Lloyds Banking Group Bundle

Can Lloyds Banking Group Navigate the Future of Finance?

Lloyds Banking Group, a cornerstone of the UK's financial landscape, is undergoing a significant transformation. With a £3 billion investment, the company aims to revolutionize customer experiences and leverage cutting-edge technology. This strategic shift is critical for a financial institution with a rich history, evolving from its roots in the Industrial Revolution.

This deep dive into Lloyds Banking Group explores its ambitious Lloyds Banking Group SWOT Analysis, growth strategy, and future prospects within the dynamic banking industry. We'll examine how Lloyds plans to expand, innovate, and manage risks to secure its long-term growth potential. Understanding the company's strategic analysis is key to unlocking potential investment opportunities and navigating the challenges facing Lloyds Banking Group in the future, including its digital transformation initiatives and the impact of economic trends.

How Is Lloyds Banking Group Expanding Its Reach?

The Lloyds Banking Group is actively pursuing an aggressive Growth Strategy, focusing on enhancing its existing franchise and delivering superior outcomes for its customers. Their aim is to generate over £1.5 billion in additional income from strategic initiatives by 2026. This strategic direction is a key element in shaping the Future Prospects of the group within the Banking Industry.

A central aspect of this strategy involves becoming a customer-focused digital leader and an integrated Financial Services provider. This approach allows the group to capitalize on new opportunities at scale, driving both efficiency and customer satisfaction. In 2024, the Group demonstrated its commitment to this Strategic Analysis by successfully completing the first phase of its strategy and exceeding its revenue target.

The group's expansion plans also encompass a significant push into institutional markets, with a particular focus on increasing US dollar issuance and trading volumes. While maintaining its strength in sterling, Lloyds Banking Group aims to grow by increasing activity, client coverage, and market expertise. They are positioning themselves as a trusted partner for UK issuers seeking access to US investors, a move that could significantly impact their Lloyds Banking Group market share analysis.

Lloyds Banking Group is expanding its presence in institutional markets, with a focus on increasing US dollar issuance and trading volumes. This strategic move aims to capitalize on opportunities within the global financial landscape.

The group is focusing on increasing US dollar issuance and trading volumes. While its strength remains in sterling, Lloyds aims to grow by increasing activity, client coverage, and market expertise.

Lloyds Banking Group is also expanding its European product offering and rebuilding its presence in the US. This dual approach aims to diversify its revenue streams and strengthen its global footprint.

In 2024, Lloyds Banking Group became the first major UK bank to lend to a Community Development Financial Institution (CDFI), contributing £43 million to three CDFIs as part of a £62 million fund.

Key Expansion Initiatives

Lloyds Banking Group is implementing several key initiatives to drive growth and enhance its market position. These initiatives are designed to strengthen its competitiveness and ensure long-term success. For more details, you can explore the Competitors Landscape of Lloyds Banking Group.

- Focus on digital transformation to enhance customer experience and operational efficiency.

- Expansion of product offerings in both European and US markets.

- Strategic partnerships to increase market reach and service capabilities.

- Investment in sustainable and responsible banking practices.

