Principal Financial Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Principal Financial Group Bundle

What is included in the product

Tailored exclusively for Principal Financial Group, analyzing its position within its competitive landscape.

Instantly visualize competitive intensity with dynamic charts & graphs for each force.

Preview Before You Purchase

Principal Financial Group Porter's Five Forces Analysis

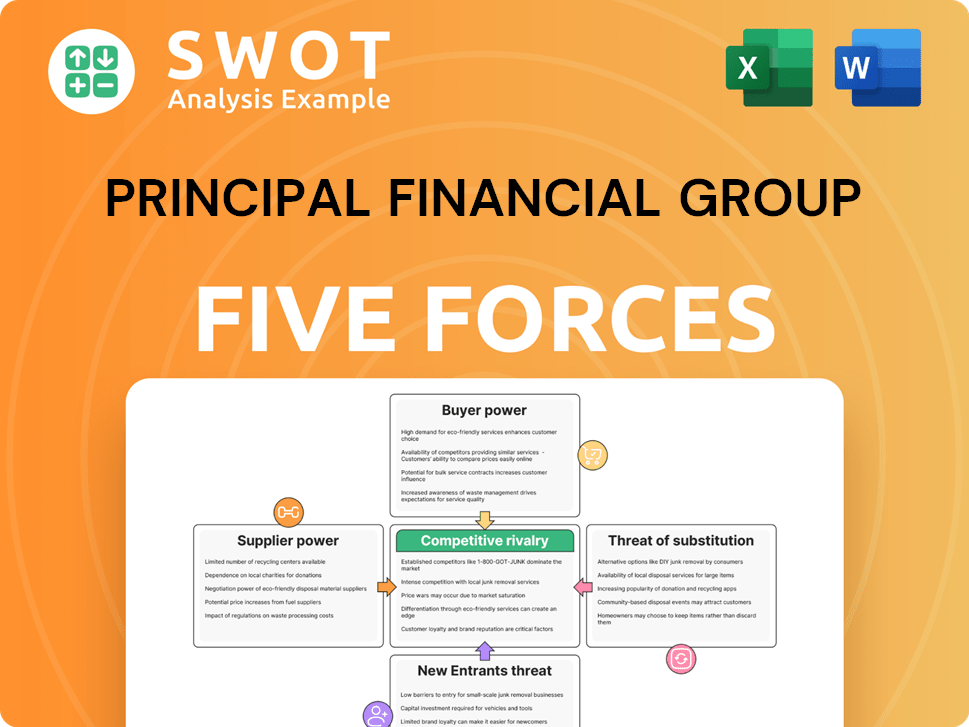

You're previewing the final version—precisely the same document that will be available to you instantly after buying. This Principal Financial Group Porter's Five Forces analysis examines the industry's competitive landscape. It assesses the threats of new entrants and substitutes. It also details the bargaining power of buyers and suppliers, and competitive rivalry.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Principal Financial Group faces moderate rivalry within the insurance and financial services sectors, with established competitors vying for market share. The threat of new entrants is relatively low due to high capital requirements and regulatory hurdles. Buyer power is concentrated, as institutional clients and large employers can negotiate favorable terms. Supplier power is limited, given the availability of various investment products and services. The threat of substitute products, such as ETFs or other investment vehicles, poses a moderate challenge.

The complete report reveals the real forces shaping Principal Financial Group’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Consolidation

The financial sector depends on suppliers like tech firms and consultants. If these suppliers are few or unique, they gain power. This can hike Principal's expenses. In 2024, tech spending in finance surged, showing supplier influence.

Switching Costs for Inputs

Principal Financial Group's ability to switch suppliers significantly impacts supplier power. High switching costs, maybe due to proprietary systems, strengthen suppliers. In 2024, companies invested heavily in tech integrations. Principal's tech flexibility influences this, affecting cost and control. Assessing adaptability is key for managing supplier relationships effectively.

Impact of Regulation on Suppliers

Regulatory requirements can significantly influence the supplier landscape, potentially reducing the number of available vendors. Principal must understand how regulations shape its supply chain and its relationships with suppliers. Compliance costs and restrictions can indirectly increase supplier power. For example, in 2024, stricter data privacy rules increased costs for tech suppliers, indirectly affecting Principal's vendor options.

