HSBC Holding Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

HSBC Holding Bundle

What is included in the product

Evaluates control held by suppliers and buyers, and their influence on pricing and profitability.

Swap in your own data, labels, and notes to reflect current business conditions.

Preview the Actual Deliverable

HSBC Holding Porter's Five Forces Analysis

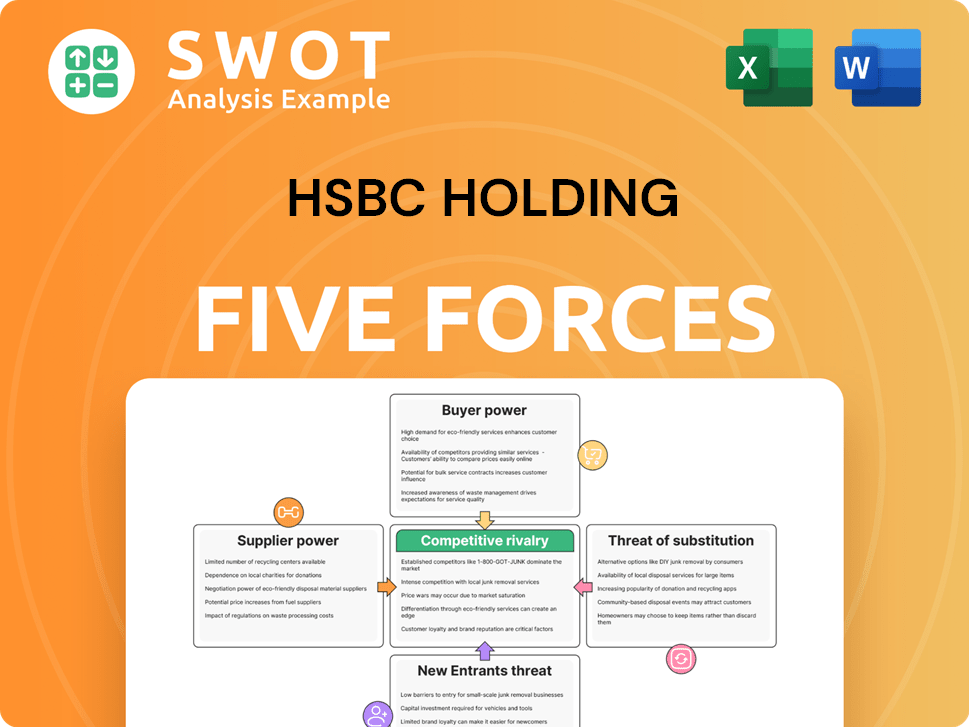

This preview details HSBC's Porter's Five Forces analysis, examining competitive rivalry, supplier power, buyer power, threat of substitutes, and threat of new entrants. The analysis assesses the banking giant's market position and industry dynamics. You're previewing the final version—precisely the same document that will be available to you instantly after buying.

Porter's Five Forces Analysis Template

Go Beyond the Preview—Access the Full Strategic Report

HSBC Holdings navigates a complex banking landscape, grappling with intense competition from global and regional players, which lowers profitability. The threat of new entrants, including fintech firms, also poses a challenge. Buyer power is relatively moderate due to the availability of alternative banking services. Supplier power, particularly from labor and IT providers, exerts some pressure. The presence of substitute products, like digital payment systems, presents another hurdle.

Ready to move beyond the basics? Get a full strategic breakdown of HSBC Holding’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Technology Vendor Dominance

HSBC's dependency on key tech vendors like IBM, Microsoft, and Oracle elevates supplier power. These vendors offer vital banking tech and software, hindering easy transitions. In 2024, tech spending by banks increased, with HSBC allocating a significant portion to these providers. The high concentration of services necessitates robust risk management to mitigate supplier-related risks.

High Switching Costs

HSBC faces high switching costs due to technology infrastructure changes. System migration can cost $75M-$250M, while software integration ranges from $35M-$120M. Implementation and training add another $15M-$50M. These expenses increase HSBC's dependence on current suppliers. Switching costs represent 2-5% of the annual IT budget, per Gartner.

Vendor Lock-In

HSBC's vendor lock-in risk is significant, particularly with essential systems. The probability of vendor lock-in is estimated at 78%, indicating high dependency. Technology contracts averaging 5-7 years strengthen suppliers' positions. This reliance can restrict HSBC's flexibility and its ability to negotiate favorable terms.

