Santander Consumer USA Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Santander Consumer USA Bundle

What is included in the product

A comprehensive, pre-written business model tailored to Santander Consumer USA's strategy.

Condenses company strategy into a digestible format for quick review.

Full Document Unlocks After Purchase

Business Model Canvas

This is a direct preview of the Santander Consumer USA Business Model Canvas. The entire document, including all sections and details, is exactly what you will receive. Purchase grants immediate access to the full, ready-to-use file, as shown. This means no content changes and the same professional layout.

Business Model Canvas Template

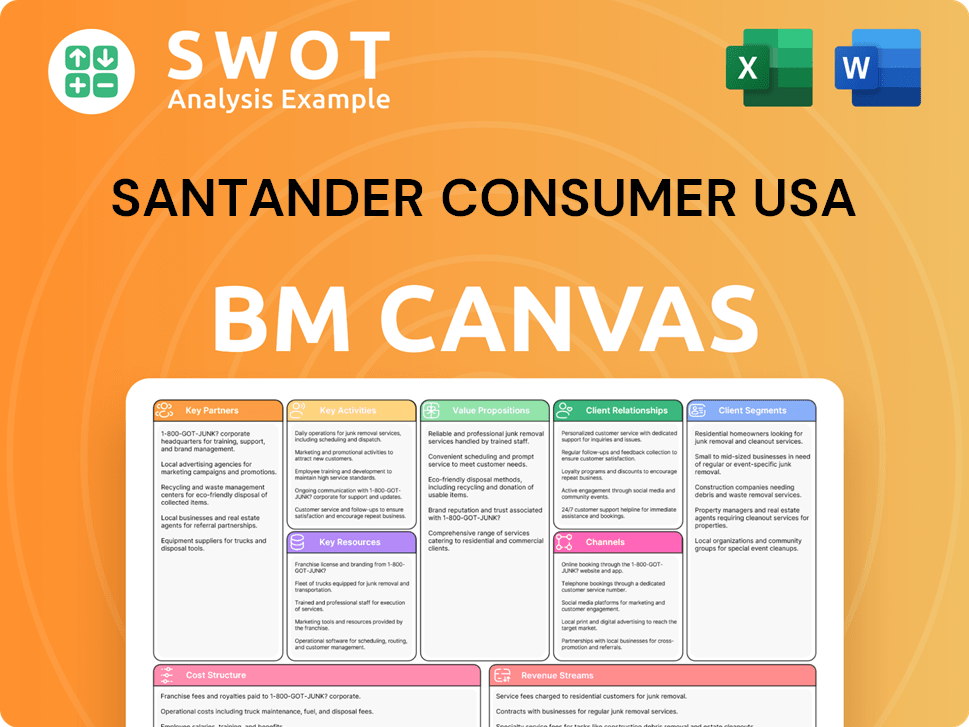

SCUSA: Unveiling the Business Model Canvas

Discover the inner workings of Santander Consumer USA with our Business Model Canvas. This powerful tool unveils their customer segments, value propositions, and revenue streams. Understand their key activities, resources, and partnerships driving success. Analyze their cost structure and gain strategic insights. The full canvas, in Word and Excel, is ready for your analysis.

Partnerships

Auto Dealership Networks

Santander Consumer USA (SCUSA) depends on auto dealerships to generate retail installment loans for cars. Dealerships act as a key link to customers needing vehicle financing. In 2024, SCUSA's loan originations through dealerships were significant. Strong dealer ties are thus vital for SCUSA's business model, influencing its financial performance.

Vehicle Manufacturers

Santander Consumer USA (SCUSA) partners with vehicle manufacturers to provide financing solutions to customers. These collaborations, potentially through private label financing, help SCUSA gain a competitive edge and reach more customers. In 2024, such partnerships facilitated a significant portion of SCUSA's auto loan originations. These agreements often involve preferred provider status, streamlining financing processes for both the manufacturer and SCUSA.

Servicing Partners

Santander Consumer USA (SCUSA) collaborates with third parties to manage loan portfolios, boosting revenue through servicing. These partnerships are essential for SCUSA's growth in loan management. In 2024, SCUSA serviced over $65 billion in loans for others. Servicing partnerships provided nearly $300 million in revenue in 2024.

