Zurich Insurance Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Zurich Insurance Group Bundle

What is included in the product

Tailored exclusively for Zurich Insurance Group, analyzing its position within its competitive landscape.

Zurich's analysis identifies vulnerabilities and opportunities, empowering swift strategic adjustments.

Preview Before You Purchase

Zurich Insurance Group Porter's Five Forces Analysis

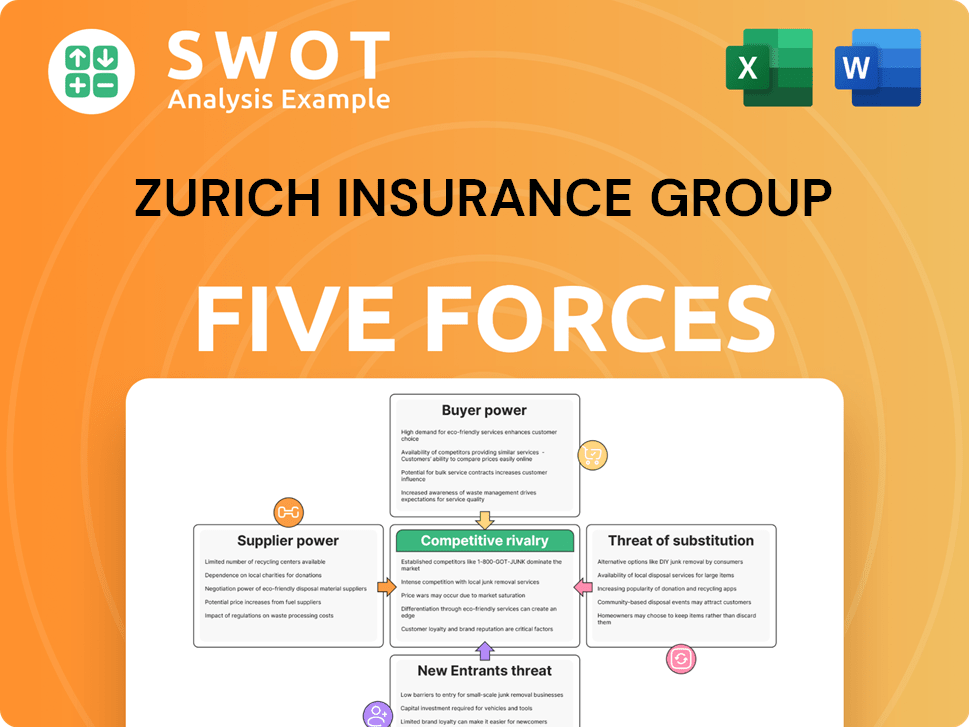

This preview unveils the complete Porter's Five Forces analysis for Zurich Insurance Group; what you see is precisely the document you'll receive. This in-depth assessment explores competitive rivalry, supplier power, buyer power, threat of substitutes, and threat of new entrants within Zurich's industry. Get immediate access to the full analysis upon purchase—no alterations, just the ready-to-use insights. This is the same professionally crafted file available for instant download.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

Zurich Insurance Group faces moderate rivalry due to diverse competitors. Buyer power is significant, influenced by customer choice and price sensitivity. Suppliers, particularly reinsurers, wield moderate influence. The threat of new entrants is limited by high capital requirements and regulations. Substitutes, like self-insurance, pose a modest threat.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Zurich Insurance Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Concentration

Zurich Insurance Group depends on suppliers like tech firms and consultants. If these suppliers are concentrated, they can dictate prices and terms. This could squeeze Zurich's profits. In 2024, the insurance tech market saw major consolidation, potentially increasing supplier power. High supplier power arises when few firms offer unique services.

Switching Costs

Switching costs involve the time, money, and effort needed to change suppliers. Zurich's reliance on specific tech or service suppliers can create high switching costs. For instance, if Zurich uses a unique claims processing system, changing providers becomes costly. This dependency boosts supplier power, potentially leading to less favorable deals for Zurich. In 2024, Zurich's IT spending was approximately CHF 2.5 billion, highlighting the significance of supplier relationships.

Supplier's Ability to Integrate Forward

Suppliers integrating forward, like tech providers offering insurance platforms, boost their bargaining power. This poses a threat to Zurich's market position by potentially bypassing them. In 2024, the InsurTech market grew, with forward integration becoming more common. For example, some tech firms now offer insurance products directly, increasing supplier leverage. This shift challenges traditional insurers like Zurich.

