Sainsbury Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Sainsbury Bundle

What is included in the product

Analyzes Sainsbury's competitive landscape, assessing supplier/buyer power, and entry/threat potential.

Instantly identify Sainsbury's vulnerabilities and opportunities with a dynamic, interactive dashboard.

What You See Is What You Get

Sainsbury Porter's Five Forces Analysis

This preview presents the complete Porter's Five Forces analysis of Sainsbury's. It comprehensively assesses industry rivalry, supplier power, buyer power, threat of substitutes, and threat of new entrants. The document is fully formatted, providing a clear, ready-to-use strategic overview. You're seeing the exact analysis you'll download immediately after purchase. No alterations, just instant access to the complete report.

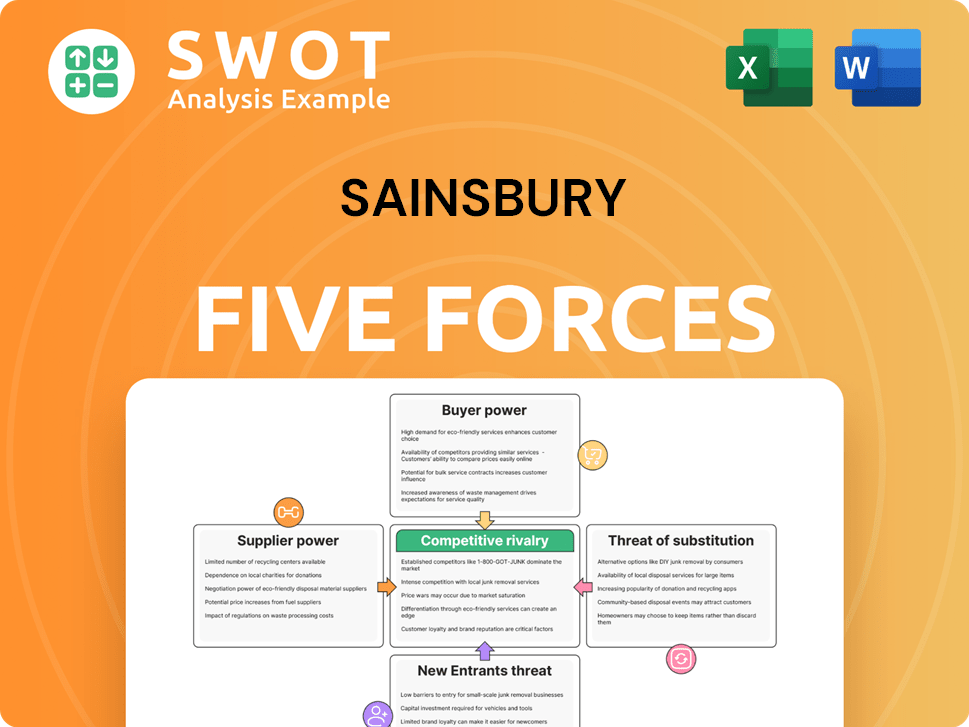

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sainsbury's faces diverse competitive pressures, as assessed by Porter's Five Forces. Bargaining power of suppliers impacts profitability, while buyer power from consumers also plays a key role. The threat of new entrants, like discounters, constantly reshapes the landscape. Substitute products, such as online grocery services, represent another challenge. Competitive rivalry within the UK grocery market is particularly intense. Ready to move beyond the basics? Get a full strategic breakdown of Sainsbury’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Supplier Brand Power Limited

Sainsbury's leverages its private label brands, like Basics and Taste the Difference, to offer consumers alternatives to branded goods. In 2024, private label products accounted for approximately 30% of Sainsbury's total sales, showcasing their importance. This strategy reduces supplier brand power by providing competitive options. This approach limits the pricing and availability control that branded suppliers can exert.

Number of Suppliers

The bargaining power of suppliers for Sainsbury's is generally low because of the high number of available suppliers. Sainsbury's has the flexibility to switch suppliers if necessary. This competitive landscape enables Sainsbury's to negotiate favorable terms and potentially lower prices for goods. For example, in 2024, Sainsbury's worked with over 2,000 suppliers, ensuring diverse sourcing options.

Long-Term Agreements

Sainsbury's leverages long-term agreements to manage supplier power, especially for fresh produce. These contracts help stabilize pricing and supply, crucial in volatile markets. Sainsbury's emphasizes supplier relationships, recognizing their importance to business strategy. In 2024, Sainsbury's reported a 6.9% increase in revenue. These agreements are a key component of their supply chain.

