Ryan Specialty Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Ryan Specialty Group Bundle

What is included in the product

Tailored exclusively for Ryan Specialty Group, analyzing its position within its competitive landscape.

Instantly understand strategic pressure with a powerful spider/radar chart.

Preview Before You Purchase

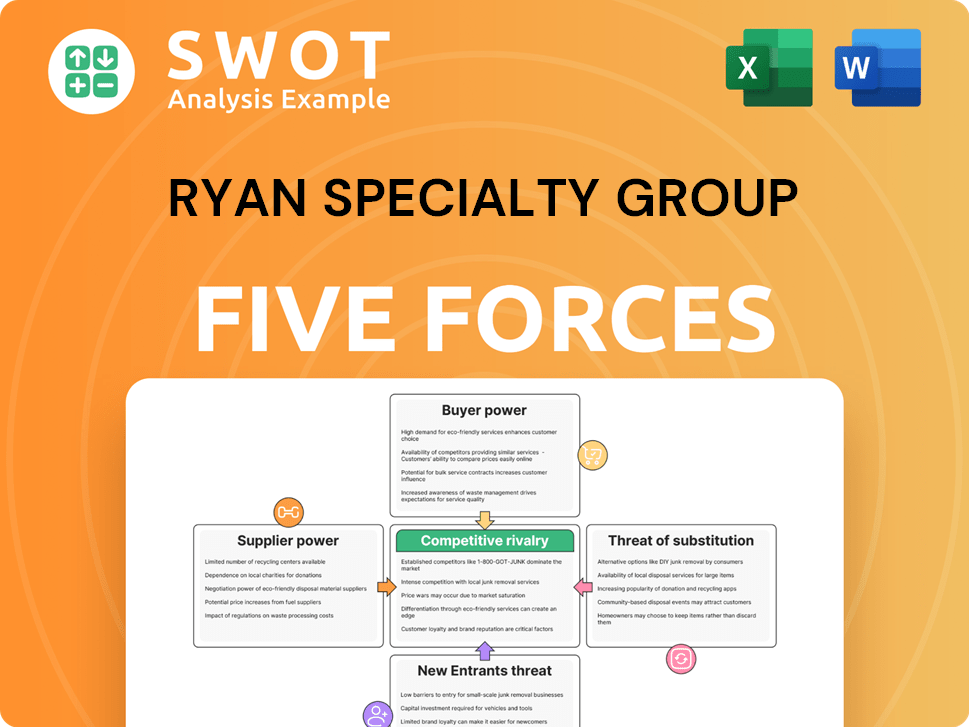

Ryan Specialty Group Porter's Five Forces Analysis

This is the comprehensive Porter's Five Forces analysis you’ll get after purchase, thoroughly examining Ryan Specialty Group. It covers key competitive elements, including industry rivalry, supplier power, and buyer power. The analysis also assesses the threat of new entrants and the threat of substitutes. You're seeing the exact, ready-to-download document.

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

Ryan Specialty Group operates in a competitive insurance market, facing pressures from various forces. Supplier power, particularly from reinsurers, plays a crucial role in cost dynamics. Buyer power is moderate, influenced by the presence of brokers and insured entities. The threat of new entrants is relatively low due to high barriers. Competitive rivalry is intense with established players. The threat of substitutes, mainly alternative risk solutions, adds complexity.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ryan Specialty Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

Ryan Specialty Group's reliance on specialized insurance expertise and data analytics from suppliers grants them considerable leverage. These suppliers, holding unique knowledge, can influence costs. In 2024, the insurance industry saw a rise in data analytics spending, increasing supplier power.

Supplier Power 2

Ryan Specialty Group faces supplier power from a limited pool of specialized insurance providers. These providers, offering unique, niche insurance products, hold significant sway. Their ability to dictate terms is enhanced by the lack of readily available alternatives, potentially impacting costs. This dynamic is reflected in the insurance market's specialized segments. For example, in 2024, the top 10 global insurance companies controlled a substantial portion of the market, thereby increasing supplier concentration.

Supplier Power 3

Ryan Specialty Group faces moderate supplier power. Switching costs for specialized insurance services can be high. The integration of new suppliers may involve significant IT and data migration expenses. In 2024, the insurance industry saw a 5% increase in IT spending, adding to switching complexity.

