Ulta Beauty Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Ulta Beauty Bundle

What is included in the product

Analyzes Ulta Beauty's competitive landscape, evaluating forces impacting profitability and sustainability.

Easily adjust the analysis to gauge Ulta's competitive stance as industry pressures shift.

Preview the Actual Deliverable

Ulta Beauty Porter's Five Forces Analysis

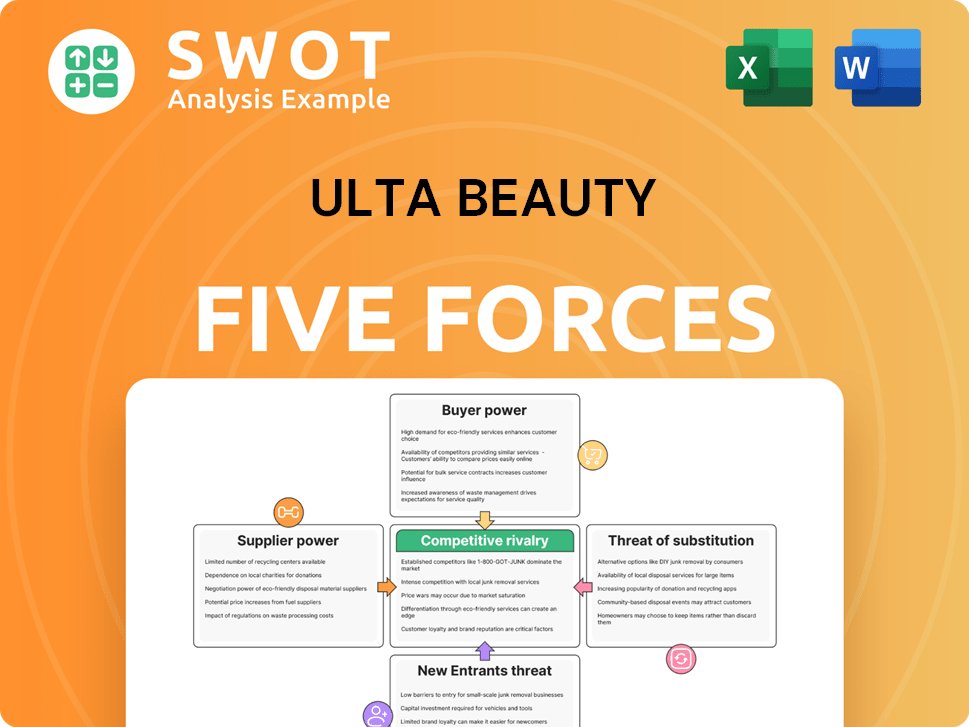

This is a comprehensive Porter's Five Forces analysis of Ulta Beauty. It examines the competitive forces shaping the company's industry. The document covers all five forces: threat of new entrants, bargaining power of suppliers, bargaining power of buyers, threat of substitutes, and rivalry among existing competitors. You're previewing the complete analysis—the same in-depth document you'll receive immediately after purchase.

Porter's Five Forces Analysis Template

Don't Miss the Bigger Picture

Ulta Beauty faces moderate rivalry, driven by competitors like Sephora and mass retailers. Buyer power is significant due to consumer choice and brand loyalty. Supplier power is limited, as various brands and distributors exist. The threat of new entrants is moderate, with high start-up costs. Substitute products pose a threat, including online retailers and direct-to-consumer brands.

The complete report reveals the real forces shaping Ulta Beauty’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Concentration

Ulta Beauty faces supplier concentration risk, with major brands like Estée Lauder and L'Oréal holding significant sway. These suppliers provide a large portion of Ulta's inventory, giving them negotiating power. In 2024, Estée Lauder's sales were around $15.9 billion, emphasizing their market influence. Price hikes or unfavorable terms from these key suppliers could hurt Ulta's profits. Managing these supplier relationships is vital for Ulta's success.

Brand Power

Ulta Beauty faces supplier power challenges due to strong brand recognition. Prestige brands, highly sought by consumers, dictate terms. These brands control pricing and placement within Ulta stores. Ulta's negotiation leverage is limited; customers pay premiums for these products. In 2024, Ulta's cost of goods sold was around 55% of revenue.

Product Differentiation

Suppliers with unique products, like those with patents, hold more power. Ulta Beauty depends on these to draw customers and stay competitive. For example, in 2024, exclusive skincare brands saw a 15% sales increase. The more unique the product, the less Ulta can negotiate. This is true for innovative skincare or exclusive cosmetic lines.

