Ferrovial Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Ferrovial Bundle

What is included in the product

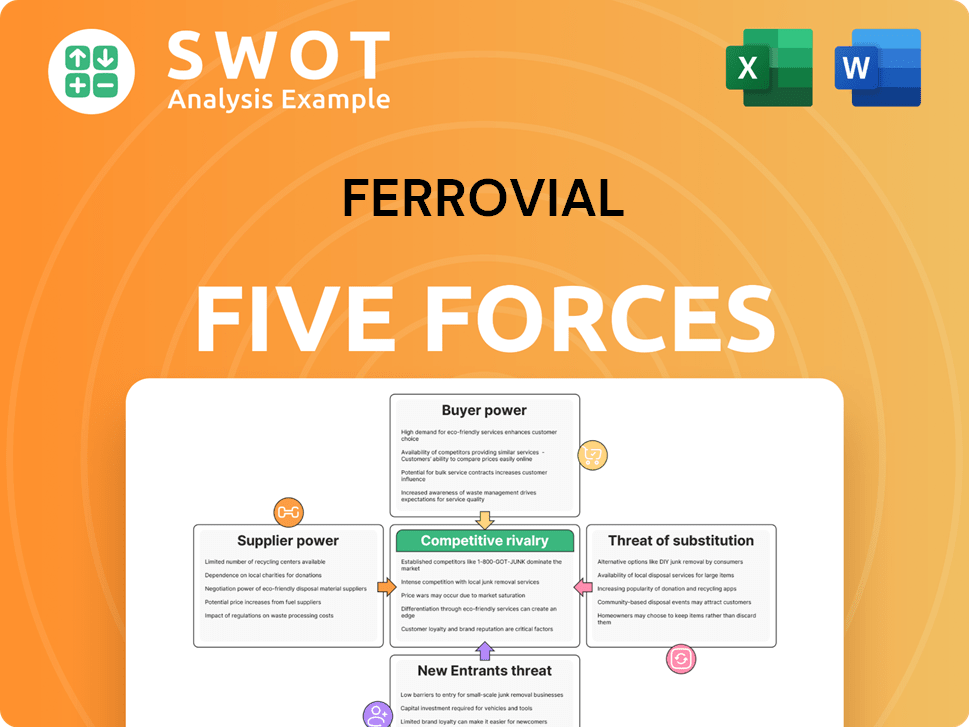

Analyzes the competitive forces shaping Ferrovial's market position, examining suppliers, buyers, and rivals.

Quickly visualize Porter's Five Forces with an intuitive radar chart, showing strategic pressures.

Preview the Actual Deliverable

Ferrovial Porter's Five Forces Analysis

This preview showcases the complete Ferrovial Porter's Five Forces analysis you'll receive. It details competitive rivalry, supplier power, buyer power, threat of substitutes, and threat of new entrants. The analysis is fully formatted and ready for your immediate use. No need for further preparation; it's the final document. You get instant access after purchase.

Porter's Five Forces Analysis Template

Go Beyond the Preview—Access the Full Strategic Report

Analyzing Ferrovial's competitive landscape using Porter's Five Forces reveals critical insights. Bargaining power of suppliers and buyers significantly shapes profitability. The threat of new entrants and substitute products adds further competitive pressure. Understanding industry rivalry is also crucial for strategic decisions.

This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Ferrovial.

Suppliers Bargaining Power

Supplier Concentration

Ferrovial's suppliers possess moderate bargaining power. Supplier concentration can affect pricing and terms. However, Ferrovial's scale offers some negotiation advantages. Suppliers include raw material providers and specialized equipment manufacturers. In 2024, Ferrovial's revenue was approximately EUR 8.6 billion, giving it leverage.

Switching Costs

Switching costs for Ferrovial are moderate. Changing suppliers incurs costs, especially for specialized equipment or long-term contracts. However, strategic sourcing and supplier diversification help mitigate these costs. This gives Ferrovial flexibility. In 2024, Ferrovial's infrastructure backlog reached €30.8 billion.

Supplier Forward Integration

The threat of supplier forward integration for Ferrovial is low to moderate. Suppliers, like material providers, might consider moving into construction, but it's complex. Ferrovial's integrated model helps mitigate this risk. In 2023, Ferrovial's construction backlog was €11.6 billion, showing its strength.

