Samsung SDI Co Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Samsung SDI Co Bundle

What is included in the product

Analyzes Samsung SDI Co's competitive landscape, identifying challenges from rivals, buyers, and suppliers.

Dynamic force visualization—easily see evolving competitive pressures.

Preview Before You Purchase

Samsung SDI Co Porter's Five Forces Analysis

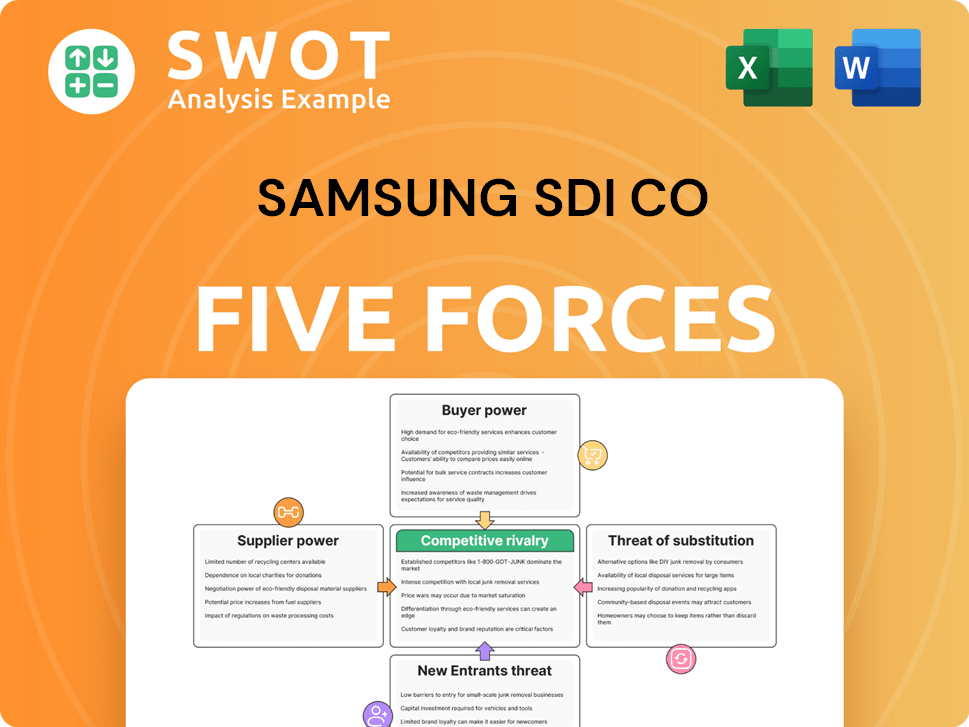

This preview offers Samsung SDI Co.'s Porter's Five Forces Analysis. It covers competitive rivalry, supplier power, buyer power, threat of substitutes, & threat of new entrants.

The analysis is thorough, examining each force's impact on SDI's battery and materials business.

You're viewing the actual document. Once purchased, you'll get immediate, full access to this exact file.

No edits or changes—the document is ready to use as soon as your transaction is complete.

Get this comprehensive analysis instantly after buying—no delays, no alterations needed!

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Samsung SDI Co faces intense rivalry, especially from competitors like LG Energy Solution. Bargaining power of buyers is moderate due to diverse end-markets. Supplier power is a factor given raw material dependence, like lithium. Threat of new entrants is moderate, hindered by high capital needs. The threat of substitutes, especially from alternative battery technologies, exists.

The complete report reveals the real forces shaping Samsung SDI Co’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Limited Key Suppliers

Samsung SDI faces strong supplier bargaining power due to a concentrated raw material market. Key suppliers, such as those providing lithium, hold significant control over the supply chain. In 2021, the top three lithium suppliers controlled over 50% of the global supply, impacting pricing. This concentration can drive up costs for Samsung SDI.

Dependence on Specific Materials

Samsung SDI's bargaining power of suppliers is influenced by its dependence on specific materials essential for battery production. The company is heavily reliant on materials like lithium and cobalt. Price fluctuations in these materials directly affect Samsung SDI's profitability. For example, battery-grade lithium prices peaked at around $75,000 per metric ton in 2022.

Influence on Pricing

Samsung SDI's profitability is significantly impacted by supplier bargaining power, especially concerning raw materials. Material price volatility directly affects pricing strategies; for instance, lithium prices surged over 300% in 2022. This volatility challenges Samsung SDI's cost management and pricing predictability. Strong supplier influence can squeeze profit margins.