Switching Costs

Switching suppliers in the beauty industry, like for Ulta Beauty, can be costly due to factors like reformulation, packaging, and marketing. These costs can make Ulta less likely to aggressively negotiate with current suppliers. Consider that in 2024, Ulta's cost of goods sold was around 57% of revenue, showing the impact of supplier costs.

- Reformulation costs: Vary by product, potentially reaching $10,000-$50,000.

- Packaging adjustments: Can range from $5,000-$25,000 depending on complexity.

- Marketing changes: Budgeted at 10-20% of the product's retail price.

- Customer disruption: Potential loss of sales during brand transitions.

Exclusive Arrangements

Ulta Beauty's exclusive supplier arrangements help manage supplier power. These deals offer unique products, boosting customer appeal and sales. However, they also create dependency on specific vendors. In 2024, Ulta's strategic brand partnerships contributed significantly to its revenue growth. Maintaining a balance is key.

- Exclusive brands drive sales, as seen in Ulta's 10% sales increase in Q3 2024.

- Dependency on key suppliers can limit flexibility in pricing and product offerings.

- Strategic brand diversification helps mitigate supplier influence.

- Ulta's focus on a mix of exclusive and non-exclusive products is crucial for long-term stability.

Supplier Dynamics: Shaping Beauty Retail

Ulta Beauty's suppliers, like Estée Lauder, hold considerable power. They provide essential, in-demand products, influencing Ulta's profitability. Exclusive and unique brands strengthen supplier control, limiting Ulta's negotiation leverage. Switching costs and strategic brand deals further shape this dynamic, impacting Ulta's margins. In 2024, Ulta’s net sales reached approximately $11.2 billion, highlighting the importance of effectively managing these supplier relationships.

| Factor | Impact on Supplier Power | Financial Implication (2024) |

|---|---|---|

| Brand Recognition | High demand for prestige brands | 55% Cost of Goods Sold |

| Product Uniqueness | Patents & exclusivity increase leverage | 15% sales increase (exclusive brands) |

| Switching Costs | High costs decrease negotiation | Reformulation: $10K-$50K |

Customers Bargaining Power

Price Sensitivity

Beauty consumers show price sensitivity, particularly with mass-market brands and daily items, pushing Ulta to offer competitive pricing. Online price comparisons make it easy for customers to switch, impacting Ulta's pricing strategies. In 2024, the beauty market saw intense price competition, with many brands offering discounts. Ulta's pricing must stay competitive to retain its customer base. This limits Ulta's ability to increase prices without losing customers.

Product Availability

Many beauty products are widely available from various retailers, including drugstores, department stores, and online platforms. This extensive product availability significantly boosts customer bargaining power. Consumers can easily switch retailers, which increases competition. In 2024, the beauty industry's online sales reached $26.7 billion, reflecting this shift.

Brand Loyalty

Brand loyalty in the beauty sector is generally moderate. Consumers often explore new products, particularly those trending or influencer-endorsed. This willingness to switch reduces individual brand influence. Consequently, customer bargaining power is elevated as they aren't confined to a single brand or retailer. Ulta's diverse offerings cater to this behavior, with 2024 sales showing a continued shift towards diverse brand exploration.

Information Availability

Customers' bargaining power at Ulta Beauty is heightened by easy access to information. Online reviews, social media, and beauty blogs provide a wealth of data for informed decisions. This allows for product comparisons and the ability to seek the best deals. In 2024, Ulta's digital sales reached $3.1 billion, showing the impact of online information on consumer behavior.

- Digital sales influence consumer choice.

- Consumers easily compare product information.

- Informed customers seek better deals.

Loyalty Programs

Ulta Beauty's Ultamate Rewards program is a significant tool in managing customer bargaining power. This program offers exclusive discounts, rewards, and personalized offers, aiming to enhance customer retention. In 2024, Ulta Beauty's loyalty program included millions of members, contributing to customer stickiness. However, the program's effectiveness is limited by customers' ability to switch to competitors. Ulta aims to grow its loyalty base to 50 million members by 2028.

- Ultamate Rewards members benefit from exclusive deals and offers.

- The loyalty program aims to increase customer retention.

- Customer can switch to competitors if they find better deals.

- Ulta Beauty plans to reach 50 million loyalty members by 2028.

