Santander Consumer USA Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Santander Consumer USA Bundle

What is included in the product

Analyzes Santander Consumer USA's competitive environment, including rivals, buyers, suppliers, and potential threats.

Adapt quickly: Adjust force ratings as the market shifts, keeping analysis relevant.

Full Version Awaits

Santander Consumer USA Porter's Five Forces Analysis

This preview demonstrates the full Santander Consumer USA Porter's Five Forces analysis you'll receive instantly after purchase.

The document breaks down key competitive forces affecting SCUSA's industry, from threat of new entrants to bargaining power of suppliers.

It offers detailed insights, assessing each force's impact on the company's strategic positioning and profitability.

You're getting the same professionally formatted analysis you are previewing—ready for your immediate use.

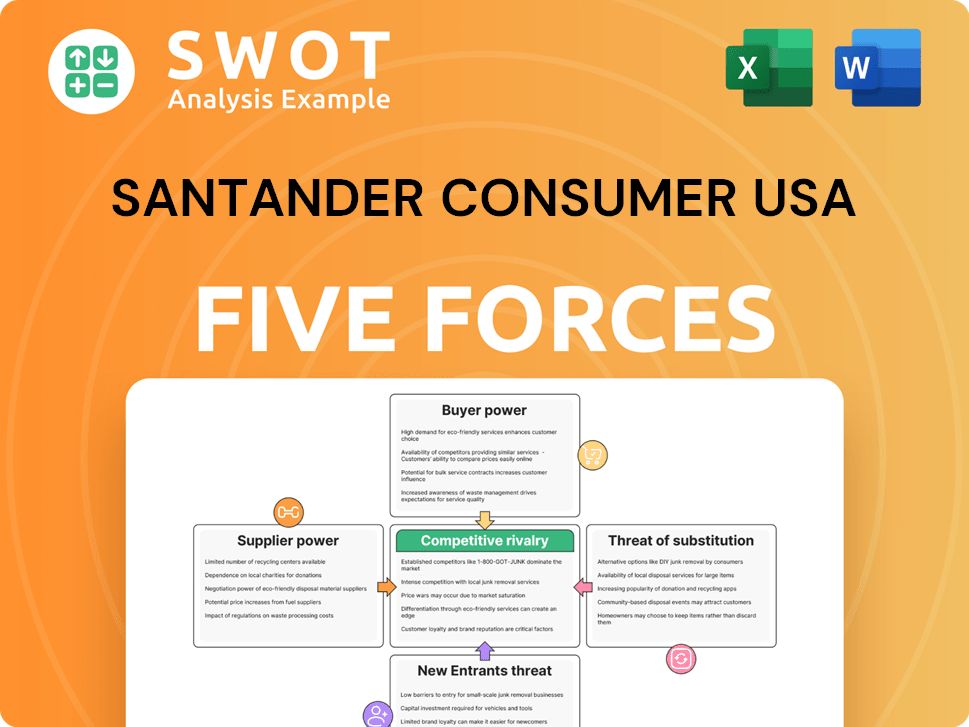

Porter's Five Forces Analysis Template

A Must-Have Tool for Decision-Makers

Analyzing Santander Consumer USA through Porter's Five Forces reveals intense competition in the auto finance sector, squeezing profit margins. Bargaining power of buyers is moderate, driven by readily available financing options. The threat of new entrants is also moderate due to high capital requirements and regulatory hurdles. Substitute products, like leasing, pose a potential challenge. Supplier power, mainly dealerships, is a factor.

Ready to move beyond the basics? Get a full strategic breakdown of Santander Consumer USA’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Supplier power: Moderate

Santander Consumer USA's (SCUSA) supplier power is moderate. SCUSA relies on tech, data, and funding suppliers. Multiple providers for most services keep supplier power in check. SCUSA’s size helps negotiate better terms. In 2024, SCUSA's tech spending was ~$300 million.

Funding sources diversification

Santander Consumer USA (SCUSA) strategically diversifies its funding sources to mitigate supplier power. In 2024, SCUSA employed a mix of securitization and bank credit lines for funding. This strategy reduces dependence on any single lender. For example, SCUSA issued $750 million in auto-loan asset-backed securities in February 2024. Maintaining robust relationships with various financial institutions is crucial for stability.