Technology Providers

Santander Consumer USA (SCUSA) heavily relies on technology providers to support its digital operations. These partnerships are crucial for SCUSA's online platforms and loan processes. In 2024, SCUSA spent approximately $100 million on technology and digital initiatives. These providers help SCUSA stay competitive in the fintech space.

- Enhance digital platforms

- Streamline loan processes

- Improve customer experience

- Maintain competitive edge

Community Organizations

Santander Consumer USA (SCUSA) collaborates with community organizations, including City Year Dallas and Dallas College, to boost local social and economic growth. This aligns with SCUSA's corporate social responsibility, enhancing its community-focused image. These partnerships emphasize education, financial literacy, and workforce preparation. In 2024, SCUSA invested $1.5 million in community programs. These collaborations are vital for SCUSA's brand reputation.

- SCUSA's community investments totaled $1.5 million in 2024.

- Partnerships include City Year Dallas and Dallas College.

- Focus areas: education, financial literacy, and workforce readiness.

- These initiatives support SCUSA's CSR goals.

Strategic Alliances Fueling $65B+ in Auto Loan Servicing

Santander Consumer USA (SCUSA) relies on auto dealerships, manufacturer partnerships, and third-party loan servicing firms. These strategic alliances drive loan originations and manage portfolios effectively. In 2024, these partnerships supported over $65 billion in loan servicing. Technology providers and community organizations also play crucial roles.

| Partnership Type | Description | 2024 Impact |

|---|---|---|

| Dealerships | Generate retail installment loans. | Significant loan originations. |

| Manufacturers | Provide financing solutions. | Facilitated loan originations. |

| Servicing Partners | Manage loan portfolios. | Serviced over $65B in loans. |

Activities

Loan Origination

Loan origination is SCUSA's primary activity, focusing on retail installment loans for vehicles. They assess credit risk and structure loan terms, ensuring regulatory compliance. SCUSA's efficiency in loan origination directly impacts revenue and profitability. In 2024, SCUSA originated approximately $10 billion in new loans.

Loan Purchasing

Santander Consumer USA (SCUSA) strategically buys retail installment loans from other firms. This tactic helps SCUSA grow its loan portfolio and manage its risk. In 2024, this approach supported SCUSA's financial expansion. Strategic loan purchases enhance SCUSA's profitability.

Loan Servicing

Loan servicing is a core activity for Santander Consumer USA (SCUSA). They manage retail installment loans, including those they originate, purchase, or service for others. SCUSA's servicing involves collecting payments, handling delinquent accounts, and offering customer service. In 2024, SCUSA managed a portfolio of approximately $60 billion in loans. Effective loan servicing is crucial for SCUSA to reduce losses and ensure customer satisfaction.

Risk Management

Risk management is a cornerstone for Santander Consumer USA (SCUSA), given its financial services focus. SCUSA actively manages credit risk, which is the potential for losses from borrowers failing to repay loans. Compliance risk is addressed through adherence to regulations, and operational risk is managed to ensure smooth business processes. Effective risk management is crucial for SCUSA's financial health and long-term viability.

- In 2024, SCUSA's allowance for credit losses was a significant portion of its loan portfolio.

- The company's risk management framework includes regular stress tests to assess its resilience.

- Compliance with consumer finance regulations is a key focus area.

- Operational risk is mitigated through internal controls and audits.

Technology Development

Santander Consumer USA (SCUSA) prioritizes technology development to maintain its competitive edge. This involves continuous investment in its digital infrastructure, including online platforms and loan processing systems. Technology upgrades are crucial for improving customer service and operational efficiency. SCUSA's tech investments support loan origination and servicing.

- In 2024, SCUSA allocated a significant portion of its budget to technology upgrades.

- SCUSA's online platform saw a 15% increase in user engagement in 2024 after the latest updates.

- Customer service tools were updated to reduce average call times by 10% in 2024.

- Loan origination systems processed 20% more applications in 2024.

