State Farm Bundle

How did a farmer's vision revolutionize the insurance industry?

State Farm, a household name, boasts a fascinating history that began with a simple yet revolutionary idea. Founded in 1922, this insurance giant emerged from a commitment to fairness and affordability, specifically targeting a segment often overlooked. Learn how State Farm SWOT Analysis can help you understand the company's strategic position today.

From its roots as an auto insurer for farmers, the State Farm company has experienced remarkable growth, evolving into a comprehensive financial services provider. Understanding the State Farm history reveals the company's adaptability and its unwavering focus on customer needs. Exploring the State Farm background and timeline unveils key milestones that shaped its journey to become a leader in the insurance industry.

What is the State Farm Founding Story?

The State Farm history begins on June 7, 1922. Founded by George Jacob Mecherle in Bloomington, Illinois, the company initially focused on providing auto insurance to farmers. This marked the start of an insurance provider designed to offer tailored rates.

Mecherle, a former farmer and insurance salesman, saw that farmers paid the same high auto insurance premiums as city drivers. His solution was to create a mutual insurance company. This company would be owned by its policyholders, offering lower rates to reflect the lower risk profile of farmers. This approach set the stage for State Farm's customer-focused strategy.

The company's early years were defined by its commitment to fairness and affordability. Mecherle's door-to-door sales approach helped to build a customer base. The company's original name, State Farm Mutual Automobile Insurance Company, reflected its initial focus on auto insurance for farmers in Illinois.

Key Aspects of State Farm's Founding

State Farm's founding was driven by a need for fairer insurance rates. Mecherle's vision was to create a company that understood and served the specific needs of farmers.

- State Farm founder George Jacob Mecherle identified a gap in the market.

- The initial focus was on providing auto insurance to farmers in Illinois.

- The business model was built on the principle of offering lower rates based on risk.

- Mecherle's determination led him to leave an existing company to start his own venture.

The economic context of the early 20th century, with the growing popularity of automobiles, influenced State Farm's establishment. The company's early success was a result of its focus on a specific market segment. This approach allowed State Farm to establish a strong foundation.

For more details on the company's business model and revenue streams, you can explore the Revenue Streams & Business Model of State Farm.

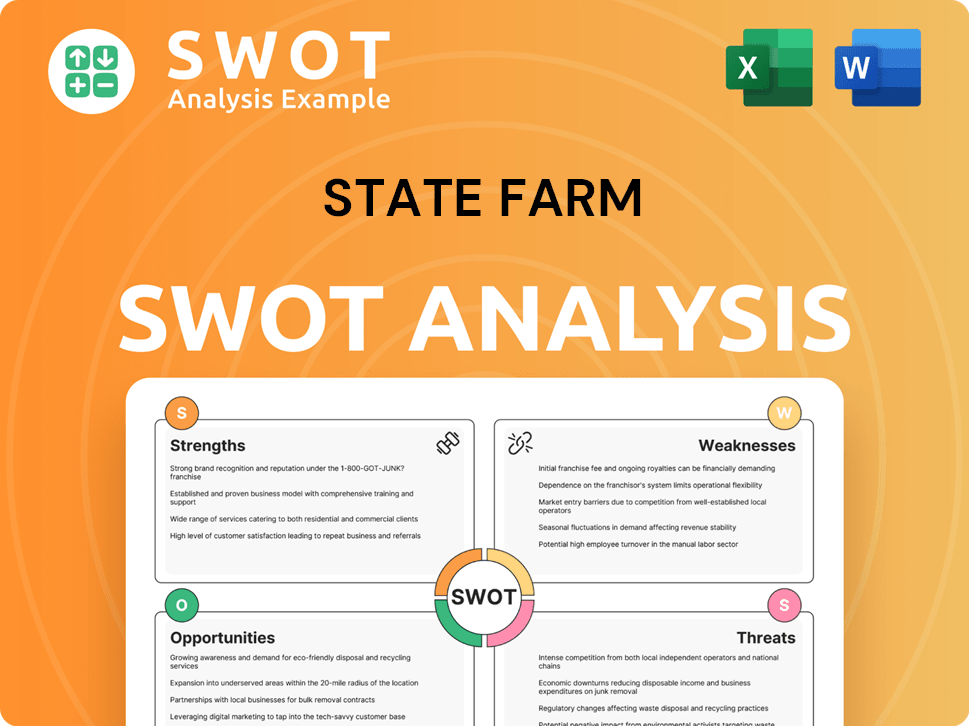

State Farm SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of State Farm?

