Bank of Nova Scotia SWOT Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Bank of Nova Scotia Bundle

What is included in the product

Offers a full breakdown of Bank of Nova Scotia’s strategic business environment

Perfect for summarizing SWOT insights across business units.

What You See Is What You Get

Bank of Nova Scotia SWOT Analysis

Get a look at the actual SWOT analysis file. This preview offers an inside look at the high-quality report you will get.

SWOT Analysis Template

Elevate Your Analysis with the Complete SWOT Report

Scotiabank, a global financial leader, navigates a complex landscape. Its strengths lie in strong brand recognition and diversified services. However, economic fluctuations pose a significant threat, influencing its strategic agility. Furthermore, evolving digital trends shape the industry, necessitating proactive adaptation. Acknowledging opportunities, such as expansion in emerging markets, is key. Identify internal capabilities. Unlock strategic advantages by examining all aspects.

Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

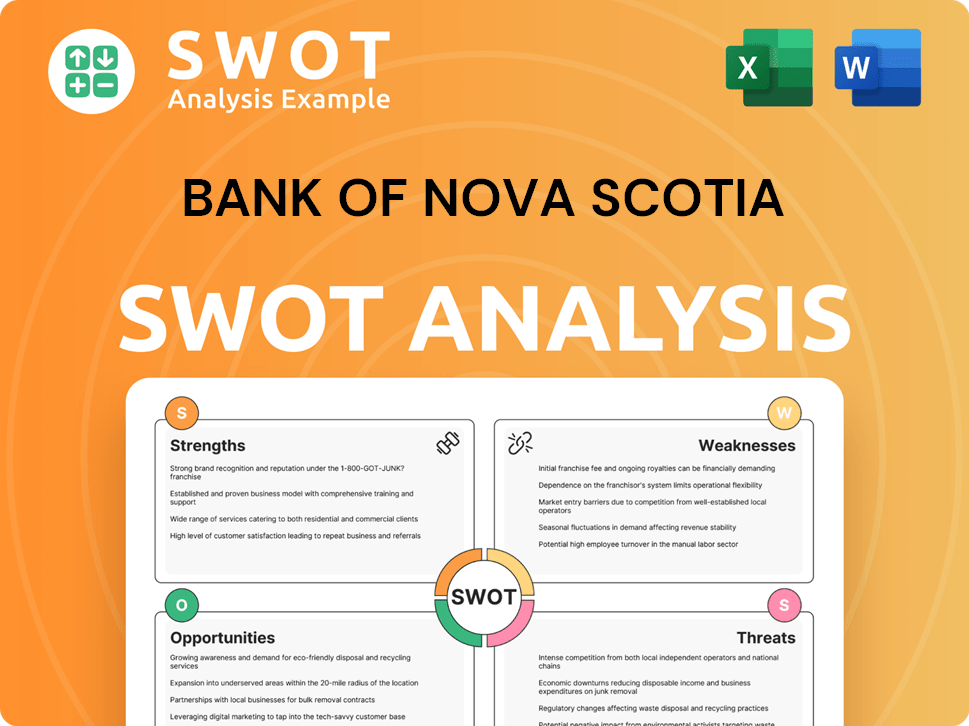

Strengths

Strong Presence in Canada and North America

Scotiabank's strong presence in Canada, holding a significant share of the Canadian deposit market, is a key strength. The bank strategically focuses on its priority markets in North America, including the United States and Mexico. This offers a unique advantage as the only bank operating at scale across this corridor. As of April 2024, Scotiabank's Canadian banking arm reported strong earnings, reflecting its robust domestic position.

Diversified Business Segments

Scotiabank's diverse business segments, including Canadian Banking, International Banking, Global Wealth Management, and Global Banking and Markets, are a significant strength. In Q1 2024, International Banking contributed 28% of total revenue, showcasing its importance. This diversification reduces reliance on any single market or product. This approach helps the bank manage risks effectively.

Focus on Digital Transformation

Scotiabank's strong focus on digital transformation is a key strength. They're boosting customer experience via mobile banking and AI. A partnership with Dalhousie University supports digital inclusion. In Q1 2024, digital sales were up 10% year-over-year, showing progress.

Solid Financial Performance in Key Areas

Scotiabank's strengths include solid financial performance in key areas. In fiscal year 2024, both Canadian and International Banking saw increased adjusted earnings. Global Wealth Management also performed well, driven by revenue growth. These results demonstrate Scotiabank's ability to generate earnings.

- Canadian Banking: Increased adjusted earnings in fiscal 2024.

- International Banking: Also showed increased adjusted earnings.

- Global Wealth Management: Strong revenue growth.

