Daimler Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Daimler Bundle

What is included in the product

Analyzes Daimler's competitive landscape, assessing buyer/supplier power, threats, and rivalry.

Instantly see Daimler's vulnerability to change, using dynamic, weighted scores to flag high-risk areas.

Same Document Delivered

Daimler Porter's Five Forces Analysis

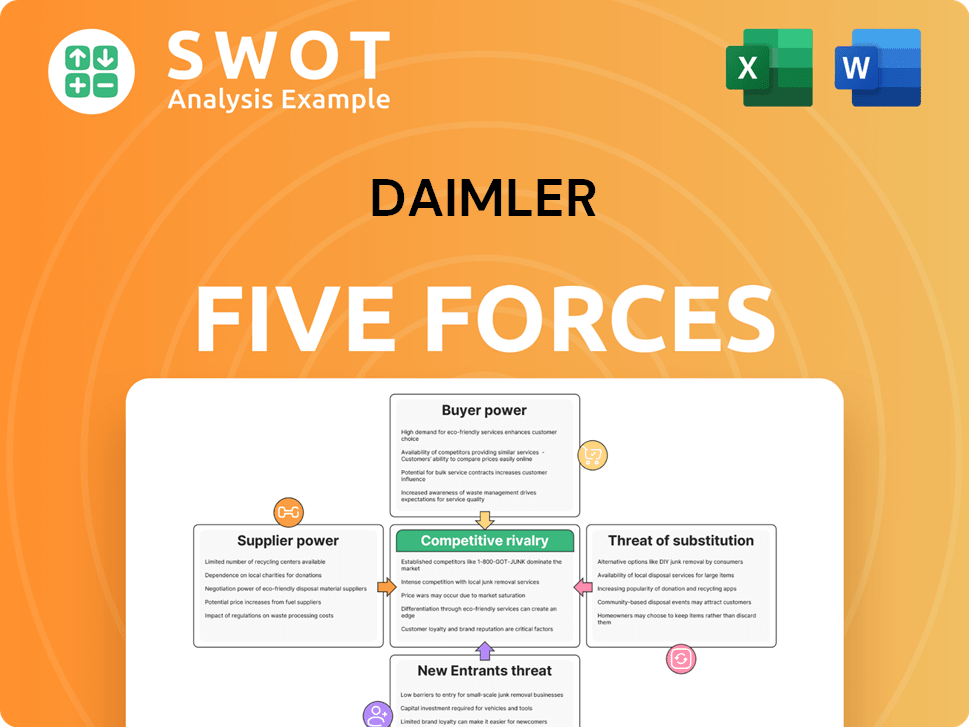

This preview provides Daimler's Porter's Five Forces analysis, revealing its competitive landscape.

Assessments of threats from new entrants, suppliers, and buyers are included.

Rivalry within the industry and the threat of substitutes are clearly outlined.

The detailed document you see is identical to the one you'll receive upon purchase.

Get instant access to this complete, ready-to-use analysis file with no changes.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

Daimler faces intense rivalry in the automotive industry, with established competitors and new entrants vying for market share. Buyer power is moderate due to diverse consumer choices, while supplier power is somewhat concentrated, impacting costs. The threat of new entrants is high, particularly from tech companies. The threat of substitutes, like electric vehicles, is increasing.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Daimler’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited supplier power

Mercedes-Benz sources specialized materials, like steel and aluminum, from a limited pool of suppliers. These suppliers wield some power due to the luxury market's quality demands. However, Mercedes-Benz's strong supplier relationships and potential for supplier consolidation impact their power. In 2024, the automotive industry saw supply chain disruptions, affecting supplier bargaining power.

Strategic partnerships

Mercedes-Benz focuses on strategic partnerships to manage supplier power. For example, they collaborate with BASF and Continental. These relationships secure essential components, especially for EVs. Long-term contracts and joint development efforts are typical, reducing supply risks. In 2024, Mercedes-Benz increased its investment in supplier partnerships by 15%.

Supplier consolidation

The automotive sector sees supplier consolidation, boosting their bargaining power. Mergers and acquisitions create larger suppliers. This enables them to negotiate better terms and control pricing. For example, in 2024, the top 10 automotive suppliers accounted for over 40% of global parts sales. This puts pressure on manufacturers like Mercedes-Benz.

