SVB Bundle

Can First Citizens Bank Revitalize SVB's Legacy?

The acquisition of Silicon Valley Bank (SVB) by First Citizens Bank in 2023 was a seismic event, reshaping the banking industry's landscape. SVB, once a powerhouse in the tech startup ecosystem, now operates under new ownership. This analysis delves into the SVB SWOT Analysis, exploring the strategies driving SVB's future prospects and growth.

Understanding SVB's evolution post-acquisition is crucial for investors and strategists alike. This includes a deep dive into SVB's financial performance, the challenges it faces, and how it plans to navigate banking industry trends. We'll explore SVB's expansion plans in 2024, its market share analysis, and the impact on the tech startup ecosystem to provide a comprehensive SVB Company Analysis.

How Is SVB Expanding Its Reach?

First Citizens Bank is actively pursuing several expansion initiatives, leveraging the integration of SVB to capitalize on new opportunities and diversify its revenue streams. These initiatives are designed to strengthen its market position and enhance its service offerings, particularly in specialized sectors and the innovation economy. The bank's approach includes both organic growth and strategic partnerships, aiming to provide comprehensive financial solutions to a diverse customer base.

A key element of the expansion strategy involves focusing on customer retention and acquisition, alongside entering new markets and introducing new products and services. This multi-faceted approach is intended to drive sustainable growth and increase market share. The acquisition of SVB's assets has significantly enhanced First Citizens Bank's capabilities, especially in serving the technology and life science sectors.

The bank's strategic focus on customer acquisition and retention, alongside expansion into new markets and the introduction of new products and services, is designed to drive sustainable growth and increase market share. The acquisition of SVB's assets has significantly enhanced First Citizens Bank's capabilities, particularly in serving the technology and life science sectors.

In February 2025, First Citizens Bank launched Sixty-First Commercial Finance, a joint venture with Sixth Street. This new platform offers flexible capital equipment financing solutions. These solutions range from $5 million to $100 million, targeting middle-market companies across various equipment asset types and industries.

With over 500 branches and offices across 30 states, First Citizens Bank continues to grow its presence geographically. The bank is also expanding within specialized sectors. This includes a strong focus on the innovation economy, particularly through the integration of SVB's operations.

SVB, a division of First Citizens Bank, is primarily divided into Global Fund Banking and Healthcare and Technology. This strategic alignment allows First Citizens to extend venture debt availability to fast-growing technology and life science companies. This approach enables the bank to provide specialized financial products and services.

In March 2025, SVB announced a strategic lending relationship with Pinegrove Venture Partners. The collaboration aims to deploy a combined $2.5 billion in venture debt loans to technology and life science companies in the coming years. This partnership leverages the expertise of both entities.

Key Expansion Initiatives

First Citizens Bank's expansion strategy focuses on both organic growth and strategic partnerships. The bank aims to enhance its market position and diversify revenue streams. The integration of SVB has been a key factor in these initiatives, particularly in the innovation economy. These initiatives are designed to solidify its position in the banking industry trends.

- Launch of Sixty-First Commercial Finance to provide equipment financing.

- Geographic expansion and focus on specialized sectors.

- Strategic lending relationships to support technology and life science companies.

- Leveraging SVB's expertise in venture debt and specialized banking services.