The early growth of the company, a key part of the Marketing Strategy of State Farm, involved significant expansion beyond its initial focus. This period saw the company broaden its customer base and geographic reach, alongside strategic diversification into new product lines. These moves were crucial in establishing the company as a leading insurer, marking the start of its long-term success.

In 1928, the company began offering policies to non-farmers, extending its reach to towns and cities. This expansion significantly increased its customer base. The same year, the company's income exceeded $1 million, and it opened its first branch office in Berkeley, California.

A key development in 1929 was the completion of the Home Office Building in Downtown Bloomington, centralizing operations. This was followed by the formation of the Life Insurance Company in January 1929, marking the company's entry into life insurance. The founder, G.J. Mecherle, purchased the first life policy.

The company continued to diversify, establishing the Fire Company in 1935, which sold Homeowner's Insurance. By 1942, the company had become the number one auto insurance company in the United States. Despite challenges like World War II, the company maintained a strong policyholder base, reaching one million auto insurance policies by March 1944.

Leadership transitions included George Mecherle becoming chairman of the board in 1937 and Raymond Mecherle being elected president. In 1947, the company expanded its geographical footprint by opening regional offices across the United States and Canada. These offices included localized mail operations for more efficient customer service.

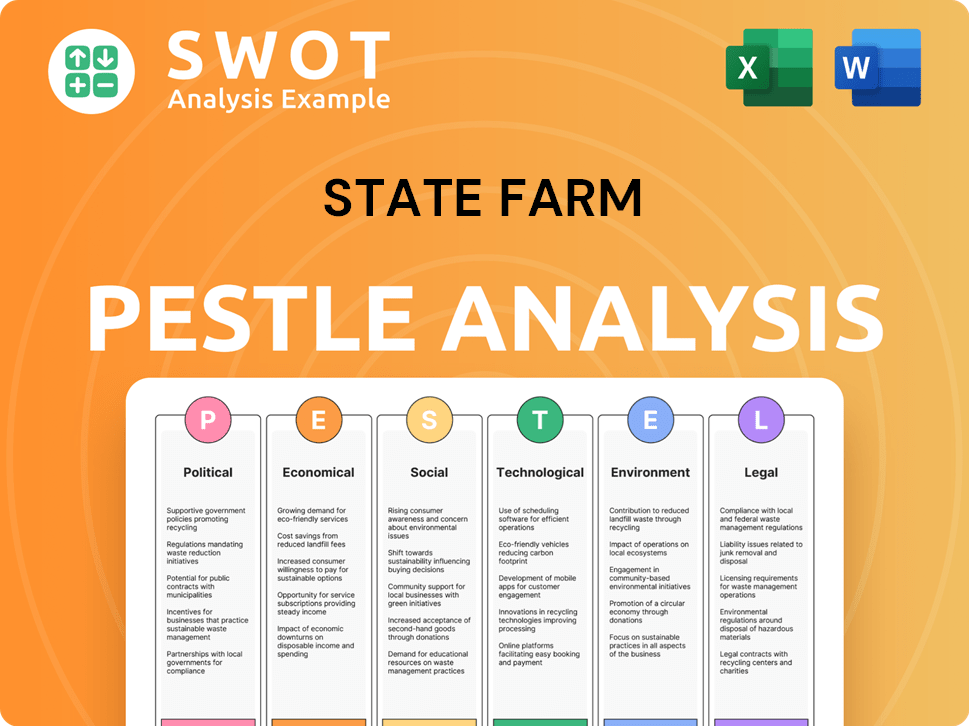

State Farm PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in State Farm history?