Impact of Supplier Inputs on Differentiation

The quality and uniqueness of supplier inputs critically affect Zurich's product and service differentiation. Standardized inputs reduce supplier bargaining power, while unique inputs increase it. Differentiated inputs often allow suppliers to charge premium prices, impacting Zurich's costs. For instance, specialized software or data analytics from a unique provider could give Zurich a competitive edge. This directly influences Zurich's ability to offer innovative insurance solutions.

- Supplier inputs impact Zurich's differentiation.

- Standardized inputs decrease supplier power.

- Unique inputs increase supplier power and costs.

- Specialized software enhances competitive advantage.

Availability of Substitute Suppliers

The availability of substitute suppliers significantly impacts supplier power for Zurich Insurance Group. When Zurich can choose from many suppliers offering similar goods or services, each supplier's bargaining power diminishes. This competitive landscape enables Zurich to negotiate better prices and terms, reducing its reliance on any single supplier. Conversely, if few substitutes exist, suppliers gain leverage.

- Zurich's procurement strategy focuses on diversifying its supplier base to mitigate risks associated with limited substitutes.

- The insurance industry often involves specialized services, potentially increasing supplier power if substitutes are scarce.

- In 2024, Zurich's operating profit reached $7.4 billion, reflecting efficient cost management, which includes supplier negotiations.

Supplier Dynamics at Zurich: A Snapshot

Zurich faces supplier power from concentrated or integrated suppliers, particularly in tech. Switching costs and the uniqueness of inputs also impact Zurich's supplier relationships. The availability of substitute suppliers greatly affects Zurich's ability to negotiate favorable terms. Zurich's 2024 IT spending was roughly CHF 2.5 billion.

| Factor | Impact on Zurich | 2024 Data Point |

|---|---|---|

| Concentration | Increased supplier power | Insurance tech market consolidation. |

| Switching Costs | Higher supplier power | IT spend approx. CHF 2.5B. |

| Substitutes | Affects bargaining power | Operating profit $7.4B. |

Customers Bargaining Power

Customer Concentration

Customer concentration highlights how Zurich's customer base is spread. If a few big clients drive most revenue, they wield significant bargaining power. For instance, in 2024, a major corporate client could negotiate lower premiums. This can reduce Zurich's profits.

Price Sensitivity

Price sensitivity measures how much customers change insurers due to price changes. In competitive insurance markets, where products seem similar, customers are more price-sensitive, boosting their power. Zurich must skillfully manage pricing with value-added services to lessen price sensitivity's effect. Increased price sensitivity strengthens buyer power. In 2024, the global insurance market reached $6.7 trillion, highlighting intense competition and customer price awareness.

Availability of Information

Customers' access to information significantly shapes their bargaining power. Online platforms and comparison tools allow easy evaluation of insurance options. This transparency compels Zurich to provide competitive pricing. For example, in 2024, digital insurance sales accounted for approximately 30% of total premiums.

Switching Costs for Customers

Switching costs for Zurich's customers involve the effort and costs of changing insurers. Low switching costs, due to easy cancellation and minimal paperwork, boost customer bargaining power. Zurich aims to retain customers through exceptional service, customized offerings, and bundled insurance packages. This strategy is essential, as low switching costs increase buyer power.

- In 2024, the average customer retention rate in the insurance industry was approximately 85%.

- Zurich's customer satisfaction scores and retention rates are key metrics to monitor.

- Offering competitive pricing and value-added services are crucial for customer loyalty.

- Digital platforms can streamline the switching process, impacting customer choice.

Customer's Ability to Self-Insure

The bargaining power of customers is amplified by their ability to self-insure, especially large corporations. This strategic move involves setting aside funds to cover potential losses internally. For instance, in 2024, companies with robust financial health increasingly chose this route. This shift gives customers greater control over their risk management, reducing their reliance on insurance providers. Consequently, Zurich and other insurers face pressure on premiums and market share as self-insurance capabilities grow.

- Self-insurance reduces customer dependence on Zurich.

- Customers gain control over risk management.

- Zurich may face pressure on premiums.

- Greater self-insurance increases buyer power.

Customer Power: Zurich's Revenue at Stake

Customer concentration significantly impacts Zurich's revenue. Price sensitivity and easy access to information empower customers. Low switching costs further amplify customer bargaining power. In 2024, the global insurance market was $6.7T.

| Factor | Impact on Customer Bargaining Power | 2024 Data |

|---|---|---|

| Customer Concentration | High concentration increases power | Major clients negotiate premiums. |

| Price Sensitivity | High sensitivity boosts power | Insurance market: $6.7T. |

| Information Access | Easy access strengthens power | Digital sales: ~30% of premiums. |

Rivalry Among Competitors

Number of Competitors

The insurance industry is highly competitive, featuring numerous rivals. Zurich faces pressure to stand out via product differentiation, pricing, and service. The fragmented market, with many players, intensifies rivalry. For example, in 2024, the global insurance market was estimated at over $6 trillion, highlighting the broad competitive landscape.

