MBSs provide liquidity to the housing market.

- This approach helps manage credit risk exposure.

Mortgage Channels: Key Players & 2024 Data

Fannie Mae's diverse channels include DUS partners, correspondent lenders, and mortgage brokers. In 2024, these channels facilitated substantial mortgage activity, with the broker channel representing 10% of the total volume. Online platforms and direct sales of MBS also played key roles.

| Channel | Description | 2024 Data |

|---|---|---|

| DUS Lenders | Multifamily loan originations | Significant portion of multifamily lending |

| Correspondent Lenders | Acquire mortgages compliant with standards | $381B injected into housing market |

| Mortgage Brokers | Intermediaries, connecting borrowers | 10% of total volume |

Customer Segments

Mortgage Lenders

Mortgage lenders are Fannie Mae's primary customers, as the agency buys mortgages from them, injecting liquidity into the market. Fannie Mae then pools these mortgages to create mortgage-backed securities (MBSs). In 2024, Fannie Mae enhanced its multifamily initiatives. These initiatives used private financing to create and preserve workforce and affordable housing.

Mortgage Servicers

Mortgage servicers manage loan portfolios and interact directly with borrowers, playing a crucial role in Fannie Mae's operations. Fannie Mae depends on these servicers for loan administration, ensuring smooth operations. The STAR Program recognizes top-performing servicers based on their competency and performance. In 2024, Fannie Mae recognized certain servicers as STAR Performers in General Servicing. As of late 2024, data indicates significant reliance on servicers to manage approximately $4.3 trillion in outstanding mortgage debt.

Homebuyers

Fannie Mae indirectly supports homebuyers by facilitating mortgage availability. In 2024, Fannie Mae provided $381 billion in liquidity, enabling 1.4 million home purchases and refinances. About half of the 778,000 single-family purchase loans acquired were for first-time buyers. Additionally, around 204,000 single-family refinance loans were completed in 2024.

Multifamily Borrowers

Multifamily borrowers, including apartment building developers and owners, rely on Fannie Mae's financing programs. In 2024, Fannie Mae, through its DUS lender partners, supported these borrowers by expanding its product offerings and strengthening its underwriting processes. Fannie Mae's commitment provided substantial liquidity across essential housing sectors. This ensured continued support for multifamily projects.

- Fannie Mae's 2024 multifamily business volume reached $79.5 billion.

- DUS lenders completed over 1,700 transactions in 2024.

- The DUS program maintained a 98% customer satisfaction rating.

- Fannie Mae supported over 800,000 rental units in 2024.

Investors

Investors, including institutional investors like pension funds and insurance companies, are key customer segments for Fannie Mae. They buy Fannie Mae's mortgage-backed securities (MBS), which are essentially bonds backed by pools of mortgages. This investment provides capital, supporting the housing market by funding new mortgages. The Enterprises guarantee the credit risk of the mortgages.

- In 2024, Fannie Mae's outstanding MBS reached trillions of dollars.

- MBSs offer investors a relatively safe investment with steady income.

- The guarantee provided by Fannie Mae reduces investor risk.

- Institutional investors are the primary buyers of these securities.

Who Benefits from Fannie Mae's Operations?

Fannie Mae's customer base includes mortgage lenders, vital for purchasing mortgages and injecting market liquidity. Mortgage servicers manage loan portfolios, ensuring smooth operations and direct borrower interaction. Homebuyers benefit indirectly from Fannie Mae's efforts, as it facilitates mortgage availability.

Multifamily borrowers, such as apartment developers, rely on Fannie Mae's financing programs, with 2024's business volume reaching $79.5 billion. Investors, including institutions, buy mortgage-backed securities (MBSs), backed by mortgage pools. These MBSs provide capital to support the housing market.

| Customer Segment | Role | 2024 Data |

|---|---|---|

| Mortgage Lenders | Sell mortgages | Provided $381B in liquidity |

| Mortgage Servicers | Manage loans | Managed ~$4.3T in debt |

| Homebuyers | Benefit from mortgages | Enabled 1.4M home transactions |

| Multifamily Borrowers | Utilize financing | $79.5B business volume |

| Investors | Buy MBSs | Outstanding MBSs in trillions |

Cost Structure

Loan Purchases

The cost structure for Fannie Mae includes significant expenses related to loan purchases. In 2024, Fannie Mae provided $381 billion in liquidity across mortgage markets. This involved acquiring roughly 778,000 single-family purchase loans, totaling $326 billion. Approximately half of those were for first-time homebuyers, plus around 204,000 single-family refinances.

Operating Expenses

Operating expenses encompass general and administrative costs, such as salaries, technology, and infrastructure. In 2023, Fannie Mae's non-interest expenses remained stable at $9.8 billion. These expenses are crucial for supporting daily operations. Fannie Mae's net worth increased by 22% year-over-year, as reported recently.

Guarantee Fees

Guarantee fees are a significant cost for Fannie Mae, representing payments to investors who hold mortgage-backed securities. In 2024, these fees were the primary driver of $29.1 billion in revenue. This revenue was generated from its $4.1 trillion guaranty book of business. This model has been transforming for over a decade.

