Standard Chartered Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Standard Chartered Bundle

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Standard Chartered.

Customize pressure levels for fluctuating interest rates & global markets.

Preview Before You Purchase

Standard Chartered Porter's Five Forces Analysis

This is the full Standard Chartered Porter's Five Forces Analysis. The preview reveals the complete, professionally written document you'll receive. It details each force impacting Standard Chartered, offering insights and strategic considerations. There are no differences between this preview and the file ready for immediate download after purchase. This detailed analysis will be yours instantly.

Porter's Five Forces Analysis Template

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

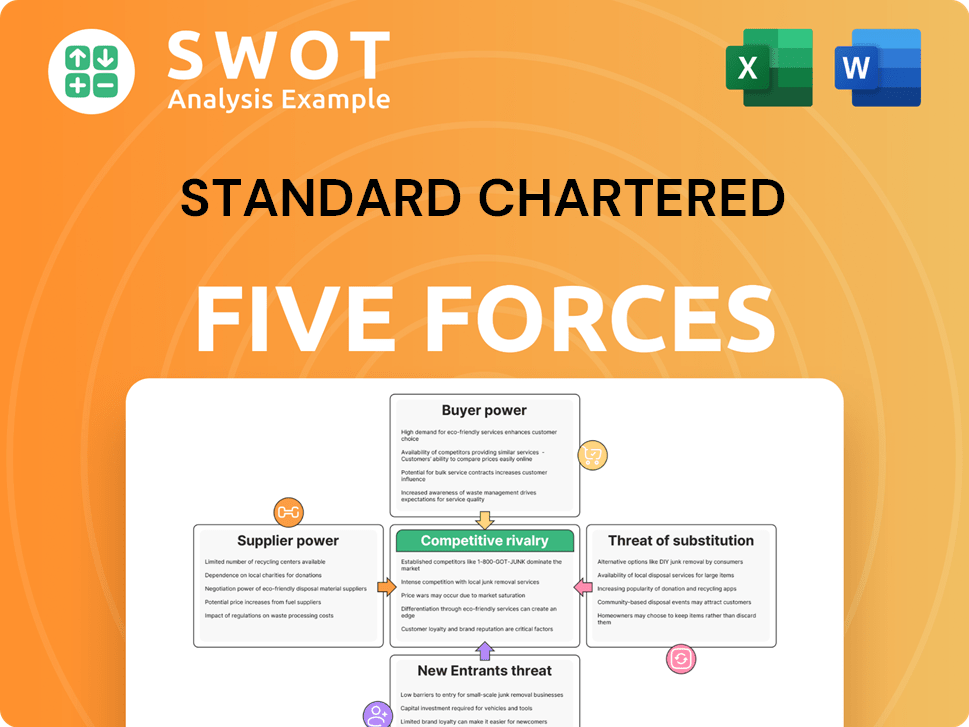

Analyzing Standard Chartered through Porter's Five Forces reveals intense competition, especially from established banking giants. The threat of new entrants is moderate, given high capital requirements. Bargaining power of both buyers and suppliers is relatively balanced, with diverse customer and supplier bases. Substitute products, such as fintech solutions, pose a growing but manageable threat. This initial look only highlights major aspects of the industry.

Ready to move beyond the basics? Get a full strategic breakdown of Standard Chartered’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Concentration of Financial Data Providers

Financial data providers, critical to Standard Chartered, are consolidating, potentially boosting their bargaining power. This concentration, with companies like S&P Global and Bloomberg dominating, limits Standard Chartered's choices. In 2024, these firms controlled a significant share of the market, impacting pricing. Diversifying data sources and in-house development are key for mitigating risks.

Specialized Technology Vendors

Standard Chartered's reliance on specialized tech vendors for core banking systems and AI solutions is rising. In 2024, global IT spending in the banking sector reached approximately $600 billion. This dependence increases these vendors' bargaining power. To mitigate this, Standard Chartered needs robust vendor management and strategic contract negotiations. Exploring open-source solutions is also crucial for reducing supplier influence.

Consulting Services for Regulatory Compliance

Standard Chartered relies heavily on consulting services for regulatory compliance, especially for AML and data privacy. The specialized knowledge of consulting firms in these areas gives them significant bargaining power. In 2024, the global compliance consulting market was valued at approximately $70 billion, reflecting the high demand and influence of these firms. To mitigate this, Standard Chartered should build internal expertise and standardize processes.