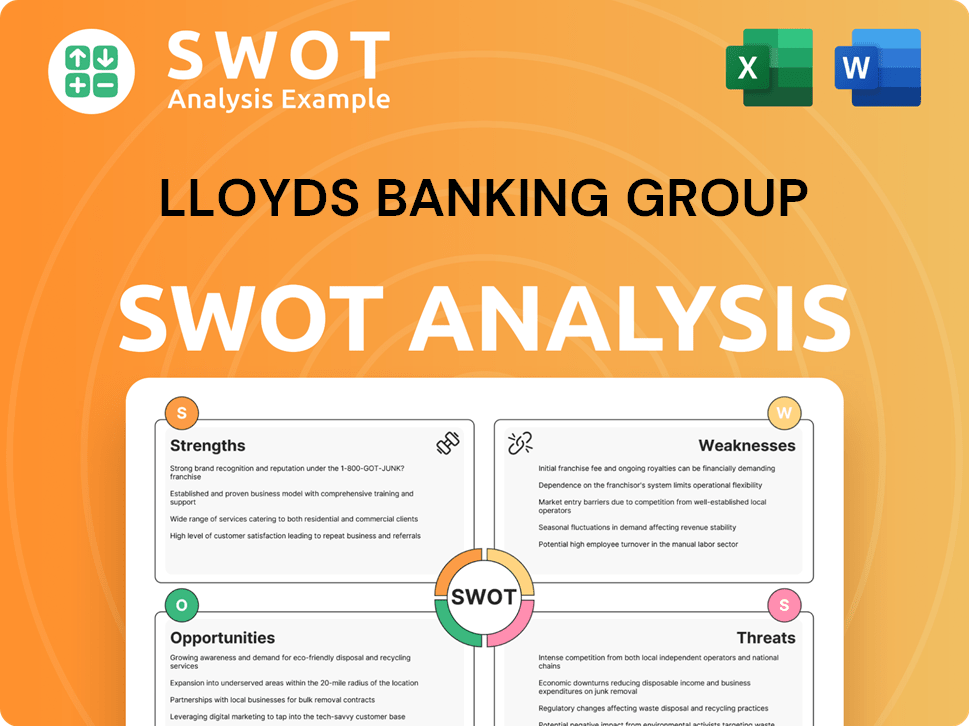

Lloyds Banking Group SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Lloyds Banking Group Invest in Innovation?

Lloyds Banking Group is heavily investing in technology and innovation to drive its growth. The company's approach centers on enhancing customer experiences and improving service delivery through digital means. This strategic focus is crucial in the evolving landscape of the Banking Industry and Financial Services.

The company is committed to a digital transformation strategy that focuses on integrating products and services. This involves leveraging technologies like AI, big data, cloud computing, and advancements in payments. These initiatives are designed to optimize operations and enhance customer engagement.

The Group's commitment to innovation is evident in its substantial investments. This includes an estimated annual ICT spending of $1.9 billion in 2024, primarily allocated to software, ICT services, and network and communications. This financial commitment underscores the importance of technology in the company's strategic plans.

Digital Customer Experience

Lloyds is enhancing its consumer mobile app to provide a better customer experience. This includes interactive tools, personalized insights, and conversational prompts. The focus is on making banking more accessible and user-friendly.

Data and Organizational Agility

The Group is investing in technology transformation to realize the value of customer data and improve organizational agility. Since 2021, over 10% of legacy applications have been decommissioned. This streamlining helps in adapting to market changes.

Talent Acquisition

In 2024, Lloyds remodeled its recruitment function to align talent acquisition with strategic workforce planning. This also includes reducing agency dependency. Attracting and retaining top talent is crucial for their long-term success.

Cultural Shift

The Group is shifting its culture to be more collaborative, customer-obsessed, and growth-oriented. The aim is to be seen as a technology company that does banking. This cultural shift is vital for innovation.

Sustainable Practices

The refurbishment of its 33 Old Broad Street office, reopening in November 2024, exemplifies this. The office features state-of-the-art technology and significantly reduced CO2 emissions by 428 tonnes annually through gas-free technology. This shows their commitment to sustainability.

Strategic Investments

The substantial ICT spending of $1.9 billion in 2024 highlights the importance of technology. These investments are critical for driving the company's Growth Strategy and achieving its Future Prospects. These investments are key for the company's future.

These strategic initiatives are designed to position Lloyds Banking Group for sustained success in the competitive Banking Industry. For further insights into the company's ownership structure and strategic direction, explore Owners & Shareholders of Lloyds Banking Group.

Key Technology Focus Areas

Lloyds Banking Group's technology strategy focuses on several key areas to enhance its operations and customer service. This includes leveraging advanced technologies to improve efficiency and customer experience.

- AI: Implementing artificial intelligence to automate tasks and provide personalized customer experiences.

- Big Data: Utilizing big data analytics to gain insights into customer behavior and market trends.

- Cloud: Migrating to cloud-based solutions for scalability, flexibility, and cost efficiency.

- Payments: Investing in modern payment systems to offer seamless and secure transactions.