Market Growth Rate

Market growth rate heavily shapes competitive intensity. Slow growth often sparks intense competition, driving down prices. Zurich must innovate and target high-growth areas to counter this. In 2023, the global insurance market grew by about 5%, a moderate pace. Slow growth intensifies rivalry.

Product Differentiation

Product differentiation significantly impacts competitive rivalry in the insurance sector. When products are similar, competition becomes price-driven, and rivalry intensifies. Zurich Insurance Group should highlight its value-added services and brand reputation. In 2024, the insurance industry saw a 6% increase in claims, pushing firms to differentiate. Low differentiation leads to aggressive price wars.

Switching Costs

Switching costs significantly impact the competitive landscape for Zurich Insurance Group. Low switching costs make it easier for customers to switch insurers, which intensifies competition. Zurich must focus on building customer loyalty to combat this, as it reduces the ease with which customers can move to competitors. Zurich can achieve this through tailored services, bundled insurance products, and efficient claims handling. This is essential in a market where customers have numerous choices.

- Customer retention is key in competitive markets.

- Personalized services enhance loyalty.

- Efficient claims processing builds trust.

- Bundled products can lock in customers.

Exit Barriers

Exit barriers significantly influence competitive rivalry within the insurance sector, impacting Zurich Insurance Group. Regulatory requirements, such as solvency standards, and long-term contracts, can make it difficult for insurers to leave the market. These barriers can trap companies, intensifying competition, even when profitability is low. Zurich must strategically manage its portfolio, considering these barriers to optimize market positions. For example, in 2024, the global insurance industry saw mergers and acquisitions slow slightly due to higher interest rates and regulatory scrutiny, indicating the impact of exit barriers.

- Regulatory Compliance: Adherence to stringent financial regulations.

- Contractual Obligations: Long-term policies with policyholders limit flexibility.

- Asset Specificity: Investments in specialized assets can be hard to liquidate.

- Market Conditions: Economic downturns can exacerbate exit challenges.

Insurance Market's Competitive Landscape

Zurich Insurance Group faces intense competition due to a fragmented market, as the global insurance market was over $6 trillion in 2024. Slow market growth, around 5% in 2023, heightens rivalry. Low product differentiation and easy switching costs intensify price wars.

| Factor | Impact on Rivalry | Zurich Strategy |

|---|---|---|

| Market Structure | Fragmented, many competitors | Differentiate products and services |

| Growth Rate | Slow growth intensifies competition | Target high-growth areas |

| Product Differentiation | Low differentiation drives price wars | Highlight value-added services |

SSubstitutes Threaten

Availability of Alternative Risk Management Solutions

The threat of substitutes for Zurich Insurance Group comes from alternative risk management options. These include self-insurance and government programs. Increased availability of alternatives heightens this threat. Zurich must highlight its unique value to compete effectively. In 2024, the global insurance market was valued at over $6 trillion, with self-insurance representing a significant portion.

Price Performance of Substitutes

The price-performance ratio of substitutes significantly impacts their appeal. If alternatives offer similar coverage at a lower cost, Zurich faces a real threat to its market share. Improving efficiency and cost-effectiveness is crucial for Zurich. For example, the rise of parametric insurance, offering automated payouts, presents a competitive alternative. Favorable price-performance boosts the threat from substitutes.

Customer Propensity to Switch

Customer propensity to switch to substitutes like self-insurance or parametric insurance hinges on risk tolerance and awareness. A 2024 study showed 20% of businesses are considering alternative risk solutions. Zurich must highlight the limitations of substitutes. Increased switching willingness, potentially due to cost savings, elevates the threat; in 2024, a 15% price difference significantly influenced customer decisions.

Technological Advancements

Technological advancements pose a significant threat to Zurich Insurance Group by enabling the emergence of substitute solutions. Advanced analytics and predictive modeling allow businesses to self-insure or reduce their insurance needs. This shift is driven by tech-savvy companies seeking cost-effective risk management. Zurich must innovate to stay ahead of these changes. New technologies are increasing the threat of substitutes.

- In 2024, the global insurtech market was valued at approximately $73.2 billion.

- The adoption of AI in risk assessment and claims processing is growing rapidly.

- Companies like Lemonade are using technology to offer simplified insurance products.