Impact of Legacy System Dependence

Standard Chartered, like many banks, grapples with legacy systems. These older systems require specialized support, which boosts the bargaining power of suppliers. High maintenance costs and dependency on specific vendors are significant challenges. Modernizing core infrastructure is vital to reduce reliance and enhance negotiating leverage.

- Standard Chartered's IT spending in 2023 was approximately $1.5 billion.

- Globally, the market for legacy system modernization is projected to reach $20 billion by 2024.

- Banks spend an average of 60% of their IT budget on maintaining legacy systems.

- Modernization can reduce operational costs by up to 30%.

Cybersecurity Solution Providers

Cybersecurity solution providers possess significant bargaining power due to the increasing frequency and sophistication of cyber threats. Standard Chartered, like all major banks, is highly reliant on these providers for protection. The bank's dependence is amplified by the escalating costs of cyberattacks, which, according to IBM, averaged $4.45 million per incident globally in 2023. To counter this, Standard Chartered should implement strong cybersecurity frameworks and regularly assess risks.

- The global cybersecurity market is projected to reach $345.7 billion by 2027.

- Ransomware attacks increased by 13% in 2023.

- Data breaches cost an average of $15.2 million in the financial sector in 2023.

- Diversifying cybersecurity vendors helps mitigate supplier power.

Supplier Power Dynamics at a Global Bank

Standard Chartered faces supplier power challenges from financial data providers, tech vendors, and consulting firms. Consolidation in financial data, like S&P Global and Bloomberg dominating, impacts pricing. Dependence on tech vendors for core systems and consultants for compliance amplifies supplier leverage.

| Supplier Type | Impact on Standard Chartered | Mitigation Strategies |

|---|---|---|

| Financial Data Providers | Concentration & Price Influence | Diversify sources, in-house development |

| Tech Vendors | Dependence on Core Systems | Vendor management, contract negotiations, open-source solutions |

| Consulting Firms | Specialized Knowledge & Demand | Build internal expertise, standardize processes |

Customers Bargaining Power

Increased Customer Expectations for Digital Services

Customers now expect top-notch digital services, boosting their bargaining power. To stay competitive, Standard Chartered must invest in technology. In 2024, digital banking users grew, emphasizing the need for user-friendly interfaces and mobile banking. Banks must offer personalized service; research shows 75% of customers prefer tailored experiences.

Low Switching Costs due to Digital Banking

Digital banking has lowered switching costs, making it easier for customers to switch banks. This intensifies the pressure on Standard Chartered to offer competitive services. Banks must build customer loyalty through rewards and personalized offers. Customer churn rates in the banking sector averaged 10-15% in 2024.

Demand for Competitive Interest Rates and Fees

Customers' sensitivity to interest rates and fees is high, enabling easy comparison across banks. Standard Chartered faces pressure to offer competitive pricing to attract and retain clients. In 2024, banks like Standard Chartered compete by regularly benchmarking rates. This is crucial, as even small fee differences can drive customer decisions. Competitive pressure is intense; for example, in 2024, average savings account rates varied considerably across institutions.

Greater Transparency and Access to Information

Customers now wield significant power due to unprecedented access to information, enabling them to make well-informed choices and demand better value from financial institutions like Standard Chartered. This shift necessitates greater transparency in pricing, terms, and conditions. Banks must clearly communicate product details and empower customers with tools for effective financial management. For instance, in 2024, digital banking adoption rates surged, with over 70% of consumers using online or mobile banking platforms.

- Transparency in fees and charges is crucial, as highlighted by the Consumer Financial Protection Bureau's (CFPB) focus on preventing hidden fees in 2024.

- Clear communication about interest rates and loan terms is essential.

- Providing educational resources and financial planning tools can help customers make informed decisions.

- Digital banking platforms are key in providing access to real-time financial data.

Rise of Fintech and Alternative Financial Providers

The rise of Fintech companies and alternative financial providers is reshaping the banking industry. These entities offer innovative products, heightening customer choice and bargaining power. Standard Chartered faces pressure to adapt to this shift by innovating or partnering with Fintechs. The bank must embrace open banking to stay competitive.

- Fintech funding in 2024 reached $48 billion, signaling strong customer interest.

- Open banking adoption grew by 30% in 2024, expanding customer choice.

- Alternative lenders increased market share by 15% in 2024, boosting competition.

