Veritex Community Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Veritex Community Bank Bundle

What is included in the product

Tailored exclusively for Veritex Community Bank, analyzing its position within its competitive landscape.

Swap in your own data, labels, and notes to reflect current business conditions.

Same Document Delivered

Veritex Community Bank Porter's Five Forces Analysis

This preview showcases the comprehensive Veritex Community Bank Porter's Five Forces analysis. You'll receive the identical, fully detailed document after your purchase. It includes an in-depth examination of the bank's competitive landscape. The analysis thoroughly covers all five forces with expert insights. This means immediate access, no hidden components.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

Veritex Community Bank operates within a competitive banking landscape, influenced by factors like buyer power and the threat of substitutes. Its success hinges on navigating these challenges effectively. The analysis reveals moderate rivalry among existing competitors and a manageable threat from new entrants. This snapshot provides a glimpse of the bank's market dynamics.

Ready to move beyond the basics? Get a full strategic breakdown of Veritex Community Bank’s market position, competitive intensity, and external threats—all in one powerful analysis.

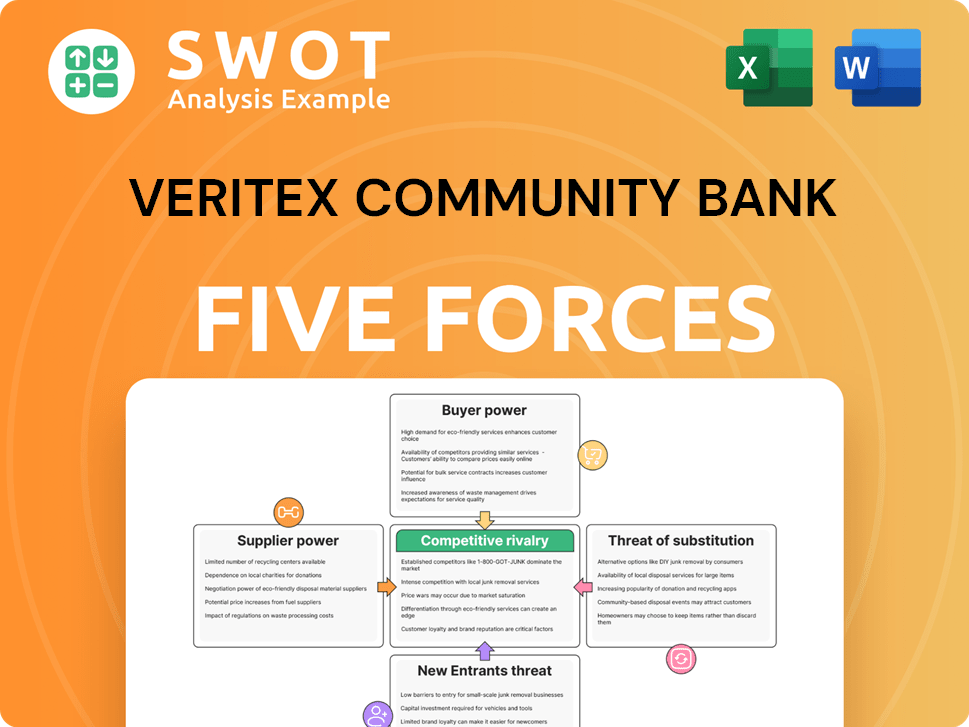

Suppliers Bargaining Power

Supplier Power: Tech Vendors

Veritex Community Bank depends on tech vendors. Key suppliers include Fiserv, Jack Henry, and FIS Global. These limited options boost supplier power. Banking's AI spending, projected at $20.3 billion in 2024, enhances vendor leverage. This concentrated market gives vendors significant influence over Veritex.

Supplier Power: Labor Market

Veritex Community Bank faces supplier power challenges within the labor market. The banking industry heavily relies on skilled labor such as tellers, loan officers, and IT specialists. Competition for talent, particularly in cybersecurity and technology, strengthens the bargaining power of employees. According to the Bureau of Labor Statistics, the finance and insurance sector employed over 6.2 million people in 2023. Hybrid work policies further influence talent retention strategies.

Supplier Power: Data Providers

Veritex Community Bank relies on financial data for operations. The cost of data from providers like Bloomberg and Refinitiv is significant. In 2024, data subscriptions can range from $20,000 to over $100,000 annually depending on services needed. Dependence on specific data sources increases supplier power, especially for exclusive data.

