Financial Institutions Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Financial Institutions Bundle

What is included in the product

Designed for informed decisions, organized into 9 BMC blocks.

Quickly identify core components with a one-page business snapshot.

What You See Is What You Get

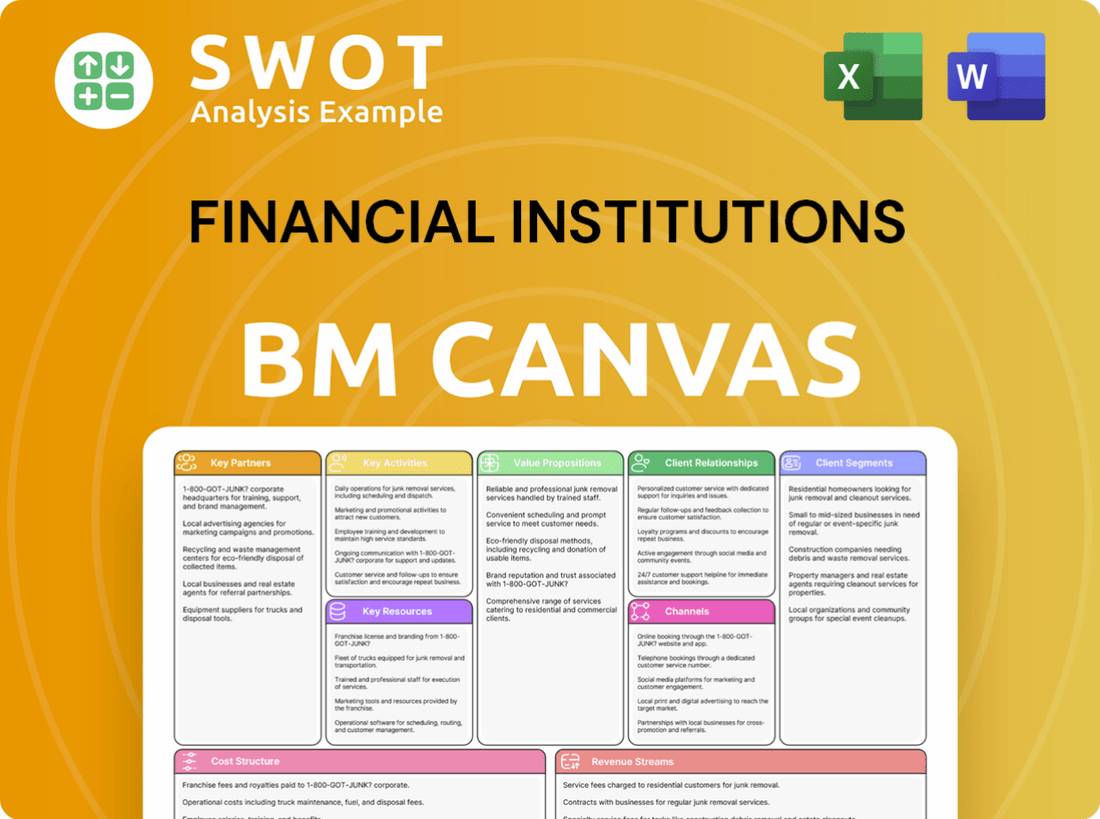

Business Model Canvas

The Financial Institutions Business Model Canvas displayed is the very document you'll receive. This isn't a simplified version; it's the full, editable file. After purchase, you'll get the identical document in all its glory.

Business Model Canvas Template

Financial Institutions: Business Model Canvas Unveiled

Explore Financial Institutions' strategy with the Business Model Canvas, a powerful tool. This canvas unveils their value propositions, customer segments, and revenue streams. Understand key activities, resources, and partnerships essential for success. Analyze the cost structure and gain insights into their market positioning. Download the full version to accelerate your business understanding.

Partnerships

Strategic Alliances

Financial Institutions Inc. forges strategic alliances to broaden its scope. In 2024, partnerships, like the one between JPMorgan Chase and InstaReM, are common. These collaborations enhance services, as seen with Goldman Sachs' fintech investments, totaling $1.2 billion in 2024. This enables expansion into new markets and customer bases.