Digital Banking Drives Customer Power

Customers' bargaining power is amplified by digital tools and Fintechs, as digital banking adoption grew in 2024. This forces Standard Chartered to prioritize competitive pricing, transparency, and user-friendly services. Failure to adapt to customer demands could result in significant customer churn.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Digital Banking Adoption | Increased customer choice | 70% of consumers use online banking |

| Customer Churn | Higher with easier switching | 10-15% average in banking |

| Fintech Funding | Increased competition | $48 billion invested in Fintech |

Rivalry Among Competitors

Intense Competition from Global Banks

Standard Chartered contends with fierce rivalry from global banks across Asia, Africa, and the Middle East. Competitors offer similar services, fueling price wars, and squeezing profit margins. In 2024, Standard Chartered's net interest margin faced pressure. To thrive, the bank must differentiate itself. This can be achieved through superior service and innovative products.

Growing Presence of Regional Banks

Regional banks are becoming more competitive, expanding their services, and intensifying rivalry. They understand local markets better, giving them an edge. In 2024, regional banks saw a 7% increase in market share in some areas. To compete, banks must offer tailored products and build strong community ties. This strategic focus is crucial for survival.

Rise of Digital-Only Banks and Neobanks

Digital-only banks and neobanks are intensifying competitive rivalry by challenging traditional banks. These digital platforms offer low-cost, tech-forward services, drawing in customers seeking convenience. In 2024, neobanks saw a 15% increase in user adoption, highlighting their growing influence. To stay competitive, banks must embrace digital transformation, offering innovative mobile solutions and personalized customer experiences.

Increased Focus on Wealth Management

The wealth management sector is heating up, making it a tough arena for Standard Chartered. They're up against seasoned wealth managers and tech-savvy fintech firms. To stay competitive, Standard Chartered needs to offer top-notch financial advice and a wide array of investment choices. This includes leveraging tech for a better client experience.

- Global wealth management assets are projected to reach $140 trillion by 2025.

- Fintech investments in wealth management hit $1.2 billion in 2024.

- Competition is fierce, with over 20,000 wealth management firms globally.

- Personalized advice and tech integration drive client loyalty.

Impact of Consolidation in the Banking Industry

Consolidation in banking intensifies competition, creating giants with more clout. Mergers lead to economies of scale and broader market presence. This boosts their ability to pressure rivals. Banks must assess M&A prospects, focusing on effective integration for synergy and competitiveness.

- In 2024, the total value of M&A deals in the global banking sector reached $500 billion.

- Large banks like JPMorgan Chase and Bank of America control over 20% of U.S. banking assets.

- Post-merger integration failures can lead to a 10-15% decline in shareholder value within the first year.

- The top 10 global banks increased their combined assets by 8% in 2024 due to M&A activity.

Standard Chartered: Navigating Market Challenges

Standard Chartered faces intense rivalry across its global markets. Competitors, offering similar services, drive price wars and margin compression. The bank must differentiate through superior service and product innovation to stay ahead. Digital transformation is vital to compete effectively.

| Metric | 2024 Data | Impact |

|---|---|---|

| Net Interest Margin Pressure | 2.3% (Average) | Reduced profitability |

| Neobank User Growth | 15% Increase | Increased competition |

| M&A Deal Value | $500B (Global Banking) | Increased consolidation |

SSubstitutes Threaten

Rise of Fintech Payment Solutions

Fintech payment solutions, like mobile wallets and P2P apps, pose a significant threat. These alternatives often offer lower fees and quicker transactions compared to traditional banking. In 2024, the global fintech market is valued at approximately $150 billion, showing strong growth. Standard Chartered must integrate with fintech or develop its own platforms. Banks risk losing market share if they fail to adapt to these convenient alternatives.

Growing Popularity of Cryptocurrency and Blockchain

Cryptocurrencies and blockchain are emerging substitutes for traditional banking. They offer alternative payment and transaction methods, potentially disrupting the current financial system. While regulations evolve, cryptocurrencies present a long-term threat to traditional banking services. Banks must explore blockchain and digital currencies, closely monitoring the regulatory landscape. In 2024, the global cryptocurrency market was valued at approximately $1.07 trillion, highlighting its growing influence.

Peer-to-Peer Lending Platforms

Peer-to-peer (P2P) lending platforms pose a threat by connecting borrowers and lenders directly, sidestepping banks. These platforms frequently offer more attractive interest rates and flexible terms. In 2024, the P2P lending market was valued at approximately $150 billion globally. To compete, banks like Standard Chartered should consider developing their own P2P platforms or partnering with existing ones.