Supplier Power: Core System Vendors

Veritex Community Bank faces supplier power challenges, especially from core system vendors. Switching core banking systems is costly and disruptive, increasing vendor influence. Dependence on vendors like Fiserv gives them substantial bargaining power. Strategic partnerships can help, but also create reliance.

- Fiserv reported $18.23 billion in revenue in 2023.

- The cost to switch core banking systems can range from $5 million to $10 million.

- Approximately 70% of U.S. banks use a core system from one of the top three vendors.

- Long-term contracts with core banking providers often span 5-7 years.

Supplier Power: Regulatory Compliance

Veritex Community Bank confronts supplier power, particularly in regulatory compliance. Community banks are under growing regulatory scrutiny, increasing their dependence on compliance service providers. This reliance stems from the need for specialized expertise and software, which drives up costs. The evolving regulatory landscape strengthens these suppliers' position.

- Compliance costs for banks rose, with the average bank spending $230,000 annually in 2024.

- The regulatory compliance market is valued at approximately $60 billion as of 2024.

- Consulting fees have increased 15% due to demand.

- Banks now allocate 10-15% of their IT budgets to compliance.

Veritex's Supplier Power Dynamics: A Deep Dive

Veritex faces high supplier power across tech and labor. Key vendors like Fiserv hold significant leverage. Compliance and data costs add to supplier challenges.

| Supplier Type | Impact on Veritex | Data Point (2024) |

|---|---|---|

| Core Banking Vendors | High bargaining power | Switching costs: $5M-$10M |

| IT and Cybersecurity | Increased labor costs | Industry employment: 6.2M+ |

| Data Providers | Elevated subscription costs | Data subscriptions: $20K-$100K+ |

Customers Bargaining Power

Customer Power: Rate Sensitivity

Customers' rate sensitivity has intensified, particularly amid rising interest rates. In 2024, the Federal Reserve maintained higher rates. Depositors are inclined to move funds to institutions offering better yields. Veritex needs to balance deposit growth and competitive rates to retain customers.

Customer Power: Digital Expectations

Customers now demand smooth digital banking, like mobile apps and easy online account opening. Big banks and fintechs set a high bar with their digital platforms, raising customer expectations. In 2024, 89% of U.S. adults use online banking. Community banks, like Veritex, need to update their tech to stay relevant. Banks invested $30 billion in digital transformation in 2023.

Customer Power: Loan Terms

SMBs need flexible loan terms and fast financing, driving customer power. Fintech lenders and big banks intensify competition, impacting community banks. Veritex, like others, must adjust lending approaches. Personalized service and strong relationships can set them apart. In 2024, the US saw a 3.6% increase in SMB loan applications.

Customer Power: Service Personalization

Customers today highly value personalized service and financial solutions tailored to their specific needs. While community banks like Veritex excel in relationship-building, even larger institutions are enhancing their personalization efforts. Offering customized financial products and services is essential for customer retention in the competitive banking landscape. In 2024, banks that effectively personalize services see a 15-20% increase in customer satisfaction scores.

- Personalized service drives customer loyalty.

- Banks are investing in personalization technologies.

- Customized offerings are a key differentiator.

- Customer satisfaction is directly linked to personalization.

Customer Power: Switching Costs

Individual Veritex Community Bank customers have minimal bargaining power. However, larger groups and corporate clients wield more influence. Banks aim to boost switching costs to retain customers. They encourage multiple account usage and service adoption. For instance, in 2024, around 60% of banks are focusing on customer retention strategies.

- Corporate clients negotiate favorable terms.

- HNWIs demand personalized service.

- Banks offer bundled services to lock in clients.

- Switching costs include fees and time investment.

Veritex's Customer Power: Rates, Digital, and SMB Loans

Customer bargaining power at Veritex hinges on rate sensitivity and digital banking demands. SMBs seek flexible loan terms amid fintech competition, influencing Veritex. Banks prioritize personalized services to retain clients. Customer satisfaction correlates with personalized offerings.

| Aspect | Details | Data (2024) |

|---|---|---|

| Rate Sensitivity | Deposit movement based on rates | 89% US adults use online banking |

| Digital Banking | Demand for easy online access | Banks invested $30B in digital transformation (2023) |

| SMB Loans | Need for flexible terms | SMB loan applications increased 3.6% |

Rivalry Among Competitors

Rivalry: Large vs. Community Banks

Veritex Community Bank contends with formidable rivalry from larger national and regional banks. These larger institutions boast significantly greater resources, enabling substantial investments in cutting-edge technology and expansive marketing campaigns. Community banks, like Veritex, must strategically differentiate themselves by emphasizing personalized customer service and leveraging their deep understanding of local markets. In 2024, national banks held approximately 50% of total U.S. banking assets, highlighting the competitive landscape.