Supplier Power 4

Supplier power in Ryan Specialty Group's context relates to the influence of service providers, potentially including reinsurers and specialized underwriters. Suppliers could, in theory, integrate forward, although this is less common in the insurance sector compared to manufacturing. The ability of suppliers to offer services directly to brokers and agents would increase their bargaining power, potentially disintermediating Ryan Specialty Group. This threat is mitigated by the specialized nature of Ryan Specialty Group's services and its established relationships. The insurance industry saw over $600 billion in premiums written in 2024, but disintermediation remains a limited threat.

- Reinsurers: Key suppliers with significant influence due to their role in risk transfer.

- Specialized Underwriters: Providers of unique expertise, able to exert influence.

- Brokerage Networks: Potential direct service providers, posing a disintermediation risk.

- Market Dynamics: Industry-specific factors that influence supplier power.

Supplier Power 5

Ryan Specialty Group's (RSG) suppliers, particularly those with proprietary data, wield substantial influence. These suppliers often possess unique insights into risk assessment and market trends, giving them an edge in negotiations. This data advantage allows them to dictate terms, affecting RSG's operational costs and service offerings. This dynamic is crucial to understand when evaluating RSG's market position.

- Proprietary data enables suppliers to set pricing and terms.

- RSG's dependence on specific data sources increases supplier power.

- Limited competition among data providers can further strengthen supplier influence.

- Data exclusivity directly impacts RSG's profitability and market competitiveness.

RSG's Supplier Power: Data & Market Dynamics

Ryan Specialty Group (RSG) faces moderate supplier power due to specialized expertise and data dependency. Limited competition among data providers strengthens supplier influence, impacting costs. The insurance industry saw over $600 billion in premiums written in 2024.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Data Dependence | High | Data analytics spending increased 5% |

| Supplier Concentration | Moderate | Top 10 insurers control substantial market share |

| Switching Costs | Moderate | IT spending up 5% |

Customers Bargaining Power

Buyer Power 1

Ryan Specialty Group's extensive broker network gives customers considerable bargaining power. A vast network of brokers and agents means clients have choices. For example, in 2024, Ryan Specialty Group’s network included over 4,000 brokers. This broad reach allows customers to negotiate better terms.

Buyer Power 2

Buyer power significantly impacts Ryan Specialty Group. Price sensitivity varies across segments. For example, in 2024, specialized insurance premiums saw fluctuations, reflecting customer negotiation abilities. Complex or highly specialized products often face less price sensitivity than standard offerings. This dynamic shapes Ryan Specialty's pricing strategies and profitability.

Buyer Power 3

Customer bargaining power is moderate. Customers, like brokers, can switch to competitors. In 2024, the insurance brokerage market saw significant competition. Brokers and agents can move business. Data from 2024 shows that switching costs are relatively low.

Buyer Power 4

Buyer power is a significant factor for Ryan Specialty Group. Large brokerage houses can aggregate demand, giving them more leverage when negotiating with Ryan Specialty Group. This can lead to pressure on pricing and service terms. Specifically, in 2024, the top 10 global insurance brokers controlled a substantial portion of the market.

- Demand aggregation enables larger brokers to negotiate better terms.

- Pricing and service terms are under pressure due to high buyer power.

- Market concentration among large brokers is high.

- This affects Ryan Specialty Group's profitability.

Buyer Power 5

Ryan Specialty Group's ability to withstand customer bargaining power hinges on its service differentiation. This means how uniquely it can offer services that clients can't easily find elsewhere. Strong differentiation enables the company to command better prices and terms. In 2024, the specialty insurance market, where Ryan Specialty operates, saw a 7% increase in premiums, showing ongoing demand. Therefore, unique services are crucial.

- Differentiated services reduce customer price sensitivity.

- Specialized expertise creates barriers to switching providers.

- Strong client relationships lessen buyer power.

- Market leadership enhances pricing leverage.

