Sydbank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Sydbank Bundle

What is included in the product

Tailored exclusively for Sydbank, analyzing its position within its competitive landscape.

Easily visualize the Sydbank Porter's Five Forces with an intuitive, color-coded chart.

What You See Is What You Get

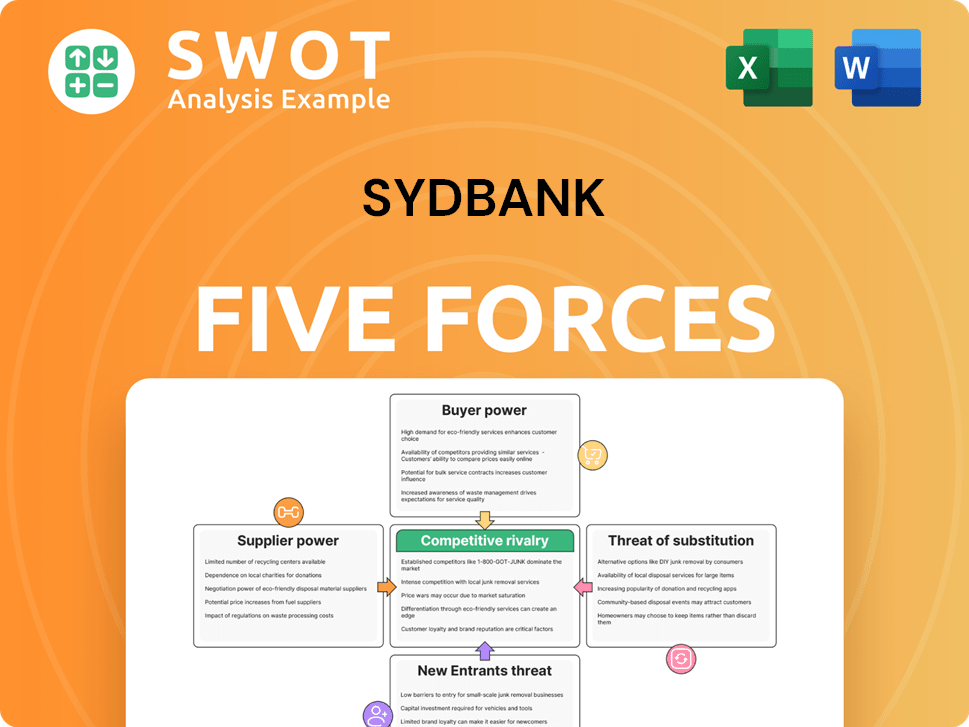

Sydbank Porter's Five Forces Analysis

This preview showcases the complete Sydbank Porter's Five Forces analysis you'll receive. It examines competitive rivalry, supplier power, buyer power, threat of substitutes, and threat of new entrants. The document provides a detailed, in-depth look at these forces, offering valuable insights. This is the document you get; no changes are made.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

Sydbank faces complex competitive pressures. The threat of new entrants is moderate due to capital requirements. Bargaining power of suppliers is low, as many exist. Buyer power is moderate due to alternative banking options. Rivalry among existing firms is intense. The threat of substitutes like fintech is growing.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sydbank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited Supplier Concentration

Sydbank, like other banks, depends on suppliers like tech and consulting firms. Concentrated suppliers, for core banking software, for example, have more power. In 2024, the global banking software market was valued at approximately $70 billion. This dependence means Sydbank must manage these relationships carefully. Diversification might be necessary to reduce supplier influence.

High Switching Costs

Switching costs are significant for core banking systems. The financial cost, implementation time, and operational disruptions can be substantial. For example, migrating a core banking system can cost a bank like Sydbank millions of euros and take several years. These high costs limit Sydbank’s flexibility.

Dependence on Specialized Expertise

Sydbank's dependence on specialized expertise, such as regulatory compliance and cybersecurity, grants suppliers significant power. These suppliers, crucial for operations, can dictate terms. In 2024, cybersecurity spending in the banking sector reached $20 billion globally. Sydbank must manage costs and risks tied to these critical suppliers.