Supplier Relationships

Sainsbury's prioritizes strong supplier relationships, which are crucial for its operations. They actively collaborate with suppliers to manage cost fluctuations effectively. This approach includes supporting farmers and producers to ensure a secure supply chain. In 2024, Sainsbury's reported spending £1.8 billion with UK suppliers, highlighting its commitment. They also aim to help suppliers invest in their businesses.

- Sainsbury's actively collaborates with suppliers to manage cost fluctuations.

- In 2024, Sainsbury's spent £1.8 billion with UK suppliers.

- The company supports farmers and producers for supply chain security.

Productivity Gains

Sainsbury's productivity gains, particularly in its supply chain, allow depots to manage high volumes of fresh food, critical during peak times such as Christmas. This operational efficiency is a direct result of collaboration with their supply base. The consistently growing volumes make Sainsbury's an appealing client for suppliers, fostering strong relationships. For example, in 2024, Sainsbury's reported a 5.3% increase in sales, showing its robust supply chain management.

- Increased Sales: Sainsbury's saw a 5.3% rise in sales in 2024.

- Christmas Peak: The supply chain is crucial for handling high volumes during Christmas.

- Supplier Collaboration: Efficiency stems from working closely with suppliers.

- Attractiveness: Growing volumes make Sainsbury's an attractive client for suppliers.

Supplier Power: How It's Kept Low

Sainsbury's maintains low supplier bargaining power through diverse sourcing and private labels. In 2024, 30% of sales came from private labels, reducing supplier influence. The company's strategic supplier relationships, including £1.8B spent with UK suppliers in 2024, fortify this position.

| Aspect | Details | 2024 Data |

|---|---|---|

| Private Label Sales | Percentage of total sales | ~30% |

| UK Supplier Spending | Total amount spent | £1.8 billion |

| Supplier Count | Approximate number | Over 2,000 |

Customers Bargaining Power

Price Sensitivity

Sainsbury's customers are highly price-sensitive, a common trait in the grocery market. Consumers are always looking for better deals. In response, Sainsbury's invested £1 billion in price reductions. This strategy aimed to attract and keep customers by offering competitive pricing.

Availability of Alternatives

Customers of Sainsbury's benefit from a wide array of choices. Competitors include Tesco, Asda, and Morrisons, alongside discounters such as Aldi and Lidl, providing ample alternatives. This extensive availability of options significantly boosts customer bargaining power in the market. Online platforms and international brands further expand consumer choices, intensifying competition. In 2024, the UK grocery market saw intense price wars, showing customer leverage.

Ease of Price Comparison

Customers' ability to compare prices significantly boosts their bargaining power. Smartphones and the internet enable rapid price checks across retailers. Sainsbury's combats this with strategies like "Aldi Price Match." In 2024, online grocery sales accounted for about 13% of total grocery sales, heightening price sensitivity. This environment pressures Sainsbury's to offer competitive pricing.

Loyalty Programs

Sainsbury's strategically uses loyalty programs to mitigate customer bargaining power. The Nectar program, with over 16 million digital subscribers, offers personalized deals, encouraging repeat purchases. This strategy reduces customer price sensitivity and strengthens brand loyalty. The Nectar Prices initiative provides savings, boosting sales and customer retention. These tactics collectively enhance Sainsbury's market position.

- Nectar's digital engagement drives millions of weekly personalized offers.

- Nectar Prices initiative enhances customer loyalty and boosts sales.

- Over 16 million digital subscribers actively engage with Nectar.

- Loyalty programs reduce customer bargaining power.

Demand for Quality and Sustainability

Customers' demand for quality and sustainable products significantly impacts Sainsbury's strategy. Sainsbury's responds by offering high-quality products at competitive prices. They also focus on ethical sourcing and sustainability. This approach aims to satisfy evolving consumer preferences. In 2024, Sainsbury's reported a 10% increase in sales of its own-brand 'Taste the Difference' range, reflecting the demand for quality.

- Quality products drive sales.

- Sainsbury's emphasizes affordable prices.

- Ethical sourcing is a key focus.

- Sustainability meets consumer needs.