Input Differentiation

Input differentiation for Ferrovial is moderate. Some inputs are standard commodities, while others, like specialized engineering or tech, are unique. This differentiation impacts supplier power, yet Ferrovial's diverse abilities help manage this. For example, in 2024, Ferrovial's infrastructure projects used both readily available materials and specialized components. The company strategically balances its sourcing.

- Commodity inputs include materials like steel and cement.

- Differentiated inputs include proprietary technology.

- Ferrovial's varied projects give it sourcing leverage.

- In 2024, Ferrovial's revenue was 8.5 billion euros.

Impact of Inputs on Cost

The impact of supplier inputs on Ferrovial's cost structure is substantial. Raw materials, equipment, and subcontracted services are a significant part of project costs, influencing profitability and pricing. Effective supplier management is key to controlling costs. Ferrovial's efficiency and innovation efforts help mitigate this impact.

- In 2024, Ferrovial's construction division faced increased material costs, impacting project margins.

- Supplier negotiations and strategic sourcing strategies helped offset some cost increases.

- The company invested in technology to enhance supply chain efficiency.

- Subcontractor expenses accounted for approximately 30% of total project costs.

Supplier Dynamics: Power & Impact

Ferrovial's suppliers hold moderate power, affected by concentration. Switching costs are manageable, given strategic sourcing. Forward integration threat is low, thanks to its integrated model. Input differentiation impacts supplier power.

| Factor | Impact | Details |

|---|---|---|

| Supplier Concentration | Moderate | Raw materials vs. specialized inputs affect pricing. |

| Switching Costs | Moderate | Strategic sourcing and diversification ease changes. |

| Forward Integration | Low to Moderate | Ferrovial's model mitigates risks from suppliers. |

Customers Bargaining Power

Customer Concentration

Customer concentration for Ferrovial is generally low to moderate. The company serves various clients, including governments and private developers. Although individual projects can be substantial, Ferrovial's portfolio diversification mitigates reliance on any single client. This diversity enhances its stability and bargaining leverage. In 2024, Ferrovial's revenue reached €8.5 billion, with a broad client base across different geographies and project types.

Switching Costs for Customers

Switching costs for Ferrovial's customers are substantial due to the long-term and intricate nature of infrastructure projects. Customers face significant financial and operational hurdles to change contractors once a project is underway. This setup reduces customer bargaining power, providing Ferrovial with a more stable project environment. The high cost of switching is reflected in the industry's low attrition rates, with projects often spanning years. For example, Ferrovial's 2024 annual report shows a high rate of project continuation due to these factors.

Customer Information

Customer information is high for Ferrovial's projects, particularly with government and large developers. These clients often have access to various competitors. This informed customer base demands competitive pricing and innovative solutions, adding pressure to Ferrovial. To secure contracts, Ferrovial must showcase its value and expertise effectively.

Price Sensitivity

Price sensitivity among Ferrovial's customers is notably high. Large infrastructure projects involve significant capital, making clients acutely aware of pricing. Ferrovial must balance competitive pricing with profitability and quality. This necessitates careful cost management and value engineering strategies. In 2024, Ferrovial's revenue was approximately EUR 8.6 billion, highlighting the scale of its projects and the importance of managing customer expectations.

- High project costs increase customer price sensitivity.

- Ferrovial must balance pricing with profitability and quality.

- Cost management and value engineering are crucial.

- 2024 revenue was around EUR 8.6 billion.

Customer Ability to Backward Integrate

The ability of customers to backward integrate is low, meaning they're unlikely to design, construct, and operate large-scale infrastructure projects. This limits customer power, giving Ferrovial an advantage. Most customers lack the specialized expertise and resources required for such complex undertakings. For example, in 2024, infrastructure projects often involve intricate engineering and financial modeling skills. This keeps customer bargaining power in check.

- Limited customer ability to independently handle complex infrastructure projects.

- Customers typically lack the internal expertise for design, construction, and operation.

- This provides Ferrovial with a strong competitive position.

- The trend continues in 2024, with specialized skills remaining crucial.

Analyzing Customer Power Dynamics

Customer bargaining power for Ferrovial is moderate, influenced by project specifics. Switching costs are high due to the nature of infrastructure projects, reducing customer leverage. However, informed customers and price sensitivity necessitate competitive offerings. In 2024, revenue was around EUR 8.6 billion, highlighting project scale.

| Factor | Impact | Data |

|---|---|---|

| Customer Concentration | Low to Moderate | Diversified client base |

| Switching Costs | High | Long-term projects |

| Customer Info | High | Access to competitors |

| Price Sensitivity | High | Large project capital |

| Backward Integration | Low | Specialized expertise needed |

Rivalry Among Competitors

Number of Competitors

Ferrovial operates in a highly competitive infrastructure market, facing many rivals. The presence of numerous global and regional players, such as ACS and Skanska, increases competition. This intense rivalry puts pressure on pricing strategies. For instance, in 2024, the infrastructure sector saw a 5% decrease in profit margins due to stiff competition.