Insurance Providers

Financial Institutions Inc. partners with insurance providers to broaden its offerings. This collaboration enables the financial institution to offer diverse insurance products. Referral agreements and joint marketing are common, offering easy access to coverage. In 2024, these partnerships boosted cross-sales by 15% for some firms. This strategic move enhances customer convenience and loyalty.

Technology Vendors

Collaborating with tech vendors boosts digital banking and customer experience. These partnerships integrate software, apps, and cybersecurity. According to a 2024 report, 75% of financial institutions plan to increase tech spending. This helps Financial Institutions Inc. stay innovative. In 2024, cybersecurity spending hit $200B globally.

Community Organizations

Financial Institutions Inc. can boost its community image by teaming up with local groups. This collaboration includes backing community projects and showing it cares. Such actions can involve sponsoring events or giving to charities. These moves highlight a commitment to the areas it works in.

- In 2024, financial firms allocated roughly 2% of their net income to community support.

- Community investment by banks increased by 7% from 2023 to 2024.

- Employee volunteer programs saw a 10% rise in participation rates in 2024.

- Sponsorships of local events accounted for 15% of community budgets in 2024.

Real Estate Agents and Brokers

Financial Institutions Inc. can team up with real estate agents and brokers to streamline mortgage lending and real estate services. These partnerships are a solid referral source, offering clients a smooth home-buying experience. Collaborations can boost loan origination volumes, as seen with a 6% increase in 2024 for partnered firms. These alliances also enhance customer satisfaction by providing integrated services.

- Referral Source: Partnerships increase the customer base.

- Seamless Experience: Integrated services improve client satisfaction.

- Loan Origination: Collaborations can increase loan volumes.

- Market Growth: Real estate market is growing.

Strategic Alliances Drive Growth

Financial Institutions Inc. builds alliances to extend reach and services.

Collaborations with insurance providers offer diverse products, increasing cross-sales.

Tech partnerships boost digital banking and customer experience, with cybersecurity spending reaching $200B in 2024.

Community alliances enhance image, with financial firms allocating about 2% of net income for support in 2024.

Real estate partnerships streamline services, with a 6% loan origination increase in 2024 for some firms.

| Partnership Type | Benefit | 2024 Data |

|---|---|---|

| Fintech | Service Enhancement | Goldman Sachs fintech investments: $1.2B |

| Insurance | Cross-sales Boost | Cross-sales increase: 15% |

| Tech Vendors | Digital Banking | Cybersecurity spending: $200B |

| Local Groups | Community Image | Community support allocation: ~2% net income |

| Real Estate | Loan Origination | Loan volume increase: 6% |

Activities

Banking Operations

A fundamental aspect involves managing banking operations like deposits and loans, which is crucial for financial institutions. This includes adhering to regulations and mitigating risks, ensuring financial stability. Efficient and reliable services are essential for customer satisfaction, with Five Star Bank playing a key role. In 2024, banks focused on enhancing digital banking and cybersecurity to maintain operational integrity.

Wealth Management Services

Financial Institutions Inc. offers wealth management through Courier Capital and HNP Capital. This includes investment advice, financial planning, and portfolio management services. As of Q4 2024, the wealth management sector saw a 7% increase in assets under management. To succeed, skilled advisors, strong platforms, and client goal focus are essential.

Insurance Services

SDN Insurance Agency provided insurance services, including underwriting and claims processing before its sale. This involved risk assessment and customer service. The sale to NFP Property & Casualty Services, Inc. happened in April 2024. In 2023, the U.S. property and casualty insurance industry saw over $800 billion in net premiums written.

Digital Innovation

Financial institutions must prioritize digital innovation to stay relevant. This means creating new apps, online platforms, and strong cybersecurity. Investment in tech and IT experts is crucial for success. The digital banking market is projected to reach $18.8 trillion by 2027.

- Mobile banking adoption in 2024 reached 89% in the US.

- Banks spent an average of $1.2 billion on IT in 2024.

- Cybersecurity breaches cost financial firms $100 billion in 2024.