Regulatory Scrutiny on Third-Party Risk

Financial regulators are intensifying their focus on third-party risks, especially those related to technology providers, which impacts HSBC. The bank must now thoroughly assess its reliance on these providers and update its risk mitigation strategies. This includes mapping out all exposures to ensure resilience. Increased scrutiny aims to manage risks tied to concentrated dependencies.

- In 2024, regulatory fines for third-party risk failures rose by 15%.

- HSBC's IT spending on third-party vendors is approximately $6 billion annually.

- The bank has identified over 500 critical third-party tech providers.

- Recent reports indicate a 20% increase in audits related to third-party risk management.

Concentration of Outsourced Services

HSBC's reliance on outsourced services, particularly for critical functions, concentrates bargaining power among a few key suppliers. The bank allocates a significant portion of its budget to a limited number of external providers. This concentration poses operational risks if a major supplier faces disruptions.

- In 2024, HSBC's spending was heavily concentrated, with 50% of the budget going to just 30 providers.

- This setup increases the risk of operational failures if a key provider experiences issues.

- HSBC must manage these supplier relationships carefully to maintain resilience.

Tech Vendor Dependence: A $6B Financial Impact

HSBC's supplier power is heightened by dependence on key tech vendors. High switching costs and vendor lock-in, with tech contracts averaging 5-7 years, bolster supplier leverage. In 2024, HSBC's IT spending on third-party vendors was about $6 billion annually, significantly impacting its financial flexibility.

| Aspect | Details | Impact |

|---|---|---|

| Vendor Concentration | 50% budget to 30 providers in 2024 | Increased operational risk |

| Switching Costs | System migration: $75M-$250M | Higher vendor power |

| Regulatory Scrutiny | Fines up 15% in 2024 | Focus on risk management |

Customers Bargaining Power

Customer Price Sensitivity

HSBC's retail customers exhibit strong price sensitivity, frequently comparing fees across banks, thus boosting their bargaining power. In 2024, a survey showed that over 60% of retail banking customers actively seek better rates. This drives customers to switch providers, pressuring HSBC to keep its pricing competitive. Consequently, HSBC must carefully manage its pricing strategies to retain customers.

Low Switching Costs

Customers of HSBC have low switching costs, enabling them to easily compare and select the best financial products. Moderate product differentiation means alternatives are readily available. This ease of switching strengthens customer bargaining power. In 2024, the average cost to switch banks in the UK was around £25, reflecting low barriers.

Demand for Digital Services

Customers increasingly demand digital banking. HSBC's digital adoption is high globally, with 71% of retail customers using digital channels in 2023. They expect seamless experiences. HSBC must invest in tech to retain customers; otherwise, attrition risks increase.

Competition in Interest Rates and Fees

Customers wield significant bargaining power in the banking sector, especially when comparing interest rates and fees. Banks are in constant competition to attract and retain customers by offering the most appealing financial products. This environment allows customers to easily switch between institutions to find the best deals. This dynamic is evident in 2024, with average savings account interest rates fluctuating as banks compete for deposits.

- Competitive pressure forces banks to offer better terms.

- Customers can quickly compare rates and fees online.

- Switching costs are low, increasing customer power.

- HSBC must adapt to stay competitive.

Multiple Banking Options

Customers wield significant bargaining power due to the availability of numerous banking options in their markets. This widespread choice allows them to readily switch providers based on more favorable terms or services. HSBC faces competition from a multitude of major global banks, intensifying the pressure to offer competitive rates and services to retain customers. For instance, in 2024, the U.S. banking sector saw over 4,000 FDIC-insured institutions. This competitive landscape significantly impacts HSBC's pricing and service strategies.

- High Customer Choice: Availability of many banking alternatives enhances customer leverage.

- Competitive Pressure: HSBC competes with numerous global banks, affecting its strategies.

- Impact on Terms: Customers can negotiate for better terms and service.

- Switching Ability: Easy switching enhances customer bargaining power.

Banking: Customer Power Surges in 2024!

