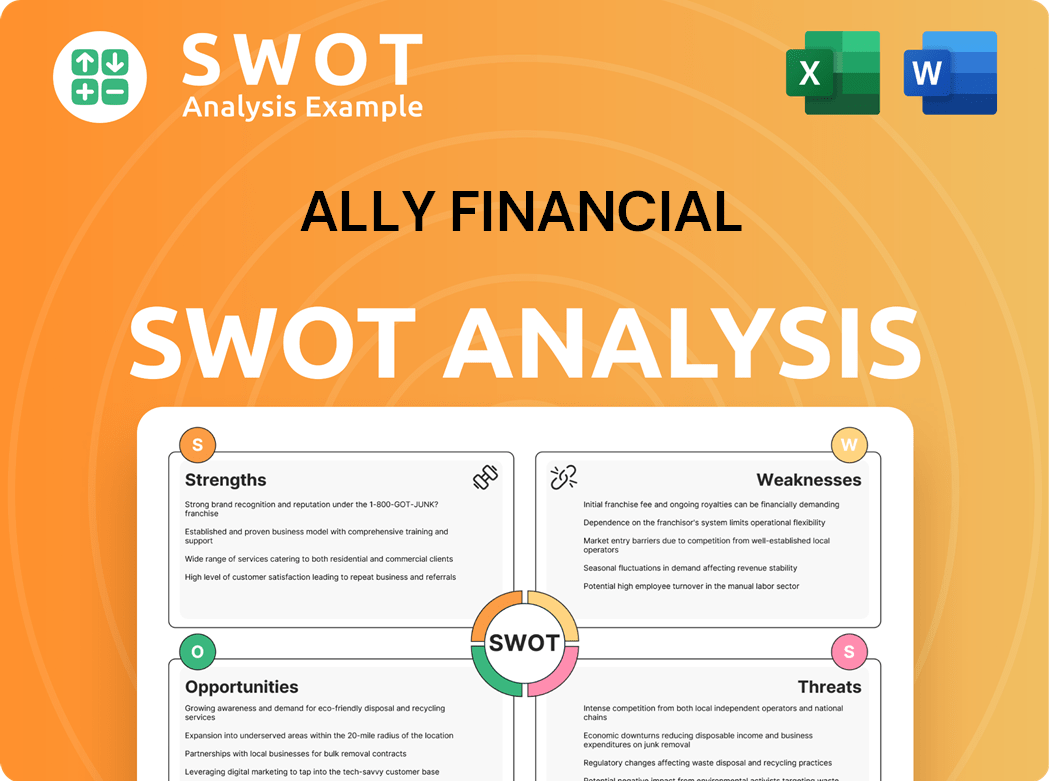

Ally Financial SWOT Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Ally Financial Bundle

What is included in the product

Provides a clear SWOT framework for analyzing Ally Financial’s business strategy.

Facilitates interactive planning with a structured, at-a-glance view.

What You See Is What You Get

Ally Financial SWOT Analysis

See exactly what you'll get! The SWOT analysis previewed here mirrors the complete, comprehensive report you’ll receive instantly after purchase.

SWOT Analysis Template

Elevate Your Analysis with the Complete SWOT Report

Ally Financial shows strength in its digital presence and diverse product offerings. Its weaknesses include reliance on the auto loan market and interest rate sensitivity. Opportunities lie in expanding its banking services and strategic partnerships, yet threats like competition and economic downturns persist. To grasp a complete understanding, don't miss the comprehensive SWOT analysis.

Gain full access to a research-backed, editable breakdown of the company’s position—ideal for strategic planning and market comparison.

Strengths

Strong Digital Presence

Ally Financial's strong digital presence is a key strength, as it operates primarily as a digital bank. This allows Ally to offer competitive rates and lower fees. Enhanced online and mobile banking capabilities drive high customer satisfaction. In Q3 2024, Ally reported an 89% customer satisfaction rate. Their customer retention rate was 95%.

Leading Auto Finance Business

Ally Financial excels in auto finance, with a robust dealer network exceeding 22,000. In 2024, the company's new auto loans yield averaged 10.4%. Its strong credit underwriting supports loan performance. Application volumes saw a 6% increase YoY.

Diversified Financial Products

Ally Financial's strength lies in its diversified financial product offerings, including auto loans, savings accounts, and investment services. This strategy allows Ally to serve a broad customer base. The insurance segment has performed well, with the highest quarter of earned premiums since its IPO in Q4 2024. This diversification helps mitigate risks.

Solid Capital Position

Ally Financial's strong financial standing is a key advantage. Being a digital bank allows Ally to offer competitive rates and lower fees, boosting customer satisfaction. In Q3 2024, Ally's digital banking services boasted an 89% customer satisfaction rate. The customer retention rate reached an impressive 95%.

- Competitive Rates: Offers attractive interest rates on savings accounts and competitive loan rates.

- Low Fees: Operates with lower overhead costs, enabling reduced or no-fee services.

- Customer Satisfaction: High satisfaction and retention rates due to user-friendly digital platforms.

- Financial Health: Strong capital position, ensuring stability and ability to manage risks.

