CPI Card Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

CPI Card Bundle

What is included in the product

Detailed analysis of each competitive force, supported by industry data and strategic commentary.

Instantly grasp market pressure with intuitive spider/radar charts, revealing strategic vulnerabilities.

Preview the Actual Deliverable

CPI Card Porter's Five Forces Analysis

This preview showcases the complete Five Forces analysis. Upon purchase, you'll receive this same in-depth document. It offers insights into industry competition, buyer power, and more. The analysis is professionally written and ready to utilize. Download it instantly after buying.

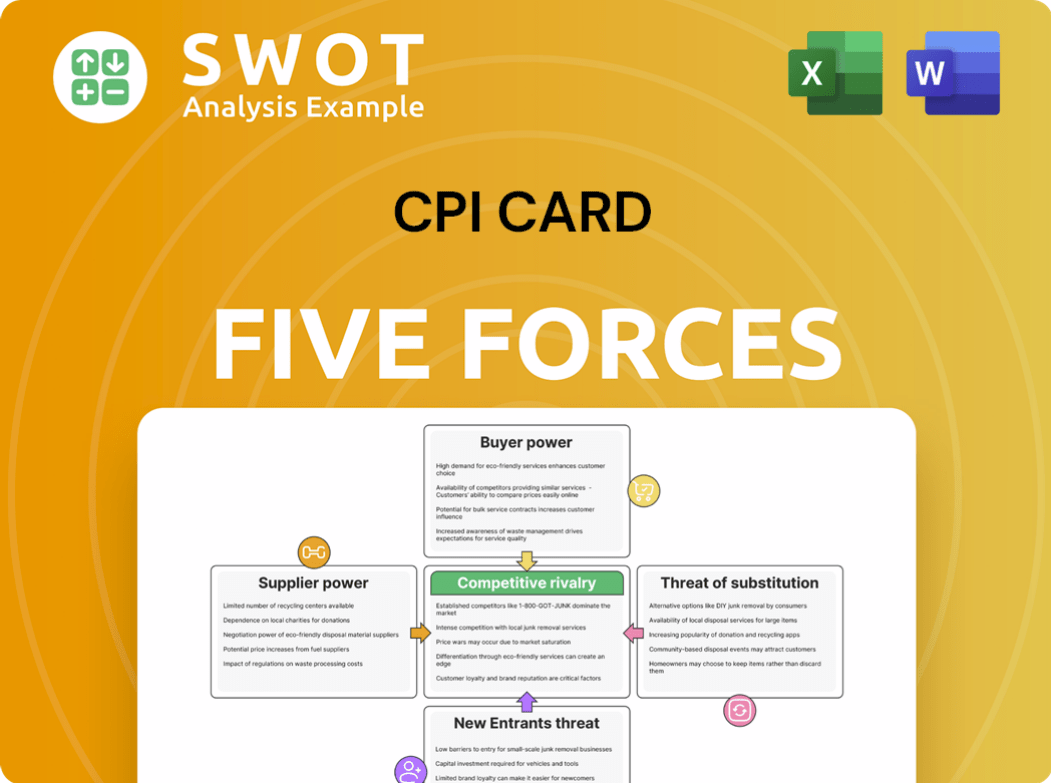

Porter's Five Forces Analysis Template

From Overview to Strategy Blueprint

CPI Card's competitive landscape is shaped by five key forces. The threat of new entrants is moderate, balanced by established brands. Buyer power is significant, due to diverse options. Supplier power is somewhat limited. The threat of substitutes is rising with digital payment solutions. Rivalry is high within the industry.

Unlock key insights into CPI Card’s industry forces—from buyer power to substitute threats—and use this knowledge to inform strategy or investment decisions.

Suppliers Bargaining Power

Limited Number of Key Suppliers

CPI Card Group's dependence on a few key suppliers for crucial card components elevates supplier bargaining power. This concentration, especially for printing equipment and semiconductors, limits CPI's alternatives. In 2024, the market for specialized card components was valued at approximately $1.2 billion, with a few dominant suppliers controlling a significant share.

High Switching Costs

Switching suppliers can be costly for CPI Card Porter due to specialized components. High switching costs strengthen supplier power. Transitioning semiconductor suppliers can cost $1.2M-$3.5M per platform. This limits CPI's ability to negotiate favorable terms. This gives suppliers more control over pricing and contract terms.