Data Provider Influence

Access to high-quality data is vital for Principal Financial Group's operations. Data and analytics suppliers can exert substantial influence if their offerings are crucial and hard to duplicate. Principal's dependence on specific data providers needs careful assessment to understand potential risks. For example, in 2024, the market for financial data services was estimated at over $30 billion globally, with significant growth projected. This highlights the high stakes involved.

- Data Dependence: Principal's reliance on key data vendors.

- Market Dynamics: The competitive landscape of data providers.

- Cost Analysis: The expense of data services compared to revenue.

- Strategic Alternatives: The potential for in-house data solutions.

Labor Market Dynamics

The labor market significantly influences Principal Financial Group's supplier power. The availability and cost of skilled labor, especially in tech and finance, are critical. For instance, in 2024, the average financial analyst salary in the US was around $85,000, reflecting labor market dynamics.

Tight labor markets can increase compensation costs, impacting Principal's operational expenses, as seen with rising salaries for tech roles. Principal must monitor these trends to manage costs effectively. This is crucial for maintaining profitability and competitiveness within the financial services sector.

- Skilled labor costs are crucial for financial services.

- Tight labor markets drive up compensation.

- Principal must monitor labor market trends.

- Rising labor costs can affect profitability.

Supplier Power Dynamics at a Financial Giant

Principal Financial faces supplier power influenced by tech and data dependence. High costs and switching barriers give suppliers leverage. In 2024, the financial data services market was over $30 billion. Labor costs also impact supplier power.

| Factor | Impact | 2024 Data Point |

|---|---|---|

| Tech Spend | Increased Costs | Finance tech spending surged |

| Switching Costs | Supplier Leverage | High costs due to proprietary tech. |

| Data Market | Vendor Power | $30B+ financial data market. |

Customers Bargaining Power

Customer Concentration

Principal Financial Group's customer concentration varies across its business lines. The bargaining power of customers is higher when a few large clients make up a significant portion of revenue. For instance, institutional clients managing large pension funds may have considerable negotiating power. In 2024, Principal's institutional clients represented a notable share of its assets under management.

Switching Costs for Customers

Switching costs significantly influence customer bargaining power in the financial sector. Principal Financial Group's customer retention is affected by the ease of switching to competitors. High switching costs, like surrender charges on annuities, reduce customer power; in 2024, these charges averaged 5-7% of the contract value. Conversely, simple transfers enhance customer leverage.

Price Sensitivity

The price sensitivity of Principal's customers significantly influences their bargaining power. In areas with high price sensitivity, like low-cost investment options, Principal might have to cut fees, squeezing profits. For example, in 2024, the demand for cheaper financial products grew, impacting Principal's pricing strategies. Understanding customer price elasticity is crucial for Principal's financial planning.

Information Availability

Customers with ample information on financial products can negotiate better terms and switch providers, increasing their bargaining power. Transparency in the financial sector has grown, empowering customers to make informed decisions. Principal Financial Group must differentiate its offerings to maintain its competitive edge. The rise of online comparison tools and financial news sources has significantly increased customer awareness. In 2024, approximately 78% of U.S. adults use online resources to manage their finances.

- Increased Online Resources: The availability of online financial tools and comparison websites.

- Customer Awareness: Enhanced knowledge and understanding of financial products.

- Negotiating Power: Ability of customers to negotiate better terms.

- Competitive Advantage: Principal's need to differentiate its offerings.

Service Customization

Principal Financial Group's ability to customize services significantly impacts customer bargaining power. Tailoring financial plans and investment solutions can enhance customer loyalty. This personalization makes it harder for customers to switch to competitors. Customization reduces customer power by making alternatives less comparable. In 2024, Principal reported a 95% client retention rate for its wealth management services, highlighting the effectiveness of personalized offerings.

- Personalized financial planning boosts customer loyalty.

- Custom solutions make switching to competitors difficult.

- High client retention rates reflect successful customization.

- Customization lowers customer bargaining power.