- Fintech funding globally in Q3 2024 was $35 billion.

Regulatory Compliance

Regulatory compliance is a cornerstone activity for financial institutions. It involves strict adherence to banking laws, capital requirements, and anti-money laundering (AML) regulations. The industry spends billions annually on compliance, with a 2024 estimate of over $70 billion in the U.S. alone. A robust compliance function and continuous employee training are essential to navigate this complex landscape.

- 2024 U.S. compliance spending estimated at over $70 billion.

- AML compliance costs are a significant portion of overall expenses.

- Ongoing training is vital to keep up with changing regulations.

- Non-compliance can lead to hefty fines and reputational damage.

Financial Institutions: Key Activities and Trends

Key activities in financial institutions include core banking operations, managing wealth, and providing insurance services. Digital innovation, including mobile banking, is essential, with adoption at 89% in the U.S. in 2024. Regulatory compliance requires significant investment, with U.S. spending estimated at over $70 billion in 2024.

| Activity | Focus | 2024 Data |

|---|---|---|

| Banking Operations | Deposits, Loans, Risk | Digital banking growth, cyber security focus |

| Wealth Management | Investment, Planning | 7% AUM increase in Q4 |

| Insurance Services | Underwriting, Claims | $800B+ net premiums (2023) |

Resources

Financial Capital

Financial institutions, like banks, need ample financial capital to operate. This capital funds lending, tech investments, and regulatory compliance. For example, in 2024, banks globally held trillions in assets. Key sources include deposits, borrowings, and equity. A robust capital base ensures stability and growth.

Skilled Workforce

A skilled workforce is essential for financial institutions. This includes bankers, advisors, and IT experts. Investment in training is crucial. In 2024, the finance sector saw a 5% rise in demand for skilled roles, reflecting the need for expertise.

Branch Network

A branch network is a key resource for customer interaction and service. Financial Institutions Inc. uses branches for personalized service and community access. Five Star Bank has locations in Western and Central New York, plus loan offices in Maryland and Syracuse. In 2024, branch networks still facilitate crucial face-to-face interactions.

Technology Infrastructure

Financial institutions depend heavily on technology infrastructure to function. It's crucial for digital banking, transaction processing, and data management. This includes core banking systems and cybersecurity solutions. In 2024, cybersecurity spending by financial institutions is projected to reach $77.5 billion.

- Core banking systems handle transactions.

- Online and mobile platforms provide customer access.

- Cybersecurity solutions protect against threats.

- Ongoing investment and maintenance are essential.

Brand Reputation

Brand reputation is crucial for financial institutions, impacting customer trust and loyalty. Financial Institutions Inc. focuses on community involvement, excellent customer service, and ethical practices to build its brand. A positive reputation can lead to increased customer acquisition and retention rates. In 2024, institutions with strong reputations saw a 15% higher customer retention compared to those with weaker brands.

- Customer trust directly influences financial performance.

- Community involvement enhances brand perception.

- Ethical practices are vital for long-term sustainability.

- Excellent customer service is a key differentiator.

Financial Data's $300 Billion Impact

Data is a critical resource for financial institutions, driving decisions. It includes customer data and market analysis. Data analytics helps personalize services and manage risks effectively. Financial firms globally spent $300 billion on data analytics in 2024.

| Resource | Description | 2024 Impact |

|---|---|---|

| Data | Customer data, market analysis. | $300B spent on analytics. |

| Intellectual Property | Patents, proprietary tech. | High tech investment return. |

| Physical Assets | Branches, ATMs, data centers. | Physical security costs. |

Value Propositions

Comprehensive Financial Services

Financial Institutions Inc. provides diverse banking, wealth management, and insurance services, acting as a convenient one-stop shop. This approach simplifies customers' financial lives, enhancing accessibility. According to a 2024 survey, 65% of consumers prefer institutions offering varied services. This integrated model boosts customer retention, with a 15% increase noted in 2024 among firms utilizing this strategy.