Dependency on Advanced Technology

CPI Card Group's dependence on suppliers for advanced tech, like EMV chips, impacts bargaining power. Suppliers with unique tech hold more power, potentially increasing prices. This reliance makes CPI vulnerable to cost hikes or supply issues. In 2024, the chip shortage affected card production significantly, highlighting this vulnerability.

Global Supply Chain Constraints

CPI Card Group confronts strong supplier power due to global supply chain issues, especially in electronic materials. Semiconductor shortages, a critical component, significantly inflate costs and reduce CPI's bargaining power. Logistics disruptions and raw material scarcity exacerbate these challenges, limiting supply and increasing prices. These issues collectively diminish CPI's ability to negotiate favorable terms with suppliers, affecting profitability.

- Semiconductor prices surged by 20-30% in 2024 due to shortages.

- Raw material costs for plastics increased by 15% in the same period.

- Logistics expenses rose by 10% due to supply chain disruptions.

Specialized Card Manufacturing Equipment

The bargaining power of suppliers is significant for CPI Card Group, particularly concerning specialized card manufacturing equipment. The market is concentrated, with a few dominant global suppliers controlling the technology. This concentration gives suppliers leverage over pricing and terms, impacting CPI's operational costs. This can potentially squeeze CPI's profit margins, making cost management crucial.

- Market concentration: Few key suppliers.

- Supplier control: Specialized knowledge and equipment.

- Impact: Higher operational costs.

- Result: Potential profit margin squeeze.

Supplier Power: A Costly Challenge

CPI Card Group faces substantial supplier power due to reliance on key vendors for specialized components. Concentration among suppliers, like in chip production, limits alternatives, increasing costs. High switching costs and supply chain disruptions in 2024, further empower suppliers, impacting profitability.

| Factor | Impact | 2024 Data |

|---|---|---|

| Market Concentration | Fewer supplier options | Chip market: top 3 suppliers control 70% |

| Switching Costs | High switching costs | Platform switch: $1.2M-$3.5M |

| Supply Chain | Disruptions & shortages | Semiconductor price increase: 20-30% |

Customers Bargaining Power

Large Volume Purchases

CPI Card Group's main clients, big financial institutions, buy payment cards in bulk. These large orders give them strong bargaining power. They can push for lower prices or better terms, leveraging their significant purchase volumes. For instance, in 2024, major banks' card orders might influence CPI's pricing due to the scale.

Customer Switching Ability

Financial institutions can switch card manufacturers, but it involves costs. This switching ability gives customers leverage when negotiating with CPI Card Group. The average switching cost is around $250,000, impacting negotiation power. This affects pricing and service terms.

Commoditized Product Perception

Payment cards, like standard credit and debit cards, can appear similar to customers, increasing their bargaining power. This commoditization means consumers can easily switch providers. To counter this, CPI Card Group should highlight distinctive features. In 2024, the global payment cards market was valued at $400 billion.

Demand for Low-Cost Solutions

Financial institutions' constant cost-cutting efforts significantly amplify customer bargaining power, pushing CPI Card Group to offer competitive pricing. The growing demand for cheaper solutions allows customers to easily switch to manufacturers with lower prices. CPI Card Group must emphasize value-added services to maintain its market position. According to a 2024 report, the average cost reduction target for financial institutions is 10-15%.

- Cost Pressure: Financial institutions aim to cut costs, increasing customer bargaining power.

- Price Sensitivity: Customers can easily switch to lower-priced manufacturers.

- Value-Added Services: CPI must offer these to stay competitive.

- Industry Data: Average cost reduction targets are 10-15% (2024).

Influence of Card Networks

Card networks such as Visa and Mastercard significantly influence customer bargaining power by setting industry standards, which impacts the demand for specific card features. These networks shape CPI Card Group's offerings through technology and security standards, affecting consumer expectations. Compliance with these standards can limit CPI's flexibility in negotiations. In 2024, Visa and Mastercard processed approximately $14 trillion in transactions globally.

- Visa and Mastercard's combined market share is over 90% of the global card network market.

- CPI must adhere to PCI DSS standards mandated by card networks.