Sainsbury's: Navigating Price Wars and Customer Power

Sainsbury's faces strong customer bargaining power due to price sensitivity and many choices. Online grocery sales hit 13% in 2024, heightening price wars. Loyalty programs, like Nectar with 16M+ subscribers, aim to reduce this power.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Price Sensitivity | High | Intense price wars |

| Customer Choice | Wide | Online grocery sales at 13% |

| Loyalty Programs | Mitigation | Nectar has 16M+ digital users |

Rivalry Among Competitors

Intense Competition

Sainsbury's faces fierce competition in the UK grocery market. Rivals include Tesco, Asda, and Morrisons. Discounters Aldi and Lidl add to the pressure. In 2024, Sainsbury's reported a 1.1% drop in sales volume. This highlights the intense price wars.

Market Share

Maintaining market share demands ongoing investment in both price competitiveness and the overall shopping experience. Sainsbury's has seen modest gains in market share; however, sustaining this requires continuous financial commitment. In 2024, Sainsbury's held approximately 15.2% of the UK grocery market. Market share trends are closely monitored, with the company's ability to maintain or increase its share being critically important for its success.

Online Grocery Shopping

Online grocery shopping is competitive, with Sainsbury's facing traditional and online rivals. Digital performance is key. Sainsbury's saw sales growth via improved online customer experiences. In 2024, online grocery sales in the UK grew, intensifying the competition. Sainsbury's digital sales are crucial for maintaining market share.

Price Wars

The UK supermarket sector is facing heightened price competition, signaling a potential price war. Sainsbury's is actively cutting prices to maintain its market share, responding to competitive pressures. This strategy involves significant investment aimed at attracting and retaining customers. Competitors like Asda are also prioritizing price cuts over profit margins, intensifying the competitive landscape.

- Sainsbury's has been investing in price cuts to combat competition.

- Asda's focus on price cuts intensifies the competitive environment.

- The price war could result in lower prices for consumers.

- The sector's profit margins may be affected by these strategies.

Differentiation

Differentiation is key in the competitive grocery market, and Sainsbury's strives to stand out. The company emphasizes value, quality, and excellent service to differentiate itself from rivals. Sainsbury's has been actively investing in lowering prices and improving its overall value proposition to attract and retain customers. This strategic focus helps them compete effectively.

- Sainsbury's reported a 1.1% increase in like-for-like sales, excluding fuel, in the first half of 2024.

- The company's focus on value includes initiatives to lower prices on essential items.

- Sainsbury's continues to invest in its brand, with a focus on quality and customer experience.

Sainsbury's Navigates UK Grocery Challenges in 2024

Sainsbury's faces tough competition in the UK grocery market, with rivals like Tesco and Asda. Price wars and online grocery competition are intense. Sainsbury's strategy includes price cuts to stay competitive. In 2024, the UK grocery market saw significant changes.

| Metric | Value (2024) | Notes |

|---|---|---|

| Sainsbury's Market Share | 15.2% | Approximate |

| Like-for-like Sales Growth | 1.1% | Excluding fuel |

| Online Grocery Growth | Increased | Intensifying Competition |

SSubstitutes Threaten

Wide Range of Retailers

Sainsbury's confronts a significant threat from substitutes due to the diverse retail landscape. Supermarkets, discounters like Aldi and Lidl, and online retailers offer alternatives. This broad range of options increases the risk of customers switching. In 2024, online grocery sales grew, intensifying substitution pressure. Customers' ability to compare prices and access various brands is a key factor.

Online Retailers

The threat of substitutes for Sainsbury's is significant, particularly from online retailers. Amazon and other e-commerce giants are expanding their grocery and household goods offerings. Sainsbury's has invested heavily in online sales to compete, with online representing a growing share of its revenue. In 2024, online grocery sales accounted for approximately 15% of the UK grocery market, highlighting the need for Sainsbury's to stay competitive in this area.

Non-Food Products

Retailers like House of Fraser and Debenhams offer non-food alternatives, increasing competition for Sainsbury's. In 2024, these stores may offer similar products, impacting Sainsbury's sales. Tu clothing and Argos integration pose challenges in complementing grocery sales. Sainsbury's must compete effectively to maintain market share against these substitutes.

Brand Switching

The threat of substitutes in the grocery sector is significant, given the availability of alternatives. Grocery products are generally not unique, enabling easy brand switching. This poses a considerable risk for retailers like Sainsbury's. To mitigate this, Sainsbury's must prioritize customer satisfaction and focus on competitive pricing.

- In 2024, the UK grocery market saw intense competition, with discounters like Aldi and Lidl increasing their market share.