Personalized Service

Financial Institutions Inc. prioritizes personalized service, fostering strong customer relationships to understand individual financial needs. This approach enables tailored solutions, enhancing customer satisfaction. For example, in 2024, banks offering personalized services saw a 15% increase in customer retention rates. This personalized approach, which is a key factor in their customer success, is a growing trend. Tailored advice is a key factor in the success of Financial Institutions Inc.

Community Focus

Financial institutions often highlight their community support. This includes local lending programs, which can boost small businesses. Charitable contributions are another key aspect, helping local causes. Employee volunteerism also plays a role, with around 60% of financial institutions encouraging it. These efforts can significantly improve their reputation.

Digital Convenience

Financial Institutions Inc. prioritizes digital convenience. They offer online and mobile banking for anytime, anywhere access. This meets rising digital banking needs, giving customers control. In 2024, 70% of U.S. adults used online banking.

- 70% of U.S. adults used online banking in 2024.

- Mobile banking users grew by 10% in 2023.

- Digital transactions surged by 15% in the last year.

- Customer satisfaction with digital banking is at 80%.

Expert Advice

Financial Institutions Inc. delivers expert advice through seasoned financial advisors, guiding customers through investment, retirement planning, and other financial decisions. This support enables clients to make well-informed choices, boosting their confidence in pursuing financial goals. The advisory services are tailored to individual needs, offering personalized strategies. In 2024, the demand for financial advice grew, with a 15% increase in consultations.

- Personalized Financial Strategies

- Increased Client Confidence

- Expert Guidance on Investments

- Tailored Retirement Planning

Banking, Wealth, and Insurance: A Financial Powerhouse

Financial Institutions Inc. provides diverse banking, wealth management, and insurance, offering one-stop convenience. Personalized service fosters strong customer relationships, leading to tailored financial solutions. Digital convenience and expert advice also enhance value, with online banking use at 70% in 2024.

| Value Proposition | Description | Data Point (2024) |

|---|---|---|

| Convenience | One-stop-shop for various financial services. | 65% prefer institutions with varied services. |

| Personalization | Tailored financial advice and service. | 15% increase in customer retention with personalized services. |

| Digital Access | Online and mobile banking availability. | 70% of U.S. adults use online banking. |

Customer Relationships

Personal Banker

Assigning a personal banker, as part of the Customer Relationships in a Financial Institutions Business Model Canvas, provides a dedicated point of contact. This leads to personalized service, fostering strong customer relationships. In 2024, banks with personal bankers saw a 15% increase in customer satisfaction scores. Tailored advice and support, stemming from a direct relationship, boosted client retention rates by approximately 10% in the same year.

Branch Interactions

Physical branches foster direct customer engagement, crucial for building strong relationships. Staff at branches facilitate transactions, offer support, and give financial guidance. In 2024, despite digital trends, many still value in-person banking; 54% of US adults visited a bank branch monthly. Branch interactions help build trust and offer personalized service.

Online and Mobile Support

Financial institutions provide online and mobile support for convenient customer assistance. Live chat, email, and self-service knowledge bases are key. In 2024, mobile banking users reached 160 million, up 15% YOY. This boosts customer satisfaction and operational efficiency.

Community Events

Financial institutions boost customer relationships by actively participating in community events and sponsoring local initiatives, fostering brand loyalty. This engagement shows a genuine commitment to the community, creating chances for informal interactions. Such activities help build trust and a positive brand image. For instance, in 2024, community involvement by banks increased by 15% compared to the previous year. This strategy is crucial for attracting and retaining customers.

- Increased Brand Loyalty: Community involvement boosts customer loyalty.

- Enhanced Trust: Sponsoring local events builds trust.

- Positive Brand Image: Active participation improves brand image.

- Informal Interactions: Events create opportunities for customer engagement.

Customer Feedback

Actively seeking and responding to customer feedback is crucial for Financial Institutions Inc. to refine its services and address customer issues. This proactive approach shows dedication to customer happiness and encourages a culture of constant enhancement. In 2024, institutions with robust feedback systems saw a 15% increase in customer retention rates. This commitment to improvement can lead to increased customer loyalty and positive word-of-mouth referrals.

