Santander Consumer USA Bundle

How Does Santander Consumer USA Drive the Auto Finance Market?

Santander Consumer USA (SCUSA) is a major player in the auto financing world, providing Santander Consumer USA SWOT Analysis. As a subsidiary of Santander Holdings USA and part of the global Banco Santander, SCUSA offers crucial financial services for vehicle purchases. Their commitment to expanding financing options, including a small business program, demonstrates their dedication to meeting market needs.

With a substantial asset portfolio and a vast dealer network, SCUSA significantly impacts the U.S. auto lending landscape, offering both new and used car loans. The launch of a full-service digital bank by the end of 2025, with an emphasis on Santander auto loans, further highlights their strategic vision. Understanding SCUSA's operations is key for anyone interested in the financial sector, especially concerning auto financing and the dynamics of car loans, including subprime auto loans, and how they navigate the market, including Santander Consumer USA interest rates and the Santander Consumer USA loan application process.

What Are the Key Operations Driving Santander Consumer USA’s Success?

The core operations of Santander Consumer USA (SCUSA) revolve around providing vehicle finance solutions and third-party servicing. SCUSA specializes in originating, purchasing, and servicing retail installment loans for both new and used vehicles, catering to a diverse customer base across the credit spectrum. This includes offering support to small businesses with fewer than ten vehicles through its small business program, expanding its reach and service offerings.

Operational processes are supported by a robust network and technological integration. SCUSA collaborates with approximately 14,000 dealers nationwide to facilitate vehicle financing for a wide range of consumers and businesses. The company's investment in proprietary technology platforms is a key strength, designed to enhance efficiency and improve customer experience. This technological focus is further exemplified by the expansion of Openbank in the U.S., which is set to broaden its product range, including certificates of deposit, payments, and checking accounts in 2025 and beyond. This digital expansion is strategically designed to generate lower-cost, national deposits, which in turn fuel Santander's leading auto lending franchise.

SCUSA's approach to auto financing is unique, combining a full-spectrum lending model with digital banking initiatives. This strategy offers customers a comprehensive suite of vehicle financing options, supported by seamless online experiences and the stability of a global banking institution. Strong partnerships with dealers and importers have helped it maintain a market leader position in auto finance in 2024, despite increased competition. For more insights, explore the Target Market of Santander Consumer USA.

SCUSA primarily originates and services retail installment loans for new and used vehicles. They work with a vast dealer network to provide auto financing solutions. The company also offers third-party servicing for vehicle loans.

SCUSA offers a full-spectrum lending approach, serving a wide range of customers. It combines digital banking with traditional services, providing convenience and stability. Strong dealer relationships and technological advancements enhance customer experience.

SCUSA invests in proprietary technology platforms to boost efficiency. The expansion of Openbank in the U.S. is a key part of its digital strategy. This digital focus aims to attract lower-cost deposits to support auto lending.

SCUSA maintains a leading position in auto finance, despite increasing competition. The company’s strong partnerships with dealers are crucial to its success. They offer a comprehensive suite of vehicle financing options.

Key Operational Highlights

SCUSA's operations are marked by several key features that set it apart in the competitive auto financing market. These include a commitment to technological innovation and a focus on customer service.

- Full-Spectrum Lending: SCUSA provides financing solutions for a wide range of credit profiles.

- Dealer Network: The company partners with approximately 14,000 dealers nationwide.

- Digital Banking Integration: Openbank's expansion enhances digital service offerings.

- Market Leadership: Maintains a strong position in the auto finance sector.