Industry Growth Rate

Ferrovial operates in an industry with a moderate growth rate. Infrastructure spending is rising, yet growth varies by region and sector. For instance, the global construction market was valued at $15.2 trillion in 2023, with a projected CAGR of 4.8% from 2024 to 2030. This moderate growth intensifies competition among firms.

Product Differentiation

Product differentiation in Ferrovial's sector is moderate. Basic construction and engineering services see limited differentiation. Innovation, sustainability, and project management expertise offer a competitive edge. Ferrovial invests in innovation, aiming to stand out. In 2024, Ferrovial's revenue was €8.6 billion.

Switching Costs for Projects

Switching costs are a significant factor in Ferrovial's project landscape. Changing contractors mid-project is expensive and can cause delays, reducing competitive pressure after a contract is secured. This situation offers stability to Ferrovial, but demands excellent project execution. For instance, in 2024, project delays due to contractor changes cost the construction industry an estimated $150 billion globally. It is difficult to switch the contractor once the project has begun.

- High costs associated with contractor changes deter switching.

- Delays and disruptions increase project expenses.

- Stability for Ferrovial, but requires strong performance.

- Changing contractors mid-project is challenging.

Exit Barriers

Exit barriers for Ferrovial are moderate. Leaving specific projects can be tricky due to contracts, but the infrastructure industry as a whole is easier to exit. This dynamic fuels competition, as struggling firms may not stick around. Ferrovial's diverse holdings cushion the blow of individual project issues.

- Ferrovial's 2023 revenue: €8.5 billion, showing financial resilience.

- Infrastructure projects often involve long-term contracts, impacting exit timing.

- The company's diversified portfolio spreads risk across various projects.

- Competitive pressures are sustained by the possibility of firms exiting the market.

Ferrovial's Market: Intense Rivalry & Margin Squeeze

Competitive rivalry in Ferrovial's market is high, with many competitors like ACS and Skanska. This rivalry impacts pricing and profit margins. In 2024, profit margins in the infrastructure sector decreased by 5% due to intense competition. Ferrovial’s focus on innovation and project management helps it stand out.

| Factor | Impact on Ferrovial | 2024 Data |

|---|---|---|

| Competition Level | High | 5% decrease in profit margins |

| Key Competitors | ACS, Skanska | - |

| Differentiation | Moderate | €8.6 billion revenue |

SSubstitutes Threaten

Substitute Availability

The threat of substitutes for Ferrovial's infrastructure projects is generally low to moderate. Direct replacements are scarce, but alternatives like smaller projects or different transport modes exist. Technological progress could introduce new substitutes over time. Ferrovial's revenue in 2024 was approximately €8.5 billion, demonstrating its market position despite potential substitutes.

Relative Price Performance

The relative price performance of substitutes for Ferrovial's services is moderate. Alternative options can provide cost savings. However, they often lack the scale of Ferrovial's projects. For example, in 2024, the cost of renewable energy projects, a substitute for some infrastructure, varied widely, but Ferrovial must highlight its long-term value. Ferrovial must demonstrate the value of its solutions.

Switching Costs for Customers

Switching costs to substitutes for Ferrovial are moderate. Implementing alternative solutions may require initial investment and planning changes, yet the long-term advantages could surpass these costs. This prompts Ferrovial to focus on innovation and providing strong value propositions to retain customers. For example, in 2024, Ferrovial's infrastructure projects faced competition from alternative transport solutions. Customers consider long-term benefits.

Customer Propensity to Substitute

Customer propensity to substitute is moderate, particularly in infrastructure projects. Governments and developers might consider alternatives if they offer cost savings or environmental advantages. Ferrovial must proactively address these concerns, emphasizing its project benefits. There's a moderate openness to alternatives, influencing project decisions. In 2024, the infrastructure sector saw a shift, with about 15% of projects exploring green alternatives.