Beauty Shoppers Dictate the Market: Pricing, Choice, and Digital Dominance

Customers exert considerable power over Ulta Beauty. Price sensitivity and online comparisons intensify this, encouraging competitive pricing. Availability of beauty products from various retailers bolsters customer choice, increasing competition. In 2024, digital sales reached $3.1 billion, with online information driving informed decisions.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Price Sensitivity | Forces Competitive Pricing | Intense price competition among brands |

| Product Availability | Boosts Customer Choice | Online sales reached $26.7 billion |

| Information Access | Informed Decisions | Ulta's digital sales: $3.1 billion |

Rivalry Among Competitors

Intense Competition

The beauty retail market is incredibly competitive, featuring many businesses striving for market share. Ulta Beauty competes with Sephora and department stores such as Nordstrom. Drugstores like CVS and mass retailers like Target also pose competition. This high level of rivalry forces Ulta to stand out and provide attractive pricing. In 2024, the beauty industry's revenue is projected to reach $716 billion.

Market Share

Ulta Beauty maintains a substantial market share within the beauty retail industry. The market's fragmented nature means no single entity reigns supreme. Ulta's market share faces persistent challenges from rivals, necessitating ongoing innovation and strategic adjustments. Notably, Ulta experienced its first market share decline in 2024. In 2024, Ulta's market share was around 11.8%.

Differentiation

Ulta Beauty distinguishes itself with a broad product selection, featuring mass-market and luxury brands, plus salon services. Competitors are also enhancing their offerings, forming exclusive partnerships, and improving customer experiences. For instance, Sephora, Ulta's main rival, reported $9.3 billion in 2023 sales. Maintaining a strong, differentiated value is key for Ulta in this competitive landscape.

Online vs. In-Store

Competitive rivalry in the beauty retail sector has increased due to online retailers and direct-to-consumer brands. Ulta Beauty faces competition from online platforms offering convenience and often lower prices. To combat this, Ulta is investing in its online presence and omnichannel strategies. E-commerce significantly impacts beauty sales, with Amazon playing a key role. The beauty industry's online sales were substantial in 2024.

- Online sales growth continues to impact the beauty industry.

- Ulta's omnichannel strategy is crucial for maintaining its market position.

- Amazon remains a dominant player in online beauty retail.

- Competitive pressures require continuous innovation.

Promotional Activity

The beauty retail sector sees intense promotional activity like discounts and loyalty programs. This can squeeze profit margins and increase rivalry among competitors. Ulta Beauty needs a careful promotional strategy to balance sales growth with financial health. In 2023, Ulta's gross profit margin was around 38.5%. Ulta anticipates a stable promotional environment in 2025.

- Intense promotions erode profit margins.

- Ulta's 2023 gross profit margin was approximately 38.5%.

- Loyalty programs increase competitive pressure.

- Ulta aims for a balanced promotional approach.

Ulta's Market Share Faces Intense Competition

Competitive rivalry in beauty retail is fierce, with many players vying for market share. Ulta battles Sephora, department stores, and mass retailers, and it must continually innovate to stand out. Ulta's market share dipped in 2024, signaling intense competition.

| Metric | 2023 | 2024 (Projected) |

|---|---|---|

| Beauty Industry Revenue (Billion USD) | $680 | $716 |

| Ulta Market Share (%) | 12.1% | 11.8% |

| Ulta Gross Profit Margin (%) | 38.5% | (Stably projected) |

SSubstitutes Threaten

Other Retailers

Customers have numerous options for beauty products beyond Ulta. Competitors include drugstores, department stores, and online retailers. The presence of substitutes impacts Ulta's pricing ability. In 2024, the beauty market saw significant growth, with online sales increasing by 15%.

Direct-to-Consumer Brands

The rise of direct-to-consumer (DTC) beauty brands poses a notable threat of substitutes for Ulta Beauty. DTC brands often provide unique products, personalized experiences, and competitive pricing. In 2023, these brands captured 12.7% of the total beauty market share, pulling customers from traditional retailers. Ulta must adapt by offering exclusive brands and boosting its online presence to compete effectively.

Subscription Boxes

Subscription beauty boxes pose a threat by offering curated product selections delivered regularly. These boxes can substitute for individual Ulta purchases. The subscription box market was valued at $26.3 billion in 2023. Ulta must enhance its in-store and online experience to compete effectively. Ulta's 2024 revenue is expected to reach $11.6 billion.

DIY Beauty

The "DIY beauty" trend presents a threat to Ulta Beauty as some consumers opt for homemade beauty solutions, using natural ingredients or DIY kits. This shift acts as a substitute for buying Ulta's manufactured products, potentially impacting sales. To counter this, Ulta could offer high-quality ingredients and educational resources, appealing to DIY enthusiasts. This strategic move could transform a threat into an opportunity, enhancing customer engagement and loyalty.