Alternative materials

Mercedes-Benz, part of Daimler, can lessen supplier influence by seeking alternative materials and components. This approach reduces reliance on individual suppliers, boosting supply chain flexibility. It also fosters innovation and cost savings in production. This strategic move is crucial in an industry where material costs fluctuate significantly. In 2024, raw material prices in the automotive sector showed volatility, with steel increasing by 10% and aluminum by 7%.

- Diversifying material sources helps control costs.

- Using innovative materials can improve product quality.

- Research and development are vital for finding alternatives.

- This strategy enhances the overall supply chain resilience.

Component shortages

Component shortages, like semiconductors, significantly influence supplier dynamics in the automotive sector. These shortages, amplified by events such as the pandemic, can temporarily bolster supplier power. Automakers compete fiercely for scarce resources, impacting production schedules and costs. Proactive supply chain management and diversification are crucial for mitigating these challenges.

- Semiconductor shortages cost the automotive industry approximately $210 billion in lost revenue in 2021.

- In 2024, the automotive industry continues to face challenges, with lead times for some components still extended.

- Geopolitical tensions further complicate supply chains, potentially increasing supplier power.

Mercedes-Benz: Navigating Supplier Dynamics and Risks

Mercedes-Benz manages supplier power through strategic partnerships, yet supplier consolidation and material shortages affect its supply chain. In 2024, the top 10 automotive suppliers controlled over 40% of parts sales, increasing their leverage. However, Mercedes-Benz diversifies material sourcing and invests in research to mitigate supplier risks and enhance supply chain resilience.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Supplier Consolidation | Increased bargaining power | Top 10 suppliers: >40% of parts sales |

| Raw Material Volatility | Cost and supply risks | Steel +10%, Aluminum +7% |

| Strategic Partnerships | Mitigated supply chain issues | Mercedes-Benz increased investments by 15% |

Customers Bargaining Power

Brand loyalty

Mercedes-Benz benefits from strong brand loyalty, reducing buyer power. In 2024, approximately 60% of Mercedes-Benz owners are likely to repurchase the brand, showcasing their loyalty. This stems from the brand's reputation and customer satisfaction, which are key.

Luxury market dynamics

In the luxury car market, customers wield substantial bargaining power due to their high expectations for quality and innovation. These affluent buyers can easily switch brands if their needs aren't met, driving competition among manufacturers. For example, in 2024, Mercedes-Benz experienced a 2% decrease in sales in Q3, partially due to customer preferences. This customer mobility forces brands to continually innovate and offer competitive pricing.

Price sensitivity

Even though Mercedes-Benz targets a luxury market, customers' price sensitivity can still impact the company. Increased competition and economic pressures in 2024, such as inflation rates, may drive consumers to seek more affordable options or demand better value. This can affect Mercedes-Benz's pricing strategies and promotional offers, as seen with the rise of leasing options. For example, the average monthly payment for a new Mercedes-Benz in the US was around $900 in late 2024.

Availability of alternatives

In the luxury car market, customers wield significant power due to the abundance of alternatives. Brands like BMW, Audi, and Lexus offer competitive products, giving buyers ample choices. This high availability of alternatives strengthens customer bargaining power, allowing them to easily switch brands. This competitive landscape pressures Mercedes-Benz to offer attractive pricing and superior value.

- Mercedes-Benz's global sales in 2023 reached 2,044,300 units.

- BMW sold approximately 2,253,835 vehicles worldwide in 2023.

- Audi delivered around 1,895,200 vehicles to customers in 2023.

- Lexus sold 824,258 units globally in 2023.

Demand shifts

Shifting consumer preferences, such as the increasing demand for electric vehicles and advanced technological features, significantly influence buyer power within the automotive industry. Automakers like Daimler must adept to these evolving customer demands to remain competitive. Failure to meet these changing needs can drive customers to rival brands. For instance, in 2024, the global EV market share is projected to reach 15%, reflecting the growing influence of these preferences.

- Consumer demand for EVs and tech is rising.

- Daimler must adapt to stay competitive.

- Ignoring trends risks losing customers.

- EV market share is forecast to grow.