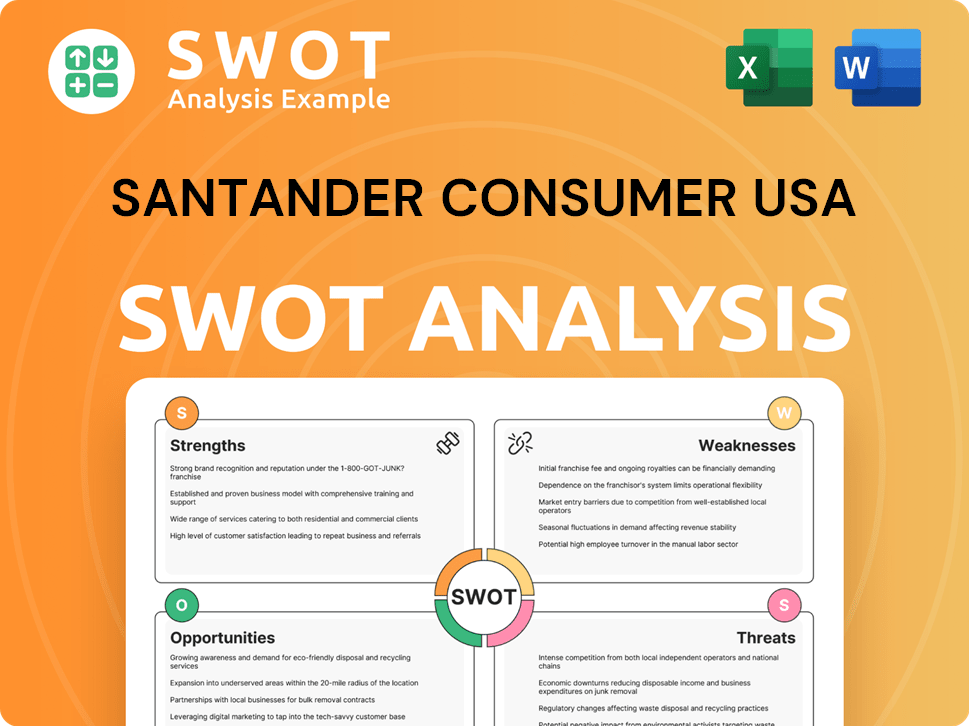

Santander Consumer USA SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Santander Consumer USA Make Money?

Santander Consumer USA (SCUSA) primarily generates revenue through its vehicle finance operations. This involves originating, purchasing, and servicing retail installment loans for new and used vehicles, making Santander auto loans a key revenue driver. The company's financial performance is closely tied to the auto financing market and its ability to manage risk and maintain profitability in its loan portfolio.

SCUSA's monetization strategies extend beyond direct loan interest, including third-party servicing for portfolios owned by other entities. The company also leverages digital banking services through Openbank, aiming to diversify funding sources and attract new customers. This approach supports a broader strategy of profitable growth and capital optimization across its diverse segments.

Banco Santander reported a record attributable profit of €3.4 billion in Q1 2025, a 19% increase year-over-year, with total income increasing 1% to €15.537 billion, driven by record net fee income and customer growth. More than 95% of the Group's total revenue is customer-related, highlighting the quality and recurrence of its results. This financial performance reflects the overall health of the parent company and its impact on subsidiaries like SCUSA.

Key Revenue Streams and Monetization Strategies

SCUSA's revenue streams and monetization strategies are multifaceted, focusing on vehicle finance as the core business. The company's approach includes leveraging various channels to maximize profitability and maintain a strong market position. The expansion of digital banking services through Openbank is an innovative monetization strategy aimed at diversifying funding sources and attracting new customers.

- Vehicle Finance: Originating, purchasing, and servicing retail installment loans for new and used vehicles. This is the primary source of revenue, with interest income from car loans being a significant contributor.

- Third-Party Servicing: Servicing loan portfolios owned by other entities, generating fee income.

- Digital Banking: Utilizing Openbank to generate lower-cost deposits, which can then be used to fund Santander auto loans, creating a synergistic relationship between its deposit-taking and lending activities. In 2024, Santander's digital banking user base in the U.S. grew by 15%.

- Cross-selling Services: Potentially offering insurance products and other services to increase fee-based income, similar to strategies employed by Santander Consumer Finance (SCF) in Europe.