Regulatory Compliance Requirements

Suppliers of regulatory compliance services, like those offering anti-money laundering (AML) solutions, hold significant bargaining power due to strict regulations. Sydbank, and other banks, rely heavily on these suppliers to meet regulatory demands. This dependence can escalate costs and limit Sydbank's negotiating strength. The global AML market was valued at $19.8 billion in 2023, with projections to reach $40.7 billion by 2030, highlighting this supplier power. The increasing regulatory complexity further strengthens their position.

- AML software market is projected to grow.

- Compliance costs are increasing.

- Regulatory demands are rising.

- Supplier dependency is a key factor.

Labor Market Dynamics

The labor market significantly influences Sydbank's operational costs. Skilled employees, such as financial analysts and IT specialists, are essential suppliers. Increased competition for talent drives up wages, affecting profitability. In 2024, the average salary for financial analysts in Denmark was approximately DKK 650,000 annually. A strong labor market gives employees leverage.

- Labor costs directly impact profitability, with salaries being a major expense.

- Competition for skilled workers can lead to higher operational costs.

- Employee bargaining power increases during periods of low unemployment.

- Staffing challenges may arise if Sydbank cannot offer competitive packages.

Sydbank: Supplier Power & Financial Impacts

Supplier bargaining power significantly impacts Sydbank's operations. High switching costs for core systems limit flexibility. Dependency on specialized expertise, like cybersecurity (with $20B spending in 2024), grants suppliers considerable power. Regulatory demands and the AML market ($19.8B in 2023, growing to $40.7B by 2030) further strengthen suppliers.

| Aspect | Impact on Sydbank | Data (2024) |

|---|---|---|

| Core Banking Systems | High switching costs limit flexibility. | Migration costs can reach millions of euros. |

| Cybersecurity | Dependence on specialized expertise. | Sector spending at $20B globally. |

| Regulatory Compliance (AML) | Rising costs and supplier power. | AML market valued at $19.8B in 2023. |

Customers Bargaining Power

Price Sensitivity

Customers' price sensitivity is heightened by digital banking and fintech. They now easily compare rates and fees, increasing their bargaining power. Sydbank must strategically balance pricing to stay competitive while maintaining profitability. In 2024, the average consumer switched banks for better rates, a trend impacting pricing strategies.

Availability of Alternatives

The rise of fintech and other financial services has given customers more options. These include peer-to-peer lending and mobile payment systems. Sydbank needs to stand out by offering unique services to compete. In 2024, the fintech market is expected to reach $190 billion.

Demand for Personalized Services

Customers increasingly seek personalized financial services, expecting banks to tailor solutions. This trend is evident; in 2024, 65% of banking customers preferred personalized offers. Sydbank needs robust data analytics and CRM systems to meet these demands. Investing in personalization can boost customer loyalty, as demonstrated by a 15% increase in retention rates for banks with strong CRM.

Switching Costs

Switching costs are diminishing due to tech advancements and rising competition. Digital platforms simplify fund transfers, easing the move between banks. In 2024, 68% of US consumers used online banking. Sydbank needs robust customer relationships and excellent service to deter customer churn. A focus on service can offset the impact of lower switching costs.

- Online banking usage in the US reached 68% in 2024.

- Digital platforms facilitate easier fund transfers.

- Customer relationships are crucial for Sydbank's retention.

- Excellent service mitigates churn despite lower switching costs.

Access to Information

Customers' access to information significantly impacts Sydbank's bargaining power. Online resources and comparison websites offer customers detailed insights into financial products, enabling informed decisions. This increased knowledge allows customers to negotiate more favorable terms with banks. Sydbank must prioritize transparent pricing and provide clear, accurate information to maintain a competitive edge. Data indicates that in 2024, online banking usage continues to rise, with over 70% of customers utilizing digital platforms for financial management.

- 70% of customers use digital platforms for banking.

- Transparency in pricing is crucial.

- Customers negotiate better terms.

- Sydbank must provide accurate information.

Navigating Price Wars and Fintech's Rise

Customers' bargaining power is amplified by digital tools and increased price sensitivity. This enables easy rate comparisons, prompting Sydbank to balance competitive pricing with profitability. Fintech competition is growing, with the market projected at $190 billion in 2024. Personalized services and robust customer relationships are crucial, with CRM improving retention rates.

| Factor | Impact | 2024 Data |

|---|---|---|

| Price Sensitivity | Higher due to comparison tools | Switching for better rates |

| Fintech Growth | Increased competition | $190B market |

| Personalization | Customer expectations | 65% prefer personalized offers |

Rivalry Among Competitors

Intense Competition

The Danish banking sector is fiercely competitive, with Sydbank battling for market share against major domestic and international banks. This competition is evident in pricing, with banks constantly adjusting interest rates and fees to attract customers. For example, in 2024, the average interest rate on new DKK loans was around 4.5%. The pressure also drives banks to innovate in services, such as digital banking and personalized financial advice.