SCUSA's Core: Loans, Tech, and Growth

SCUSA's key activities center on loan origination, strategic loan purchases, and robust loan servicing, driving revenue generation and portfolio growth. Risk management is a crucial activity, encompassing credit, compliance, and operational risk mitigation. Technology investments are ongoing to enhance customer service and streamline operations.

| Key Activities | 2024 Data Highlights | Impact on SCUSA |

|---|---|---|

| Loan Origination | $10B in new loans originated | Revenue generation and portfolio growth |

| Loan Servicing | $60B loan portfolio managed | Reduced losses and improved customer satisfaction |

| Technology Development | 15% increase in online platform engagement | Enhanced customer service & operational efficiency |

Resources

Loan Portfolio

Santander Consumer USA (SCUSA) heavily relies on its loan portfolio, primarily composed of retail installment loans for vehicles, as its core asset. This portfolio's magnitude and caliber directly influence SCUSA's financial performance, with interest income being a key revenue driver. In 2024, the total loan portfolio was approximately $50 billion. Managing this portfolio effectively, which included a 1.5% net charge-off rate in 2024, is vital for boosting returns and mitigating potential losses.

Technology Platform

Santander Consumer USA (SCUSA) relies heavily on its technology platform. This platform, featuring online portals and loan management systems, is crucial for operations. It streamlines loan origination, servicing, and portfolio management. In 2024, SCUSA's digital channels facilitated a significant portion of its loan activities, enhancing efficiency. A strong platform improves customer experience.

Data Analytics Capabilities

Santander Consumer USA (SCUSA) leverages data analytics to evaluate credit risk, pinpoint market trends, and boost operational efficiency. Robust data analytics are vital for well-informed decisions and peak performance. These capabilities support risk management, marketing, and customer service. In 2024, SCUSA's data-driven strategies helped manage a $47.7 billion portfolio.

Funding Sources

Santander Consumer USA (SCUSA) relies heavily on stable funding to fuel its lending operations. They tap into various sources like deposits, securitization, and borrowing from their parent, Banco Santander. Efficiently managing these funds is crucial for SCUSA's profitability. Securing cost-effective funding is a key focus for them to maintain a competitive edge in the market.

- In 2024, SCUSA's total assets were around $50 billion.

- Securitization is a major funding tool, with billions raised annually.

- Banco Santander provides significant financial backing.

- SCUSA's funding costs directly impact its net interest margin.

Human Capital

Human capital is a crucial key resource for Santander Consumer USA (SCUSA). The company relies on its employees, including loan officers, servicing representatives, and tech specialists. Their skills and commitment are vital for great service and meeting company objectives. SCUSA invested $22.8 million in employee training in 2023, reflecting its commitment to workforce development.

- Employee expertise and dedication are essential for SCUSA's operations.

- Training is vital for maintaining a skilled workforce.

- SCUSA invested $22.8 million in employee training in 2023.

- The company focuses on developing its human capital.

SCUSA's Resources: Loans, Tech, and Funding

Santander Consumer USA's (SCUSA) key resources are its loan portfolio, tech platform, data analytics, and funding sources. In 2024, the loan portfolio was valued around $50 billion. SCUSA's funding strategy included $5 billion in term asset-backed securities in Q4 2024.

| Key Resource | Description | 2024 Data |

|---|---|---|

| Loan Portfolio | Retail installment loans, primarily for vehicles. | $50B portfolio |

| Technology Platform | Online portals, loan management systems. | Enhanced operational efficiency. |

| Data Analytics | Credit risk assessment, market trend identification. | $47.7B portfolio managed. |

| Funding Sources | Deposits, securitization, Banco Santander. | $5B in term ABS in Q4 2024 |

Value Propositions

Vehicle Financing for a Wide Credit Spectrum

Santander Consumer USA (SCUSA) provides vehicle financing across the credit spectrum, even for subprime borrowers. This strategy lets SCUSA reach a wider customer base, unlike lenders that are more selective. Approximately 30% of SCUSA's originations target subprime customers. This inclusive model draws in customers who might struggle to find financing, helping SCUSA gain market share.

Technology-Driven Convenience

Santander Consumer USA (SCUSA) leverages technology to offer a streamlined experience. Their online platforms and digital tools simplify loan applications, account management, and payments. This tech-focused approach sets them apart in the competitive landscape. In 2024, digital interactions accounted for over 60% of customer engagements, boosting satisfaction.