Rivalry: Fintech Competition

Fintech firms, like PayPal and Square, intensify competition by offering digital payments and online lending. Their user-friendly platforms attract customers, pressuring community banks. In 2024, fintech transaction values reached $1.1 trillion, highlighting their growing influence. Veritex must modernize to stay competitive.

Rivalry: Market Saturation

The Texas banking sector is intensely competitive. With approximately 370 community banks, the market is saturated. This high level of competition pressures Veritex's profit margins. Veritex Community Bank faces significant rivalry for market share in Texas's crowded banking environment.

Rivalry: Consolidation

The banking sector is seeing a wave of consolidation, with mergers and acquisitions reshaping the competitive landscape. These mergers often result in larger, more efficient banks, intensifying competition. For community banks like Veritex, merging might be a strategic move to boost their scale and competitiveness. In 2024, the industry witnessed several significant mergers, reflecting this trend.

- Mergers and acquisitions in the banking sector increased by 15% in Q3 2024.

- Community banks are facing pressure to consolidate to reduce operational costs.

- Large banks are acquiring smaller ones to expand their market share.

- The trend is expected to continue into 2025.

Rivalry: Credit Quality

Maintaining credit quality is crucial for Veritex Community Bank. Competition for loans can push banks toward riskier lending. Economic uncertainty and rising credit costs increase pressure. Fintech and larger banks challenge market share.

- Veritex's Q4 2023 net charge-offs were 0.16%.

- Community banks face increased competition, impacting credit quality.

- Economic downturns amplify credit risk.

- Fintechs and larger banks offer alternative lending options.

Texas Bank's Fight: Big Banks & Fintechs

Veritex Community Bank faces tough competition from big banks and fintech firms. The Texas banking market, with roughly 370 community banks, is highly competitive, pressuring profits. The industry is consolidating with mergers and acquisitions increasing, especially in Q3 2024.

| Aspect | Details |

|---|---|

| Market Share | National banks hold ~50% of U.S. banking assets in 2024. |

| Fintech Impact | Fintech transactions reached $1.1T in 2024. |

| M&A Activity | Banking sector M&A increased by 15% in Q3 2024. |

SSubstitutes Threaten

Substitution: Fintech Alternatives

Fintech firms provide substitutes like mobile payments and online lending, challenging traditional banking. These alternatives can replace services offered by community banks. In 2024, digital payments grew, with mobile transactions up by 25% globally. Community banks must evolve to compete and retain customers.

Substitution: Credit Unions

Credit unions pose a threat to Veritex Community Bank by offering comparable services, frequently at more favorable terms. They can serve as a substitute, especially for retail customers seeking better rates and lower fees. In 2024, credit unions held about $2.1 trillion in assets, highlighting their substantial market presence. To counter this, Veritex must differentiate itself through superior service and unique offerings.

Substitution: Non-bank Lenders

Non-bank lenders are a significant threat, offering alternative financing through online platforms and peer-to-peer lending. These entities often provide quicker and more flexible loan options. In 2024, fintech lending grew, capturing a larger market share, and putting pressure on traditional banks. Veritex Community Bank must compete by improving its speed and adaptability to retain customers.

Substitution: Digital Payment Platforms

Digital payment platforms, including PayPal and Apple Pay, pose a threat by offering alternatives to traditional banking. These platforms facilitate transactions, potentially reducing reliance on conventional banking services. Veritex Community Bank must integrate with or compete against these platforms to stay relevant. The rise of digital payments is evident, with mobile payment transactions in the U.S. reaching $1.5 trillion in 2023.

- Mobile payment users in the U.S. are projected to reach 150 million by 2025.

- PayPal processed $1.53 trillion in total payment volume in 2023.

- Apple Pay's transaction value in 2023 was approximately $1 trillion.

Substitution: Investment Alternatives

The threat of substitutes for Veritex Community Bank involves alternative investment options that compete with traditional banking products. Cryptocurrencies and peer-to-peer lending platforms offer potential customers higher returns, drawing funds away from conventional savings and investment accounts. To stay competitive, Veritex must provide attractive investment options and services. The bank should consider diversifying its portfolio and improving its digital offerings.