Strategic Initiatives

Ally Financial's strategic strengths are evident in its dominant auto finance role, backed by enduring dealer relationships and operational history. In 2024, its average yield on new auto loans hit 10.4%, showcasing profitability. This segment's success stems from excellent credit underwriting, boosting loan performance. Application volume increased by 6% year-over-year, indicating strong market demand.

- Strong Dealer Network: Over 22,000 active dealers.

- High Yield on Loans: 10.4% on new auto loans in 2024.

- Credit Quality: Strong credit underwriting capabilities.

- Application Growth: 6% year-over-year increase in application volume.

Ally's 2024: Digital, Auto, and Record-Breaking Performance

Ally Financial's digital focus fosters customer satisfaction with 89% rating in Q3 2024, coupled with a 95% retention rate. Auto finance shines through a network of 22,000+ dealers; in 2024, new auto loans had a yield of 10.4%. Diversified offerings like insurance achieved record premiums in Q4 2024.

| Strength | Details | 2024 Data |

|---|---|---|

| Digital Presence | User-friendly platforms drive high customer satisfaction. | 89% Customer Satisfaction (Q3) |

| Auto Finance | Robust dealer network, strong loan yields. | 10.4% Avg. Yield (New Loans) |

| Diversified Products | Wide range including insurance and investment services. | Record Insurance Premiums (Q4) |

Weaknesses

Sensitivity to Interest Rate Fluctuations

Ally Financial faces a key weakness: sensitivity to interest rate fluctuations. Its net interest margin (NIM) is vulnerable due to its balance sheet structure. In 2024, Ally's NIM decreased by 6 basis points year-over-year, reaching 3.27%. Rising interest rates can increase funding costs, impacting profitability.

Exposure to Cyclical Auto Industry

Ally's heavy focus on auto financing exposes it to industry cycles. Economic downturns can slash loan demand and boost defaults. In 2024, auto loan delinquencies rose, signaling potential challenges. The company's financial health directly correlates with the auto market's stability, as demonstrated by recent fluctuations in used car prices.

Challenges in Retail Auto Credit Quality

Ally Financial faces challenges in its retail auto credit quality. Delinquencies and net charge-offs (NCOs) are rising, signaling potential loan issues. Rising credit costs and falling used-car prices are impacting collateral value. In Q4 2023, Ally's net charge-off rate for auto loans was 1.85%, up from 1.17% the prior year. Continued trends may force Ally to increase loan loss reserves, affecting profitability.

Dependence on Wholesale Funding

Ally Financial's reliance on wholesale funding exposes it to interest rate risk. The company's net interest margin (NIM) is vulnerable to interest rate fluctuations, impacting profitability. In 2024, the NIM decreased by 6 basis points year-over-year to 3.27%, due to rising funding costs. This sensitivity can squeeze profits when rates climb.

- Interest rate sensitivity impacts profitability.

- NIM compression in 2024: 6 basis points.

- NIM in 2024: 3.27%.

Smaller Asset Base Compared to Major Banks

Ally Financial's smaller asset base compared to major banks exposes it to concentrated risks, especially in the auto finance sector. This concentration makes Ally vulnerable to economic downturns, which can reduce auto loan demand and increase defaults. The company's performance is closely linked to the auto market's health, with cyclical downturns directly impacting profitability. In 2024, Ally's auto loan originations were approximately $12.5 billion, signaling this dependency.

- Reliance on auto finance creates vulnerability.

- Economic downturns can hurt asset quality.

- Performance is tied to the auto market.

- 2024 originations were around $12.5B.

Navigating Headwinds: Financial Challenges

Ally Financial faces challenges from rising interest rates and a reliance on auto financing. Its profitability is affected by interest rate sensitivity. The auto market's health significantly impacts its financial performance.

| Issue | Impact | 2024 Data |

|---|---|---|

| Interest Rate Sensitivity | Reduced profitability | NIM down 6 bps to 3.27% |

| Auto Loan Concentration | Higher delinquency rates | NCO rate up to 1.85% in Q4 2023 |

| Funding Model | Exposure to market risks | 2024 auto loan originations ~$12.5B |

Opportunities

Growth in Digital Financial Services Market

Ally Financial can capitalize on the growing digital banking market. Their existing digital platform is well-positioned to attract new customers. In 2024, digital banking adoption grew, with over 60% of Americans using online banking regularly. Enhanced digital services can boost customer loyalty. Ally's focus on digital innovation aligns well with market trends.

Strategic Partnerships in Auto Finance

Ally Financial could forge strategic partnerships within auto finance to broaden its scope and improve services. Collaborations with entities like Carvana could unlock new customer bases and financing options. Such alliances can boost auto loan originations and market share. In Q4 2023, Ally's auto loan originations were $9.8 billion, showing growth potential through partnerships.

Expansion of Consumer Banking Products

Ally Financial can expand consumer banking products to boost customer relationships and revenue. Offering personal loans, wealth management (Ally Invest), and better credit cards can attract customers. This diversifies revenue, lessening dependence on auto finance. In 2024, Ally's consumer banking segment saw growth, indicating potential for further expansion in services.