Third-Party Servicing Expertise

Santander Consumer USA (SCUSA) leverages its loan servicing prowess by offering third-party services. This involves managing loans for other companies, boosting efficiency. In 2024, this generated a stable revenue stream. This attracts those seeking loan management outsourcing. SCUSA's servicing expertise is a valuable asset.

Community Support

Santander Consumer USA (SCUSA) emphasizes community support through charitable contributions and volunteer activities. This commitment boosts SCUSA's brand image and stakeholder relations. Community engagement helps build goodwill and customer loyalty. In 2024, SCUSA allocated $1.5 million to community programs. SCUSA employees volunteered over 10,000 hours.

- Social responsibility enhances reputation.

- Community involvement fosters brand loyalty.

- SCUSA allocated $1.5M to community programs.

- Employees volunteered over 10,000 hours.

Flexible Payment Options

Santander Consumer USA (SCUSA) offers flexible payment options, catering to customer needs. These include online payments and auto-pay for convenience. Such flexibility enhances customer satisfaction, and reduces delinquencies. In 2024, SCUSA processed millions of payments through various channels.

- Online payments are a popular choice for their ease.

- Auto-pay ensures timely payments, reducing late fees.

- Flexible options contribute to higher customer retention rates.

- These methods help SCUSA manage its loan portfolio effectively.

SCUSA: Financing, Tech, and Community

SCUSA's value lies in accessible auto financing, even for subprime borrowers, broadening its market reach.

Technology streamlines loan processes. Over 60% of customer interactions were digital in 2024, boosting satisfaction.

Third-party loan servicing, generating revenue and attracting partners, showcases SCUSA's expertise.

Community involvement enhances brand image; $1.5M and 10,000 volunteer hours in 2024.

Flexible payment options, with millions of payments processed in 2024, improve customer satisfaction.

| Value Proposition | Description | Key Benefit |

|---|---|---|

| Inclusive Financing | Vehicle financing for all credit tiers, including subprime. | Wider customer base and market share. |

| Tech-Driven Experience | Online platforms and digital tools for applications and payments. | Streamlined processes and enhanced customer satisfaction. |

| Loan Servicing | Third-party loan management services. | Stable revenue streams and expertise. |

| Community Engagement | Charitable contributions and volunteer activities. | Enhanced brand image and stakeholder relations. |

| Flexible Payments | Online and auto-pay options. | Convenience and customer satisfaction. |

Customer Relationships

Online Account Management

Santander Consumer USA (SCUSA) offers online account management. This feature allows customers to monitor loan balances, make payments, and manage accounts digitally. In 2024, approximately 70% of SCUSA's customers utilized online or mobile channels for account management. This self-service approach boosts customer convenience and reduces direct service interactions.

Customer Service Support

Santander Consumer USA (SCUSA) provides customer service via phone, email, and online chat. In 2024, SCUSA aimed to resolve 80% of customer inquiries during the first contact, improving customer satisfaction. This support is crucial for addressing issues promptly. Positive customer service builds trust, potentially boosting customer retention rates, which were at 75% in Q4 2024.

Automated Payment Options

Santander Consumer USA (SCUSA) facilitates customer relationships through automated payment options. They encourage auto-pay enrollment, ensuring timely payments and minimizing delinquencies. This strategy boosts efficiency and cuts collection expenses for SCUSA. In 2024, auto-pay adoption likely contributed to improved payment rates.

Financial Literacy Resources

Santander Consumer USA (SCUSA) could offer financial literacy resources, assisting customers in managing finances and making informed borrowing choices. This commitment to customer education can enhance their financial well-being. Financial literacy initiatives may improve customer creditworthiness and decrease defaults. For example, in 2024, the Consumer Financial Protection Bureau (CFPB) emphasized financial education to protect consumers. SCUSA might align with such trends to boost customer trust and responsible lending.

- Financial literacy programs can lead to better repayment rates.

- Improved financial knowledge can reduce the risk of loan defaults.

- Offering educational resources builds customer loyalty.

Payment Assistance Programs

Santander Consumer USA (SCUSA) provides payment assistance to customers. These programs help those facing financial difficulties. Support includes deferrals or modified schedules. This builds loyalty and reduces losses. SCUSA's focus on customer support is vital.