Customer Power & Market Dynamics

Ryan Specialty Group faces moderate customer bargaining power. Customers can switch to competitors; in 2024, market competition was high. Large brokers aggregate demand, pressuring pricing. Differentiation through services like specialized expertise is key.

| Aspect | Impact | Data (2024) |

|---|---|---|

| Broker Network | Customer Choice | 4,000+ brokers |

| Market Competition | Switching Options | High in insurance brokerage |

| Premium Growth | Demand | Specialty insurance: +7% |

Rivalry Among Competitors

Competitive Rivalry 1

The specialty insurance market is fragmented, featuring many players. This includes many wholesale brokers and underwriting managers, intensifying competition. In 2024, the global insurance market was valued at approximately $6.7 trillion, and the specialty segment is highly competitive. This fragmentation means no single entity dominates, leading to constant jockeying for market share.

Competitive Rivalry 2

Competitive rivalry in the insurance industry is fierce, with service innovation being a key differentiator. Companies continuously develop new insurance products and enhance service offerings to attract and retain clients. For example, in 2024, the global insurance market was valued at approximately $6.3 trillion, and it's highly competitive.

Competitive Rivalry 3

Acquisitions and consolidation are prevalent in the insurance industry. Ryan Specialty Group actively participates in mergers and acquisitions, like the 2024 acquisition of Socius Insurance Services. This reshapes the competitive environment, leading to larger, more influential competitors. For example, in 2024, the top 10 insurance brokers controlled a significant market share.

Competitive Rivalry 4

Competitive rivalry in Ryan Specialty Group is amplified by its focus on niche markets. This specialization intensifies competition, as firms target specific risk categories. The company faces fierce competition within specialized areas. For instance, in 2024, the market for professional liability insurance saw increased competition.

- Specialization drives rivalry.

- Niche markets are highly contested.

- Competition in specialized risk areas.

- Professional liability insurance is competitive.

Competitive Rivalry 5

Competitive rivalry within Ryan Specialty Group is significantly shaped by performance metrics, pushing firms to excel. Competition is fierce, with companies vying for market share based on service speed and expertise. Underwriting proficiency and claims handling efficiency are key differentiators. This dynamic environment fosters innovation and better service for clients.

- Ryan Specialty's revenue increased to $2.7 billion in 2023, reflecting strong market competition.

- The specialty insurance market is highly fragmented, increasing rivalry.

- Efficiency in claims processing is a critical competitive factor, with average processing times constantly monitored.

Ryan Specialty Group Faces Fierce Market Competition

Competitive rivalry at Ryan Specialty Group is intense due to market fragmentation and specialization. Firms compete fiercely, driving innovation in services and products. For example, in 2023, Ryan Specialty Group reported revenues of $2.7 billion, highlighting strong market competition.

| Aspect | Details | 2024 Data |

|---|---|---|

| Market Value | Global Insurance Market | $6.7 trillion |

| Competitive Factors | Service speed, expertise | Underwriting proficiency, claims handling |

| Key Strategy | M&A (e.g., Socius) | Consolidation activity |

SSubstitutes Threaten

Threat of Substitution 1

The threat of substitutes for Ryan Specialty Group comes from direct insurance writing. Carriers selling specialty insurance directly to brokers and agents could bypass wholesale brokers. This shift could impact Ryan Specialty's role. In 2024, direct sales strategies are increasing, potentially affecting wholesale broker market share. This trend reflects evolving distribution models.

Threat of Substitution 2

Technology-driven solutions are emerging rapidly. Insurtech companies are developing risk assessment and placement solutions, acting as substitutes. These alternatives could reduce the need for traditional intermediaries like Ryan Specialty Group. For example, in 2024, insurtech funding reached $14.8 billion globally, signaling growing competition.

Threat of Substitution 3

The threat of substitutes for Ryan Specialty Group comes from alternative risk transfer (ART) methods. These include captive insurance companies. In 2024, the ART market was estimated at $100 billion. These solutions can replace traditional insurance products.

Threat of Substitution 4

The threat of substitutes for Ryan Specialty Group (RSG) is moderate. Standardization in specialty insurance could lessen the demand for specialized brokers. However, RSG's focus on complex risks provides some protection. This differentiation limits the availability of direct substitutes. The industry is evolving, but RSG's niche remains valuable.