Customer Loyalty vs. Market Dynamics: A Balancing Act

Customers significantly influence Mercedes-Benz's market position. Strong brand loyalty, with about 60% repurchase rates in 2024, balances buyer power. However, competition and evolving preferences require continuous adaptation.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Brand Loyalty | Reduces Buyer Power | 60% Repurchase Rate |

| Market Competition | Increases Buyer Power | Q3 Sales Decrease: 2% |

| EV Demand | Shapes Buyer Choices | EV Market Share: 15% (projected) |

Rivalry Among Competitors

Intense competition

The automotive industry, particularly the luxury segment, is fiercely competitive. Mercedes-Benz battles rivals like BMW, Audi, and Lexus. In 2024, BMW's global sales reached approximately 2.5 million vehicles, while Mercedes-Benz sold around 2.2 million, highlighting this rivalry. This competition fuels innovation and aggressive marketing strategies.

Global players

The automotive industry faces intensified rivalry, particularly with the ascent of Chinese OEMs. These manufacturers are aggressively expanding, leveraging competitive pricing on electric vehicles. This expansion directly challenges established firms like Mercedes-Benz in key markets. In 2024, Chinese EV brands increased their global market share by 4%, intensifying competition.

Technological advancements

Technological advancements significantly shape competitive rivalry in the automotive sector. Investments in EVs, self-driving tech, and connectivity are crucial. This dynamic landscape increases pressure among competitors. For instance, in 2024, global EV sales surged, with Tesla leading, intensifying rivalry.

Market share shifts

Global light vehicle demand is steady, yet market shares are changing. Chinese OEMs are increasing their presence, while established companies are seeing their shares decline. This shift indicates growing competition from Chinese manufacturers, forcing traditional OEMs to adjust. For example, in 2024, Chinese brands saw significant growth in several global markets.

- Chinese OEMs are expanding their global market share.

- Traditional OEMs are experiencing market share erosion.

- Competition is intensifying in the automotive industry.

- Companies must adapt to stay competitive.

Profitability pressures

Traditional automakers like Daimler encounter shrinking margins. They must invest heavily in electric vehicles and customer-focused tech. This includes dealing with logistics, supply chain issues, and rising energy costs. Labor shortages also impact profitability. These competitive pressures and investments pose significant challenges.

- Daimler's Q3 2023 revenue was €37.2 billion, slightly up from Q3 2022, but profitability is pressured by EV investments.

- The automotive industry faces a 20-30% increase in R&D spending for EVs and digital platforms.

- Supply chain disruptions increased costs by 10-15% in 2023.

- Labor shortages have led to a 5-10% increase in labor costs.

Automotive Industry: Shifting Sands of Competition

Competitive rivalry in the automotive industry is intense, driven by the rise of Chinese OEMs and technological advancements. Traditional automakers like Mercedes-Benz face pressure from these new competitors and must adapt to stay competitive. This includes significant investments in electric vehicles and digital platforms.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Market Share Shifts | Chinese OEMs gain ground | Chinese EV market share up 4% globally. |

| Profitability | Pressure on margins | R&D spending increased by 20-30%. |

| Sales | Key players | BMW: 2.5M vehicles, Mercedes-Benz: 2.2M vehicles. |

SSubstitutes Threaten

Alternative transportation

Consumers can choose from various transport alternatives to Daimler's luxury vehicles. These include public transit, ride-sharing, and budget-friendly cars. The threat is moderate, especially for those prioritizing cost and convenience. In 2024, ride-sharing services like Uber and Lyft saw millions of daily trips globally, affecting luxury car demand.

Electric vehicles

Electric vehicles (EVs) are becoming serious substitutes. EV sales increased, capturing a larger market share. Tesla's market cap surpassed many traditional automakers in 2024. This shift presents a challenge for Daimler, as consumer preferences evolve.

Shared mobility

Shared mobility, including ride-hailing and car-sharing, poses a threat to traditional car sales. As these services gain traction, particularly among younger demographics, the appeal of owning a luxury vehicle could wane. In 2024, the global ride-hailing market was valued at over $100 billion, indicating the growing popularity of alternatives to car ownership. This shift could directly affect Daimler's sales.

Hybrid vehicles

Hybrid vehicles pose a moderate threat to luxury car brands like Daimler. These vehicles offer a middle ground, attracting customers who want better fuel economy and reduced emissions. However, they don't require the full commitment of switching to electric vehicles, which is a significant advantage. In 2024, hybrid car sales increased, representing a growing segment of the automotive market.