- Moderate Substitution Risk

- Cost and Benefit Considerations

- Proactive Strategy is Key

- Green Alternatives Influence

Technological Disruption

Technological disruption poses a rising threat to Ferrovial. Innovations like 3D printing and autonomous vehicles could revolutionize infrastructure, creating substitutes. Ferrovial must invest in innovation and adapt to stay competitive. Keeping up with tech is crucial for Ferrovial's future.

- 3D printing market is projected to reach $55.8 billion by 2027.

- Autonomous vehicles market is expected to reach $65.3 billion by 2026.

- Ferrovial's R&D spending in 2023 was €45 million.

- Modular construction market is growing at 10% annually.

Ferrovial's Substitute Risk: A Balanced View

The threat of substitutes for Ferrovial is moderate due to limited direct replacements, but alternative transport modes and smaller projects exist. Price performance of substitutes is moderate with cost-saving potential, and switching costs are also moderate, prompting Ferrovial to emphasize value. Customer propensity to substitute is moderate, especially with green alternatives influencing infrastructure decisions.

| Factor | Impact | 2024 Data |

|---|---|---|

| Substitution Risk | Moderate | 15% of projects explored green alternatives. |

| Price Performance | Moderate | Renewable energy costs varied. |

| Switching Costs | Moderate | Initial investment for alternatives. |

Entrants Threaten

Barriers to Entry: Capital Requirements

The threat of new entrants is moderate due to high capital requirements. Infrastructure projects like those Ferrovial undertakes demand substantial upfront investment in equipment, technology, and skilled personnel, with costs potentially reaching billions of dollars. Ferrovial's strong financial position, including a revenue of €8.5 billion in 2024, provides a significant advantage. Entering the infrastructure market is undeniably expensive, creating a barrier for smaller firms.

Barriers to Entry: Regulatory Hurdles

Regulatory hurdles are significant in the infrastructure industry. New entrants face complex permit requirements and environmental approvals. Compliance with local laws is also essential, posing challenges. Ferrovial's established regulatory expertise offers a considerable advantage. The infrastructure sector saw roughly $1.5 trillion in global investments in 2024, highlighting the scale of regulatory complexity.

Barriers to Entry: Economies of Scale

Economies of scale are significant in Ferrovial's industry, providing a barrier to entry. Established firms benefit from procurement advantages, project management efficiencies, and access to financing. These advantages, like the €1.7 billion revenue in Construction in 2023, make it hard for new entrants. Established players have a clear competitive edge.

Barriers to Entry: Brand Recognition

Brand recognition is a significant barrier for new entrants in the infrastructure sector. Customers typically favor established companies like Ferrovial, which have a history of successful project delivery. Ferrovial's brand strength offers a competitive edge. A strong reputation is key to winning contracts and building trust. In 2024, Ferrovial's brand value was estimated at over €2.5 billion, reflecting its market position.

- Brand Reputation: Ferrovial's strong reputation is a major advantage.

- Customer Preference: Clients often choose proven companies.

- Competitive Edge: Brand recognition provides a significant barrier.

- Financial Impact: Ferrovial's brand value supports its market position.

Access to Technology and Expertise

The threat from new entrants in the infrastructure sector is often limited by the need for advanced technology and specialized expertise. Infrastructure projects demand substantial technical know-how and specific skills, creating a significant hurdle for newcomers. Ferrovial, with its investments in innovation and its experienced team, has established a strong barrier to entry. However, continual innovation is crucial for Ferrovial to maintain its competitive edge.

- Specialized Knowledge: Infrastructure projects need specific expertise.

- Technical Barriers: New entrants face challenges in acquiring necessary expertise.

- Ferrovial's Advantage: Investments in innovation and workforce give it an edge.

- Ongoing Innovation: Ferrovial must keep innovating to stay ahead.

Barriers to Entry: The Industry's Challenges

New entrants face significant hurdles. High capital needs, like billions of euros for projects, and regulatory complexity create barriers. Ferrovial's €8.5B 2024 revenue shows its advantage, along with strong brand recognition. The industry's technological demands and specialized expertise also limit new entries.

| Factor | Impact on New Entrants | Ferrovial's Advantage |

|---|---|---|

| Capital Requirements | High upfront investment | Strong financial position |

| Regulatory Hurdles | Complex permits and approvals | Established regulatory expertise |

| Economies of Scale | Difficult to compete | Procurement and management efficiency |

Porter's Five Forces Analysis Data Sources

Ferrovial's Five Forces analysis utilizes financial reports, industry analyses, and market data to assess competitiveness. These sources include company filings, economic indicators, and consulting reports.