Customer Power Dynamics at a Financial Institution

Customer bargaining power at Principal Financial Group varies based on client concentration, switching costs, and price sensitivity. High switching costs and personalized services reduce customer leverage, while access to information and price transparency enhance it. In 2024, client retention remained high, showing the impact of customized offerings.

| Factor | Impact | 2024 Data |

|---|---|---|

| Client Concentration | High concentration = Higher Power | Institutional clients: Significant AUM share |

| Switching Costs | High costs = Lower Power | Annuity surrender charges: 5-7% |

| Price Sensitivity | High sensitivity = Higher Power | Demand for cheaper products grew |

Rivalry Among Competitors

Market Concentration

The financial services sector is intensely competitive, featuring many large firms. High market concentration, where a few firms dominate, can boost rivalry. Principal competes with insurance companies, asset managers, and retirement service providers. For example, in 2024, the top 10 US life insurance companies held over 60% of the market share, intensifying competition.

Differentiation

Principal Financial Group's differentiation strategies significantly impact its competitive landscape. Principal's robust brand enhances its market position, reducing rivalry. Innovative products and services are key for gaining an edge. In 2024, Principal's focus on personalized financial solutions aimed to stand out. Differentiation helps Principal maintain its competitive advantage.

Industry Growth Rate

Slower industry growth often fuels intense competition as companies fight for market share. Principal Financial Group must monitor the growth rate of the retirement, insurance, and investment management sectors. For instance, in 2024, the U.S. life insurance market saw moderate growth. This contrasts with rapid growth phases, where multiple firms can expand easily.

Exit Barriers

High exit barriers, like stringent regulations or unique assets, can trap struggling companies, amplifying competition. Understanding why competitors find it hard to leave is crucial. These barriers often lead to a saturated market. For Principal Financial Group, this means sustained rivalry. The insurance sector faces such challenges.

- Regulatory hurdles can slow exits.

- Specialized assets limit resale options.

- High exit costs intensify competition.

- Market saturation affects profitability.

Strategic Alliances

Strategic alliances significantly influence competitive dynamics in the financial services sector. These collaborations can lead to new competitive advantages or reshape existing rivalries. Principal Financial Group must actively monitor these partnerships to stay competitive. In 2024, the number of strategic alliances grew by 12% in the insurance sector. Considering the evolving landscape is crucial for Principal's strategic positioning.

- Growing Alliances: The financial services sector saw a 12% increase in strategic alliances in 2024.

- Competitive Advantage: Alliances can create new advantages.

- Monitoring Landscape: Principal must monitor partnerships.

- Strategic Positioning: Vital for Principal's future.

Financial Services: Navigating the Competitive Landscape

Competitive rivalry in financial services is intense, with many players vying for market share. Principal Financial Group faces significant competition from various firms, including insurance and asset management companies. Strategic alliances and differentiation are crucial for Principal to maintain its market position. The evolving landscape requires careful monitoring of competitors and industry dynamics.

| Aspect | Details | 2024 Data |

|---|---|---|

| Market Share | Top 10 US life insurance companies | Over 60% |

| Strategic Alliances | Increase in financial services | 12% growth |

| Industry Growth | U.S. life insurance market | Moderate |

SSubstitutes Threaten

Alternative Investment Options

Principal Financial Group faces threats from alternative investments like real estate and commodities. These substitutes can curb Principal's pricing power. In 2024, real estate saw varied returns, while commodities experienced fluctuations. Assessing alternative investments' performance is vital for Principal. Peer-to-peer lending also presents a substitute.

DIY Investing

The DIY investing trend, fueled by platforms like Robinhood and Fidelity, presents a substitute threat. These platforms provide low-cost access to markets, challenging traditional advisory services. In 2024, DIY investors manage a significant portion of assets, potentially impacting Principal's revenue. The rise of robo-advisors also offers automated, low-fee alternatives, further intensifying this threat. Principal must adapt to retain clients.

Government Programs

Government-sponsored retirement programs, like Social Security, present a substitute threat to Principal's private retirement plans. In 2024, Social Security benefits saw a cost-of-living adjustment of 3.2%, influencing consumer decisions. Changes in these benefits or eligibility requirements can directly affect the demand for Principal's offerings. Policy changes require careful monitoring to understand their impact.

Insurance Alternatives

Insurance alternatives present a notable threat to Principal Financial Group. Customers might opt for self-insurance or alternative risk transfer, impacting Principal's market share. These substitutes offer ways to manage risk outside of traditional insurance. This dynamic influences Principal's pricing and product strategies. The availability of these alternatives is a key consideration for Principal's competitive positioning.

- Self-insurance popularity is growing, especially among large corporations.

- Alternative risk transfer methods, such as captive insurance, are expanding.

- Principal must compete with these alternatives to retain customers.