Vertical Integration Potential

Several suppliers are considering vertical integration, aiming to boost production control and influence pricing. This strategic move could enhance their bargaining power, potentially limiting Samsung SDI's choices. For instance, Albemarle's investments in mining operations aim to control lithium supplies. This shift could impact Samsung SDI's costs and supply chain stability.

- Albemarle's 2023 revenue: $9.6 billion.

- Lithium price volatility in 2024: Significant fluctuations due to demand and supply shifts.

- Samsung SDI's 2023 revenue: Approximately $18 billion (estimated).

- Vertical integration trend: Increasing among battery material suppliers.

Long-Term Agreements

Samsung SDI's bargaining power with suppliers is influenced by long-term agreements. These agreements are vital for shielding against price volatility and supply disruptions. Securing stable production costs is a key benefit. According to a 2024 industry report, 70% of firms use long-term contracts with suppliers.

- Long-term agreements provide price stability.

- They help secure a consistent supply of materials.

- This strategy is common in the industry.

Supplier Power Squeezes Battery Maker

Samsung SDI faces strong supplier bargaining power, especially for essential materials like lithium and cobalt. The top lithium suppliers control a significant market share. Vertical integration by suppliers, like Albemarle with $9.6B revenue in 2023, further strengthens their position.

| Aspect | Impact | Data |

|---|---|---|

| Concentrated Market | Increased costs | Top 3 Li suppliers control >50% of global supply (2021) |

| Material Dependence | Profit margin squeeze | Li prices peaked at ~$75,000/MT (2022) |

| Vertical Integration | Reduced choices | Albemarle's 2023 Revenue: $9.6B |

Customers Bargaining Power

Customer Concentration

Samsung SDI's customer base includes major automotive manufacturers, energy storage system integrators, and IT device companies. The bargaining power of these customers is moderate due to their large purchasing volumes. Samsung SDI supplies batteries for BMW, Rivian, and Audi. Declining sales in these models have negatively impacted Samsung SDI's battery usage; for example, BMW's global sales decreased by 1.5% in 2024.

Switching Costs

Switching costs significantly influence customer bargaining power. For products like mobile phones, where switching is easy, customer power is high. Despite this, Samsung's brand loyalty in home appliances somewhat mitigates this. In 2024, Samsung's revenue was approximately $250 billion, with no single customer holding major sway over sales. Thus, individual customer bargaining power remains limited.

Price Sensitivity

Customers' price sensitivity significantly impacts Samsung SDI, especially in the EV battery market. Intense competition among auto manufacturers creates substantial pricing pressure. The average selling price of lithium-ion batteries decreased by about 20% between 2020 and 2022, reflecting this trend. This pressure forces Samsung SDI to manage costs and potentially lower prices to remain competitive.

Product Differentiation

Samsung SDI's product differentiation, driven by advanced technology and quality, lessens customer bargaining power. This strength is evident in its battery and material solutions for EVs and electronics. The company's ability to innovate, as seen in its solid-state battery developments, is crucial for maintaining this advantage. However, constant innovation is essential to protect against the erosion of this advantage. Samsung SDI invested ₩867 billion in R&D in 2023, showing its commitment to staying ahead.

- Technological Innovation: Samsung SDI invests heavily in R&D to differentiate its products.

- Product Quality: High-quality products reduce customer leverage.

- Continuous Maintenance: Ongoing innovation is vital to sustain differentiation.

- Financial Commitment: ₩867 billion R&D investment in 2023 supports differentiation.

Demand Slowdown

A slowdown in demand from major car OEMs in Europe and North America has negatively impacted Samsung SDI's battery usage. This decline in demand increases customer bargaining power, as OEMs have more options. The downward trend in Samsung SDI's battery usage was mainly caused by a decline in demand for batteries from major car OEMs in Europe and North America. This situation allows customers to negotiate lower prices or demand better terms.

- In 2024, the global EV market growth slowed, with some regions experiencing demand contraction.

- Samsung SDI's battery sales growth rate has decreased due to this market shift.

- Car manufacturers can now more easily switch between battery suppliers.

- Customer bargaining power is up, putting pressure on margins.