- Feedback mechanisms include surveys, reviews, and direct communication channels.

- Responding promptly to feedback is essential for demonstrating value.

- Data from feedback can inform strategic decisions and product development.

- Regularly analyze feedback to identify trends and areas for improvement.

Banking's Human Touch: Branches, Tech & Trust

Customer Relationships in financial institutions thrive on personal connections, like personal bankers, leading to higher customer satisfaction. Physical branches support direct interactions; in 2024, 54% of US adults visited banks monthly. Digital tools boost convenience, with mobile banking users growing by 15% YOY. Community involvement also plays a key role.

| Customer Relationship Strategy | Key Activities | 2024 Impact |

|---|---|---|

| Personal Banking | Dedicated contact, tailored service | 15% satisfaction increase |

| Physical Branches | In-person support, financial guidance | 54% monthly visits |

| Digital Support | Online and mobile assistance | 15% YOY mobile users growth |

Channels

Branch Network

The branch network is a key channel for financial institutions, facilitating direct customer interaction and service delivery. In 2024, despite the rise of digital banking, physical branches still handled a significant portion of transactions, with roughly 30% of customers preferring in-person services, according to a recent survey. Branches offer a local presence for community engagement and provide face-to-face financial advice.

Online Banking

Online banking is a key channel, offering remote account management and services. Customers can pay bills and transfer funds digitally. Usage is soaring; in 2024, over 70% of U.S. adults bank online. This channel enhances customer convenience and flexibility significantly.

Mobile Banking

Mobile banking apps are key to modern banking. They offer customers access to services via smartphones and tablets. This convenience meets the rising demand for mobile solutions. For example, in 2024, mobile banking adoption has increased by 15% globally. This shift is changing how financial institutions operate.

ATM Network

ATM networks are crucial for financial institutions, offering customers easy cash access. ATMs are typically placed in bank branches and various retail sites, enhancing accessibility. This widespread network supports customer convenience, driving transaction volumes. In 2024, the U.S. had roughly 470,000 ATMs, highlighting their importance.

- Convenient Cash Access: ATMs offer 24/7 cash access.

- Strategic Placement: Located in high-traffic areas.

- Transaction Volume: Drives substantial transaction numbers.

- Market Presence: Significant ATM count in the U.S.

Call Center

Call centers are crucial for financial institutions, offering phone support for customer inquiries and problem-solving. They facilitate transactions and provide efficient service through trained staff. In 2024, the global call center market is valued at approximately $350 billion, reflecting its importance. This support enhances customer satisfaction and operational efficiency.

- Market Growth: The call center market is projected to reach $496 billion by 2030.

- Employment: The call center industry employs millions globally.

- Technology: AI and automation are increasingly used in call centers to improve efficiency.

- Customer Service: Call centers are essential for maintaining strong customer relationships.

Banking Channels: A 2024 Snapshot

Financial institutions use diverse channels to serve customers effectively. Branches offer in-person services, though their usage is declining. Online and mobile banking channels are vital, with digital adoption soaring in 2024. ATMs and call centers ensure transaction access and support.

| Channel | Description | 2024 Data |

|---|---|---|

| Branches | Physical locations for direct service. | 30% customers prefer in-person |

| Online Banking | Remote account management. | 70%+ U.S. adults use online |

| Mobile Apps | Access via smartphones/tablets. | 15% global adoption growth |

| ATMs | Cash access. | ~470,000 in U.S. |

| Call Centers | Customer support via phone. | $350B global market value |

Customer Segments

Retail Customers

Retail customers are individual consumers using financial institutions for personal banking, savings, and loans. This segment includes students, young professionals, families, and retirees. In 2024, retail banking accounted for roughly 40% of financial institutions' revenue. The average savings account balance in the US was around $40,000 in early 2024.

Small Businesses

Small businesses are key clients of Financial Institutions Inc., utilizing services like loans and banking. This segment spans startups to established firms. In 2024, small business lending represented a significant portion of financial institutions' portfolios. For instance, the SBA approved over $20 billion in loans to small businesses in the first half of 2024.

