SCB X Public Company Bundle

How Does SCB X Public Company Thrive in the Fintech Revolution?

SCB X Public Company (SCBX) is reshaping the financial landscape, evolving from a traditional bank into a regional fintech powerhouse. With a strategic restructuring completed in 2021, SCBX is aggressively pursuing its vision to become the leading financial technology group in ASEAN. Understanding SCB X Public Company SWOT Analysis is crucial to grasping the company's competitive position and future prospects.

This transformation, driven by a comprehensive digital strategy, has already yielded impressive results, evidenced by SCBX's Q1 2025 financial performance. Delving into SCB X operations reveals a dynamic business model encompassing banking, insurance, and digital financial solutions. Examining SCB X's structure and how it generates revenue is essential for anyone seeking to understand the company's role in Thailand's economy and its ambitious future plans.

What Are the Key Operations Driving SCB X Public Company’s Success?

The core operations of SCB X Public Company are structured around a financial holding company model, designed to provide a wide array of financial products and services. This structure is divided into three key generations: Banking Business (Gen 1), Consumer and Digital Finance Business (Gen 2), and Platform and Technology Business (Gen 3). This multi-generational approach allows SCB X to cater to a broad customer base, from traditional banking clients to those seeking digital-first financial and investment solutions.

The value proposition of SCB X lies in its comprehensive suite of financial services, delivered through a blend of traditional banking and advanced digital platforms. This includes deposit-taking, lending, payments, and wealth management, all supported by a strong emphasis on technology-driven innovation and financial inclusion. The company aims to leverage technology to improve efficiency and expand its reach within the financial sector.

SCB X is committed to digital transformation, as evidenced by its investments in technology and digital platforms across its various business units. The company's focus on fintech and digital solutions positions it to capitalize on the evolving financial landscape, particularly in the context of Thailand's economy. Further insights can be found in an article about Competitors Landscape of SCB X Public Company.

The Banking Business, primarily driven by Siam Commercial Bank (SCB), offers integrated banking services. These include deposit-taking, secured consumer credit, business loans, payments, foreign currency exchange, and wealth management. SCB is modernizing its core banking system, with a pilot project launched at the beginning of 2025, to enhance digital services and efficiency.

This generation includes subsidiaries like CardX (credit cards and personal loans), AutoX (auto title loans), and MONIX and SCB Abacus (digital lending). These entities use AI and machine learning, along with alternative data, to provide accessible financial solutions, especially to underserved segments. AutoX is known for its high loan yield and quick approval process.

This includes InnovestX (integrated investment platform), SCB 10X (venture capital and builder focusing on disruptive tech), Token X (ICO Portal and digital asset solutions), and PointX (loyalty program). SCB TechX and SCB DataX act as accelerators, providing technology and data capabilities across the group. SCB DataX focuses on systematic quality data management and AI integration.

SCB TechX and SCB DataX play crucial roles in providing technology and data capabilities across the group. SCB DataX emphasizes systematic quality data management and the integration of AI to enhance operational efficiency and decision-making. This strategic focus supports SCB X's broader goals of digital transformation and innovation.

Key Highlights of SCB X Operations

SCB X operates a diversified business model across banking, consumer finance, and technology platforms. The company's structure allows it to serve a broad customer base and adapt to changing market dynamics. The focus on digital transformation and fintech solutions positions SCB X for future growth.

- SCB X aims for a long-term cost-to-income ratio of 30%.

- AutoX is known for its rapid loan approval process, often within an hour.

- InnovestX offers an integrated investment platform, enhancing its wealth management services.

- SCB 10X focuses on venture capital and building disruptive technology solutions.