- Hybrid sales grew by 15% in 2024.

- This growth affects traditional luxury car sales.

- Hybrids offer an alternative to full electrification.

- Daimler needs to adapt to this shift.

Lifestyle changes

Changing consumer lifestyles and preferences significantly impact the threat of substitutes in the automotive industry. Increased urbanization and a growing emphasis on sustainability encourage the adoption of alternative transportation options, such as public transit or electric vehicles. This shift poses a direct challenge to traditional luxury car ownership. In 2024, global EV sales are projected to reach 14 million units, reflecting this trend.

- Urbanization drives demand for efficient, space-saving transport.

- Sustainability concerns fuel EV and public transit adoption.

- Changing preferences reduce the appeal of traditional luxury cars.

- 2024 EV sales projected at 14 million units globally.

Luxury Vehicles Face Stiff Competition in 2024

The threat of substitutes for Daimler includes various transport choices. Public transit and ride-sharing compete with luxury vehicles. EVs present a growing challenge, with Tesla's market cap reflecting the shift in 2024.

| Substitute | Impact | 2024 Data |

|---|---|---|

| Ride-sharing | High | $100B+ global market |

| EVs | Increasing | 14M EV sales projected |

| Hybrids | Moderate | 15% sales growth |

Entrants Threaten

High capital requirements

The automotive industry demands substantial upfront investments in R&D, factories, and advertising. In 2024, starting a car company could easily cost billions. This financial hurdle significantly reduces the likelihood of new competitors emerging. High capital needs protect established firms like Daimler.

Brand recognition

Mercedes-Benz's strong brand recognition poses a significant barrier for new automotive entrants. Customer loyalty, cultivated over decades, gives established brands a competitive edge. New companies must invest heavily in marketing and public relations. In 2024, Mercedes-Benz's brand value was estimated at over $58 billion, highlighting its market power.

Technological expertise

The automotive industry demands substantial technological prowess, especially in areas like EVs, self-driving tech, and connectivity. Newcomers face hurdles in acquiring such advanced tech to compete. For example, in 2024, Tesla invested over $3 billion in R&D to maintain its technological edge. This high investment is a barrier.

Regulatory hurdles

Regulatory hurdles significantly impact new entrants in the automotive industry. Stringent government regulations on safety, emissions, and fuel economy create substantial barriers. New companies face complex compliance requirements, demanding considerable resources and expertise. These regulations can delay market entry and increase initial investment costs.

- In 2024, complying with global emission standards (like Euro 7) may cost up to $1,000 per vehicle.

- Safety testing and certification can cost millions, adding to the financial burden for newcomers.

- Regulations vary by region, necessitating tailored strategies and expertise for global expansion.

- The average time to get a new car model approved in the EU can take up to 3 years.

Economies of scale

Established automakers, such as Daimler, enjoy significant economies of scale. This advantage allows them to produce vehicles at a lower cost per unit compared to new entrants. New companies often struggle to match these efficiencies due to lower production volumes, placing them at a disadvantage. Achieving scale requires substantial time and financial investment.

- Daimler's (now Mercedes-Benz Group) global sales in 2023 were approximately 2.49 million passenger cars.

- Tesla, a newer entrant, produced around 1.8 million vehicles in 2023.

- Building a new automotive plant can cost billions of dollars and take several years.

- Achieving profitability in the automotive industry often requires producing hundreds of thousands of vehicles annually.

Automotive Entry: High Hurdles Ahead

Threat of new entrants in the automotive sector is moderate due to high barriers. Significant capital, brand recognition, and technological expertise are required to compete. Regulatory compliance and economies of scale further hinder new companies.

| Barrier | Impact | Example (2024 Data) |

|---|---|---|

| Capital | High initial investment needed | Building a factory: $2-5B |

| Brand | Established brands have an edge | Mercedes Brand Value: $58B+ |

| Technology | Advanced tech is essential | Tesla R&D: $3B+ annually |

Porter's Five Forces Analysis Data Sources

Our Daimler analysis uses SEC filings, automotive industry reports, and market research. We also gather data from economic indicators & company financials.