Consolidation Trends

The banking sector's consolidation, marked by mergers and acquisitions, intensifies rivalry. Larger entities emerge, wielding significant economies of scale. In 2024, M&A activity in European banking totaled $35 billion. This creates a competitive environment where Sydbank must strategize. Sydbank's options include partnerships or acquisitions to stay competitive.

Focus on Digitalization

Digitalization is a fierce battleground for banks. In 2024, digital banking users surged, with mobile banking app usage up by 15% across Europe. Sydbank must keep pace. They are investing heavily in digital platforms and online services to remain competitive. It is critical to innovate and enhance its digital capabilities.

Differentiation Strategies

Banks are intensely competing, using differentiation to attract customers. They're targeting specific segments and offering specialized products. Superior customer service is another key differentiator. Sydbank needs a unique strategy to compete effectively.

- Digital banking services are growing rapidly, with 70% of adults using online banking in 2024.

- Wealth management services are a key area, with assets under management (AUM) projected to reach $145 trillion globally by the end of 2024.

- Customer experience is critical; 86% of customers are willing to pay more for a better experience.

- Sydbank's net interest income in 2023 was DKK 2.3 billion.

Regulatory Environment

The regulatory environment significantly influences competitive dynamics in the banking sector. Regulations affect operational costs and introduce both opportunities and risks for banks like Sydbank. Staying informed about regulatory changes is essential for Sydbank's strategic adaptability.

- In 2024, European banks faced increased regulatory scrutiny regarding capital requirements.

- The Danish Financial Supervisory Authority (Finanstilsynet) regularly updates banking regulations.

- Compliance costs can represent a substantial portion of a bank's operational budget.

- Sydbank's ability to navigate these changes impacts its competitive position.

Sydbank's Competitive Battle: Pricing, Digital, and M&A

Sydbank faces tough competition in Denmark’s banking sector, battling for market share through pricing and innovative services. Consolidation, with $35 billion in M&A in 2024, intensifies rivalry, demanding strategic responses like partnerships. Digitalization is crucial; 70% use online banking, urging Sydbank's investment in digital platforms to compete effectively. Customer experience matters; 86% pay more for it.

| Competitive Factor | Impact on Sydbank | 2024 Data |

|---|---|---|

| Interest Rate Competition | Affects profitability | Avg. DKK loan rate ~4.5% |

| Digital Banking Adoption | Requires digital investment | Mobile banking app usage up 15% |

| M&A Activity | Shifts market structure | European banking M&A: $35B |

SSubstitutes Threaten

Fintech Disruption

Fintech companies pose a significant threat to traditional banks like Sydbank. They offer alternatives like mobile payments, peer-to-peer lending, and robo-advisors. For example, the global fintech market was valued at $112.5 billion in 2020 and is projected to reach $698 billion by 2030. Sydbank must innovate to compete effectively. This includes offering similar services and improving customer experience.

Non-Bank Financial Institutions

Non-bank financial institutions (NBFIs) like credit unions and insurance companies offer alternatives to Sydbank's services. These entities often benefit from reduced overhead, potentially leading to more competitive pricing. In 2024, NBFIs managed assets totaling trillions, indicating their significant market presence. Sydbank must analyze these competitors to maintain its market share and competitive edge.

Digital Payment Solutions

Digital payment solutions pose a significant threat to Sydbank. The adoption of mobile wallets and online platforms is surging, reducing the reliance on traditional banking. In 2024, mobile payment transactions in Europe reached €1.5 trillion, a 20% increase. To stay competitive, Sydbank needs to integrate these technologies.

Alternative Investments

The threat of substitutes for Sydbank is growing due to the rise of alternative investments. Cryptocurrencies and peer-to-peer lending are attracting investors, potentially diverting funds from traditional banking products. To stay competitive, Sydbank needs to analyze these alternatives and their impact on its market share. A strategic move could involve offering its own alternative investment options to meet evolving investor demands. In 2024, the crypto market cap reached $2.6 trillion, indicating significant investor interest.