Commitment to Community Investment

Scotiabank's dedication to community investment is a notable strength. Initiatives like ScotiaRISE showcase its commitment to economic resilience, education, and newcomer inclusion. This involves substantial investments in programs designed to boost opportunities for individuals and families. In 2024, Scotiabank invested $65 million in ScotiaRISE.

- $65 million invested in ScotiaRISE in 2024.

- Focus on economic resilience, education, and newcomer inclusion.

Key Strengths Fueling Financial Performance

Scotiabank's robust Canadian presence and North American focus are key. Diverse segments like International Banking contribute significantly to revenue. Digital transformation efforts boost customer experience. These strengths drive earnings, as demonstrated by financial results.

| Strength | Details | Data |

|---|---|---|

| Canadian Presence | Significant market share | Strong domestic earnings (2024) |

| Diversified Segments | Multiple revenue streams | Int. Banking: 28% of revenue (Q1 2024) |

| Digital Transformation | Enhanced customer experience | Digital sales up 10% YoY (Q1 2024) |

Weaknesses

Underperformance Compared to Peers

Scotiabank's financial performance has lagged behind some competitors. Over the past five years, its stock has shown a total return of approximately 40%, while peers like TD Bank have seen returns closer to 60%. This underperformance highlights challenges in its international operations. Scotiabank's global footprint, particularly in Latin America, has faced economic headwinds. These markets often experience slower recoveries from economic downturns compared to North America, impacting overall profitability.

Challenges in Canadian Banking Segment

The Canadian banking segment faces headwinds, despite strengths in other areas. The segment, BNS's largest, is dealing with net interest margin compression. This has contributed to higher credit costs. Net income in this segment has declined recently. In Q1 2024, Canadian Banking net income was $2.2B, down from $2.4B in Q1 2023.

Exposure to International Market Risks

The Bank of Nova Scotia's international presence, while a growth driver, creates vulnerabilities. Economic instability in Latin America, where it has significant operations, poses a risk. In 2024, Scotiabank's net income from its international business was CAD 2.7 billion. This exposure makes the bank susceptible to market downturns. This could impact overall profitability.

Higher Operating Expenses

Higher operating expenses have been a challenge for Scotiabank, impacting its financial performance. The bank's efficiency ratio, a key metric, may face headwinds in meeting internal goals. For instance, in Q1 2024, Scotiabank's expenses rose, even as revenue increased. Management is actively working on cost-cutting measures, but the impact is still unfolding.

- Efficiency Ratio: Scotiabank's efficiency ratio was 55.4% in Q1 2024.

- Operating Expenses: Increased in Q1 2024, impacting overall profitability.

- Cost-Cutting: Ongoing initiatives to improve efficiency.

Impact of Asset Sales and Impairment Charges

Bank of Nova Scotia's strategic shifts, including selling international banking operations, have led to substantial impairment charges. These decisions, while aiming for a sharper focus, create short-term pain. For instance, in fiscal 2024, the bank recorded impairment charges related to its international operations. This can temporarily depress earnings.

- Impairment charges can reduce net income.

- Strategic sales may cause short-term financial hits.

- Focusing on core markets can lead to asset sales.

Scotiabank's Challenges: Underperformance, Costs, and Strategy

Scotiabank faces underperformance and net interest margin compression, affecting profitability in key segments. Economic instability in Latin America and higher operating expenses present challenges.

Strategic shifts, like selling international assets, lead to impairment charges, impacting short-term earnings. The bank's efficiency ratio and cost management are ongoing focus areas.

| Weakness | Details |

|---|---|

| Financial Underperformance | Stock return ~40% (5yr), lags peers like TD Bank at ~60%. |

| Efficiency Ratio | 55.4% in Q1 2024, faces headwinds. |

| Impairment Charges | In fiscal 2024 due to strategic shifts. |

Opportunities

Growth in North American Priority Markets

Scotiabank's strategic growth in Canada, the U.S., and Mexico is a key opportunity. The bank aims to increase its deposit share in Canada. It also plans to expand in the U.S. with investments. Finally, it will leverage the North American trade corridor. For instance, in Q1 2024, Scotiabank's Canadian banking net income was $1.07 billion.

Expansion of Digital Banking and Fintech Partnerships

Scotiabank can capitalize on the rising demand for digital banking and the shift towards consumer-focused services in Canada. This presents a chance to broaden its digital services and collaborate with fintech firms. In 2024, digital banking adoption in Canada continued to rise, with over 70% of Canadians using online banking regularly, according to recent reports. Investments in digital tech and AI can boost customer satisfaction and streamline operations.

Potential for Increased Lending Activity with Interest Rate Cuts

Anticipated interest rate reductions by the Bank of Canada and the Federal Reserve could spark higher lending, benefiting Scotiabank. Lower rates often boost both loan originations and mortgage activity. For instance, in 2023, the Canadian mortgage market experienced a slowdown due to high rates; a rate cut could reverse this trend. The bank can capitalize on increased borrowing demand.