- Card networks' influence affects feature demands like contactless payments.

Card Market Dynamics: Bargaining Power & Costs

CPI Card Group faces strong customer bargaining power due to bulk purchases by financial institutions, allowing negotiation of lower prices and better terms. Switching costs, averaging around $250,000, impact this power, influencing pricing and service conditions. In 2024, the global payment cards market was valued at $400 billion.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Bulk Purchases | Strong customer leverage | Major banks' card orders influence pricing. |

| Switching Costs | Moderate customer leverage | Average switching cost: $250,000 |

| Market Size | Increased competition | Global market: $400B |

Rivalry Among Competitors

Numerous Competitors

The payment card market is highly competitive, with CPI Card Group contending with numerous rivals. Major players like Giesecke+Devrient and smaller regional firms create a challenging environment. The presence of many competitors intensifies price wars and battles for market share. In 2024, the industry saw a 5% price reduction due to aggressive rivalry, impacting profit margins.

Price Competition

Price competition is fierce in payment card manufacturing. Competitors aggressively lower prices to win contracts, squeezing profit margins. In 2024, CPI Card Group faced pressure to match lower bids. To counter this, CPI must offer unique services and products.

Product Differentiation Challenges

CPI Card Group faces product differentiation challenges because basic card functions are standardized. This intensifies competitive rivalry. To stand out, CPI must innovate with features like advanced security or sustainable materials. In 2024, the global payment cards market was valued at $400 billion, highlighting the need for CPI to differentiate. Focusing on eco-friendly materials, as seen in the rise of sustainable cards, is crucial for competitive advantage.

Market Concentration

The payment card manufacturing sector sees intense competition, driven by a high market concentration. About 65.6% of the market is controlled by a few major players. This concentration fuels aggressive rivalry, with firms constantly vying for market share. This dynamic impacts pricing and innovation strategies.

- Market concentration means fewer firms control most sales.

- High concentration often leads to intense competition.

- Firms compete on price, features, and service.

- This can pressure profit margins.

Innovation and R&D Investments

Innovation is crucial in the payment card industry, with companies like CPI Card Group constantly investing in research and development (R&D). This investment allows them to introduce new technologies and features. CPI Card Group’s ability to stay ahead of competitors is heavily dependent on its innovation efforts. For 2023, CPI Card Group’s competitive innovation spending was $31.2 million, which accounted for 6.8% of total revenue.

- Continuous innovation is essential to keep pace with competitors.

- CPI Card Group's 2023 R&D investment was $31.2 million.

- R&D spending represented 6.8% of total revenue in 2023.

- New technologies and features are key competitive differentiators.

Payment Card Market: Fierce Competition

CPI Card Group operates in a highly competitive payment card market. Aggressive price wars and the need for differentiation squeeze profit margins. Market concentration, with top players controlling 65.6%, fuels rivalry. Innovation, like CPI's $31.2 million R&D in 2023, is key.

| Aspect | Details | Impact |

|---|---|---|

| Market Share Control | Top firms control 65.6% | Intense competition, price pressure |

| R&D Investment (2023) | CPI spent $31.2 million | Innovation, differentiation |

| Price Reduction (2024) | Industry saw 5% drop | Margin squeeze, competitive need |

SSubstitutes Threaten

Digital Payment Platforms

Digital payment platforms are a growing threat. They offer convenient, secure alternatives to cards. Apple Pay's 5.4 billion transactions in 2023 show rapid growth. This impacts CPI Card Group's market share. Consumers increasingly choose digital options.

Contactless and Virtual Payments

The rise of contactless and virtual payments poses a significant threat to CPI Card Group. Mobile wallets and virtual cards are becoming mainstream, with 89% of millennials using contactless payments in 2023. This shift reduces the need for physical cards, impacting CPI's core product demand. Competitors offering digital payment solutions further intensify this threat, potentially eroding CPI Card Group's market share.

Blockchain and Cryptocurrency

Emerging blockchain and cryptocurrency payment options pose a threat to traditional payment card providers. These technologies offer decentralized, secure alternatives, although they are still developing. The cryptocurrency payment market was valued at $2.1 trillion in 2023. This could impact companies like CPI Card Group.

