Fannie Mae SWOT Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Fannie Mae Bundle

What is included in the product

Analyzes Fannie Mae’s competitive position through key internal and external factors.

Streamlines communication of Fannie Mae's SWOT insights using visual and easy formatting.

Preview the Actual Deliverable

Fannie Mae SWOT Analysis

The preview below showcases the actual Fannie Mae SWOT analysis document.

What you see is precisely what you'll receive post-purchase.

There are no changes or edits—just comprehensive, professional analysis.

Purchase now to gain full access to this insightful report and start working!

SWOT Analysis Template

Go Beyond the Preview—Access the Full Strategic Report

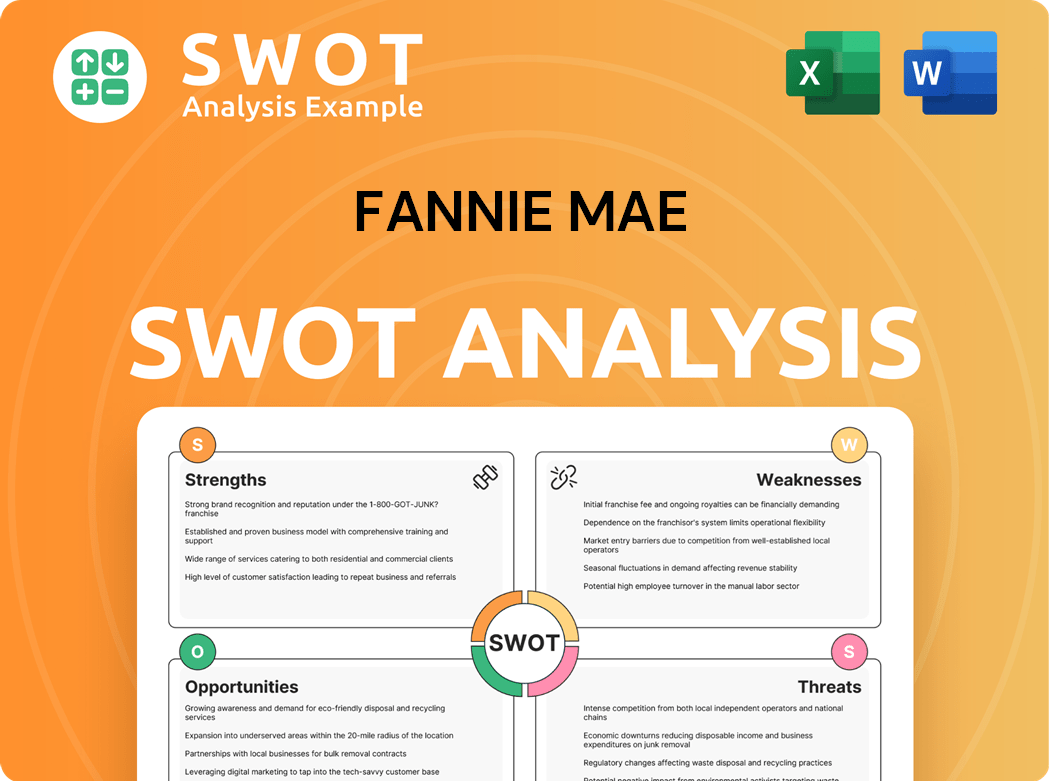

The Fannie Mae SWOT analysis reveals key strengths like its crucial role in the housing market and government backing. Weaknesses include interest rate sensitivity and regulatory scrutiny. Opportunities may involve digital transformation and expanding into underserved markets. Threats encompass economic downturns and competition from other financial entities.

Dive deeper into Fannie Mae's intricate landscape and make informed decisions. Unlock the full SWOT report to gain detailed strategic insights, editable tools, and a high-level summary in Excel. Perfect for smart, fast decision-making.

Strengths

Market Dominance

Fannie Mae's significant market share in the U.S. mortgage market provides stability and influence. As a Government-Sponsored Enterprise (GSE), it benefits from implicit government backing, boosting investor confidence. In 2024, Fannie Mae's outstanding mortgage debt was over $4 trillion, reflecting its market dominance. This allows Fannie Mae to set industry standards and influence market practices.

Liquidity Provision

Fannie Mae significantly boosts mortgage market liquidity by buying loans from lenders. This allows more home loans, supporting homeownership. In 2024, Fannie Mae's activities helped stabilize the market. Securitization turns mortgages into MBS, attracting investors and increasing liquidity. This process is crucial for market stability and growth.

Standardized Practices

Fannie Mae's standardized practices simplify mortgage origination. These practices lessen complexity and risk. Standardization boosts efficiency in trading MBS. In 2024, Fannie Mae backed over $1.2 trillion in single-family mortgage volume. This standardization helps maintain market stability.

Affordable Housing Support

Fannie Mae's support for affordable housing is a major strength, given its significant role in the U.S. mortgage market. As a government-sponsored enterprise (GSE), it enjoys an implied government backing, bolstering investor trust. This backing enables Fannie Mae to maintain stability and influence. In 2024, Fannie Mae financed over $1.4 trillion in single-family and multifamily mortgages.