- In 2024, SCUSA's net charge-offs were 3.86%, showing the impact of economic pressures on borrowers.

- Payment deferrals offer crucial short-term relief, potentially preventing defaults and repossession.

- Modified payment schedules help customers manage debt.

- Customer-centric strategies, such as assistance programs, are essential for SCUSA's long-term success.

Digital Tools Drive Customer Engagement

Santander Consumer USA (SCUSA) prioritizes customer relationships through digital tools, aiming for efficient account management. They provide robust customer service via multiple channels to address inquiries promptly. Payment assistance and financial literacy programs further support customers, aligning with industry standards.

| Customer Interaction | Description | 2024 Metrics |

|---|---|---|

| Online Management | Digital tools for account access and payments | 70% of customers used online/mobile |

| Customer Service | Support via phone, email, and chat | 80% inquiries resolved in first contact |

| Payment Assistance | Deferrals, modified schedules | Net charge-offs: 3.86% |

Channels

Auto Dealerships

Auto dealerships are a key channel for Santander Consumer USA (SCUSA), connecting them with car buyers needing financing. Dealerships present SCUSA's loan options directly to customers during the sales process. In 2024, SCUSA's auto loan originations were substantial, reflecting the importance of these partnerships. SCUSA collaborates with thousands of dealerships across the US. Strong dealer relationships are vital for loan volume.

Online Platforms

Santander Consumer USA (SCUSA) leverages its online platforms, including its website and mobile app, for loan applications, account management, and payments. This digital approach broadens its reach and streamlines customer interactions. In 2024, digital transactions significantly increased, representing over 70% of all customer interactions. This shift boosts efficiency and customer convenience.

Third-Party Servicing Agreements

Santander Consumer USA (SCUSA) utilizes third-party servicing agreements to broaden its market presence and manage loan portfolios for others. These agreements enable SCUSA to earn revenue through servicing activities, adding a vital revenue stream. Servicing partnerships help diversify income sources, capitalizing on SCUSA's servicing proficiency. As of 2024, servicing revenue contributes a significant portion to SCUSA's overall earnings.

Call Centers

Santander Consumer USA (SCUSA) utilizes call centers to deliver customer service and support, addressing inquiries and resolving account-related issues. These centers are crucial for maintaining customer satisfaction and operational efficiency. In 2024, SCUSA likely managed thousands of daily customer interactions through these channels. Efficient call center operations are vital for SCUSA's customer service strategy.

- Call centers are used to handle customer inquiries and resolve issues.

- Effective operations are essential for customer satisfaction.

- SCUSA manages thousands of customer interactions daily.

- These channels are a vital part of SCUSA's customer service strategy.

Direct Mail Marketing

Santander Consumer USA (SCUSA) utilizes direct mail marketing to offer targeted loan products. This channel allows SCUSA to precisely reach specific demographics or geographic regions, enhancing the effectiveness of marketing efforts. Direct mail campaigns serve to generate leads and encourage loan applications, contributing to customer acquisition. This strategy is supported by data showing that direct mail boasts a higher response rate compared to digital channels.

- In 2024, direct mail response rates averaged 3-5%, significantly higher than email's 0.1-1%.

- Direct mail campaigns can be highly targeted, with segmentation leading to conversion rate improvements of up to 20%.

- SCUSA can tailor offers based on credit scores and financial profiles, optimizing campaign performance.

- The cost-effectiveness of direct mail is enhanced through data analytics, leading to better ROI.

SCUSA's 2024 Customer Service: Key Channels and Impact

Call centers, crucial for Santander Consumer USA (SCUSA), manage customer inquiries and account issues, vital for customer satisfaction. In 2024, SCUSA's centers likely handled numerous daily interactions, key to its service strategy. Effective operations are essential for maintaining a high level of service and efficiency.

| Channel | Description | 2024 Impact |

|---|---|---|

| Call Centers | Handles customer service and account management. | Processed thousands of daily interactions. |

| Direct Mail | Targets offers to specific demographics. | Response rates of 3-5%, higher than digital. |

| Online Platforms | Facilitates loan applications and account management. | Over 70% of interactions were digital. |

Customer Segments

Subprime Borrowers

A large part of Santander Consumer USA's (SCUSA) business centers on subprime borrowers. SCUSA offers financing to those with less-than-ideal credit. In 2024, subprime auto loan originations hit $120 billion. This market segment can be lucrative, yet it requires strict risk management.