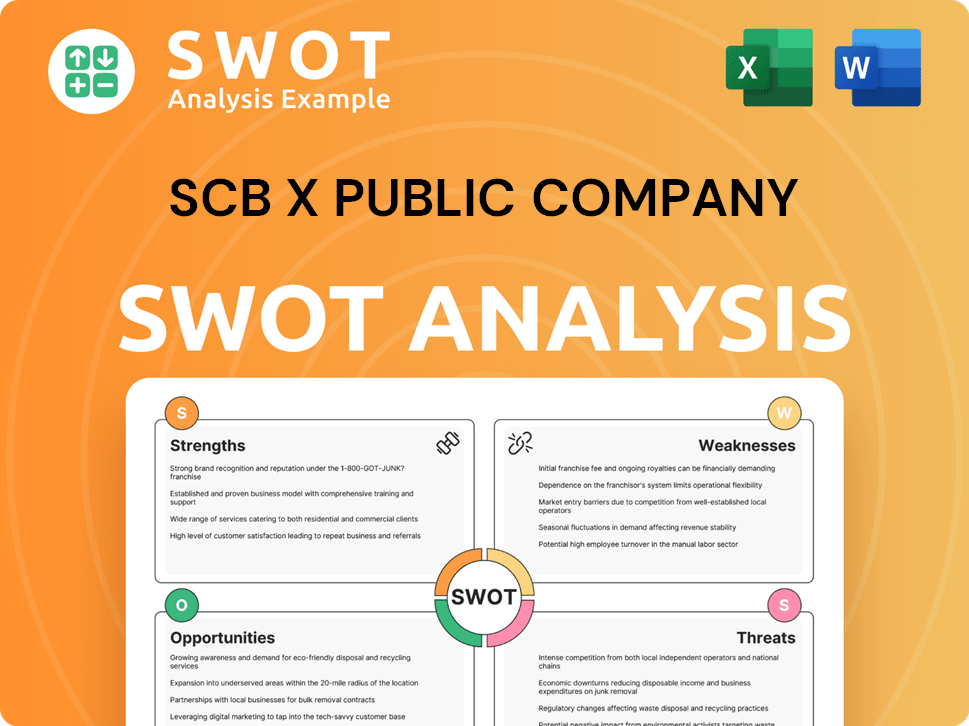

SCB X Public Company SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does SCB X Public Company Make Money?

The revenue streams and monetization strategies of the company, SCB X Public Company, are centered around its diverse financial products and services. These are categorized across its three business generations. The company's financial performance is a key indicator of its success in generating revenue and effectively monetizing its operations.

In Q1 2025, the company reported a consolidated net profit of THB 12.5 billion, marking a 10.8% increase year-on-year. This financial growth reflects the effectiveness of its monetization strategies across various segments.

The company's primary revenue streams include net interest income and fee-based income. While net interest income experienced a slight decrease, fee and other income saw growth, particularly in wealth management. The company is strategically focused on enhancing its digital wealth management offerings to increase fee income.

Key Revenue Components and Strategies

The company's monetization strategies are multifaceted, involving both traditional and innovative approaches. The company's focus on digital transformation is evident in its investment in AI and fintech solutions.

- Net Interest Income (NII): Although NII decreased by 2.2% year-on-year to THB 31.04 billion in Q1 2025, it remains a significant revenue source.

- Fee and Other Income: This segment increased by 0.7% year-on-year to THB 10.25 billion in Q1 2025, driven by growth in wealth management fees.

- Digital Lending: Platforms like MONIX and Abacus Digital contribute to revenue by providing loans to underserved segments.

- Strategic Initiatives: The company is exploring new revenue streams through ClimateTech investments and plans for a virtual bank. The Target Market of SCB X Public Company shows the company's focus on specific customer segments.

- AI Integration: The company aims to generate 75% of its revenue through AI technologies by 2027.