- Cryptocurrency market capitalization reached $2.6 trillion in 2024.

- Peer-to-peer lending volumes grew by 15% in 2024.

- Veritex's net interest margin was 3.2% in Q4 2024.

- Digital banking adoption increased by 20% in 2024.

Banking's Shifting Sands: Rivals Emerge

Veritex faces substitutes like fintech, credit unions, and non-bank lenders, impacting traditional services. Digital payments and crypto offer alternatives. Competition intensifies with mobile payment users projected at 150M by 2025.

| Substitute | Impact | 2024 Data |

|---|---|---|

| Fintech | Mobile payments & online lending | Digital payment growth: 25% |

| Credit Unions | Competitive services & terms | $2.1T in assets |

| Non-bank lenders | Alternative financing | Fintech lending growth |

Entrants Threaten

Entry Barriers: Capital Requirements

Starting a new bank necessitates substantial capital, with initial investments often reaching millions. Regulatory hurdles and compliance expenses, including those related to the Community Reinvestment Act, further elevate the entry barriers. These high requirements, like those seen in 2024 where the average startup cost exceeded $20 million, significantly diminish the threat of new competitors. The need to meet strict capital adequacy ratios, such as those mandated by Basel III, adds to the financial burden. These factors collectively make it difficult for new banks to enter the market.

Entry Barriers: Regulatory Hurdles

The banking sector faces significant regulatory hurdles, including obtaining licenses and adhering to extensive laws. Strict regulations and compliance expenses discourage new competitors. The evolving regulatory landscape adds complexity, making market entry difficult. In 2024, the cost of regulatory compliance for banks rose by approximately 7%. These costs are a substantial barrier.

Entry Barriers: Brand Recognition

Building brand recognition and trust is crucial, requiring significant time and resources. Established banks like Veritex have a distinct advantage due to their existing brand recognition. New entrants face the challenge of investing heavily in marketing and customer acquisition. For example, in 2024, marketing expenses for new financial institutions averaged around $5 million to $10 million to gain initial market visibility.

Entry Barriers: Technology Investment

Competing in the digital age demands substantial tech investments. New banks need advanced technology to operate effectively, increasing the financial burden. The integration of AI in banking elevates the technological requirements even further. Banks are spending more on technology; for instance, in 2024, U.S. banks allocated an average of 7% of their revenue to IT. This trend makes it harder for new entrants to compete.

- High Tech Costs: New banks face significant initial and ongoing technology expenditures.

- AI Integration: AI adoption increases the investment needed for new banking platforms.

- Rising IT Budgets: Banks are increasing IT spending, making it harder for newcomers.

- Competitive Landscape: Established banks have a tech advantage, increasing barriers.

Entry Barriers: Customer Relationships

Established banks like Veritex Community Bank benefit from existing customer relationships and loyalty, creating a significant barrier for new entrants. New banks must actively attract customers away from established institutions, which is a challenging endeavor. Building trust and strong customer relationships takes considerable time, effort, and resources. These relationships often hinge on personalized service and local presence, which are hard to replicate quickly. This dynamic impacts Veritex's ability to maintain its market position.

- Customer retention rates for established banks are often high, with some reporting rates above 90% annually.

- New banks may need to offer higher interest rates or incentives to attract customers, impacting profitability.

- Marketing and advertising costs for new entrants are typically substantial, potentially exceeding 20% of revenue in the initial years.

- Veritex Community Bank's focus on community banking provides a competitive edge in building local customer relationships.

Veritex: New Entrants Face High Barriers

The threat of new entrants to Veritex Community Bank is low due to high barriers.

Substantial capital needs, regulatory compliance, and brand recognition pose challenges. In 2024, startup costs often exceeded $20 million, limiting new competitors.

Established banks like Veritex benefit from existing customer relationships and digital infrastructure.

| Factor | Impact | Data (2024) |

|---|---|---|

| Capital Requirements | High initial investment | Avg. startup cost: $20M+ |

| Regulatory Hurdles | Compliance costs | Compliance cost increase: 7% |

| Brand Recognition | Established advantage | Marketing spend: $5-$10M |

Porter's Five Forces Analysis Data Sources

Veritex Community Bank's analysis uses financial statements, market data, competitor information, and industry reports. We consult SEC filings, analyst reports, and bank-specific disclosures.