Decline in Physical Card Usage

The threat of substitutes for CPI Card Group includes the shift away from physical cards. Digital payment methods are becoming more popular, which could decrease the need for traditional cards. This trend is evident in the declining usage of physical credit cards. For example, in 2023, physical credit card usage decreased by 12.3%.

- Digital wallets and mobile payments are growing rapidly.

- Contactless payments offer convenience.

- Consumers are adopting digital payment methods.

- This shift could reduce demand for physical cards.

Mobile Payment Growth

The rise of mobile payments poses a significant threat to CPI Card Group. Consumers increasingly favor digital wallets, which offer a convenient alternative to physical cards. The global mobile wallet market was valued at $6.2 trillion in transaction value in 2023, showing strong growth. This shift could diminish the demand for traditional payment cards.

- Mobile wallet transaction volume increased by 28.6% year-over-year.

- Consumers are moving towards digital payment methods.

- CPI Card Group's core product faces growing competition.

- Mobile payments offer greater convenience and ease of use.

Digital Payments Surge: Physical Cards Under Pressure

CPI Card Group faces threats from digital payment alternatives. Mobile wallets and contactless options are increasingly popular. Digital payment methods continue to grow, impacting demand for physical cards.

| Digital Payment Type | 2023 Market Value | Growth Rate (2022-2023) |

|---|---|---|

| Mobile Wallets | $6.2 Trillion | 28.6% |

| Cryptocurrency Payments | $2.1 Trillion | 24% |

| Contactless Payments | $5.3 Trillion | 21% |

Entrants Threaten

High Capital Requirements

CPI Card Group faces challenges from new entrants due to high capital demands. The payment card sector needs considerable investments in machinery and technology. Setting up a facility involves huge initial expenses, acting as a deterrent. In 2024, new card manufacturing plants can cost upwards of $50 million. This financial burden limits the number of potential competitors.

Established Customer Relationships

CPI Card Group benefits from established customer relationships with key financial institutions. New competitors face significant hurdles in gaining the trust and securing contracts with these major players. This existing network offers a substantial competitive edge. Data from 2024 shows CPI's strong market share, reflecting these relationships' value.

Stringent Regulatory Requirements

Stringent regulations pose a significant barrier. The payment card industry, including CPI Card Group, faces rigorous rules like PCI DSS. New entrants must invest heavily in compliance. The cost of adhering to these standards is substantial, deterring newcomers. Compliance expenses can reach millions annually, hindering smaller firms.

Economies of Scale

CPI Card Group, as an established player, enjoys significant economies of scale, which translates to lower per-unit production costs. New entrants face a pricing disadvantage until they reach similar production volumes, hindering their ability to compete effectively. Achieving this scale requires a considerable market share, posing a substantial barrier. In 2024, the card manufacturing industry saw a 5% cost advantage for larger firms due to economies of scale.

- Lower production costs benefit existing firms.

- New entrants struggle with initial pricing.

- Substantial market share is crucial for scale.

- Economies of scale create a competitive advantage.

Technological Expertise

The threat of new entrants in the payment card manufacturing industry is significantly impacted by technological expertise. Producing advanced cards, such as EMV and contactless cards, requires specialized knowledge and substantial investment in research and development. New companies face a high barrier to entry due to the need for sophisticated technology and skilled personnel. These technological dependencies act as a considerable obstacle for potential competitors.

- Specialized knowledge and R&D investment are key.

- Advanced technology is a major barrier for new entrants.

- The need for skilled personnel is crucial.

- Technological dependencies limit competition.

Card Manufacturing: Barriers to Entry

New competitors in card manufacturing face significant hurdles due to high initial costs, potentially exceeding $50 million for new facilities in 2024. Established relationships and stringent regulations like PCI DSS further limit entry. Economies of scale and technological expertise provide advantages to existing firms, deterring new entrants.

| Factor | Impact | Data (2024) |

|---|---|---|

| Capital Requirements | High initial investment | New plant costs: $50M+ |

| Regulations | Compliance costs deter | PCI DSS compliance: Millions annually |

| Economies of Scale | Lower production costs | Cost advantage for large firms: 5% |

Porter's Five Forces Analysis Data Sources

The CPI Card Porter's Five Forces analysis leverages industry reports, financial statements, market data, and competitive intelligence to assess market dynamics.