New and Used Car Buyers

Santander Consumer USA (SCUSA) caters to a wide array of customers, including those buying new and used vehicles. This dual approach enhances SCUSA's market reach. In 2024, the used car market saw about 39.4 million sales. SCUSA's focus on both segments provides diverse financing options. This strategy broadens their customer base considerably.

Individuals Seeking Vehicle Financing

Santander Consumer USA (SCUSA) primarily serves individuals needing vehicle financing. This segment includes customers with different credit scores and incomes. In 2024, the auto loan market saw approximately $800 billion in originations. SCUSA's core business is providing diverse financing options to vehicle buyers. The company's portfolio includes loans to both prime and subprime borrowers.

Auto Dealers

Auto dealers are a crucial customer segment for Santander Consumer USA (SCUSA) because they initiate loan origination. SCUSA prioritizes strong dealer relationships to boost loan volume. Dealer satisfaction levels are directly tied to SCUSA's loan performance. Support and value offered to dealers are vital for success.

- SCUSA's auto loan originations in 2024 reached $27.5 billion.

- Dealer network satisfaction scores are closely monitored.

- Over 14,000 dealer relationships support SCUSA's business model.

- Dealer incentives and support programs are frequently updated.

Third-Party Portfolio Owners

Santander Consumer USA (SCUSA) serves third-party portfolio owners. These entities, owning loan portfolios, rely on SCUSA's loan servicing expertise. SCUSA's efficient services generate revenue and diversify its business model. Servicing partnerships are a key revenue stream. In 2024, SCUSA's servicing portfolio included significant third-party assets.

- Servicing partnerships are a key revenue stream for SCUSA.

- SCUSA's efficient services attract third-party portfolio owners.

- In 2024, SCUSA managed a substantial third-party servicing portfolio.

SCUSA's 2024 Auto Loan Snapshot: $27.5 Billion

Santander Consumer USA's (SCUSA) customer base includes subprime borrowers, vehicle buyers, and auto dealers. SCUSA provided around $27.5 billion in auto loan originations in 2024. It also provides services to third-party portfolio owners. Dealer network satisfaction scores are closely monitored.

| Customer Segment | Description | Key Metric (2024) |

|---|---|---|

| Subprime Borrowers | Individuals with less-than-ideal credit. | Subprime auto loan originations: $120 billion |

| Vehicle Buyers | Customers purchasing new and used vehicles. | Used car sales: ~39.4 million |

| Auto Dealers | Dealers initiating loan origination. | SCUSA's auto loan originations: $27.5B |

Cost Structure

Loan Origination Costs

Loan origination costs cover credit checks, processing, and sales commissions. Streamlining these processes can lower expenses. Santander Consumer USA must efficiently manage these costs. In 2024, the industry saw origination costs fluctuate. Controlling these expenses is key to profitability.

Funding Costs

Santander Consumer USA (SCUSA) faces funding costs to fuel its loan operations. These costs include interest paid on deposits and borrowed money. Efficiently managing funding is crucial for profitability. In 2024, SCUSA's interest expense was a significant operational cost, impacting its financial performance.

Loan Servicing Costs

Loan servicing costs cover payment processing, customer service, and collections. Santander Consumer USA must manage these expenses carefully. In 2024, effective servicing helped maintain profitability. Streamlined operations boost customer satisfaction, too.

Provision for Credit Losses

Santander Consumer USA (SCUSA) allocates funds for anticipated credit losses, crucial for its financial health. These provisions are determined by the risk associated with SCUSA's loan portfolio, impacting profitability. Effective risk management and collection strategies are key to reducing these provisions. In 2023, the provision for credit losses at Santander Consumer USA was approximately $1.7 billion.

- Loan Portfolio Risk: Higher-risk loans necessitate larger loss provisions.

- Collection Efforts: Proactive collections decrease potential losses.