Customers have significant bargaining power in the banking sector. This is due to easy switching and competitive rates. In 2024, digital banking adoption continues to rise, enhancing customer influence.

| Aspect | Details | 2024 Data |

|---|---|---|

| Switching Costs | Average cost to switch banks | £25 in the UK |

| Digital Adoption | Percentage of retail customers using digital channels | 71% (2023) |

| Banking Options | Number of FDIC-insured institutions in the U.S. | Over 4,000 |

Rivalry Among Competitors

Intense Competition

HSBC confronts fierce competition from global banking giants like Citi and Bank of America. These competitors offer similar financial products, intensifying the battle for customers. The slow market growth rate further complicates the ability of any single firm to secure a dominant position. In 2024, HSBC's revenue was approximately $66.1 billion, showcasing its scale amidst competition.

Replication of Practices

HSBC faces intense rivalry because competitors quickly copy new practices. This replication creates market stalemates, making differentiation tough. Rapid imitation increases competitive pressures. In 2024, HSBC's net interest income was $35.8 billion, showing how competition impacts financial results.

Digital Transformation and Fintech

The surge of digital-first neobanks and tech firms as financial advisors heightens competition. Technology streamlines tasks like money transfers and balance checks, making digital transformation crucial for banks. HSBC must embrace tech to stay relevant, as seen by a 2024 rise in digital banking users. Banks need new tech to meet evolving customer demands. In 2024, digital banking adoption grew by 15% globally.

Consolidation and M&A Activity

The financial services sector is seeing a resurgence in mergers and acquisitions (M&A), with a focus on scale and capability enhancements. Limited financial resources within the industry are expected to fuel further consolidation, favoring larger firms acquiring smaller ones. This trend intensifies competition. In 2024, global M&A activity in financial services reached $300 billion, a 20% increase from 2023.

- M&A in financial services increased by 20% in 2024.

- Global M&A activity in financial services reached $300 billion in 2024.

- Consolidation is driven by the need for scale and enhanced capabilities.

Focus on Efficiency and AI

Competitive rivalry in the banking sector is intense, with HSBC and its peers constantly seeking ways to boost efficiency. Banks are increasingly using AI and automation to cut costs and improve customer service. Generative AI tools are offering even greater efficiency potential. Community banks are also investing heavily in tech to stay competitive.

- In 2024, the global fintech market was valued at over $150 billion, showing the industry's tech focus.

- Automation in banking is expected to reduce operational costs by up to 30% by 2025.

- Community banks' tech spending rose by 15% in 2024 to compete with larger institutions.

Banking Battleground: Competition Heats Up!

HSBC navigates fierce competition, particularly from global banks, complicating market dominance. Rapid imitation and digital advancements intensify this rivalry. Mergers & Acquisitions further concentrate the competitive landscape. In 2024, the digital banking sector saw a 15% growth.

| Aspect | Details | 2024 Data |

|---|---|---|

| M&A Activity | Financial services M&A | $300 billion |

| Fintech Market | Global market value | Over $150 billion |

| Digital Banking Adoption | Growth in adoption | 15% |

SSubstitutes Threaten

Emergence of Digital Payment Platforms

Digital payment platforms, such as WhatsApp Pay and Apple Pay, are increasingly viable substitutes for traditional banking services. These platforms are gaining traction by offering user-friendly experiences and competitive services, directly challenging the dominance of established financial institutions. This shift poses a moderate threat to HSBC, as these platforms can erode its customer base and revenue streams. In 2024, digital payments accounted for over 60% of all transactions in many developed markets, highlighting the growing influence of these alternatives.

Cryptocurrency and Blockchain Technologies

Cryptocurrencies and blockchain could substitute traditional services, but adoption and regulation are evolving. These technologies could disrupt traditional banking models. Banks have largely been out of the crypto sector. In 2024, the global cryptocurrency market was valued at around $1.11 trillion. If crypto becomes more open to banking, it could threaten banks' core business.

Peer-to-Peer Lending

Peer-to-peer lending platforms, like LendingClub and Prosper, offer direct lending, increasing the threat of substitutes for HSBC. These platforms allow individuals to lend to each other, circumventing traditional banks. Digital wallets, such as PayPal and Venmo, also compete by offering payment and lending services. In 2024, the peer-to-peer lending market was valued at approximately $120 billion, growing annually by about 8%.

Digital Wallets and Mobile Banking

Mobile banking and digital wallets present a significant threat to traditional banking. Customers now have convenient alternatives for managing finances. HSBC's digital banking adoption is soaring globally. Digital solutions offer ease of access and control. This impacts HSBC's traditional service models.