The history of the State Farm company is marked by significant milestones, starting with its innovative approach to insurance. From its early years, the company has consistently adapted and expanded, shaping its position in the insurance industry.

| Year | Milestone |

|---|---|

| 1922 | State Farm founder, George J. Mecherle, established the company, focusing on auto insurance for farmers. |

| 1929 | State Farm Life Insurance Company was launched, broadening the company's offerings. |

| 1935 | State Farm Fire and Casualty Company was established, extending coverage to homeowners insurance. |

| 1942 | State Farm became the number one auto insurance company in the U.S., a major achievement. |

| 1966 | An advanced computer system was installed, enhancing operational efficiency. |

| 1971 | A $30 million refund was issued to policyholders, demonstrating the company's mutual structure. |

| 2022 | A strategic collaboration and a $1.2 billion equity investment in ADT Inc. was made, focusing on smart home ecosystems. |

| 2023 | Secured a patent for an IoT-driven claims process to enhance efficiency and insights. |

| 2024 | The company reported a net income of $5.3 billion, reflecting a rebound from previous losses. |

State Farm insurance has consistently embraced technological advancements to improve its services. This includes the development of telematics-based auto insurance through HiRoad and the use of advanced risk prediction solutions via Quanata.

Telematics-Based Insurance

HiRoad, a telematics-based insurance program, rewards good driving behavior. This innovation helps in personalizing insurance rates based on driving habits.

Advanced Risk Prediction

Quanata is being developed to provide advanced risk prediction solutions. This aims to enhance the accuracy of risk assessments and improve customer service.

IoT-Driven Claims Process

A patent for an IoT-driven claims process was secured in spring 2023. This innovation is designed to streamline claims handling and provide deeper insights for claims handlers.

Smart Home Ecosystems

A strategic collaboration and a $1.2 billion equity investment in ADT Inc. in September 2022, alongside a $300 million opportunity fund, focusing on smart home ecosystems. This initiative aims to integrate experiences and proactively predict and prevent losses.

Despite its successes, State Farm's history includes periods of significant challenges. The company has faced underwriting losses due to natural disasters and, more recently, in its auto and homeowners insurance segments.

Underwriting Losses

The company reported a net loss of $6.3 billion in 2023, although it rebounded to a net income of $5.3 billion in 2024. Underwriting losses in the auto and homeowners insurance segments continue to be a challenge.

Auto Insurance Challenges

The auto insurance business, representing 65% of its property-casualty net written premium, saw its underwriting loss decrease to $2.7 billion in 2024 from $9.7 billion in 2023. This segment still faces challenges related to claims and rising costs.

Homeowners Insurance Challenges

The homeowners line faces significant financial impacts from wildfires, particularly in California. State Farm General faces an estimated $7.9 billion in direct losses and loss adjustment expenses related to wildfires.

Strategic Adjustments

State Farm has made strategic decisions, such as exiting LYNX Services for auto glass claims administration, transitioning to Safelite Solutions starting July 1, 2025. These moves reflect the company's efforts to adapt and improve its service offerings.