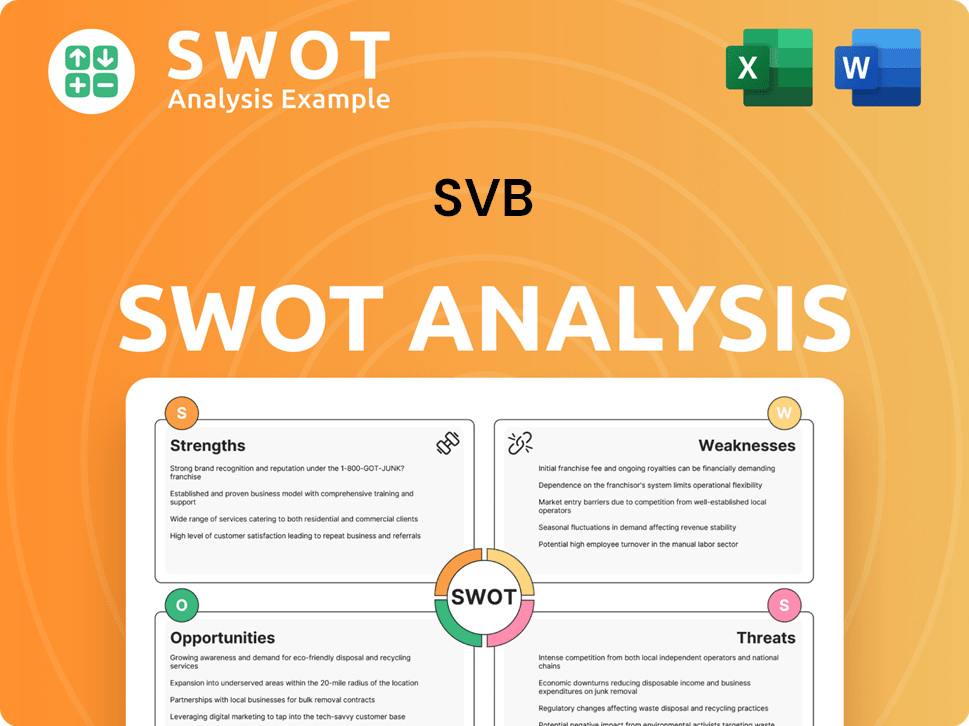

SVB SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does SVB Invest in Innovation?

First Citizens Bank, the parent company, is actively using technology and innovation to foster growth, particularly focusing on digital transformation. This commitment includes significant investments in technological infrastructure, such as mobile banking apps, online financial planning tools, and advanced cybersecurity measures. These initiatives aim to improve customer experience, streamline operations, and enhance security.

The bank's innovation strategy extends to exploring emerging technologies like AI, Machine Learning, IoT, and Blockchain. By integrating these technologies, First Citizens Bank aims to increase operational efficiency and stay ahead of industry trends. The importance of technology is further emphasized by the appointment of a new chief information and operations officer and the addition of board members with senior executive roles at large banks, demonstrating a commitment to robust risk management and governance in the context of technological advancements.

Within the SVB division, there is a specific emphasis on the climate tech sector. The Brief History of SVB highlights the bank's strategic focus on innovation and its ability to adapt to evolving market needs.

Climate Tech Investments

SVB's 'Future of Climate Tech 2025 Report,' released in April 2025, highlights a positive trajectory for the climate tech sector. The report indicates six consecutive months of growth in US climate tech investments, surpassing overall VC investments.

Outperforming VC Investments

Climate tech investments have outperformed overall VC investments, with a 9% higher internal rate of return (IRR) in the 2020-2024 fund vintage. This demonstrates strong financial performance in the climate tech sector.

Focus Areas: Energy, Manufacturing, and Carbon Tech

The report highlights the increasing flow of venture capital into energy, manufacturing, and carbon tech. Clean energy deals reached an all-time high of over $7 billion in 2024, marking a 15% year-over-year increase.

Series B and C+ Rounds

Series B and C+ rounds in climate tech hit decade highs in 2024, with $30 million and $60 million, respectively. This indicates significant contributions to growth objectives through specialized financial services and insights.

AI Dominance

AI continues to dominate funding, with over 50% of all VC deals being AI-related in 2024. This highlights AI as a significant area of focus for the innovation economy.

SVB's Role in Climate Tech

SVB is playing a crucial role in supporting the growth of the climate tech sector through specialized financial services and insights. This strategic focus contributes to SVB's future prospects and overall SVB Growth Strategy.

Key Takeaways

The focus on technology and innovation, particularly in the climate tech sector, is a key component of SVB's strategy. The data from the 'Future of Climate Tech 2025 Report' underscores the potential for continued growth and the importance of specialized financial services in supporting emerging technologies.

- SVB is investing heavily in digital transformation.

- Climate tech investments are outperforming overall VC investments.

- AI continues to be a dominant area for VC funding.

- SVB is providing specialized financial services to support the growth of the climate tech sector.