- Digital banking users globally reached 65% in 2024.

- HSBC's mobile transaction volume grew by 20% in 2024.

- The digital wallet market is projected to reach $10 trillion by 2025.

- HSBC invested $7 billion in digital initiatives in 2024.

Limited Substitutes for Core Banking

HSBC faces minimal threat from substitutes for core banking services, as financial products are unique. However, the rise of fintech and specialized financial services poses a challenge. These new entrants offer targeted solutions, potentially eroding HSBC's market share in specific areas. HSBC must innovate to remain competitive. The overall market share of fintech companies increased to approximately 7% in 2024.

- Financial services are rarely fully replicable.

- Fintech companies are growing.

- HSBC needs to keep innovating.

- Fintech market share is around 7%.

HSBC Faces Rising Fintech & Digital Payment Challenges

The threat of substitutes to HSBC is moderate, fueled by digital platforms and fintech advancements. Digital payment methods like Apple Pay and digital banking options are gaining popularity, challenging traditional banking. The digital wallet market is set to reach $10 trillion by 2025, highlighting the need for HSBC to adapt and innovate.

| Substitute Type | Market Share/Value (2024) | Key Impact on HSBC |

|---|---|---|

| Digital Payments | 60%+ of transactions | Erosion of customer base |

| P2P Lending | $120B market, 8% annual growth | Direct competition on lending |

| Fintech | ~7% market share | Competition in specific services |

Entrants Threaten

High Regulatory Barriers

New banks face significant barriers to entry, especially due to high regulatory hurdles. These regulations often require massive capital investments and extensive compliance procedures. For example, in 2024, new banks in the UK needed to meet stringent capital adequacy ratios, complicating market entry. This makes it difficult for new players to compete with established giants like HSBC.

Incumbent Goodwill

HSBC's strong brand recognition and existing customer relationships create a significant barrier against new competitors. Customer loyalty is high among high-net-worth clients, making them less likely to switch. In 2024, HSBC's global brand value was estimated at $17.4 billion, reflecting strong customer trust. This goodwill advantage makes it challenging for new entrants to gain market share.

Focus on Differentiation

New entrants to the banking sector face significant hurdles, particularly in differentiating their offerings. HSBC's established brand and global presence make it tough to compete. Stringent regulations, like those set by the Basel Committee, add to the complexity and cost for new players. For example, in 2024, complying with these rules required substantial capital investments. New entrants must offer unique services or products to attract customers.

International Players

HSBC faces threats from international players eager to expand into new markets. These entrants might possess varying risk tolerances and strategic aims, potentially disrupting established market dynamics. The conditions are indeed different for international players entering new geographies, impacting competition. For example, in 2024, several international banks have increased their presence in Asia, signaling heightened competitive pressure for HSBC.

- Increased competition from international banks in key markets.

- Different risk profiles and strategic goals of new entrants.

- Potential for market disruption due to aggressive expansion strategies.

- Adapting to new regulatory landscapes in different geographies.

Fintech and Neobanks

The threat of new entrants, especially fintechs and neobanks, poses a significant challenge to HSBC. These digital-first neobanks attract customers with innovative services and competitive rates, potentially eroding HSBC's customer base. Fintechs are reshaping banking, often providing superior user experiences compared to traditional universal banks. Technology simplifies banking operations, making digital platforms the norm.

- Fintech funding reached $75.7 billion in 2023.

- Neobanks have seen a surge in popularity, with estimated user growth.

- HSBC must adapt to compete with these agile new entrants.

HSBC: Navigating the Competitive Banking Landscape

The threat of new entrants to HSBC is moderate due to high barriers. Established banks face stringent regulations and capital requirements. Fintechs and neobanks are increasing competition, with fintech funding reaching $75.7 billion in 2023.

| Factor | Impact | Example |

|---|---|---|

| Regulations | High compliance costs. | UK capital adequacy rules. |

| Brand Strength | Customer loyalty. | HSBC's $17.4B brand value. |

| New Entrants | Fintechs and neobanks | User growth and innovation. |

Porter's Five Forces Analysis Data Sources

Our analysis uses HSBC's annual reports, industry news, financial databases, and competitive landscape assessments for comprehensive data.