Samsung SDI's Customer Power: A Balancing Act

The bargaining power of Samsung SDI's customers is moderate, influenced by factors like large purchase volumes from major automotive manufacturers such as BMW and Audi. Switching costs play a crucial role; ease of switching, as seen in mobile phones, increases customer power. Pricing pressure, especially in the EV battery market, is a key factor.

| Aspect | Impact | Data |

|---|---|---|

| Customer Base | Moderate bargaining power | BMW sales decreased 1.5% in 2024 |

| Switching Costs | Impact on power | Samsung's 2024 revenue approx. $250B |

| Price Sensitivity | High in EV market | Li-ion battery ASP decreased 20% (2020-2022) |

Rivalry Among Competitors

Intense Competition

The material and energy solutions industry is fiercely competitive, with numerous companies striving for dominance. Samsung SDI contends with strong rivals like LG Chem and CATL. LG Chem's 2022 revenue hit roughly $22.5 billion, while CATL's reached around $23.3 billion in the same year, intensifying the rivalry.

Technological Advancements

Rapid technological advancements fuel innovation and differentiation, intensifying competitive pressures within the battery market. Samsung SDI, recognizing this, significantly invests in research and development to maintain its competitive advantage. For instance, Samsung SDI aims for a 30% increase in battery energy density by 2025. Global spending on battery research is projected to hit approximately $12 billion by 2025, indicating substantial investment across the industry.

Price Wars

Price wars are common among battery manufacturers, which puts pressure on profits. This price competition can significantly decrease profit margins. For example, the average selling price of lithium-ion batteries dropped by approximately 20% from 2020 to 2022. Samsung SDI's operating profit margin fell to about 5.2% in 2022, reflecting this intense rivalry.

Market Share Decline

Samsung SDI faces intensified competition. The market share of the top three Korean battery companies, including Samsung SDI, decreased in the global EV battery market. This decline signals a more competitive landscape. The combined market share of these firms fell to 45.6% in 2024, a 2.7 percentage point drop from the prior year.

- Competitive pressure from rivals is increasing.

- Market share erosion is a key concern.

- The industry is becoming more concentrated.

- The decrease in market share is 2.7 percentage points.

Product Differentiation

Samsung SDI must relentlessly enhance its offerings to stay competitive. Differentiation is key for Samsung SDI. To thrive, it must invest in R&D and quality. The company needs to adjust to market changes. In 2024, the global battery market is valued at approximately $150 billion, with projections of significant growth.

- Continuous innovation in battery technology.

- Focus on premium product features and performance.

- Adapt to rapid shifts in electric vehicle demands.

- Strategic partnerships for market expansion.

Battery Market Battles: Intense Competition!

Competitive rivalry is intense in the material and energy solutions sector. Samsung SDI competes with formidable rivals such as LG Chem and CATL. Price wars and market share shifts are constant challenges. The top Korean battery firms' market share dropped to 45.6% in 2024.

| Aspect | Details |

|---|---|

| Market Share Drop (2024) | Korean battery firms saw a 2.7% drop. |

| Battery Market Value (2024) | Approximately $150 billion. |

| Samsung SDI's Margin (2022) | Operating profit margin was about 5.2%. |

SSubstitutes Threaten

Availability of Alternatives

The threat of substitutes for Samsung SDI is moderate because numerous alternatives exist. The company competes in saturated markets, where each product faces viable substitutes. For example, in 2024, Samsung SDI's battery division faced competition from CATL and LG Energy Solution. These competitors offer similar products. This market saturation increases the risk.

Low Switching Costs

The low cost of switching to alternative products strengthens the bargaining power of buyers, amplifying the threat of substitutes. This easy switchability increases the risk for Samsung SDI Co. For example, the rise of alternative battery technologies like solid-state batteries, could challenge Samsung SDI's market position. The global battery market was valued at $145.1 billion in 2023, and is projected to reach $296.5 billion by 2030.

Diverse Product Portfolio

Samsung SDI's diverse product portfolio somewhat lessens the threat of substitutes. This approach allows the company to target various market segments effectively. The threat of substitutes is considered a moderate force for Samsung SDI. In 2024, Samsung SDI's revenue was approximately $16.7 billion, showing the scale of its diversified offerings.

Alternative Battery Technologies

Alternative battery technologies present a notable threat. Innovations like solid-state and LFP batteries could outperform or undercut traditional lithium-ion options. The rise of LFP batteries significantly impacts Korean manufacturers. This shift is due to their cost-effectiveness and performance improvements. In 2024, LFP batteries gained market share, affecting Samsung SDI's position.