Strengthening Wealth Management Business

Scotiabank's global wealth management arm presents a significant opportunity for expansion. This segment has demonstrated robust growth, with assets under management increasing. The bank can enhance this area by fostering deeper client connections. Tailored financial products and services can boost revenue.

- Wealth management revenue rose by 8% in fiscal 2024.

- Assets under management in the wealth division grew by 12% in the same period.

- Scotiabank aims to increase its wealth management market share by 15% by 2025.

Focus on Primary Client Relationships

Scotiabank prioritizes building primary client relationships to boost value. This strategy involves offering diverse products and services to deepen client engagement. As of Q1 2024, Scotiabank's Canadian Banking segment saw strong growth in primary client relationships, contributing to increased revenue. Focusing on existing clients is cost-effective and fosters loyalty.

- Increased cross-selling opportunities.

- Enhanced customer lifetime value.

- Improved profitability per client.

- Stronger market position.

Growth Strategies for a Financial Giant

Scotiabank can grow by expanding geographically. Digital banking is a major growth area. The wealth management arm is ripe for further expansion. These opportunities could significantly boost the bank's overall financial performance.

| Opportunity | Strategic Action | Financial Impact (Projected 2025) |

|---|---|---|

| Geographic Expansion | Increase deposit share in Canada and expand in U.S. | Increase in net income by 5% |

| Digital Banking | Expand digital services and collaborate with fintechs. | Cost savings of 3% in operational expenses |

| Wealth Management | Foster client connections and offer tailored services. | 15% growth in market share by 2025 |

Threats

Economic Uncertainty and Potential Downturns

The Bank of Nova Scotia (BNS) confronts economic headwinds. The sector faces risks from moderating economic growth and elevated household debt, especially in Canada. Though a major recession was avoided, uncertainties could still affect loan growth. In 2024, Canadian household debt-to-income ratio reached 178%.

Increased Competition in the Financial Sector

The Canadian financial sector, dominated by a few major players, faces rising competitive pressures. Initiatives like consumer-driven banking aim to boost competition, potentially eroding Scotia's market share. Lower switching costs for consumers could further intensify the battle for customers. This environment demands Scotia to innovate and improve services to maintain profitability, as evidenced by the 2024 trend of fintech partnerships.

Credit Market Volatility and Rising Credit Costs

Credit market volatility and rising credit costs are significant threats. Scotiabank faces modestly elevated credit costs as it heads into 2025. In Q1 2024, the bank reported a provision for credit losses of $813 million. Delinquencies could potentially increase. This could impact profitability.

Geopolitical Uncertainties and Trade Negotiations

Geopolitical uncertainties and trade negotiations pose significant threats to The Bank of Nova Scotia. Ongoing discussions, like those between Canada and the U.S., could destabilize markets. These uncertainties can introduce risks and affect economic growth, potentially impacting loan performance and investment portfolios. For example, in 2024, trade disputes led to a 2% decrease in global trade volume.

- Geopolitical instability can disrupt supply chains.

- Trade negotiations can create market volatility.

- Economic slowdowns can increase credit risk.

- Regulatory changes can increase compliance costs.

Cybersecurity and Data Privacy Risks

The Bank of Nova Scotia (BNS) faces growing cybersecurity and data privacy threats as it advances its digital transformation. Breaches can lead to significant financial losses and damage BNS's reputation, impacting customer trust. Recent reports indicate a rise in cyberattacks targeting financial institutions globally. BNS must invest heavily in robust security measures to safeguard sensitive customer data and maintain operational integrity.

- In 2024, cybercrime costs are projected to reach $9.5 trillion globally.

- Financial institutions are prime targets, with a 38% increase in attacks in the last year.

- Data breaches can result in fines and legal actions, as seen with other banks.

BNS Faces Economic Storm: Debt, Competition, and Risks

The Bank of Nova Scotia (BNS) is threatened by macroeconomic instability and high household debt, particularly in Canada, where the debt-to-income ratio was 178% in 2024. Competitive pressures, fueled by consumer-driven banking and fintech, could erode BNS's market share, demanding greater innovation. Rising credit costs and geopolitical uncertainties, alongside increased cybersecurity risks, also pose challenges for BNS's financial health.

| Threat | Impact | Data Point (2024/2025) |

|---|---|---|

| Economic Headwinds | Reduced loan growth, increased defaults | Canadian household debt-to-income ratio: 178% |

| Competition | Erosion of market share, need for innovation | Fintech partnerships growing; consumer switching costs lower. |

| Credit Market Volatility | Increased credit costs and potential for delinquencies. | Q1 2024 credit loss provision: $813 million. |

SWOT Analysis Data Sources

This SWOT analysis relies on data from financial reports, market analysis, and industry expert evaluations.