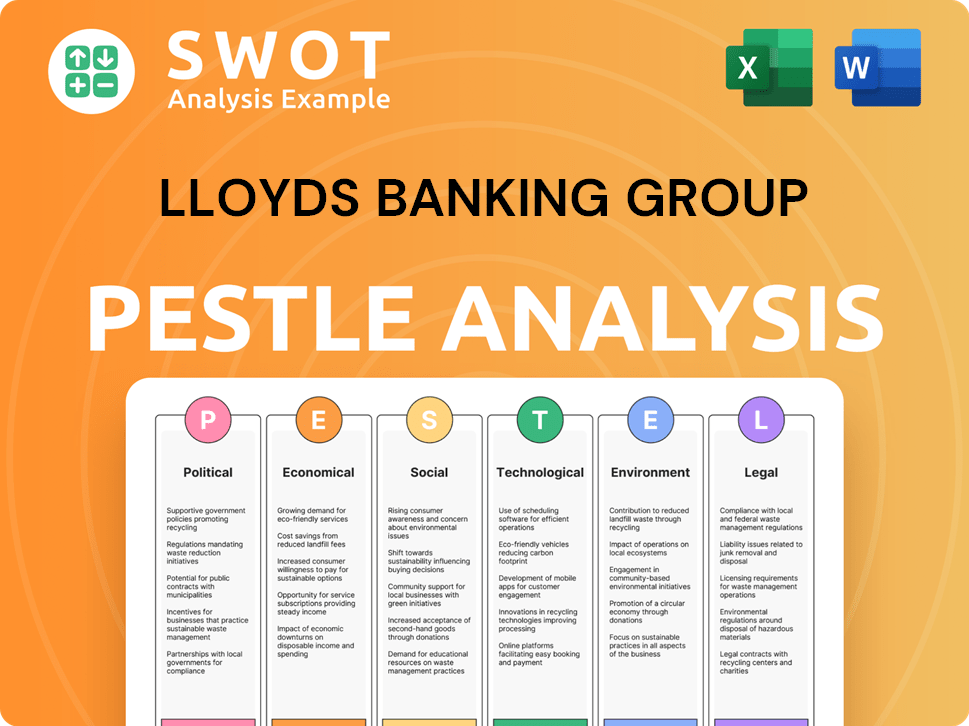

Lloyds Banking Group PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Lloyds Banking Group’s Growth Forecast?

In 2024, Lloyds Banking Group demonstrated robust financial health, with income growth in the second half of the year. This was supported by a rising net interest margin and positive momentum in other income streams. The bank's strategic initiatives are aimed at generating over £1.5 billion in additional income by 2026, showcasing a proactive approach to growth within the competitive banking industry.

The full-year 2024 results showed approximately £24.2 billion in revenue and a net profit of £6.7 billion for Lloyds. This strong performance resulted in a return on equity exceeding 21%. The cost-to-income ratio was around 60% at the end of 2024, indicating efficient operational management. These figures highlight the company's solid financial foundation and its ability to generate substantial returns.

Looking ahead to Q1 2025, Lloyds reported a statutory profit after tax of £1.1 billion. Net income increased by 4% year-on-year. The underlying net interest income was £3.3 billion, up 3% year-on-year, while the banking net interest margin improved to 3.03%, an increase of 8 basis points year-on-year. Underlying other income also saw an increase, reaching £1.5 billion, which is 8% higher than the previous year. These results suggest continued growth and profitability for the group.

Loans and Advances

Loans and advances to customers as of March 31, 2024, were £432.078 million. This figure reflects the bank's lending activities and its role in supporting the economy. The level of loans and advances is a key indicator of the bank's financial performance and its ability to generate revenue through interest income.

Total Assets

Total assets were £606,037 million as of March 31, 2024. This figure encompasses all the resources owned by the bank, including cash, investments, and loans. The size of the asset base indicates the scale of the bank's operations and its overall financial strength.

Capital Ratio

The Group's Common Equity Tier 1 (CET1) capital ratio was 14.2% at December 31, 2024, reducing to 13.5% as of May 1, 2025. This ratio measures the bank's financial stability by comparing its core capital to its risk-weighted assets. A strong CET1 ratio indicates that the bank is well-capitalized and able to withstand potential financial shocks.

Share Buyback

Lloyds has announced a share buyback program of up to £1.7 billion. This program reflects the bank's confidence in its financial position and its commitment to returning value to shareholders. Share buybacks can also increase earnings per share, making the stock more attractive to investors.

Net Interest Income

Underlying net interest income in Q1 2025 was £3.3 billion, up 3% year-on-year. This increase highlights the bank's ability to generate income from its lending activities. The rise in net interest income is a crucial factor in the overall financial performance and future prospects of Lloyds Banking Group.

Net Profit

The statutory profit after tax for Q1 2025 was £1.1 billion. This indicates a solid financial performance and demonstrates the bank's ability to generate profits. The level of profit is essential for the bank's growth and its ability to invest in future initiatives.