- Solid-state batteries offer enhanced safety and energy density.

- LFP batteries are more affordable and durable.

- Korean battery makers face challenges from LFP's growth.

- The LFP market share increased in 2024, influencing Samsung SDI.

Energy Storage Alternatives

Samsung SDI faces the threat of substitutes in the energy storage market. Alternatives like pumped hydro and compressed air storage can compete with its battery energy storage systems. These alternatives might be better for some uses. In 2024, compressed air storage led the advanced energy storage market. Compressed air offers a straightforward energy storage method.

- Pumped hydro storage accounted for about 95% of the global energy storage capacity in 2024.

- The global compressed air energy storage market was valued at approximately $1.2 billion in 2024.

- Lithium-ion batteries, a key product for Samsung SDI, face competition from various technologies.

- These alternatives may be more suitable for certain applications.

Samsung SDI: Substitute Threats Loom

The threat of substitutes for Samsung SDI is moderate, with various alternatives available. The low switching costs to these alternatives amplify the risk for the company. Emerging technologies like solid-state and LFP batteries challenge Samsung SDI's market position.

| Substitutes | Impact on Samsung SDI | 2024 Data |

|---|---|---|

| Solid-state batteries | Potential market shift | Significant advancements in safety & density |

| LFP Batteries | Increased competition | Market share growth, affecting Korean makers |

| Energy Storage Alternatives | Competition in ESS | Pumped hydro dominated, compressed air growing |

Entrants Threaten

High Capital Investment

Samsung SDI faces the threat of new entrants, particularly due to high capital investment needs. The consumer electronics sector demands substantial financial resources for infrastructure and research. New companies struggle to compete because the industry requires constant innovation and is highly competitive. For instance, in 2024, R&D spending in the tech sector reached $800 billion globally, showcasing the capital intensity. This makes it difficult for new companies to enter and sustain themselves.

Technological Expertise

Advanced technological expertise is crucial in battery manufacturing. Samsung SDI invests heavily in R&D, spending KRW 1.1 trillion in 2023. New entrants often lack the required expertise in materials science and engineering. The complexity of battery technology presents a significant barrier to entry.

Established Brand Loyalty

Established brand loyalty and trust pose a significant barrier for new competitors. Samsung SDI benefits from strong brand recognition. Samsung's brand value was about $62.4 billion in 2023. This customer loyalty hampers rapid market share gains for new entrants.

Economies of Scale

Samsung SDI benefits from significant economies of scale, a crucial advantage in the battery market. New entrants struggle to match the cost efficiencies of established players like Samsung. This cost advantage acts as a barrier, making it tough for new companies to compete on price. For example, in 2024, Samsung SDI's battery division reported a gross margin of approximately 15%, reflecting these scale benefits.

- Lower production costs.

- Established supply chain.

- Strong brand recognition.

- High capital expenditure.

Supply Chain Logistics

New entrants in the battery market face significant hurdles due to supply chain logistics. Building extensive networks for sourcing materials and distributing products presents a considerable barrier. Established companies like Samsung SDI already have well-defined relationships with suppliers and distribution channels. Replicating these networks requires substantial time and investment, making it difficult for newcomers to compete effectively.

- Supply chain complexity deters new entrants.

- Samsung SDI supplied around 40 GWh of battery cells in 2022.

- New entrants need to establish similar scale.

- Logistics networks take years and money to build.

Samsung SDI: Entry Barriers Examined

The threat of new entrants for Samsung SDI is moderate due to high capital costs, technological complexity, and established brand loyalty. Samsung SDI invested heavily in R&D, spending KRW 1.1 trillion in 2023, which is a major barrier. New entrants also struggle to match existing economies of scale.

| Barrier | Description | Impact on New Entrants |

|---|---|---|

| Capital Investment | High costs for infrastructure and R&D | Limits entry, requires significant funding |

| Technology | Advanced tech in battery manufacturing | Difficult to replicate, requires expertise |

| Brand Loyalty | Established brand recognition and trust | Challenges market share gain |

Porter's Five Forces Analysis Data Sources

The analysis utilizes Samsung SDI's annual reports, industry studies, and market research. It also incorporates insights from competitor filings.