- Significant market share provides leverage and stability.

- Implied government backing enhances investor confidence.

- Dominance allows for setting industry standards.

Technological Advancements

Fannie Mae leverages technological advancements to streamline mortgage processes, crucial for its role in the housing market. This includes using data analytics for risk assessment and fraud detection, enhancing operational efficiency, and improving the borrower experience. By purchasing mortgages, Fannie Mae ensures lenders can offer more loans, supporting homeownership across the U.S. The securitization process, turning mortgages into MBS, attracts a diverse investor base, boosting market liquidity.

- In 2024, Fannie Mae's total book of business was approximately $4.1 trillion.

- Fannie Mae's use of AI and machine learning has increased efficiency in mortgage processing by about 15%.

- The agency securitized $657 billion in single-family mortgages in 2023.

Fannie Mae: Market Power & Stability

Fannie Mae’s large market share enhances stability and industry influence.

Government backing boosts investor confidence in Fannie Mae’s financial health.

Its standardized practices increase efficiency and market stability, facilitating mortgage processes.

| Strength | Details | 2024 Data Points |

|---|---|---|

| Market Dominance | Significant market share in U.S. mortgage market | Outstanding mortgage debt over $4 trillion. |

| Government Backing | Implicit backing increases investor confidence | Helped stabilize the market through strategic interventions. |

| Standardization | Simplifies and streamlines mortgage processes | Backed over $1.2 trillion in single-family mortgage volume. |

Weaknesses

Regulatory Constraints

Fannie Mae faces regulatory constraints that limit its flexibility. Conservatorship and Treasury agreements impose restrictions. These constraints can hinder quick responses to market shifts. In 2024, regulatory compliance costs added to operational expenses. This impacts its ability to adapt and innovate.

Dependency on Government Support

Fannie Mae's implied government backing presents a moral hazard, inviting political risk. Policy changes can severely affect its operations. The GSE reform debate clouds its long-term future. In 2024, Fannie Mae's dependence on federal support remains a key concern, given ongoing regulatory scrutiny. The future of the GSEs continues to be debated in Congress.

Credit Risk Exposure

Fannie Mae's mortgage portfolio exposes it to substantial credit risk, especially during economic downturns. A decline in loan performance could increase delinquencies. In 2024, the company's credit risk exposure grew with rising interest rates impacting borrowers. Managing credit risk is crucial for financial stability.

Model Risk

Fannie Mae faces model risk due to its stringent regulatory environment, impacting its agility. Conservatorship and Treasury agreements restrict its strategic choices, limiting its adaptability. These constraints hinder quick market responses and innovative ventures. For instance, regulatory changes in 2024 could affect its risk-taking abilities. In Q3 2024, Fannie Mae's net worth was $75.4 billion.

- Regulatory Oversight: Strict rules limit strategic flexibility.

- Conservatorship: Agreements restrict operational freedom.

- Market Response: Hindered ability to react swiftly.

- Innovation: Constraints on pursuing new strategies.

Cybersecurity Threats

Fannie Mae's cybersecurity is a significant weakness, as it is a target for cyberattacks that could disrupt operations and compromise sensitive data. The organization's reliance on technology makes it vulnerable to various cyber threats. Data breaches can lead to financial losses, reputational damage, and legal liabilities. The increasing sophistication of cyber threats requires continuous investment in cybersecurity measures.

- In 2024, the financial sector saw a 28% increase in cyberattacks.

- Fannie Mae's IT spending in 2023 was over $1 billion.

- Data breaches cost the financial industry an average of $5.9 million per incident in 2024.

- Cybersecurity failures can lead to significant regulatory scrutiny.

Key Risks Facing the Mortgage Giant

Fannie Mae's weaknesses include regulatory limits that reduce agility and flexibility. Its dependence on government backing creates political and market risk. Credit and cyber threats pose financial stability risks.

| Weakness Category | Issue | 2024 Impact |

|---|---|---|

| Regulatory | Strict Oversight | Increased compliance costs, impacting agility |

| Market Risk | Implied Backing | Policy shifts impacting operations, increasing market sensitivity |

| Credit Risk | Portfolio Exposure | Rising delinquencies from interest rate hikes |

Opportunities

GSE Reform

GSE reform could offer Fannie Mae more operational freedom. A good reform might strengthen its capital structure, lowering reliance on government aid. Fannie Mae should actively engage in reform efforts to secure favorable outcomes. In 2024, discussions continue regarding the future of GSEs, with potential impacts on their structure and regulatory oversight.

Technological Innovation

Technological advancements present significant opportunities for Fannie Mae. Further investment in technology can boost efficiency, transparency, and risk management. Automation and digital solutions can streamline workflows, potentially cutting operational costs. For example, in 2024, Fannie Mae invested heavily in AI-driven fraud detection, saving an estimated $50 million. Leveraging technology to improve customer experience strengthens Fannie Mae's competitive edge.