Commercial Clients

Commercial clients, a key segment, are larger businesses needing advanced financial services. These include commercial loans, lines of credit, and cash management, serving corporations and partnerships. In 2024, commercial lending saw a 7% increase, reflecting strong demand. This segment's needs drive significant revenue for financial institutions.

Municipalities

Financial Institutions Inc. offers essential banking services to municipalities, encompassing deposit accounts, loans, and investment management. This segment demands specialized knowledge in public finance and adherence to stringent government regulations. In 2024, the municipal bond market saw over $400 billion in new issuances, reflecting significant activity. The firm must navigate complex compliance, given the evolving regulatory landscape.

- 2024 municipal bond issuances exceeded $400B.

- Requires expertise in public finance.

- Involves strict regulatory compliance.

- Offers deposit accounts, loans, and investment services.

Wealth Management Clients

Wealth management clients, including high-net-worth individuals and families, are a key customer segment for Financial Institutions. These clients seek services such as investment advice, financial planning, and estate planning, requiring sophisticated solutions. In 2024, the wealth management industry saw assets under management (AUM) reach record highs, with significant growth in personalized advisory services. This segment's demand drives the need for experienced financial advisors and diverse investment products.

- AUM in the wealth management sector increased by 8% in 2024.

- Demand for financial planning services rose by 12% among high-net-worth clients.

- Estate planning services experienced a 7% growth.

- The average account size for wealth management clients is $1 million.

Institutional Trading Dominance: Over 60% Market Share

Institutional clients comprise hedge funds, mutual funds, and pension funds, leveraging financial institutions for investment banking and asset management services. This segment’s trading volumes significantly impact market liquidity. Institutional trading accounted for over 60% of all trading volume in 2024. The sophistication of their needs requires specialized financial products.

| Customer Segment | Service Needs | 2024 Market Data |

|---|---|---|

| Retail Customers | Banking, Loans, Savings | 40% of revenue, $40K avg. savings |

| Small Businesses | Loans, Banking | $20B+ SBA loans (H1) |

| Commercial Clients | Loans, Credit, Cash Mgmt. | 7% increase in lending |

| Municipalities | Deposit, Loans, Investment | $400B+ bond issuances |

| Wealth Management | Inv. Advice, Planning | 8% AUM growth |

| Institutional Clients | Investment Banking, Asset Mgmt | 60% of trading volume |

Cost Structure

Operating Expenses

Operating expenses are essential for financial institutions. These encompass salaries, rent, and utilities, vital for branch networks and offices. Efficient management is crucial for profitability, with 2024 data showing operational costs averaging 60-70% of revenue for many banks. Consider the 2024 figures: JPMorgan Chase's operating expenses were around $80 billion.

Technology Costs

Technology costs are a hefty part of financial institutions' expenses. They must invest in and maintain tech like core banking systems, online platforms, and cybersecurity. This demands continuous spending and skilled IT staff. In 2024, banks spent billions on tech, with cybersecurity alone costing an average of $18.3 million per breach.

Regulatory Compliance

Financial institutions face significant costs to ensure regulatory compliance. This includes expenses for staff dedicated to compliance, training programs, and regular reporting. Moreover, institutions must adhere to capital requirements, anti-money laundering (AML) laws, and consumer protection regulations. In 2024, the average cost of compliance for U.S. banks was estimated at $100 million annually. These costs can vary considerably based on the size and complexity of the institution.

Interest Expense

Interest expense is a significant component of a financial institution's cost structure, primarily encompassing the interest paid on deposits and borrowed funds. Efficiently managing this expense is critical for preserving a strong net interest margin, which is the difference between interest earned and interest paid. For instance, in 2024, major banks allocated a substantial portion of their revenue to cover interest payments. Effective strategies like adjusting deposit rates and optimizing borrowing costs are essential. This directly impacts profitability and competitiveness in the market.

- Interest payments can represent 30-60% of a bank's total operating expenses.

- Net interest margin for U.S. banks in 2024 averaged around 2.8%.

- Rising interest rates in 2024 increased interest expense for many financial institutions.

- Banks use various financial instruments to manage interest rate risk.