- Sainsbury's needs to invest in personalized marketing to build brand loyalty.

- Focus on cost savings to offer competitive prices.

Convenience and Accessibility

Sainsbury's faces a significant threat from substitutes due to high convenience and accessibility demands. Consumers often choose supermarkets based on location and ease of shopping, with brand loyalty being relatively weak. This opens the door for competitors like Aldi and Lidl, which have increased their market share. The range of product options is vast, and prices are comparable, making it easy for customers to switch. Sainsbury's must prioritize convenience to maintain its customer base.

- Online grocery shopping saw a 10.8% increase in 2024.

- Discount supermarkets captured 18% of the market in 2024.

- Sainsbury's market share was around 15.6% in 2024.

- Convenience stores grew by 3.2% in 2024.

Sainsbury's Faces Rivals & Market Share Challenges

Sainsbury's confronts substantial threats from substitutes due to competition across the retail landscape, including discounters like Aldi and Lidl. Online retailers, with 10.8% growth in 2024, are also key competitors. Sainsbury's market share was about 15.6% in 2024, and they must innovate to retain customers.

| Substitute Type | 2024 Market Share | Key Challenge |

|---|---|---|

| Discounters (Aldi, Lidl) | 18% | Competitive Pricing |

| Online Retailers | Growing | Convenience |

| Sainsbury's | 15.6% | Customer Loyalty |

Entrants Threaten

Dominant Players

The UK retail sector is largely controlled by Tesco, Sainsbury's, Asda, and Morrisons. These four giants command a substantial market share, making it tough for newcomers. In 2024, these companies had over 70% of the grocery market. New entrants face high barriers to entry due to this concentrated market.

High Entry Barriers

New entrants in the UK food retail industry face considerable hurdles. They need high-quality products at low prices to succeed. High capital needs and established brand loyalty act as major barriers. For example, in 2024, the UK grocery market was dominated by existing players, making it tough for new entrants.

Established Brands

Established brands pose a significant barrier to new entrants. Sainsbury's, with its strong brand recognition, makes it hard for new competitors to gain traction. These giants have loyal customer bases, offering a competitive advantage. Smaller firms like Waitrose, Aldi, and Iceland also add to the market's competitive intensity. The UK supermarket industry generated £218.8 billion in 2024, making it a tough space for newcomers.

Economies of Scale

Economies of scale pose a significant barrier to entry, as established players like Sainsbury's can leverage their size to achieve lower per-unit costs. Sainsbury's has demonstrated a commitment to cost efficiency, targeting £1 billion in cost savings by FY27. This cost advantage makes it difficult for new entrants to compete on price and profitability. They are also planning for significant retail free cash flow over the same period, strengthening their market position.

- Sainsbury's aims for £1 billion in cost savings by FY27.

- Economies of scale provide cost advantages.

- They plan for significant retail free cash flow.

Regulatory Environment

The regulatory environment presents a significant hurdle for new entrants into the retail sector. Complex and costly regulations, including food safety standards and labor laws, increase the initial investment needed. Government regulations and business rates further create barriers to entry, impacting profitability. Sainsbury's has advocated for fairer business rates, highlighting the impact of these costs on retailers.

- Business rates in the UK are a substantial fixed cost for retailers, potentially making it difficult for new entrants to compete with established players.

- Compliance with food safety standards and other regulations can be resource-intensive, requiring significant upfront investment in infrastructure and training.

- Sainsbury's has reported challenges related to evolving regulatory requirements, indicating the ongoing nature of this threat.

- The rising cost of labor, influenced by government policies and minimum wage laws, also affects the financial viability of new market entrants.

UK Grocery Market: A Tough Nut to Crack

The UK grocery market is dominated by established players, creating high barriers for new entrants. Capital requirements and brand loyalty give existing firms an edge. New entrants face challenges competing with the economies of scale and regulatory complexities faced by Sainsbury's and other established retailers.

| Factor | Impact | Data Point (2024) |

|---|---|---|

| Market Concentration | High barriers to entry | Top 4 Grocers Market Share: Over 70% |

| Capital Needs | High initial investment | Cost of setting up a new large store: Millions |

| Brand Loyalty | Established customer base | Sainsbury's Brand Recognition: High |

Porter's Five Forces Analysis Data Sources

Sainsbury's Five Forces assessment leverages financial reports, market analysis, and competitor data for detailed insights.