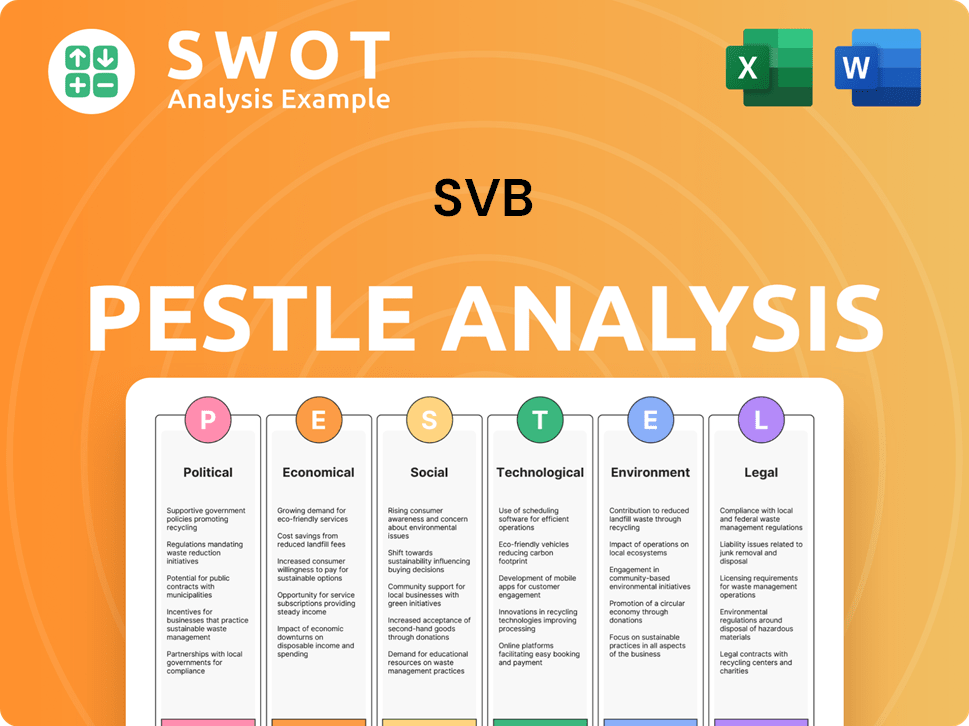

SVB PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is SVB’s Growth Forecast?

First Citizens BancShares, which includes the former SVB, has shown resilience in its financial performance. The company's Q1 2025 results reflect the integration of SVB and its adaptation to the current banking industry trends. This SVB Company Analysis provides insights into its financial health and future prospects.

The financial outlook for First Citizens BancShares, post-acquisition of SVB, reveals both challenges and opportunities. The company's ability to manage its net interest margin and deposit growth will be key to its success. The following analysis details the financial performance and future expectations for the combined entity.

First Citizens BancShares reported a net income of $483 million for Q1 2025, a decrease from $700 million in Q4 2024. Adjusted net income for Q1 2025 was $528 million, with adjusted EPS of $37.79. Revenue for Q1 2025 reached $2.3 billion, exceeding expectations. The company's financial performance is a key aspect of its SVB Financial Performance.

Net income for Q1 2025 was $483 million, down from $700 million in Q4 2024. Revenue reached $2.3 billion, surpassing expectations. Adjusted EPS was $37.79, slightly below forecasts.

Net interest income for Q1 2025 totaled $1.66 billion, a decrease from the previous quarter. The net interest margin was 3.26%, reflecting margin pressure. This impacts SVB's market share analysis.

Total deposits at March 31, 2025, were $159.33 billion, a 10.7% annualized increase since December 31, 2024. Loans and leases totaled $141.36 billion, up 3.3% annualized.

First Citizens BancShares anticipates mid-single-digit loan growth and significant deposit growth in 2025. The forecasted annual revenue for SVB Financial Group is $8.697 billion.

The company's financial health is supported by strong capital and liquidity positions. The CET1 ratio was 12.99% at year-end 2024, well above the target of 10.5-11.0%. First Citizens returned an additional $613 million to stockholders through share repurchases in Q1 2025. Understanding the Mission, Vision & Core Values of SVB can provide further context on its strategic direction.

Revenue Projections

The forecasted annual revenue for 2025 is $8.697 billion. Net interest income is expected to be between $6.55 billion and $6.95 billion for the full year.

Capital and Liquidity

The CET1 ratio was 12.99% at year-end 2024. The company's target CET1 ratio is 10.5-11.0%, indicating a strong capital position.

Loan and Deposit Growth

Mid-single-digit loan growth and significant deposit growth are expected in 2025. Deposit growth was driven by increases in corporate deposits and Direct Bank savings deposits.

Net Interest Margin

The net interest margin was 3.26% in Q1 2025, reflecting margin pressure. This is a key factor in SVB's financial performance.

Shareholder Returns

An additional $613 million of capital was returned to stockholders through share repurchases in Q1 2025. This demonstrates the company's commitment to shareholders.

Adjusted Earnings

Adjusted net income for Q1 2025 was $528 million, with adjusted EPS of $37.79. This provides a clearer picture of the company's profitability.