- Cryptocurrencies: Market cap reached $2.6T in 2024.

- Peer-to-peer lending: Increasing popularity, especially in areas with limited access to traditional banking.

- Sydbank: Must assess the competitive landscape and consider offering alternative investment products.

Direct Lending

Direct lending presents a growing threat to Sydbank as platforms connect borrowers directly with investors, bypassing traditional banking. This shift can decrease demand for Sydbank's loans, potentially squeezing interest rate margins. To counter this, Sydbank needs to strengthen borrower relationships and offer highly competitive loan products. In 2024, direct lending volumes continued to climb, with some estimates suggesting a 15% year-over-year increase in certain markets.

- Increased competition from alternative lenders.

- Potential for reduced loan demand.

- Pressure on interest rate spreads.

- Need for relationship-focused strategies.

Sydbank's Rivals: Fintech, NBFIs, and Digital Payments

Substitute threats to Sydbank include fintech, NBFIs, and digital payment solutions, each impacting traditional banking. Alternative investments like crypto and P2P lending also divert funds, increasing competition. Direct lending platforms offer loans, potentially squeezing interest margins.

| Threat | Impact | 2024 Data |

|---|---|---|

| Fintech | Alternative Services | Global market: $698B by 2030 |

| NBFIs | Competitive Pricing | Trillions in Assets |

| Digital Payments | Reduced Reliance on Banks | €1.5T transactions in Europe |

Entrants Threaten

High Capital Requirements

The banking sector demands substantial capital, creating a high entry barrier. New banks face strict capital adequacy rules, challenging to fulfill. In 2024, starting a bank might need over $100 million. This protects existing banks like Sydbank from new competitors.

Stringent Regulatory Environment

The banking sector faces stringent regulations, demanding extensive licensing and compliance. New entrants struggle with this complex landscape. Sydbank's established expertise gives it an advantage. In 2024, regulatory costs for banks rose by 7%, impacting new ventures. This creates a significant barrier.

Brand Reputation and Trust

Brand reputation and trust are paramount in banking. Customers often favor established institutions for financial security. Sydbank, with its history in Denmark, benefits from this trust. New entrants face challenges in building brand recognition. According to 2024 reports, acquiring customer trust can cost millions.

Economies of Scale

Established banks like Sydbank have a significant advantage due to economies of scale. This allows them to provide financial products and services at more competitive prices. New entrants often find it challenging to match these cost efficiencies. In 2024, Sydbank's operational expenses were approximately DKK 1.8 billion, reflecting its established infrastructure. This cost advantage strengthens Sydbank's position.

- Sydbank's operational expenses in 2024 were around DKK 1.8 billion.

- Economies of scale enable lower service costs for established banks.

- New entrants face difficulties competing on price.

- Sydbank's infrastructure provides a cost advantage.

Access to Distribution Channels

Sydbank, like other established banks, benefits from extensive distribution channels, including physical branches, online banking portals, and mobile applications, providing a significant competitive advantage. New entrants face considerable hurdles in replicating such widespread access to customers. This advantage is reflected in market share and customer reach. For instance, in 2024, a major Danish bank reported that over 70% of its customers actively used its digital banking platforms. New banks often struggle to match this level of accessibility, impacting their ability to attract and retain customers.

- Established banks have well-developed distribution networks.

- New entrants face challenges in gaining access to these channels.

- Sydbank's distribution network is a key advantage.

- Digital banking adoption is high among established banks' customers.

Sydbank's Fortress: Entry Barriers Explained

The banking sector's high entry barriers protect existing firms like Sydbank. Capital requirements, potentially exceeding $100 million in 2024, are a major hurdle. Regulatory compliance, with costs up 7% in 2024, adds to the challenge for new entrants.

| Factor | Impact on New Entrants | 2024 Data |

|---|---|---|

| Capital Needs | High Investment | >$100M to start a bank |

| Regulatory Costs | Increased Expenses | Up 7% in 2024 |

| Brand Trust | Difficult to Build | Millions to acquire trust |

Porter's Five Forces Analysis Data Sources

Our Sydbank analysis uses annual reports, market research, financial data, and industry publications for thorough insights.