Non-Bank Financial Institutions Offering Banking Services

The rise of non-bank financial institutions (NBFIs) poses a threat to Standard Chartered. Companies like Amazon and Apple are expanding into financial services, offering credit cards and loans. These firms leverage existing customer relationships and brand trust, creating competitive pressure. Standard Chartered must adapt to this shift to stay relevant.

- NBFI credit card spending in the US reached $1.2 trillion in 2024.

- Apple's entry into financial services has increased competition in digital payments.

- Strategic partnerships or new distribution channels are vital for banks.

Increased Use of Prepaid Cards

The rise of prepaid cards poses a threat to traditional banking services. These cards provide a substitute for checking accounts, offering convenience for various transactions. Increased adoption, especially among the unbanked, directly impacts traditional banks. In 2024, the global prepaid card market was valued at approximately $2.5 trillion.

- Market Growth: The prepaid card market is projected to reach $3.8 trillion by 2028.

- User Base: Over 15% of U.S. adults utilize prepaid cards regularly.

- Usage: Prepaid cards are increasingly used for online shopping and bill payments.

- Impact: Banks must adapt by offering their own prepaid card solutions.

Fintech & Crypto: Banking's New Rivals

Fintech's growth, valued at $150B in 2024, offers faster, cheaper alternatives. Cryptocurrencies, worth $1.07T in 2024, present long-term disruption to banking. P2P lending and NBFIs also threaten, requiring banks to adapt.

| Substitute | Description | 2024 Data |

|---|---|---|

| Fintech | Mobile wallets, P2P apps offer lower fees | $150B Market |

| Cryptocurrencies | Alternative payment methods | $1.07T Market |

| P2P Lending | Direct borrower-lender connections | $150B Market |

Entrants Threaten

High Regulatory Barriers to Entry

High regulatory hurdles significantly impact the banking sector. New banks face stringent licensing, capital needs, and operational rules. These requirements, like the Basel III framework, increase entry costs. In 2024, compliance spending for banks rose by approximately 7%. Banks should push for stable regulations that foster innovation and protect consumers.

Significant Capital Requirements

Starting a bank demands substantial capital, deterring new competitors. This capital is crucial for loans, reserves, and tech investments. For instance, in 2024, new bank formations faced regulatory hurdles increasing capital needs. Established banks like Standard Chartered, with $1.4 trillion in assets in 2023, have a significant advantage. Banks must maintain robust capital positions and use tech to cut costs.

Brand Recognition and Customer Trust

Established banks, like Standard Chartered, benefit from strong brand recognition and customer trust. New entrants struggle to replicate this, as customers hesitate to trust their finances with unproven institutions. In 2024, Standard Chartered's brand value remained high, reflecting its global presence and established customer base. Banks should prioritize brand reputation and customer service.

Economies of Scale

Established banks, like Standard Chartered, hold a significant advantage due to economies of scale, enabling competitive pricing and extensive service portfolios. New entrants struggle to match this, facing higher per-unit costs and limited service ranges. To counter this, Standard Chartered and similar institutions must streamline operations and embrace technology. They should also broaden their service offerings to maintain a strong market position.

- Standard Chartered's operating expenses were approximately $10.8 billion in 2023.

- Digital banking platforms are crucial for reducing operational costs by up to 60%.

- Expanding services to include wealth management and fintech partnerships is key.

Technological Disruption by Fintechs

Fintech companies pose a significant threat, using technology to challenge traditional banking. Despite high capital and regulatory barriers, they offer specialized services like online lending and mobile payments. This disruption pressures banks to innovate. Banks must digitally transform, partner with fintechs, and develop new solutions to stay competitive.

- Global fintech investments reached $51.2 billion in the first half of 2024.

- Mobile payments are expected to grow to $14 trillion by 2025.

- Challenger banks have increased their market share by 5% in the past year.

- Partnerships between banks and fintechs have grown by 30% in 2024.

Standard Chartered: Navigating Entry Barriers

The threat from new entrants to Standard Chartered is moderate. High barriers to entry include stringent regulations, capital demands, and the need for brand recognition. Fintechs and challenger banks are disrupting the market with digital solutions and specialized services.

| Factor | Impact | Data (2024) |

|---|---|---|

| Regulations | High Compliance Costs | Compliance spending up 7% |

| Capital Needs | Significant Investment | New bank formations faced hurdles |

| Brand Recognition | Customer Trust | Standard Chartered's value high |

Porter's Five Forces Analysis Data Sources

We synthesize data from Standard Chartered's annual reports, financial news, and industry analysis reports.