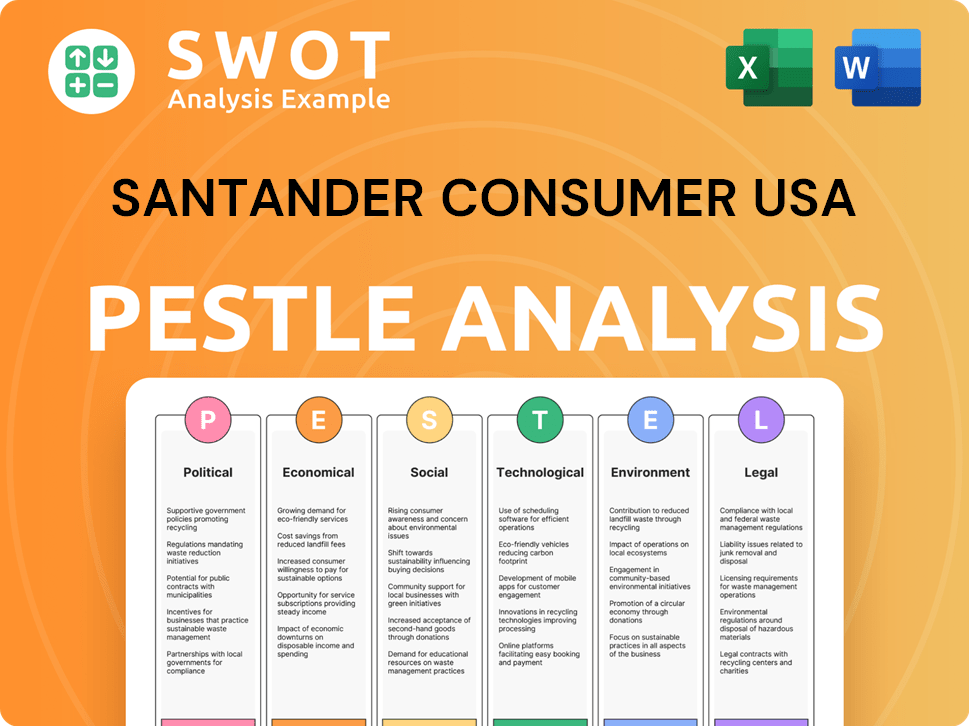

Santander Consumer USA PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Santander Consumer USA’s Business Model?

Santander Consumer USA (SCUSA) has significantly evolved in the auto finance sector, marked by strategic initiatives and key milestones. The company's focus on adapting to market changes and expanding its services highlights its commitment to growth. These efforts, combined with its competitive advantages, position SCUSA for continued success in the auto financing industry.

A key development in September 2024 was the expansion of its small business program, offering comprehensive vehicle financing options to all automotive dealers on its platform. This initiative aims to support businesses with fewer than 10 vehicles in their fleet, addressing a market gap and broadening financing options for entrepreneurs. Another pivotal strategic move is Santander's broader digital transformation, particularly the launch of Openbank in the U.S. in October 2024.

This digital banking platform, which surpassed 100,000 customers within its first six months by May 2025, is designed to generate lower-cost, national deposits to fuel Santander's auto lending franchise and expand its retail banking success. This move reflects a broader commitment to becoming a full-service digital bank in the U.S. by the end of 2025.

SCUSA has achieved several milestones, including the expansion of its small business program in September 2024. The launch of Openbank in the U.S. in October 2024, which quickly gained over 100,000 customers, is another significant achievement. These initiatives reflect SCUSA's commitment to innovation and customer service.

Strategic moves include the expansion of its small business program and the launch of Openbank. These moves aim to broaden financing options and generate lower-cost deposits. The focus on digital transformation and becoming a full-service digital bank by the end of 2025 demonstrates a forward-thinking approach.

SCUSA's competitive advantages include its scale, diversified business model, and technological advancements. Strong brand recognition and the integration of its auto business with the broader Santander US entity further strengthen its market position. The focus on cost-effective funding through deposits enhances its financial resilience.

SCUSA is adapting to market trends, as seen by the fact that 48% of new cars financed by Santander in the Nordics were Battery Electric Vehicles (BEVs) in 2024. This focus on sustainable finance and electric vehicles demonstrates SCUSA's commitment to evolving market demands.

Competitive Advantages and Market Position

SCUSA's competitive advantages are rooted in its scale, diversified business model, and technological advancements. These factors, combined with strong brand recognition and strategic integrations, contribute to a robust market position. The company's focus on generating cost-effective funding through deposits further strengthens its resilience in the auto financing sector. You can learn more about the Growth Strategy of Santander Consumer USA.

- Scale and Diversification: A diversified business model enhances financial stability.

- Technological Advancements: Investments in proprietary tech platforms improve efficiency.

- Brand Recognition: Strong brand recognition, as recognized by Fortune Magazine in 2024, boosts customer trust.

- Strategic Integration: Integration with the broader Santander US entity strengthens market presence.

- Cost-Effective Funding: Focus on generating cost-effective funding through deposits.