Potential for Margin Expansion in Improving Rate Environment

Ally Financial stands to benefit from a rising interest rate environment, potentially widening its net interest margin. This is because the company can earn more on its interest-earning assets while managing its funding costs effectively. Increased margins would lead to higher profitability and improved financial performance. In 2024, the Federal Reserve held rates steady, impacting financial institutions' margins.

- Net interest margin is a key indicator of profitability.

- Rising rates typically benefit lenders.

- Ally's efficiency in managing costs is crucial.

- Rate hikes can boost Ally's earnings.

Electric Vehicle (EV) Financing

Ally Financial has an opportunity in EV financing by forming partnerships. Collaborating with entities like Carvana can bring in new customers and innovative financing. These alliances could boost auto loan originations and market share. In Q4 2023, Ally's auto loan originations were $10.6 billion. Strategic partnerships are key for growth.

- Partnerships for EV financing can boost Ally's market share.

- Collaborations offer access to new customer segments.

- Innovative financing solutions can be a key differentiator.

- Auto loan originations are vital for revenue growth.

Ally's Digital Banking & Growth Strategies

Ally can expand digital services given high digital banking adoption. Ally should grow via partnerships and broaden products. A rising rate environment and EV financing can drive margins and growth.

| Opportunity | Details | Supporting Data (2024) |

|---|---|---|

| Digital Banking Expansion | Capitalize on digital market growth via user-friendly platforms. | Digital banking users: over 60% of Americans. |

| Strategic Partnerships | Form alliances for market share gains and finance options. | Q4 Auto loan originations: $9.8B. |

| Product Diversification | Boost customer engagement with more services. | Consumer banking segment: saw growth. |

| Benefit from Interest Rates | Widen net interest margin in a favorable rate scenario. | Federal Reserve: held rates steady. |

| EV Financing Alliances | Tap into EV sector with strategic partnerships | Q4 Auto loan originations: $10.6B |

Threats

Intense Competition in Digital Banking Sector

Ally Financial faces fierce competition in digital banking. Many banks, fintechs, and credit unions compete for customers. This rivalry can squeeze Ally's profits and raise acquisition costs. To stay ahead, Ally must constantly innovate. In Q3 2023, Ally's net interest margin decreased to 3.33%, reflecting these pressures.

Regulatory Changes Affecting Financial Services Industry

Regulatory changes pose a significant threat to Ally Financial. Stricter regulations, like those from the CFPB, can increase compliance costs. In 2024, the financial sector faced increased scrutiny. Adapting to these changes is essential for maintaining profitability. Higher capital requirements can also limit business activities.

Economic Downturns Impacting Credit Quality

Economic downturns pose a threat by potentially increasing unemployment and decreasing consumer spending, which adversely affects the credit quality of Ally Financial's loan portfolio. This can result in higher delinquency rates and loan losses, thereby eroding profitability and capital. Proactive risk management and stricter underwriting are crucial to mitigate these risks. For example, in 2024, the US unemployment rate hovered around 3.7%, showing economic instability.

Technological Disruptions in Auto Finance and Banking

Technological disruptions pose a significant threat to Ally Financial. The digital banking landscape is crowded, intensifying competition for market share. This competition, including fintechs and credit unions, can squeeze Ally's profits and increase acquisition costs. Continuous tech investment and customer service improvements are crucial to staying ahead.

- In 2024, fintech funding reached $23.8 billion, signaling robust competition.

- Ally's net financing revenue decreased by 13% in Q1 2024 due to competitive pressures.

- Digital banking users grew by 15% in 2024, highlighting the need for innovation.

Cybersecurity Risks

Cybersecurity threats pose a significant risk to Ally Financial, potentially leading to data breaches, financial losses, and reputational damage. Increased sophistication of cyberattacks necessitates continuous investment in cybersecurity measures to protect customer data and financial systems. Any successful breach could trigger regulatory penalties, legal liabilities, and erode customer trust, negatively affecting Ally's financial performance. The financial services industry is a prime target, with cybercrime costs projected to reach $10.5 trillion annually by 2025.

- Data breaches can lead to significant financial losses and legal liabilities.

- Cyberattacks are becoming increasingly sophisticated.

- Regulatory penalties and reputational damage can result from security failures.

- The financial services sector is a major target for cybercrime.

Digital Banking's Triple Threat: Competition, Economy, and Cybercrime

Ally faces stiff competition, pressuring profits and necessitating continuous innovation in a crowded digital banking space. Economic downturns and unemployment hikes pose credit quality risks, potentially increasing loan losses. Cybersecurity threats, with projected costs of $10.5 trillion by 2025, demand robust defenses against data breaches.

| Threat | Impact | Data Point (2024) |

|---|---|---|

| Competitive Pressure | Margin squeeze & higher acquisition costs. | Fintech funding reached $23.8B |

| Economic Downturn | Increased loan losses | US unemployment ~3.7% |

| Cybersecurity Threats | Data breaches, financial losses | Cybercrime costs up to $10.5T by 2025 |

SWOT Analysis Data Sources

This analysis draws upon dependable data sources: financial filings, market research, and expert evaluations to ensure a precise and informed Ally assessment.