- In 2024, the global DIY beauty market was valued at approximately $3.5 billion.

- Ulta's net sales for Q3 2024 were $2.5 billion, showing the importance of maintaining market share.

- Offering DIY resources could diversify Ulta's revenue streams and customer engagement.

No Purchase

Consumers always have the option to not buy beauty products, which acts as a direct substitute to Ulta's offerings, especially during economic hardships. This "no purchase" scenario is a significant threat, as it directly impacts Ulta's sales. Ulta aims to counter this by highlighting the value and emotional benefits of its products and services, such as self-care. In 2024, the beauty industry saw fluctuations, with some consumers cutting back on non-essential spending.

- Economic downturns can significantly increase the "no purchase" threat.

- Ulta's marketing strategies focus on value and self-care to mitigate this.

- The beauty industry's performance in 2024 reflects consumer spending trends.

- Promotions and loyalty programs help retain customers during tough times.

Ulta's Rivals: Navigating the Beauty Battleground

The threat of substitutes significantly impacts Ulta Beauty by offering consumers diverse choices, including online retailers, DTC brands, and subscription services. The availability of alternatives influences Ulta's pricing and market strategies. Ulta must adapt through exclusive offerings and enhanced customer experiences.

| Substitute Type | Market Impact (2024) | Ulta's Response |

|---|---|---|

| DTC Brands | 12.7% market share (2023) | Exclusive brands, online presence |

| Subscription Boxes | $26.3B market (2023) | Enhanced in-store/online experience |

| DIY Beauty | $3.5B market (2024) | High-quality ingredients, educational resources |

Entrants Threaten

High Capital Requirements

Launching a beauty retail business, like Ulta Beauty, demands considerable upfront investment. Building a wide product selection, setting up physical stores, and creating a strong online presence all require substantial capital. This high capital requirement significantly deters new entrants. In 2024, establishing a retail chain similar to Ulta Beauty could easily require hundreds of millions of dollars, acting as a major barrier.

Brand Relationships

Ulta Beauty's established brand relationships pose a significant barrier to new entrants. Cultivating relationships with over 600 beauty brands, particularly prestige ones, is a lengthy process. Securing access to sought-after brands is challenging, with Ulta Beauty's existing partnerships giving them an edge. In 2024, Ulta's partnerships with brands like MAC and Benefit Cosmetics, which account for a large portion of its revenue, showcase the power of these relationships. New competitors struggle to replicate these key supplier agreements.

Supply Chain Complexity

Managing a complex supply chain poses a major hurdle for new beauty retailers. Ulta Beauty's established supply chain provides a competitive edge. New entrants face the challenge of building efficient supply chain management. In 2024, supply chain disruptions increased operational costs by up to 15% for new businesses.

Brand Loyalty and Recognition

Ulta Beauty benefits from strong brand recognition and customer loyalty, a significant barrier to new entrants. Building brand awareness is expensive and time-consuming, putting new competitors at a disadvantage. Ulta's Ultamate Rewards program, with 44.6 million active members as of 2024, fosters customer retention and repeat business. This loyal customer base provides a competitive edge against newcomers.

- Brand Reputation: Ulta's established presence.

- Customer Loyalty: High retention rates.

- Ultamate Rewards: 44.6 million members.

- Competitive Advantage: Barriers for new entrants.

E-commerce Expertise

The beauty retail sector's modern success hinges on strong e-commerce. New entrants must build user-friendly websites, mobile apps, and online marketing strategies. Ulta Beauty, for instance, has invested heavily in this area. They allocated a substantial $450 million digital transformation budget in 2024.

- E-commerce capabilities are crucial for success.

- New entrants need to invest in online platforms and marketing.

- Ulta Beauty's 2024 digital transformation budget was $450 million.

Ulta's Competitive Landscape: New Entrant Analysis

The threat of new entrants to Ulta Beauty is moderate. High capital requirements, including the costs of building a brand and establishing an online presence, act as a barrier. Established brand relationships and supply chain complexities further deter new competitors. However, the market's growth and innovation do provide opportunities.

| Barrier | Description | Impact |

|---|---|---|

| Capital Needs | Building stores, inventory, & online presence. | High |

| Brand Relationships | Existing partnerships with key brands. | High |

| Supply Chain | Established logistics. | Moderate |

Porter's Five Forces Analysis Data Sources

We use Ulta's financial reports, competitor data, and industry research from sources like Statista and IBISWorld.