- Zurich's investment in technology reached $1.3 billion in 2023.

Regulatory Support for Alternatives

Regulatory support for alternative risk management solutions can indeed affect Zurich's competitive landscape. Government incentives for self-insurance or other alternatives could intensify competition for Zurich. Proactive engagement with policymakers is crucial for Zurich to maintain a fair market and advocate for regulations that value insurance. Supportive regulations would increase the threat from substitutes, potentially impacting Zurich's market share. For instance, in 2024, regulatory changes in the EU regarding Solvency II could influence the adoption of alternative risk transfer mechanisms.

- Regulatory support for alternative risk management solutions impacts adoption.

- Government incentives for alternatives intensify competition for Zurich.

- Zurich must engage with policymakers.

- Supportive regulations increase the threat of substitutes.

Substitutes Challenge Insurer's Market Position

Zurich faces substitute threats from self-insurance and parametric insurance. Cost-effectiveness and price-performance of alternatives influence their appeal. Customer switching depends on risk tolerance; tech advances also drive change. Insurtech market was $73.2B in 2024.

| Factor | Impact | 2024 Data |

|---|---|---|

| Self-Insurance | Alternative risk management | Significant portion of the $6T global market |

| Parametric Insurance | Competitive alternative | Growing market share |

| Tech Advancements | Emergence of substitutes | $73.2B Insurtech Market |

Entrants Threaten

Capital Requirements

The insurance sector demands substantial initial capital for regulatory compliance and operational setup. High capital needs act as a barrier, limiting the likelihood of new competitors entering the market. Zurich Insurance Group, with its robust financial foundation and economies of scale, possesses a significant advantage. This established financial base makes it harder for smaller, less capitalized firms to challenge Zurich. High capital requirements, therefore, reduce the threat of new entrants. For example, in 2024, Zurich reported a solvency ratio of 200%, demonstrating its strong capital position.

Regulatory Barriers

Regulatory barriers significantly impact the insurance industry, increasing the difficulty for new entrants. Strict licensing and solvency rules protect established firms like Zurich Insurance Group. Zurich's established regulatory navigation skills give it an edge. The regulatory environment in 2024 continues to be complex. These barriers therefore decrease the threat of new competitors.

Brand Recognition and Customer Loyalty

Zurich Insurance Group's established brand recognition and customer loyalty significantly deter new entrants. Customers generally favor trusted insurers like Zurich, reducing the appeal of newer, lesser-known companies. Zurich's marketing, customer service, and reputation management efforts have built a strong brand presence. The company's brand value in 2024 is estimated at $14.5 billion, which is a testament to their strong market position. This loyalty significantly lowers the threat of new competitors.

Access to Distribution Channels

Access to established distribution channels, like brokers and agents, is vital in insurance. New companies face hurdles in building their sales networks, which limits their customer reach. Zurich Insurance Group has a strong distribution advantage, reducing the threat from new competitors. For instance, Zurich's 2024 annual report highlights its vast network. This extensive reach makes it difficult for new entrants to compete effectively.

- Zurich uses a mix of agents, brokers, and direct channels.

- New entrants must build these channels, a costly and time-consuming process.

- Zurich's established presence gives it a significant market advantage.

- Limited distribution access decreases the risk from new competitors.

Economies of Scale

Zurich Insurance Group benefits from significant economies of scale, particularly in underwriting and claims processing. These operational efficiencies allow Zurich to offer competitive pricing and manage costs more effectively. New entrants struggle to match these efficiencies, facing higher per-unit costs. This cost advantage acts as a barrier, reducing the threat from new competitors. Zurich's scale strengthens its market position.

- Zurich's revenue in 2023 was $82.9 billion, demonstrating its scale.

- Operating expenses were managed efficiently.

- New entrants face hurdles.

- Economies of scale offer a competitive edge.

Insurance Sector's Entry Barriers: A Tough Climb

The insurance sector's high capital needs, regulatory hurdles, and strong brand loyalty create significant barriers, reducing the threat of new entrants. Zurich's strong financial position, with a solvency ratio of 200% in 2024, and established distribution networks further limit new competition.

Zurich's brand value, estimated at $14.5 billion in 2024, underscores its market advantage.

| Factor | Impact | Data (2024) |

|---|---|---|

| Capital Requirements | High barrier | Solvency ratio of 200% |

| Regulations | Complex | Strict licensing |

| Brand/Loyalty | Strong | $14.5B brand value |

Porter's Five Forces Analysis Data Sources

Our Zurich analysis is built on annual reports, market research, financial data, and industry publications for precise strategic insights.