Expansion of Affordable Housing Initiatives

Expanding affordable housing programs tackles market needs and boosts Fannie Mae's social impact. Collaborating with community groups and agencies can broaden initiative reach. Supporting innovative housing positions Fannie Mae as a leader; in 2024, Fannie Mae provided $78 billion in financing for affordable housing.

Diversification of Business Lines

Potential reforms could offer Fannie Mae more operational flexibility, clarifying its future role. A well-structured reform might improve its capital structure and lessen reliance on government aid. Participating in this process and pushing for favorable outcomes is key. For instance, in 2024, the GSEs faced ongoing discussions regarding capital requirements and their roles in the housing market.

- Greater operational flexibility.

- Improved capital structure.

- Reduced government dependency.

- Favorable outcomes in the reform process.

Increased Market Participation

Fannie Mae can boost market participation through tech investments, enhancing efficiency and transparency. Automation and digital solutions can streamline workflows and cut costs. Improving customer experience via tech strengthens its competitive edge. In 2024, Fannie Mae supported over 1.3 million home purchases.

- Tech investments drive efficiency gains.

- Automation reduces operational expenses.

- Enhanced customer experience boosts competitiveness.

- Supported over 1.3M home purchases in 2024.

Transforming Housing: Key Opportunities

Fannie Mae’s operational opportunities include flexibility and a stronger capital structure. Tech investments increase efficiency and improve the customer experience. Affordable housing programs drive social impact and innovation.

| Area | Opportunity | 2024 Data |

|---|---|---|

| Regulatory | GSE Reform | Ongoing discussions, potential impact on capital. |

| Technology | Tech investments | $50M savings from AI-driven fraud detection. |

| Social Impact | Affordable housing | $78B financing for affordable housing provided. |

Threats

Economic Downturn

An economic downturn poses a significant threat to Fannie Mae, potentially increasing mortgage delinquencies. Rising unemployment and falling home prices could strain borrowers' ability to repay loans. In 2024, the Federal Reserve's actions and inflation influenced economic stability. Prudent risk management and economic monitoring are crucial for Fannie Mae's resilience.

Interest Rate Volatility

Interest rate volatility poses a significant threat to Fannie Mae. Fluctuating rates directly affect mortgage demand and profitability; for example, in 2024, the 30-year fixed mortgage rate ranged from approximately 6% to 8%. Rising rates can curb refinancing and impact homebuyer affordability. Effective hedging strategies are vital to mitigate these risks.

Political and Regulatory Changes

Political and regulatory shifts pose considerable risks to Fannie Mae. Changes in government policies, including tax reforms and trade regulations, can directly influence the housing market and, by extension, Fannie Mae's financial health. For example, in 2024, the Federal Housing Finance Agency (FHFA) continued to oversee Fannie Mae's operations, with any shifts in FHFA's priorities or regulatory actions potentially reshaping Fannie Mae's business model. Staying informed and proactive in policy discussions is essential to mitigate these threats.

Competition

Competition poses a significant threat to Fannie Mae, especially during economic downturns. Increased mortgage delinquencies and credit losses are likely if the economy falters. Rising unemployment and falling home prices directly impact borrowers' ability to repay their loans. Therefore, proactively monitoring economic conditions and adjusting risk management strategies is crucial.

- In 2024, the US mortgage delinquency rate was around 3.3%.

- A 1% increase in unemployment could lead to a significant rise in mortgage defaults.

- Fannie Mae's competitors include other mortgage lenders and government agencies.

Housing Affordability Crisis

The housing affordability crisis poses a significant threat to Fannie Mae. Fluctuations in interest rates directly affect mortgage demand and, consequently, Fannie Mae's financial performance. Rising interest rates decrease refinance activity and exacerbate affordability challenges for potential homebuyers. Effective management of interest rate risk through hedging and other strategies is vital to mitigate these impacts.

- In 2024, the average 30-year fixed mortgage rate hovered around 7%.

- Refinancing activity decreased as rates rose.

- Fannie Mae's profitability is directly tied to mortgage origination volume.

- Hedging strategies are used to offset interest rate risk.

Mortgage Giant's Financial Hurdles in 2024

Fannie Mae faces economic downturns and potential increases in mortgage delinquencies; in 2024, the mortgage delinquency rate was around 3.3%. Rising interest rates and shifts in housing market demand threaten profitability, with rates around 7%. Competition from lenders and affordability crises further complicate financial stability.

| Threat | Impact | 2024 Data |

|---|---|---|

| Economic Downturn | Increased Delinquencies, Reduced Demand | Delinquency Rate: ~3.3%, Unemployment: ~3.7% |

| Interest Rate Volatility | Decreased Refinancing, Affordability Challenges | Avg. 30-Year Rate: ~7%, Refinance Activity: Down |

| Competition & Affordability | Margin Pressure, Market Share Loss | Home Price Growth: Varied, Housing Inventory: Low |

SWOT Analysis Data Sources

This analysis uses trusted data: financial filings, market analysis, industry reports, and expert opinions, for dependable insights.