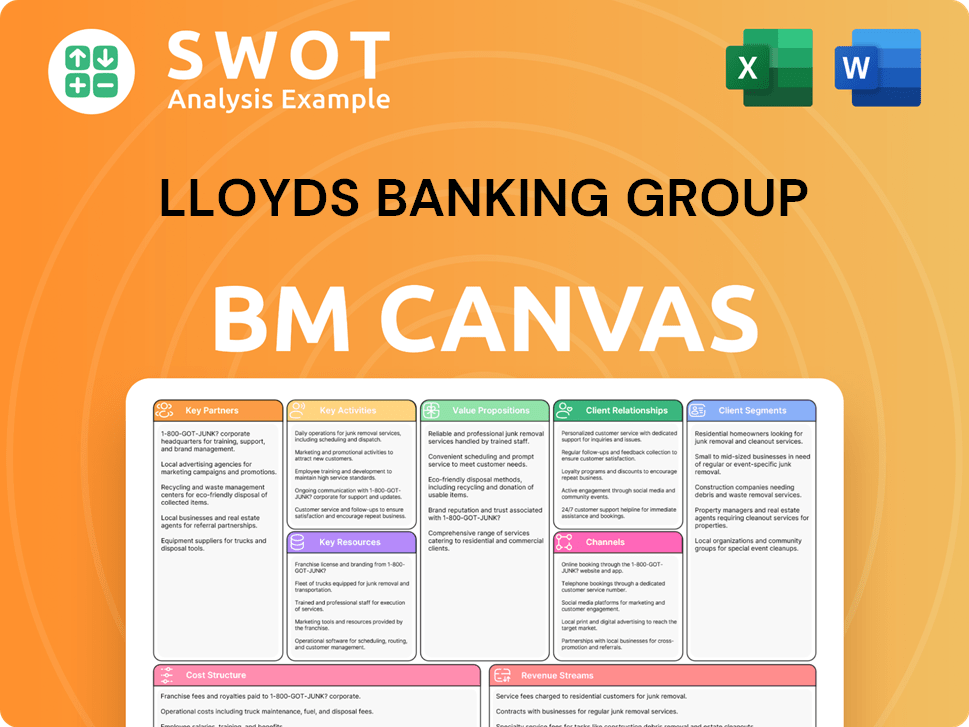

Lloyds Banking Group Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Lloyds Banking Group’s Growth?

The path forward for Lloyds Banking Group, encompassing its growth strategy and future prospects, is fraught with potential risks and obstacles. These challenges span economic, regulatory, and operational domains, potentially impacting the financial performance and strategic initiatives of the bank. A thorough understanding of these risks is crucial for investors, analysts, and stakeholders assessing the long-term viability of Lloyds.

The banking industry faces a complex web of challenges, and Lloyds is not immune. The company must navigate shifting economic landscapes, stringent regulatory environments, and evolving customer expectations. Successfully managing these risks will be critical for Lloyds Banking Group to achieve its growth objectives and maintain its competitive position in the financial services sector.

Several factors could impede the future prospects of Lloyds Banking Group. The primary concern is the potential impact of interest rate fluctuations on net interest margins, a key driver of profitability. Economic downturns, regulatory scrutiny, and internal restructuring efforts also present significant hurdles that the bank must address.

Interest Rate Environment

Changes in interest rates pose a significant risk to Lloyds' profitability. Bank of England rate cuts could compress net interest margins, which directly affects revenue. This requires careful management of its asset and liability portfolios to mitigate the impact.

Economic Uncertainty

Economic instability, including a rising UK unemployment rate, currently at 4.4%, can lead to increased loan defaults. This necessitates higher provisions for bad debts, impacting the bank's financial performance. The cyclical nature of the banking sector means that any economic downturn could disproportionately affect Lloyds' performance.

Regulatory and Legal Risks

Lloyds faces potential litigation costs from an ongoing car finance probe. The bank has set aside £450 million for potential penalties. Additionally, an investigation by the Financial Conduct Authority (FCA) into anti-money laundering controls poses an unknown financial risk.

Restructuring and Operational Risks

The bank's restructuring of its risk management division, with approximately 175 permanent roles at risk, could potentially loosen risk controls. The cyclical nature of the Banking Industry means any downturn in the UK economy could disproportionately impact Lloyds' performance. These changes require careful management to ensure operational efficiency and maintain robust risk management practices.

Competitive Pressures

The competitive landscape within the financial services sector is intense. The rise of fintech companies and other established banks puts pressure on Lloyds to innovate and maintain market share. This requires continuous investment in technology and customer service.

Technological Disruption

The rapid advancement of technology presents both opportunities and risks. Cyber security threats and the need to continuously update digital infrastructure require significant investment. Failure to adapt could lead to a loss of customers and market share. For more insight into the company's values and mission, consider reading about the Mission, Vision & Core Values of Lloyds Banking Group.

Economic trends significantly influence Lloyds' performance. Rising unemployment, currently at 4.4%, and potential economic slowdowns can lead to increased loan defaults. This necessitates higher provisions for bad debts, directly impacting profitability. The bank's ability to navigate these economic cycles is crucial for maintaining financial stability.

Regulatory scrutiny and legal challenges pose significant risks. The ongoing car finance probe and the FCA investigation into anti-money laundering controls could result in substantial financial penalties. The bank must allocate resources to address these issues and ensure compliance, impacting its financial resources.

Lloyds Banking Group Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Lloyds Banking Group Company?

- What is Competitive Landscape of Lloyds Banking Group Company?

- How Does Lloyds Banking Group Company Work?

- What is Sales and Marketing Strategy of Lloyds Banking Group Company?

- What is Brief History of Lloyds Banking Group Company?

- Who Owns Lloyds Banking Group Company?

- What is Customer Demographics and Target Market of Lloyds Banking Group Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.