Loan Losses

Loan losses represent a critical cost within a financial institution's cost structure, necessitating the allocation of reserves to cover potential defaults. This process demands robust credit risk management practices and precise forecasting of future loan losses. Accurate estimations are vital for maintaining financial stability and profitability. For instance, in 2024, the net charge-off rate for commercial and industrial loans at U.S. banks was approximately 0.45%.

- Reserves are crucial for covering potential defaults.

- Credit risk management is vital for minimizing losses.

- Accurate forecasting ensures financial stability.

- The net charge-off rate for C&I loans was ~0.45% in 2024.

Financial Institution's Cost Breakdown: Key Components

Cost Structure includes operating expenses like salaries, rent, and tech. Technology and compliance costs also play a significant role in the financial institutions. Interest and loan losses are critical components.

| Expense Category | Description | 2024 Data Points |

|---|---|---|

| Operating Expenses | Salaries, rent, utilities. | 60-70% of revenue, JPMorgan Chase: $80B. |

| Technology Costs | Tech, online platforms, cybersecurity. | Cybersecurity breach costs: $18.3M. |

| Compliance Costs | Staff, training, reporting, regulations. | U.S. banks: $100M annually. |

Revenue Streams

Interest Income

Interest income is central to financial institutions' revenue, generated from loans and lending products. This includes interest from mortgages, commercial, and consumer loans. In 2024, U.S. banks earned over $700 billion in interest income. The interest rates are influenced by the Federal Reserve's monetary policy and market conditions.

Fee Income

Fee income, derived from services like account maintenance and wire transfers, is crucial. It diversifies revenue and lessens dependence on interest. In 2024, banks earned billions from fees; JPMorgan Chase, for example, generated substantial non-interest income. This strategy enhances financial stability.

Wealth Management Fees

Financial institutions earn substantial revenue by charging fees for wealth management services. These fees cover investment advice, financial planning, and portfolio management, primarily targeting high-net-worth clients. In 2024, the global wealth management market was valued at approximately $3.5 trillion, reflecting its significant revenue potential. As Financial Institutions Inc. broadens its wealth management operations, this revenue stream is poised for continued expansion.

Insurance Commissions

Financial Institutions Inc. previously earned revenue through commissions from SDN Insurance Agency, offering a diversified income stream. This allowed the company to provide a wider range of financial services to its clients. The sale of SDN Insurance Agency to NFP Property & Casualty Services, Inc. in April 2024 changed this revenue aspect. This strategic shift impacts the financial model.

- Diversified Income: Insurance commissions offered an additional revenue source.

- Service Expansion: Enabled a broader financial service offering.

- Strategic Change: SDN Insurance Agency was sold in April 2024.

- Impact: The sale affects the company's revenue streams.

Investment Gains

Investment gains represent a crucial revenue stream for financial institutions, stemming from their strategic investments in securities and other assets. This income is realized through the sale of investments at a profit, which is a direct result of effective investment management. Generating these gains requires a well-diversified investment portfolio to mitigate risks and capitalize on market opportunities. Financial institutions often employ sophisticated strategies to optimize returns and enhance profitability.

- In 2024, the global asset management industry's revenue is projected to be around $1.2 trillion.

- The average return on investment (ROI) for a diversified portfolio can range from 7% to 10% annually, depending on market conditions.

- Successful investment management involves active portfolio adjustments.

- Diversification is essential to manage risks and maximize returns.

Financial Institutions' 2024 Revenue: Key Strategies

Financial institutions generate revenue through diverse streams, including interest income from loans and fees for services. Wealth management and investment gains are key components. In 2024, these strategies contributed significantly to their financial performance.

| Revenue Stream | Description | 2024 Data Point |

|---|---|---|

| Interest Income | Earnings from loans | U.S. banks: $700B+ |

| Fee Income | Charges for services | JPMorgan Chase: substantial |

| Wealth Management | Fees for investment services | Global market: $3.5T |

Business Model Canvas Data Sources

The Financial Institutions Business Model Canvas utilizes financial reports, industry analyses, and market research. These sources support a data-driven strategic overview.