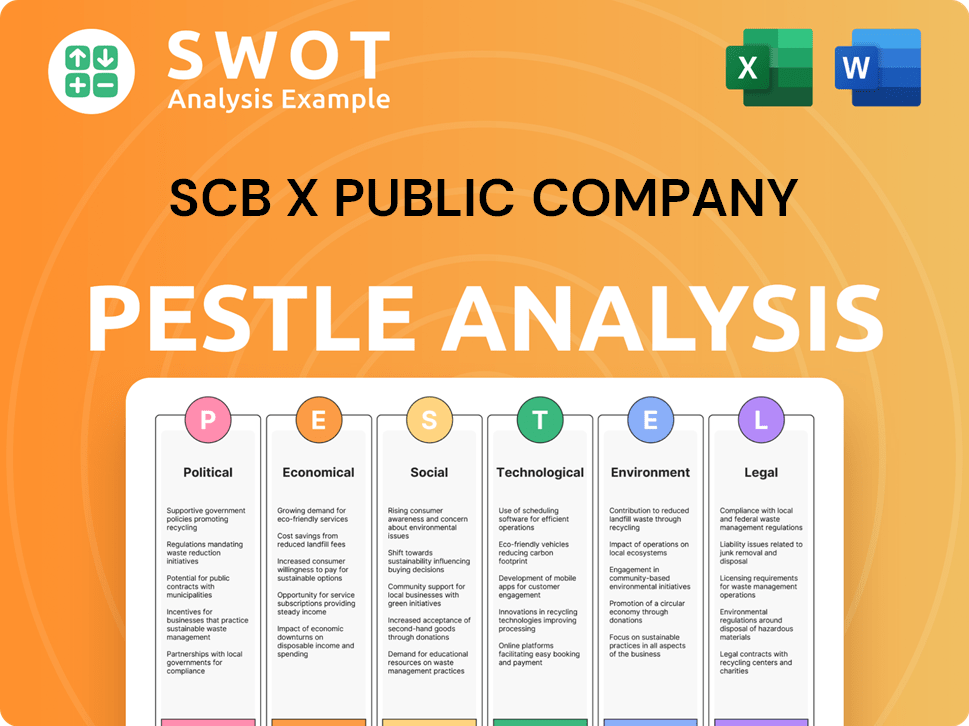

SCB X Public Company PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped SCB X Public Company’s Business Model?

The transformation of SCB X Public Company into a financial holding company on September 15, 2021, was a strategic move designed to enhance competitiveness and long-term business value. This shift has been marked by significant milestones and strategic initiatives, including a strong focus on digital transformation and AI integration. The company's efforts are geared towards maintaining a competitive edge in the financial sector.

A key highlight for SCB X was achieving 'Investment Grade' credit ratings from Moody's (Baa2) and Fitch (BBB) in August 2022, making it the first financial holding company in Thailand to achieve this. This achievement has bolstered confidence in its transformation plan. The company's operations also involve managing various challenges and leveraging its diversified business model.

SCB X Public Company's strategic moves and competitive advantages are centered on its brand strength, a diversified business model, and substantial investments in technology. The company's commitment to innovation and digital transformation, including becoming an 'AI-first Organization,' is a key differentiator. These factors contribute to its ability to personalize services, optimize operations, and gain a competitive edge in the market.

SCB X achieved 'Investment Grade' credit ratings from Moody's (Baa2) and Fitch (BBB) in August 2022. The company launched a pilot project for core banking restructuring in early 2025. The company is focused on reducing the cost-to-income ratio to 30%.

The company aggressively pursued a digital transformation, exemplified by its 'Digital Bank with a Human Touch' strategy. It has implemented prudent new loan underwriting and active non-performing loan (NPL) management. SCB X allocates 5-7% of its annual net profit to R&D.

SCB X's brand strength and diversified business model across three generations are key advantages. The company is committed to becoming an 'AI-first Organization.' It maintains an attractive dividend yield, with an expected THB 10.44 dividend per share for FY24F, implying an 8.5% yield.

Managing asset quality concerns, particularly in the SME and Gen 2 business segments, is a challenge. Navigating potential impacts from global economic shifts, such as US tariff escalations, is also crucial. The NPL ratio was at 3.45% at the end of Q1 2025.

Detailed Analysis of SCB X

SCB X has strategically positioned itself for growth through digital transformation and AI integration. The company's focus on AI and data, supported by subsidiaries like SCB DataX, enhances its ability to personalize services. For more insights, consider reading about the Growth Strategy of SCB X Public Company.

- Digital Transformation: Implementation of 'Digital Bank with a Human Touch' strategy.

- AI Focus: Target of 75% AI-derived revenue by 2027 and complete workforce AI literacy by 2025.

- Financial Performance: Expected THB 10.44 dividend per share for FY24F, implying an 8.5% yield.

- Risk Management: Prudent new loan underwriting and active non-performing loan (NPL) management.