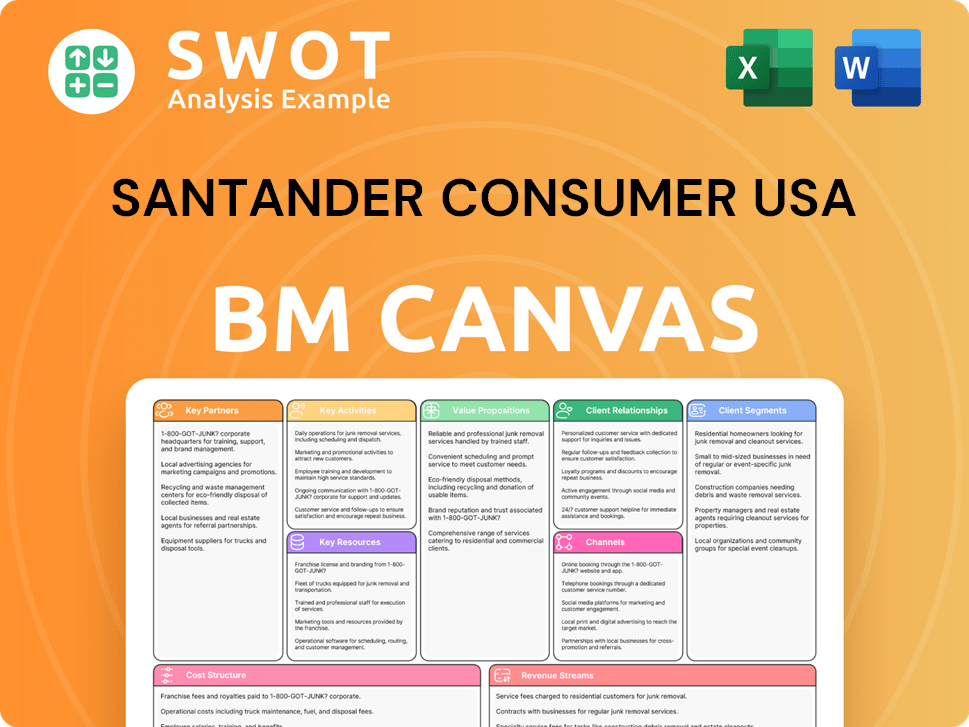

Santander Consumer USA Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Santander Consumer USA Positioning Itself for Continued Success?

Santander Consumer USA (SCUSA) holds a prominent position in the auto finance sector, recognized as a leading and large-scale lender in the U.S. The company's strategic focus on diverse customer segments and strong dealer partnerships contributes significantly to its market share and customer loyalty. SCUSA's combined asset portfolio exceeded $61 billion as of the end of 2023.

Despite its strong market presence, SCUSA faces several risks. These include potential impacts from rising interest rates, regulatory changes, and the cyclical nature of the auto market. Geopolitical risks and macroeconomic uncertainties, such as inflation, could also affect consumer demand and credit quality. Understanding these challenges is crucial for assessing SCUSA's financial health and future prospects.

SCUSA is a leading auto lender in the U.S., managing a combined asset portfolio of over $61 billion as of year-end 2023. The company's focus on diverse customer segments and strong dealer partnerships contributes to its market share. Santander is the fifth-biggest auto lender in the United States.

Key risks include the impact of rising interest rates and regulatory changes. The cyclicality of the auto market and macroeconomic uncertainties, such as inflation, also pose challenges. Potential corporate spending pullback could affect consumer demand and credit quality.

The launch of Openbank in the U.S. by the end of 2025 is a crucial strategic initiative. The company is also focused on leveraging technological advancements, including AI adoption. Santander is targeting a Return on Tangible Equity (RoTE) of greater than 17% and a Common Equity Tier 1 (CET1) ratio of 13% for 2025.

Expansion of the small business vehicle financing program. Launch of Openbank in the U.S. by the end of 2025. Focus on leveraging technological advancements, including AI. Commitment to sustainable finance and ESG initiatives.

Key Financial Targets and Strategies

SCUSA is aiming for significant financial performance improvements driven by geographic diversification, operational efficiency, and disciplined capital allocation. The company's strategic initiatives include expanding digital offerings and incorporating sustainable finance practices.

- Targeting a Return on Tangible Equity (RoTE) of greater than 17% in 2025.

- Aiming for a Common Equity Tier 1 (CET1) ratio of 13% in 2025.

- Focusing on building scale, global network, and local market leadership.

- Continuing to automate businesses and integrate global networks with local banks.

For further insights into the competitive landscape, you can explore the Competitors Landscape of Santander Consumer USA.

Santander Consumer USA Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Santander Consumer USA Company?

- What is Competitive Landscape of Santander Consumer USA Company?

- What is Growth Strategy and Future Prospects of Santander Consumer USA Company?

- What is Sales and Marketing Strategy of Santander Consumer USA Company?

- What is Brief History of Santander Consumer USA Company?

- Who Owns Santander Consumer USA Company?

- What is Customer Demographics and Target Market of Santander Consumer USA Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.