Data providers competition

Data providers, crucial for Santander Consumer USA's (SCUSA) lending decisions, face competition. This competitive landscape among providers like Experian and TransUnion limits their individual bargaining power. In 2024, these firms vied for SCUSA's business. SCUSA leverages this to negotiate better prices and service terms. For example, SCUSA's cost of data procurement might be influenced by these negotiations.

Technology vendors switching costs

Switching costs for technology vendors at Santander Consumer USA (SCUSA) are manageable. Integrating new systems or migrating data presents complexities and expenses. SCUSA reduces these challenges by thoroughly assessing technology options. This approach guarantees compatibility with their current infrastructure.

- SCUSA's IT budget in 2023 was approximately $200 million.

- Data migration projects often involve costs ranging from $1 million to $10 million.

- Interoperability testing can add 10-20% to total project costs.

- Vendor lock-in is mitigated by using open-source solutions where possible.

Regulatory compliance services

Suppliers of regulatory compliance services hold some bargaining power over Santander Consumer USA (SCUSA). This is because SCUSA must adhere to complex financial regulations. Non-compliance can lead to hefty fines; for example, in 2024, the CFPB issued over $1 billion in penalties. SCUSA must ensure these suppliers are reliable to avoid reputational damage.

- Reputable suppliers are critical for SCUSA's operations.

- Non-compliance penalties can be substantial.

- Reputational damage is a significant risk.

- SCUSA needs to carefully manage these supplier relationships.

Supplier Power Dynamics: A Strategic Overview

Santander Consumer USA (SCUSA) manages supplier power effectively. Tech spending in 2024 was ~$300 million. Funding diversification and competitive data providers help. Compliance suppliers pose a higher risk.

| Supplier Type | Bargaining Power | Mitigation Strategies |

|---|---|---|

| Tech | Moderate | Multiple vendors, ~$300M spend (2024) |

| Funding | Moderate | Securitization, bank lines, $750M ABS (Feb 2024) |

| Data | Low | Competitive market |

| Compliance | High | Reliable suppliers needed; CFPB penalties can exceed $1B (2024) |

Customers Bargaining Power

Customer price sensitivity

Customers in vehicle finance are highly price-sensitive, especially about interest rates and loan terms. Santander Consumer USA (SCUSA) must balance profitability with competitive rates. Economic conditions greatly affect affordability and demand. For example, in 2024, rising interest rates affected loan affordability. SCUSA's success hinges on managing this balance effectively.

Availability of financing options

Customers have many financing choices, like banks, credit unions, and finance firms. This boosts their power since they can quickly switch lenders. In 2024, the auto loan market saw competition with rates fluctuating. SCUSA uses service, flexible loans, and tech. In Q3 2024, Santander's auto loan originations were strong.

Customer credit profiles

Santander Consumer USA (SCUSA) caters to customers with diverse credit profiles, often focusing on subprime borrowers. Customers boasting stronger credit scores wield greater bargaining power, benefiting from a wider array of financing choices. In 2024, the average credit score for new auto loans was 680. SCUSA must adeptly manage credit risk while extending credit access to a broad customer base.

Transparency of loan terms

Increased transparency in loan terms and fees significantly empowers customers, affecting the bargaining power dynamics. Regulations, such as the Truth in Lending Act, mandate clear disclosure of all financing costs. This ensures customers understand the total cost before committing. Santander Consumer USA (SCUSA) must prioritize transparency to build trust and meet legal requirements, which is vital for customer retention.

- The Consumer Financial Protection Bureau (CFPB) actively enforces these regulations, with penalties for non-compliance.

- In 2024, the CFPB issued $1.2 billion in penalties against financial institutions for various violations, including lack of transparency.

- SCUSA's compliance efforts directly impact its ability to attract and retain customers.

- Clear communication about interest rates and fees helps customers make informed decisions.

Customer loyalty programs

While not a standard practice in auto lending, customer loyalty programs can decrease buyer power. Santander Consumer USA (SCUSA) might consider incentives for repeat customers or those with strong payment records. Enhancing customer experience is vital for building loyalty. In 2024, customer retention rates in the auto finance sector averaged around 60%.

- Loyalty programs can incentivize repeat business.

- Enhance customer experience to foster loyalty.

- Customer retention is key in auto finance.

- Consider rewards for good payment history.