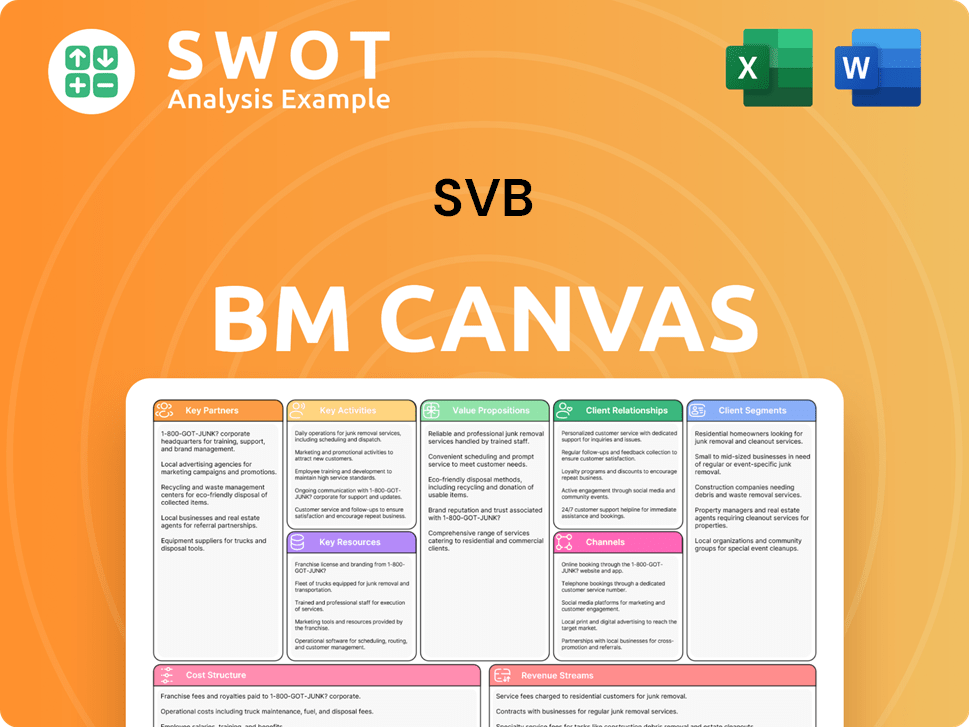

SVB Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow SVB’s Growth?

The future prospects of First Citizens Bank, and its SVB Growth Strategy, are subject to several potential risks and obstacles. These challenges span competitive pressures, regulatory changes, economic uncertainties, and operational risks. Understanding these factors is crucial for assessing the bank's ability to achieve its growth objectives and maintain financial stability. For a deeper dive into the bank's target audience, explore the Target Market of SVB.

Increased competition within the banking industry necessitates continuous innovation and differentiation. Regulatory changes, particularly for a Category IV bank like First Citizens, demand robust risk management and compliance measures. Economic fluctuations, including interest rate movements, can significantly impact loan demand and profitability, requiring strategic adaptation. The SVB Company Analysis must consider these elements.

Operational risks, such as cyberattacks and technology outages, pose a constant threat. These can disrupt business operations and lead to financial and reputational damage. Strategic risks related to acquisitions, a key part of First Citizens' growth strategy, include integration difficulties and increased regulatory scrutiny. The bank's ability to navigate these challenges will be critical to its SVB Financial Performance.

Competition and Differentiation

The banking industry is highly competitive, with both traditional banks and non-bank competitors vying for market share. To succeed, First Citizens must differentiate itself. This includes offering unique products, providing excellent customer service, and investing in advanced digital banking capabilities.

Regulatory Risks

As a Category IV bank, First Citizens faces heightened regulatory scrutiny. Changes in regulations can affect operations and require significant investments in compliance and risk management. The company has been working to enhance its risk management and governance to meet these requirements.

Economic Uncertainty

Economic factors, such as interest rate fluctuations, can significantly impact loan demand and profitability. A potential Federal Reserve pivot to lower interest rates in 2025 could affect net interest income, necessitating strategic adaptation. First Citizens’ management is focused on navigating these economic shifts effectively.

Talent Retention

Retaining skilled employees is crucial in a competitive banking environment. This requires competitive compensation packages, ample career growth opportunities, and a positive work culture. The ability to attract and retain top talent will directly impact First Citizens' ability to execute its strategic plans.

Acquisition Challenges

Acquisitions carry inherent risks, including increased regulatory scrutiny and integration difficulties. Successfully integrating acquired entities is essential for achieving projected growth and profitability. Careful planning and execution are crucial to mitigate these risks.

Operational Risks

Cyberattacks and technology outages can disrupt business operations and lead to significant financial and reputational harm. First Citizens is focused on enhancing cybersecurity measures and improving operational infrastructure. Continuous investment in these areas is critical.

Banking Industry Trends include the rise of digital banking, increasing competition from fintech companies, and evolving customer expectations. The SVB's expansion plans in 2024 and beyond will need to consider these trends. First Citizens must adapt to these trends to remain competitive and meet the changing needs of its customers.

SVB's market share analysis reveals the bank's position relative to its competitors. Understanding market share is crucial for assessing growth potential and identifying areas for improvement. First Citizens' ability to gain or maintain market share will be a key indicator of its success.

First Citizens must continuously adapt to changing regulations to maintain compliance and mitigate risks. This includes investing in compliance programs, enhancing risk management practices, and staying informed about regulatory developments. The bank's proactive approach to regulatory compliance is essential.

SVB's risk management strategies are critical for protecting the bank from potential losses. This includes credit risk management, operational risk management, and market risk management. A robust risk management framework is essential for ensuring the bank's long-term financial stability. The net charge-off (NCO) ratio fell to 39 basis points in 2024 from 55 basis points in the prior year.

SVB Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.