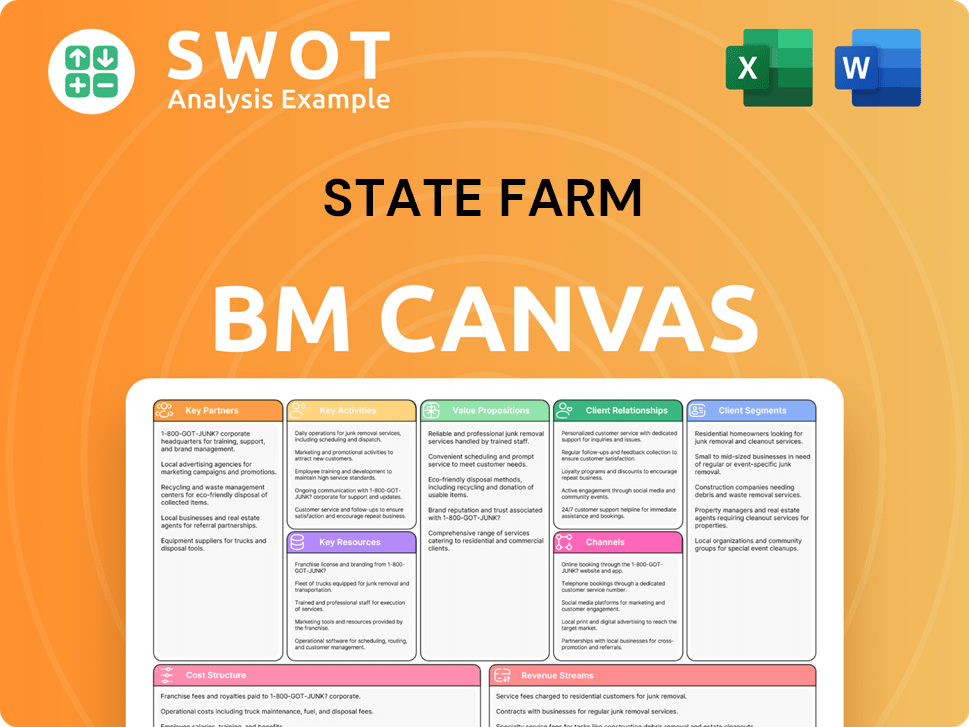

State Farm Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for State Farm?

The State Farm history is a story of growth and adaptation, starting with its foundation in 1922 and evolving into a major player in the insurance and financial services industries. The company's journey, marked by strategic expansions and innovations, reflects its commitment to serving its customers and adapting to market changes. From its early focus on auto insurance to its diversification into life, fire, and health insurance, State Farm has consistently broadened its offerings to meet the evolving needs of its customers. The company's financial performance, including recent gains and strategic investments, underscores its enduring strength and forward-looking approach.

| Year | Key Event |

|---|---|

| June 7, 1922 | State Farm Mutual Automobile Insurance Company was founded in Bloomington, Illinois, by George J. Mecherle, initially providing low-cost auto insurance to farmers. |

| 1928 | The company's income exceeded $1 million, and it began writing policies for non-farmers, expanding its customer base. |

| 1929 | State Farm Life Insurance Company was formed, marking the company's diversification into life insurance. |

| 1935 | State Farm Fire Insurance Company was launched, entering the property insurance market. |

| 1942 | State Farm became the number one auto insurance company in the United States. |

| 1944 | The company reached one million auto insurance policies in effect. |

| 1947 | Regional offices were opened across the United States and Canada, expanding geographical reach. |

| 1961 | State Farm Life and Accident Assurance Company was incorporated to serve additional states, including New York, Connecticut, and Wisconsin. |

| 1965 | State Farm entered the health insurance business. |

| 1966 | An advanced computer system was installed, linking regional offices to headquarters, improving operational efficiency. |

| 1971 | State Farm issued a $30 million refund to policyholders due to high earnings. |

| 2022 | State Farm celebrated its 100th anniversary. |

| September 2022 | State Farm made a $1.2 billion equity investment in ADT Inc. and created a $300 million opportunity fund, signaling a strategic focus on smart home ecosystems. |

| 2023 | State Farm reported a net loss of $6.3 billion. |

| 2024 | State Farm reported a net income of $5.3 billion, a significant turnaround from the previous year. The company's earned premium for property and casualty companies rose to $103 billion from $87.6 billion in 2023. |

| 2025 | State Farm leads the U.S. auto insurance market for the third consecutive year, with approximately $68 billion in direct premiums written and an 18.9% market share. The company is transitioning its auto glass claims administration from LYNX Services to Safelite Solutions starting July 1, 2025. |

State Farm is focused on maintaining its leadership in the insurance industry and expanding into financial services. It aims to be the customer's top choice for products and services. This includes investing in digital capabilities and innovation in areas like mobility, residential solutions, and artificial intelligence.

The insurance landscape in 2025 is highly competitive. Favorable underwriting results may lead to increased competition and slower premium growth. State Farm will continue its state-specific approach, emphasizing the financial strength of each affiliate. The company is also researching quantum computing.

State Farm is actively researching quantum computing to enhance its capabilities. The company is focused on innovation, particularly in areas like mobility and transportation, residential solutions (including smart home technology), and artificial intelligence to streamline operations and improve customer service.

In 2024, State Farm reported a net income of $5.3 billion, a significant improvement from a net loss of $6.3 billion in 2023. The earned premium for property and casualty companies rose to $103 billion from $87.6 billion in 2023. In 2025, it leads the U.S. auto insurance market with approximately $68 billion in direct premiums written and an 18.9% market share.

State Farm Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of State Farm Company?

- What is Growth Strategy and Future Prospects of State Farm Company?

- How Does State Farm Company Work?

- What is Sales and Marketing Strategy of State Farm Company?

- What is Brief History of State Farm Company?

- Who Owns State Farm Company?

- What is Customer Demographics and Target Market of State Farm Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.