Auto Loan Dynamics: Customer Power & Market Shifts

Customers' price sensitivity and financing options boost their bargaining power. Transparency in loan terms, mandated by regulations like the Truth in Lending Act, further empowers them. Customer loyalty programs can partially offset this. In 2024, auto loan rates fluctuated, affecting affordability.

| Aspect | Impact | 2024 Data |

|---|---|---|

| Price Sensitivity | High, affecting rates and terms. | Interest rates influenced affordability. |

| Financing Choices | Many lenders, increasing switching. | Auto loan market saw competitive rates. |

| Transparency | Empowers customers with info. | CFPB issued $1.2B in penalties for non-compliance. |

Rivalry Among Competitors

Intense competition in auto finance

The auto finance sector is fiercely competitive, with many firms battling for dominance. This rivalry significantly impacts pricing and profit margins. Santander Consumer USA (SCUSA) faces competition from banks, credit unions, captive finance arms, and independent lenders. In 2024, the auto loan market saw over $1.6 trillion in outstanding balances, reflecting the scale of competition.

Interest rate competition

Interest rates are a primary competitive factor in the financial sector. Lenders like Santander Consumer USA (SCUSA) constantly adjust rates to lure customers, particularly in the subprime segment. In 2024, the average interest rate on a new car loan was around 7.19%, showcasing the ongoing rate battle. SCUSA must carefully balance its funding costs and risk tolerance to offer attractive rates and remain profitable.

Product differentiation challenges

Differentiating loan products is tough because many lenders provide similar terms. Santander Consumer USA (SCUSA) aims to stand out via tech, service, and special programs. Innovation in loans is key to staying ahead. In 2024, SCUSA's total loan and lease portfolio was $57.5 billion, showing its market presence.

Market share concentration

The market for consumer finance is characterized by a competitive environment, with market share spread among multiple large entities, which fuels aggressive rivalry. Santander Consumer USA (SCUSA) finds itself in a dynamic situation, necessitating continuous evaluation of its competitive position. In 2024, the top five auto lenders held approximately 50% of the market share, underscoring the concentration. SCUSA must adapt its strategies. Monitoring market share and competitor moves is key to strategic decisions.

- The top 5 auto lenders held ~50% of market share in 2024.

- Aggressive competition due to market share distribution.

- SCUSA needs to adjust strategies continually.

- Monitoring competitors is crucial for decisions.

Technological innovation

Technological innovation significantly shapes competitive rivalry in auto finance. Online platforms and digital tools are becoming crucial. Santander Consumer USA (SCUSA) needs tech investments for efficiency and better customer experiences. Digital transformation is key for long-term competitiveness in this evolving market. In 2024, fintech auto loan originations reached $8.6 billion, showing the impact of tech.

- Digital adoption is increasing rapidly.

- Competition from fintech firms is intensifying.

- Investment in tech is essential for survival.

- Customer expectations are driving digital solutions.

Auto Finance: Market Dynamics in 2024

Competition is fierce in auto finance, driving rate adjustments and margin pressure. SCUSA faces rivalry from varied lenders. The top 5 lenders held about 50% of market share in 2024. Tech innovation and digital solutions are key for staying ahead.

| Aspect | Details | 2024 Data |

|---|---|---|

| Market Share | Concentration among top lenders | Top 5 held ~50% |

| Interest Rates | Average new car loan rate | ~7.19% |

| Fintech Impact | Originations through fintech | $8.6B |

SSubstitutes Threaten

Leasing as an alternative

Leasing serves as a notable substitute for traditional vehicle loans, providing an alternative route to acquire a car. This option often boasts lower monthly payments compared to buying, although it doesn't lead to outright ownership. In 2024, approximately 30% of new vehicles were leased, showing its impact. To stay ahead, Santander Consumer USA (SCUSA) needs to deeply grasp the leasing landscape and refine its financial products to stay competitive.

Public transportation and ride-sharing

In urban areas, public transit and ride-sharing substitute for vehicle ownership, impacting auto financing demand. These options, like buses and Uber, decrease the need for traditional car loans. For example, in 2024, ride-sharing use increased by 15% in major cities. SCUSA must track transport trends and adjust strategies, such as offering financing for electric bikes.

Used car market

The used car market poses a threat to Santander Consumer USA (SCUSA) by offering a substitute for new car financing. Used vehicles typically come with lower price tags, resulting in smaller loan amounts. This can attract budget-conscious consumers. In 2024, used car sales in the U.S. are projected to reach approximately 39 million units. SCUSA actively participates in used car financing. This strategy helps SCUSA to offset the potential impact of this substitution.