- The cost and complexity of alternatives influence customer choice.

FinTech Disruption

FinTech poses a significant threat to Principal Financial Group. Innovative financial products and services from FinTech companies can disrupt traditional offerings. Peer-to-peer insurance and digital retirement platforms emerge as substitutes. Blockchain-based solutions may also become viable alternatives. Monitoring technological advancements is crucial.

- In 2024, the global FinTech market was valued at over $150 billion.

- Digital retirement platforms are projected to grow substantially by 2025.

- Blockchain solutions in finance are attracting increasing investment.

- Principal Financial Group needs to adapt to stay competitive.

Principal's Pricing Power Under Siege

Principal faces threats from diverse substitutes impacting pricing power. Self-insurance and alternative risk transfer are growing, especially for large corporations, offering choices outside traditional insurance. The FinTech market, valued at over $150 billion in 2024, fuels digital alternatives, including peer-to-peer insurance and retirement platforms. Adaption is critical.

| Substitute Type | 2024 Market Data | Impact on Principal |

|---|---|---|

| Alternative Investments | Varied returns in real estate & commodities | Curb pricing power |

| DIY Investing | Significant portion of assets managed by DIY investors | Impact revenue |

| FinTech | FinTech market at $150B+ | Disrupt traditional offerings |

Entrants Threaten

Capital Requirements

The financial services sector demands substantial capital, setting a high entry bar. Regulatory needs and compliance further inflate costs, deterring newcomers. Principal Financial Group, with its established capital base, gains a competitive edge. For instance, in 2024, the average startup cost for a financial advisory firm was approximately $100,000 to $500,000, mainly due to regulatory and compliance requirements.

Regulatory Hurdles

Stringent regulations and licensing requirements pose a significant barrier for new entrants into the financial services market, increasing compliance costs. These costs can be substantial; in 2024, the average compliance budget for financial institutions rose by 7%. Regulatory expertise is a key advantage. Navigating complex legal frameworks is a challenge for new companies.

Brand Recognition

Principal Financial Group benefits from strong brand recognition, a key advantage. It takes considerable time and resources to build brand equity, discouraging new competitors. In 2024, Principal's brand value reflects its reputation in the insurance and financial services sector. Strong brand recognition helps retain customers and attract new ones. This advantage makes it harder for newcomers to gain market share.

Economies of Scale

Principal Financial Group faces a moderate threat from new entrants due to its established economies of scale. Larger firms like Principal leverage cost advantages in operations, technology, and marketing. New competitors often find it challenging to match the cost structures of established entities. Principal's extensive scale provides a significant cost advantage, enhancing its competitive position. In 2024, Principal's total revenue reached approximately $16.8 billion, demonstrating its operational capacity.

- Operational Efficiency: Principal's large scale allows for streamlined processes.

- Technology Advantage: Investments in technology provide a competitive edge.

- Marketing Reach: Extensive marketing campaigns help maintain market presence.

- Cost Leadership: Economies of scale support lower operational costs.

Access to Distribution Channels

The threat of new entrants for Principal Financial Group is moderate, primarily due to the challenges in accessing distribution channels. Access to established networks, like partnerships with employers for retirement plans, is crucial for reaching customers. New companies face significant hurdles in building these distribution networks, giving Principal a competitive advantage.

Principal's existing distribution network strengthens its market position, making it harder for new firms to compete. This advantage is particularly important in the retirement and insurance markets, where established relationships are key.

- Principal serves approximately 1.7 million customers in its retirement business.

- In 2024, Principal's assets under management were over $668 billion.

- Principal has a strong presence in the U.S. and international markets.

Market Entry Challenges: Principal's Edge

New entrants face moderate barriers. High startup costs and regulatory hurdles are significant, deterring many. Principal's brand recognition and established distribution networks further limit the threat. The firm benefits from economies of scale, making it tough for newcomers to compete.

| Factor | Impact on Principal | 2024 Data |

|---|---|---|

| Capital Requirements | High Entry Barrier | Startup costs $100K-$500K. |

| Regulatory Compliance | Increased Costs | Compliance budgets up 7%. |

| Brand Recognition | Competitive Advantage | Principal's strong brand value. |

Porter's Five Forces Analysis Data Sources

Principal Financial Group analysis utilizes SEC filings, market research, and financial publications to evaluate competitive dynamics.