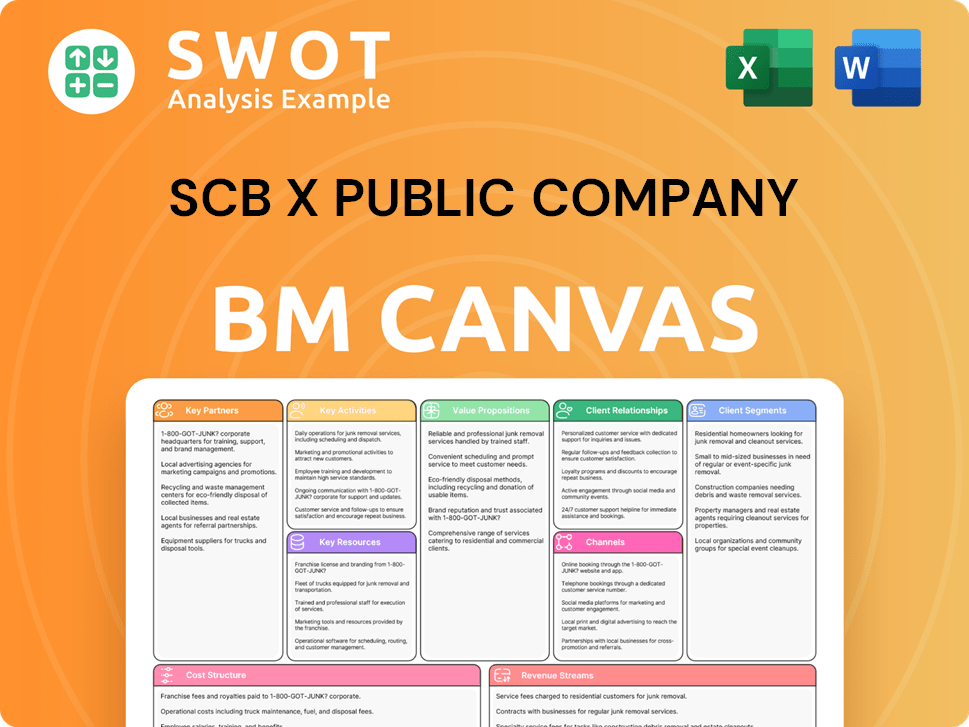

SCB X Public Company Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is SCB X Public Company Positioning Itself for Continued Success?

As a leading financial technology group in Thailand, SCB X Public Company (SCB X) aims to be the 'Most Admired Regional Financial Technology Group in ASEAN.' It held the position of the fourth-largest lender in Thailand based on total loans, deposits, and assets as of the end of 2021. The SCB X structure, changed to a holding company in 2021, has given it more flexibility for growth and investment in fintech and digital platforms.

Despite its strong market position, SCB X operations face several risks, including economic downturns that could affect loan growth and asset quality. Competition from new entrants like virtual banks, expected to launch in mid-2025, and evolving consumer preferences also pose challenges. Concerns about asset quality persist, with a higher NPL ratio noted in 4Q24, and mortgage NPLs at 3.8% in Q1 2025.

SCB X is a major player in Thailand's financial sector, aspiring to be a leading fintech group in ASEAN. Its 'Digital Bank with a Human Touch' strategy, along with its digital offerings, helps foster customer loyalty. The company's global presence extends to Singapore, Myanmar, Hong Kong, China, and Cambodia, supporting its regional ambitions.

The company faces risks such as economic slowdowns affecting loan growth and asset quality, particularly in the SME segment. Competition from virtual banks, expected to begin operations in mid-2025, and regulatory changes also pose challenges. Concerns about asset quality persist, with higher NPL ratios and NPL formation rates noted in recent reports.

SCB X is focused on growth in consumer finance and efficient cost management. Key initiatives include establishing a virtual bank in partnership with KakaoBank Korea and WeBank China. The company is also exploring Climate Tech and aims for Net Zero targets. SCB X is committed to becoming an 'AI-first Organization', targeting 75% AI-derived revenue by 2027.

SCB X plans to sustain and expand profitability by focusing on higher-quality customers and enhancing efficiency through AI. The company aims to leverage its diversified portfolio to capture growth in digital financial services. Management targets a return on equity (ROE) of 13-15% in the next 3-5 years, as detailed in the Growth Strategy of SCB X Public Company.

Key Goals and Strategies

SCB X is focused on becoming an AI-first organization, targeting 75% AI-derived revenue by 2027 and complete workforce AI literacy by 2025. The company is also expanding its digital financial services to capture growth. Management aims for an ROE of 13-15% in the next 3-5 years.

- Focus on consumer finance growth and efficient cost management.

- Establish a virtual bank in partnership with KakaoBank Korea and WeBank China.

- Explore opportunities in Climate Tech and aim for Net Zero targets.

- Leverage AI to enhance efficiency and drive revenue growth.

SCB X Public Company Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of SCB X Public Company Company?

- What is Competitive Landscape of SCB X Public Company Company?

- What is Growth Strategy and Future Prospects of SCB X Public Company Company?

- What is Sales and Marketing Strategy of SCB X Public Company Company?

- What is Brief History of SCB X Public Company Company?

- Who Owns SCB X Public Company Company?

- What is Customer Demographics and Target Market of SCB X Public Company Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.