Credit Losses

Credit losses are a substantial expense for Fannie Mae, stemming from potential mortgage defaults. In Q4 2024, Freddie Mac reported a provision for credit losses of $0.1 billion, contrasting with a benefit of $0.5 billion in Q4 2023. This difference reflects changing economic conditions and borrower risk. The single-family benefit for credit losses was $938 million. These figures are crucial for assessing Fannie Mae's financial health.

- Provisions for potential losses on mortgage defaults are a significant cost.

- Freddie Mac's Q4 2024 credit loss provision was $0.1 billion.

- Q4 2023 showed a benefit for credit losses of $0.5 billion.

- Single-family benefit for credit losses was $938 million.

Regulatory Compliance

Fannie Mae's cost structure includes significant expenses for regulatory compliance, primarily due to the oversight of the Federal Housing Finance Agency (FHFA). These costs cover legal requirements and ongoing adherence to FHFA regulations. Servicers must implement new foreclosure and bankruptcy fee guidelines, as per Servicing Announcement SVC-2024-07, with immediate encouragement and mandatory compliance by April 1, 2025. These fees are available for issues active as of January 1, 2025.

- FHFA oversight and regulatory compliance

- Legal and compliance teams' salaries and operational costs

- Fees for foreclosure and bankruptcy processes

- Regular audits and reporting requirements

Understanding the Financials: Key Costs and Revenues

Fannie Mae's cost structure involves expenses for loan acquisitions, including the $326 billion spent on single-family purchase loans in 2024. Operating costs, like salaries and tech, were approximately $9.8 billion in 2023. Guarantee fees generated $29.1 billion in revenue in 2024, crucial to the model. Credit losses and regulatory compliance also affect the costs.

| Cost Category | Description | 2024 Data |

|---|---|---|

| Loan Purchases | Cost of acquiring mortgage loans. | $326B in single-family purchase loans |

| Operating Expenses | General and administrative costs. | $9.8B (2023) |

| Guarantee Fees | Payments to investors. | $29.1B in revenue |

Revenue Streams

Guarantee Fees

Guarantee fees are a key revenue stream for Fannie Mae, charged to lenders for guaranteeing mortgage-backed securities. In 2024, these fees generated $29.1 billion in revenues. This revenue is primarily from the $4.1 trillion guaranty book of business. This demonstrates the significant financial impact of these fees.

Investment Income

Investment income for Fannie Mae stems from its mortgage portfolio and other investments. In Q4 2024, net interest income hit $5.1 billion, a 6% year-over-year increase. This growth was largely due to portfolio expansion and reduced funding costs. Non-interest income in Q4 2024 reached $1.3 billion, significantly up from $0.6 billion in Q4 2023, boosted by net investment gains.

Loan Servicing Fees

Fannie Mae earns revenue through loan servicing fees. These fees are generated by managing mortgages, including collecting payments and handling defaults. The Servicing Announcement SVC-2024-07 from Fannie Mae outlined new allowable foreclosure and bankruptcy fees. The STAR Program rewards mortgage servicers. For example, in 2023, Fannie Mae's net revenue was $19.3 billion.

Credit Risk Transfer

Fannie Mae generates revenue by transferring credit risk to private investors through various programs. In 2024, this strategy helped manage risk effectively. Approximately 99% of Fannie Mae's multifamily guaranty book used lender loss-sharing agreements, while 31% was covered by a credit risk transfer transaction. The company is poised to adjust its CRT issuance in 2025.

- Revenue from transferring credit risk to private investors.

- 99% of the company's multifamily guaranty book was subject to lender loss-sharing agreements.

- 31% was covered by a multifamily credit risk transfer transaction.

- Fannie Mae will be dynamic in its approach to CRT issuance in 2025.

Technology Solutions

Fannie Mae generates revenue by offering technology solutions and services to lenders. These solutions, like Desktop Underwriter (DU) and Desktop Originator (DO), are integrated into platforms such as Encompass. They provide in-depth eligibility and credit risk assessments, contributing to Day 1 Certainty and streamlining processes. This enhances speed and simplicity for property value, income, asset, and employment verification.

- Technology solutions contribute to operational efficiency for lenders.

- DU and DO are key components of Fannie Mae's tech offerings.

- Day 1 Certainty reduces risk for lenders.

- These tech solutions streamline various verification processes.

Key Revenue Sources Unveiled!

Fannie Mae's revenue streams include guarantee fees, generating $29.1B in 2024. Investment income, like Q4 2024's $5.1B net interest income, is another key source. Loan servicing fees also contribute to the revenue. Transferring credit risk and tech solutions also create revenue.

| Revenue Stream | Details | 2024 Data |

|---|---|---|

| Guarantee Fees | Fees from guaranteeing mortgage-backed securities. | $29.1 billion |

| Investment Income | Net interest and non-interest income from investments. | Q4 Net Interest Income: $5.1B |

| Loan Servicing Fees | Fees from managing mortgages. | STAR Program Rewards |

Business Model Canvas Data Sources

This Fannie Mae Business Model Canvas utilizes company filings, market reports, and industry analysis to inform its strategic blocks. These resources ensure accuracy and strategic relevance.