- Standardization of specialty products reduces the need for specialized brokers.

- RSG's focus on complex risks provides some protection.

- The industry is evolving, but RSG's niche remains valuable.

- The company's revenue in 2024 was $2.5 billion.

Threat of Substitution 5

The threat of substitutes for Ryan Specialty Group (RSG) is moderate. Enhanced data analytics tools are enabling customers, like large corporations, to manage risk more effectively. Brokers and agents with improved data capabilities could bypass RSG for specialized risk placement. This shift could impact RSG's revenue, especially in areas where data-driven solutions are rapidly advancing.

- Data analytics spending by insurance companies is projected to reach $19.4 billion in 2024.

- The global InsurTech market was valued at $11.1 billion in 2023.

- RSG's revenue in Q1 2024 was $682.2 million.

RSG's Substitute Threats: A Market Overview

The threat of substitutes for Ryan Specialty Group (RSG) is moderate, driven by evolving market dynamics. Direct insurance writing and insurtech solutions offer alternatives, potentially impacting RSG's role. Alternative risk transfer methods also present competition.

RSG's focus on complex risks and specialized services offers protection against substitutes. However, the rise of data analytics and standardization in specialty products requires RSG to innovate. RSG's 2024 revenue reached $2.5 billion, indicating a strong market position despite these challenges.

| Substitute | Impact | Data Point (2024) |

|---|---|---|

| Direct Insurance | Bypasses brokers | Growing market share |

| Insurtech | Risk assessment solutions | $14.8B global funding |

| ART Methods | Replaces products | $100B market est. |

Entrants Threaten

Threat of New Entrants 1

The threat of new entrants for Ryan Specialty Group is moderate due to high barriers to entry. Establishing underwriting capabilities and a robust distribution network demands significant capital. For example, in 2024, setting up a specialized insurance brokerage can cost millions.

Threat of New Entrants 2

The threat from new entrants for Ryan Specialty Group is moderate due to significant regulatory hurdles. The insurance sector is tightly regulated, demanding substantial capital and compliance expertise. New firms face high initial costs to meet these requirements. For example, in 2024, the average cost to establish a new insurance agency was about $300,000, reflecting the complexity of entry.

Threat of New Entrants 3

The threat of new entrants for Ryan Specialty Group is moderate. Established relationships play a significant role in the insurance industry. Existing connections between brokers, agents, and carriers create a barrier for new firms.

Threat of New Entrants 4

The threat of new entrants to Ryan Specialty Group is moderate. Brand reputation is critical; building a strong brand in insurance requires significant time and resources. New entrants face substantial barriers, including regulatory hurdles and the need for established relationships. However, the market's growth potential and the availability of capital could attract new players.

- High capital requirements for compliance and operations.

- Existing distribution networks and relationships with brokers.

- Regulatory compliance is complex and time-consuming.

- Established brand recognition and market share.

Threat of New Entrants 5

The threat of new entrants for Ryan Specialty Group is moderate due to barriers like specialized expertise. Accessing and mastering the intricacies of underwriting and distribution, particularly in niche insurance areas, is a significant hurdle. New entrants face challenges in recruiting and keeping professionals with the required expertise, which impacts their ability to compete effectively. The insurance industry is competitive, with established players holding a strong market position.

- Specialized knowledge in underwriting and distribution is a barrier.

- Recruiting and retaining qualified experts is challenging.

- Established firms possess significant market advantages.

- The insurance industry is highly competitive.

Insurance Entry: High Costs, Tough Competition

The threat from new entrants is moderate, influenced by high barriers. Establishing insurance operations requires substantial capital. In 2024, setting up a brokerage could cost millions. Regulatory hurdles and established market players further limit new competition.

| Barrier | Impact | 2024 Data |

|---|---|---|

| Capital Requirements | High | Brokerage setup: ~$2M-$5M |

| Regulations | Complex | Compliance costs: ~$300,000 |

| Market Dynamics | Established | Market share concentration |

Porter's Five Forces Analysis Data Sources

We base our analysis on SEC filings, insurance industry reports, and market analysis databases. These help gauge competitiveness, buyer power, and rivalry.