Car subscriptions services

Car subscription services pose a growing threat to Santander Consumer USA (SCUSA). These services are emerging substitutes, allowing consumers access to vehicles without long-term contracts, offering flexibility and convenience. SCUSA needs to evaluate how these services could affect its auto loan business. In 2024, the car subscription market is estimated to be worth billions, indicating a significant shift in consumer preferences.

- Market value of car subscriptions is in billions of dollars.

- Subscription services offer an alternative to traditional loans.

- Flexibility and convenience are key drivers for consumers.

- SCUSA must adapt its strategy to address this change.

Delayed purchases

Consumers often postpone vehicle purchases, particularly when economic conditions are unfavorable. This shift leads to decreased demand for auto financing, directly impacting companies like Santander Consumer USA (SCUSA). For example, in 2023, new vehicle sales experienced fluctuations due to economic uncertainties. SCUSA needs to proactively manage its loan portfolio and risk exposure during such periods.

- Economic downturns prompt consumers to delay vehicle purchases.

- Reduced demand for auto financing affects SCUSA's revenue.

- SCUSA must mitigate risks associated with economic instability.

- Changes in consumer behavior directly impact the company's financial performance.

SCUSA's 2024: Navigating Substitutes

Substitutes significantly impact Santander Consumer USA (SCUSA). Leasing, used cars, and subscription services provide alternatives to traditional loans. In 2024, understanding these substitutes is crucial for SCUSA's strategic planning.

| Substitute | Impact | 2024 Data |

|---|---|---|

| Leasing | Lower monthly payments | ~30% of new vehicles leased |

| Used Cars | Lower prices | ~39M used car sales projected |

| Subscription | Flexibility | Market in billions |

Entrants Threaten

High capital requirements

The auto finance sector demands hefty capital, serving as a major entry barrier. New firms need significant funds to operate. In 2024, Santander Consumer USA reported over $30 billion in assets. This financial hurdle limits the ease with which new competitors can enter and challenge existing players.

Regulatory hurdles

Regulatory hurdles pose a significant threat to new entrants in the financial industry. Compliance requirements increase operational costs and complexity, making market entry challenging. Santander Consumer USA (SCUSA) benefits from its established compliance infrastructure, creating a barrier. For instance, the average cost of regulatory compliance for financial institutions rose by 7% in 2024. SCUSA's expertise gives it an advantage.

Established brand recognition

Established brand recognition presents a significant barrier for new entrants. Santander Consumer USA (SCUSA), like other established players, benefits from years of building brand awareness and customer loyalty. This strong brand presence allows SCUSA to leverage existing customer relationships. New entrants must overcome the challenge of gaining credibility in a competitive market, requiring substantial marketing investment. In 2024, SCUSA's brand strength helped it maintain a solid position.

Access to dealer networks

Access to dealer networks is vital for auto loan originations, acting as a key barrier for new entrants. Incumbents like Santander Consumer USA benefit from existing, well-established relationships with dealerships. Newcomers face the challenge of building these relationships to effectively compete in the auto loan market. These networks are essential for channeling loan applications and driving business volume, making it a significant hurdle.

- Santander Consumer USA's loan originations in 2024 totaled approximately $18.5 billion.

- Dealer relationships are a major source of loan volume.

- New entrants struggle to match the established networks.

- Building trust and providing competitive rates are key.

Technological capabilities

Advanced technological capabilities are crucial for efficient loan processing and customer service in the financial sector. New entrants face a significant hurdle as they must invest heavily in technology to compete effectively. Santander Consumer USA (SCUSA) has a strong focus on technology, which creates a barrier to entry for less technologically advanced companies. This investment helps SCUSA maintain its market position by streamlining operations and enhancing customer experiences.

- SCUSA's focus on technology provides a barrier to entry.

- New entrants need tech investments to compete.

- Technology streamlines operations and enhances customer experience.

Auto Finance: Barriers to Entry

New auto finance entrants face high capital needs, like Santander's $30B assets in 2024. Regulatory hurdles increase costs, favoring established firms such as SCUSA. Brand recognition and dealer networks also pose challenges.

| Barrier | Impact | SCUSA Advantage |

|---|---|---|

| Capital | High entry cost | Established funds |

| Regulations | Compliance burden | Compliance infrastructure |

| Brand | Building trust | Established loyalty |

Porter's Five Forces Analysis Data Sources

Santander Consumer USA's analysis leverages SEC filings, market research reports, and financial data from reputable sources.