- Financial Impact: Provisions directly affect SCUSA's net income.

- Regulatory Compliance: Reserves must meet regulatory standards.

Technology and Infrastructure Costs

Santander Consumer USA (SCUSA) allocates substantial resources to technology and infrastructure, crucial for its operational efficiency. These investments cover software development, data processing, and IT support to maintain a competitive edge. A strong technological foundation is vital for SCUSA's ability to manage its large portfolio and provide customer services effectively. The costs are significant, reflecting the need for sophisticated systems to handle financial transactions and data security.

- In 2023, Santander Consumer USA's technology and communication expenses were approximately $300 million.

- The company's IT infrastructure supports millions of customer accounts.

- SCUSA continuously updates its systems to improve data security.

- Ongoing investments enhance operational efficiency.

SCUSA's Cost Breakdown: Origination, Funding, and Servicing

Santander Consumer USA’s (SCUSA) cost structure encompasses loan origination, funding, and servicing expenses. SCUSA manages credit loss provisions based on risk, impacting profitability. Technology investments, including software and IT support, also significantly contribute to costs. In 2023, technology and communication expenses were approximately $300 million.

| Cost Category | Description | 2024 Impact |

|---|---|---|

| Origination Costs | Credit checks, processing, sales commissions | Industry fluctuations, efficiency focus |

| Funding Costs | Interest on deposits and borrowed funds | Significant impact on financial performance |

| Servicing Costs | Payment processing, customer service | Effective servicing maintains profitability |

Revenue Streams

Interest Income

Santander Consumer USA (SCUSA) primarily generates revenue through interest income from its loan portfolio. Interest rates are determined by borrower credit risk; higher risk means higher rates. In 2024, SCUSA's net interest income was approximately $6.5 billion. Managing risk while maximizing interest income is crucial for profitability.

Servicing Fees

Santander Consumer USA (SCUSA) earns revenue by servicing loans for others. These servicing fees are a percentage of the loan balance. In 2024, this created a stable revenue stream. Servicing agreements offer predictable, recurring income. This helps SCUSA manage finances effectively.

Late Payment Fees

Santander Consumer USA (SCUSA) generates revenue through late payment fees from customers who miss their payment deadlines. These fees contribute to SCUSA's overall revenue streams, offering a supplementary income source. In 2024, late payment fees can represent a notable portion of a lender's revenue, depending on the customer base and payment behavior. SCUSA maintains transparent fee policies to uphold customer trust and regulatory compliance, key for a financial institution.

Securitization Income

Securitization income is a key revenue stream for Santander Consumer USA (SCUSA). SCUSA transforms its loan portfolio into marketable securities sold to investors, generating income. This process also releases capital for new loans. However, it demands careful structuring and regulatory compliance.

- In 2024, SCUSA securitized $9.5 billion in auto loans.

- Securitization contributed approximately 15% to SCUSA's total revenue in 2024.

- SCUSA's securitization activities are subject to stringent regulatory oversight.

- The efficiency of securitization impacts SCUSA's profitability.

Other Fees

Santander Consumer USA (SCUSA) boosts its revenue through various fees. These include origination fees charged to borrowers. Prepayment penalties also contribute to its income stream. These fees support interest and servicing income. They play a role in SCUSA's total profitability.

- Origination fees are charged to customers when a loan is initiated.

- Prepayment penalties are applied if a loan is paid off early.

- Fee income diversifies SCUSA's revenue sources.

- These fees contribute to overall financial health.

SCUSA's Revenue: Loans, Securitization, and Fees

Santander Consumer USA (SCUSA) relies on diverse revenue streams for financial health. Interest income, from loans, is a primary revenue source. Securitization and fees also boost revenue, with securitization accounting for roughly 15% of total revenue in 2024.

| Revenue Stream | Description | 2024 Contribution (approx.) |

|---|---|---|

| Interest Income | Income from loan portfolio | $6.5 billion |

| Servicing Fees | Fees from loan servicing | Stable, recurring |

| Securitization Income | Sale of loan-backed securities | 15% of total revenue |

Business Model Canvas Data Sources

The Canvas is based on financial reports, customer data, and industry benchmarks. These inputs inform each canvas component, guaranteeing precision and reliability.